BoC stands pat and maintains interest rate unchanged at 1.25% as widely expected. The most important part of the statement is that “developments since April further reinforce Governing Council’s view that higher interest rates will be warranted to keep inflation near target.” This is more hawkish than generally expected and shows that BoC is rather confident to continue with tightening, even though the timing of the next hike is still uncertain.

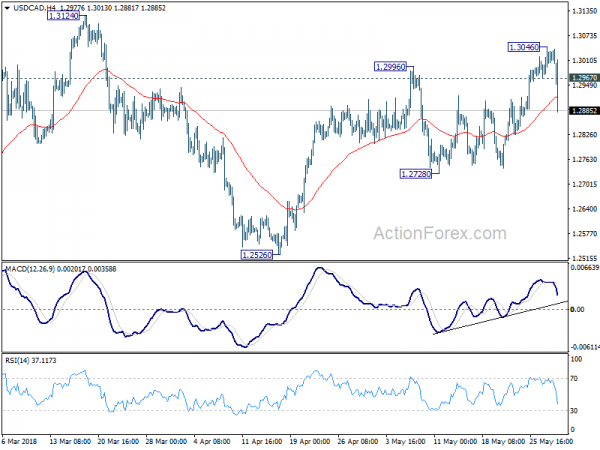

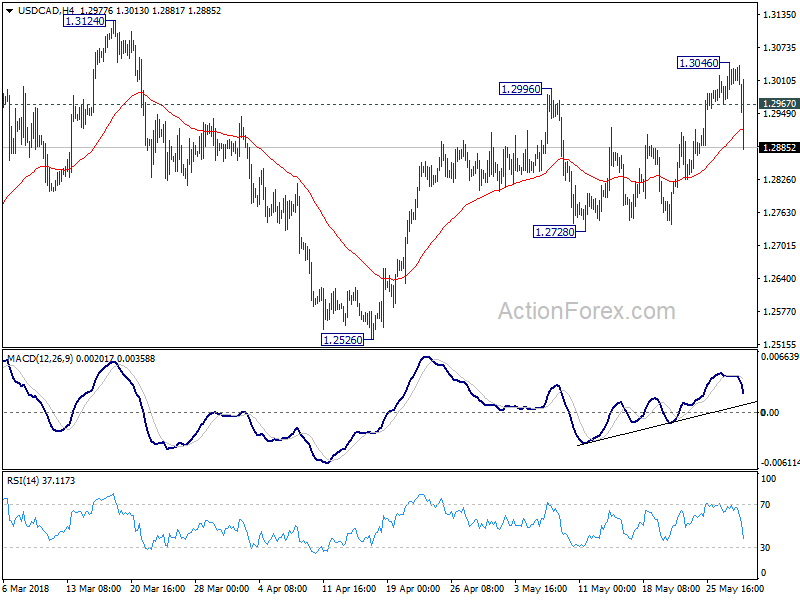

USD/CAD dives sharply after the release and should be heading back to 1.2728 support.

Here is the full statement:

Bank of Canada maintains overnight rate target at 1¼ per cent

The Bank of Canada today maintained its target for the overnight rate at 1¼ per cent. The Bank Rate is correspondingly 1½ per cent and the deposit rate is 1 per cent.

Global economic activity remains broadly on track with the Bank’s April Monetary Policy Report (MPR) forecast. Recent data point to some upside to the outlook for the US economy. At the same time, ongoing uncertainty about trade policies is dampening global business investment and stresses are developing in some emerging market economies. Global oil prices have been higher than assumed in April, in part reflecting geopolitical developments.

Inflation in Canada has been close to the 2 per cent target and will likely be a bit higher in the near term than forecast in April, largely because of recent increases in gasoline prices. Core measures of inflation remain near 2 per cent, consistent with an economy operating close to potential. As usual, the Bank will look through the transitory impact of fluctuations in gasoline prices.

In Canada, economic data since the April MPR have, on balance, supported the Bank’s outlook for growth around 2 per cent in the first half of 2018. Activity in the first quarter appears to have been a little stronger than projected. Exports of goods were more robust than forecast, and data on imports of machinery and equipment suggest continued recovery in investment. Housing resale activity has remained soft into the second quarter, as the housing market continues to adjust to new mortgage guidelines and higher borrowing rates. Going forward, solid labour income growth supports the expectation that housing activity will pick up and consumption will continue to contribute importantly to growth in 2018.

Overall, developments since April further reinforce Governing Council’s view that higher interest rates will be warranted to keep inflation near target. Governing Council will take a gradual approach to policy adjustments, guided by incoming data. In particular, the Bank will continue to assess the economy’s sensitivity to interest rate movements and the evolution of economic capacity.

Information note

The next scheduled date for announcing the overnight rate target is July 11, 2018. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.

Eurozone CPI slowed to 0.1% yoy, ECB Visco warns of prices-demand downward spiral

Eurozone CPI slowed to 0.1% yoy in May, down from 0.3% yoy. That’s also the lowest level in four years. Nevertheless, the slow down was largely driving by -12.0% yoy in energy prices. Excluding energy, CPI was unchanged at 1.4%. CPI ex energy and unprocessed food was unchanged at 1.1% yoy. CPI ex energy, good, alcohol & tobacco was also unchanged at 0.9% yoy.

Separately, ECB Governing Council member Ignazio Visco warned, “steps must be taken to counter the significant risk of low inflation and the marked fall in economic activity from translating into a permanent reduction in expected inflation or into the possible resurfacing of the threat of deflation.”

“Also as a result of the high levels of public and private debt in the euro area as a whole, this could trigger a dangerous spiral between the fall in prices and that in aggregate demand.”