UK Q3 GDP was estimated to have increased by a record 16.0% qoq in Q3, revised up from first estimate of 15.5%. Over the year, GDP dropped -8.6% yoy. The level of GDP was still -8.6% below that at the end of 2019.

UK Q3 GDP was estimated to have increased by a record 16.0% qoq in Q3, revised up from first estimate of 15.5%. Over the year, GDP dropped -8.6% yoy. The level of GDP was still -8.6% below that at the end of 2019.

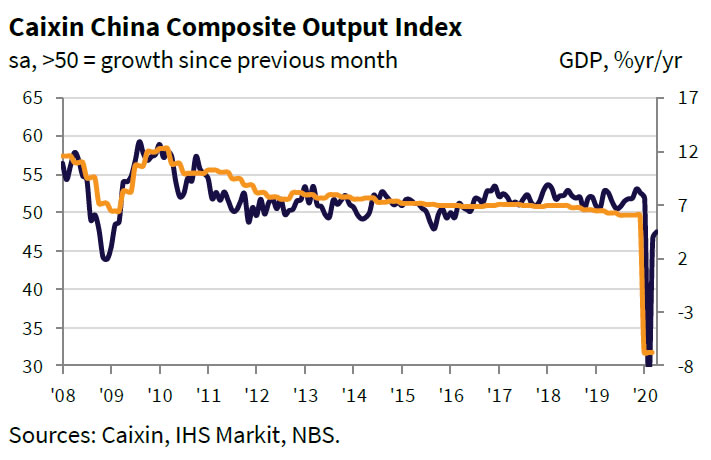

China’s Caixin PMI Services rose to 44.4 in April, up from March’s 43.0. PMI Composite rose to 47.6, up from 46.7. Both stayed in contraction region.

Zhengsheng Zhong, Chairman and Chief Economist at CEBM Group said, “domestic services activity remained under notable pressure amid the coronavirus pandemic”. New export orders shrank at a steeper rate in April than in February, “indicating that the March rebound in exports was not sustainable”. “The second shockwave for China’s economy brought about by shrinking overseas demand should not be underestimated in the second quarter”

Also from China, in April, in USD terms, exports rose 3.5% yoy while imports dropped -14.2% yoy. Trade surplus widened to USD 45.3B.

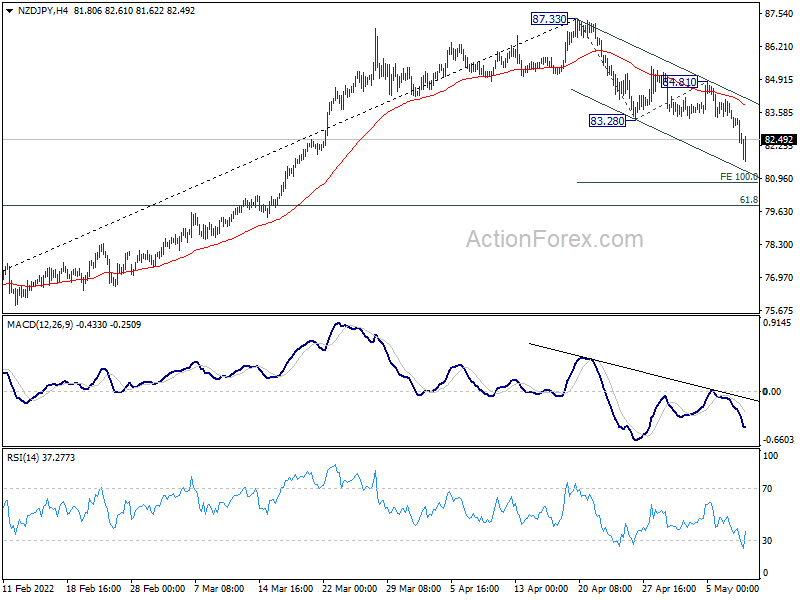

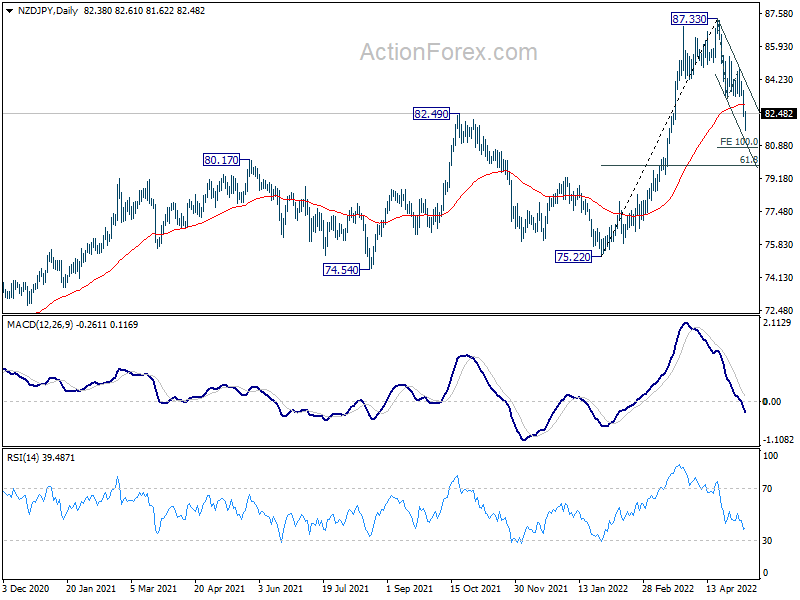

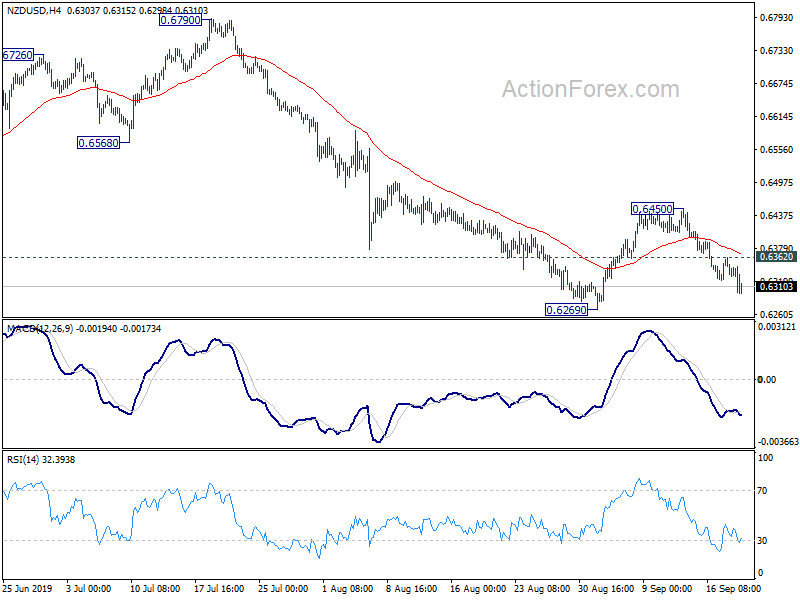

NZD/JPY dived lower this week as risk aversion dominated the markets. It is now extending the fall from 87.33 top towards 100% projection of 87.33 to 83.28 from 84.81 at 80.76. Such decline is currently still seen as a correction only. Hence, strong support is expected from 80.76 to contain downside to bring rebound. But break of 84.81 resistance is still needed to confirm completion of the fall, otherwise, risk will stay on the downside.

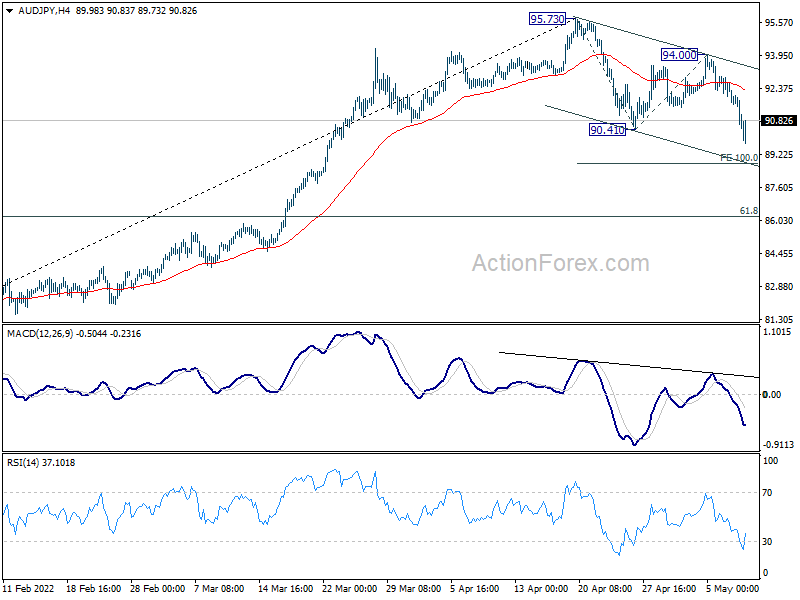

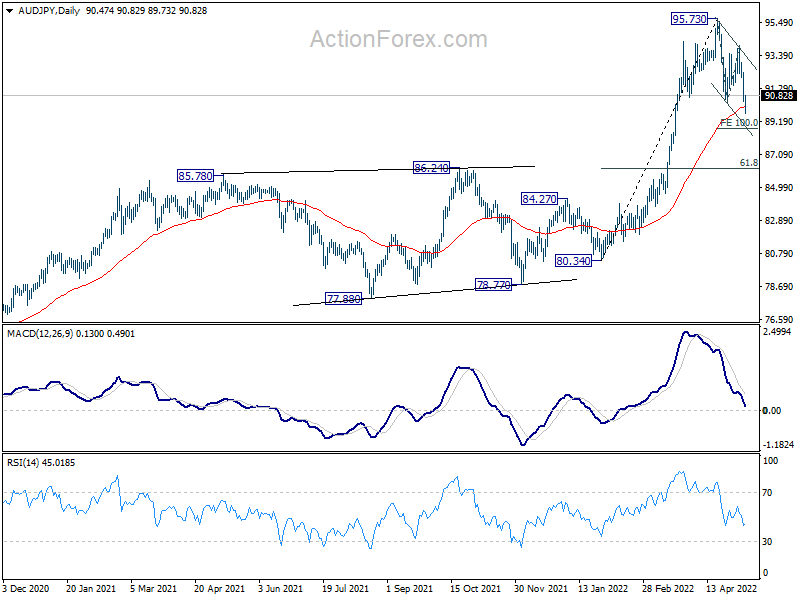

Similarly, AUD/JPY is also extending the fall from 95.73 and should target 100% projection of 95.73 to 90.41 from 94.00 at 88.68. Strong support is expected from this level to complete the correction. But break of 94.00 resistance is needed to confirmation completion of the correction, or risk will stay on the downside. too.

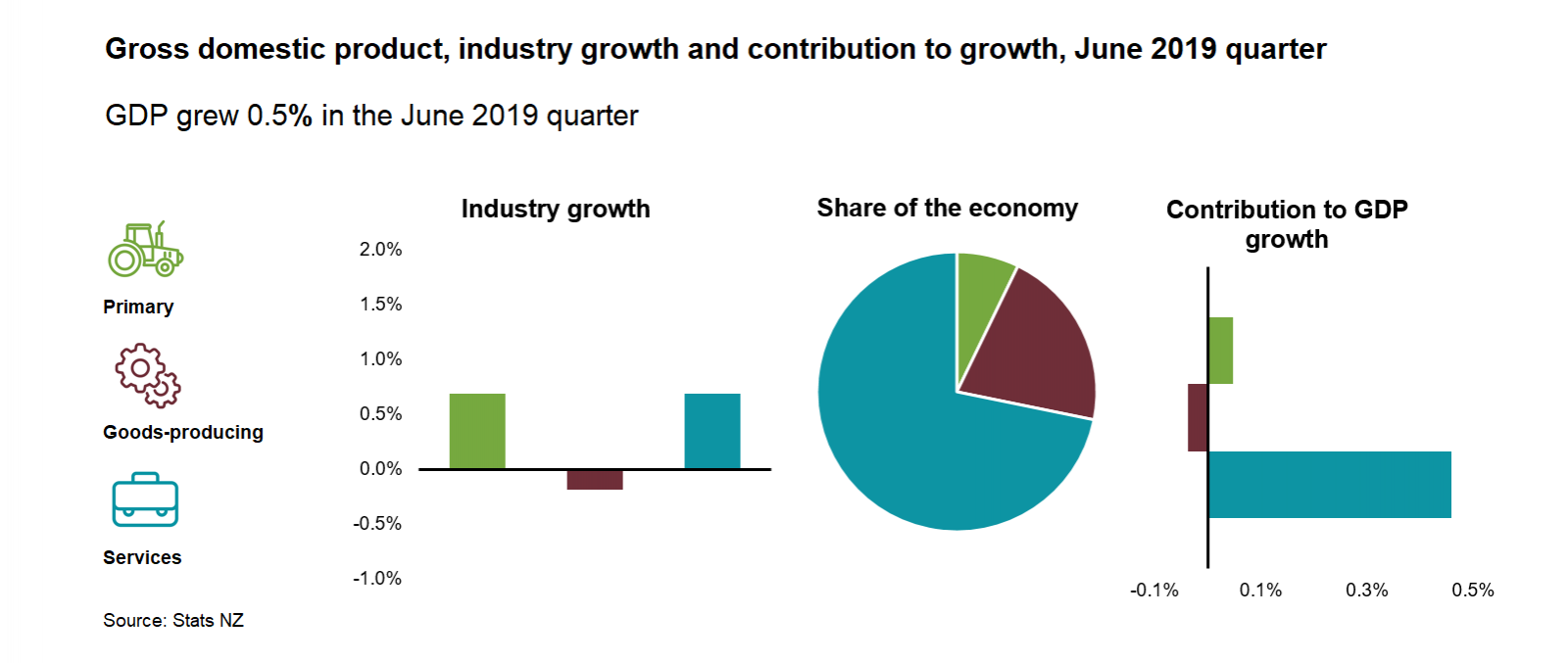

New Zealand GDP grew 0.5% qoq in Q2, above expectation of 0.4% qoq. Services industries grew 0.7%, accelerated from 0.3%. Services growth was also wide-spread, in 8 out of 11 industries. Primary industries expanded 0.7%, rebound from two consecutive declines. However, goods-producing industries fell -0.2%, following 1.9% rise back in Q1.

NZD/USD stays soft after the release even though reaction was relatively muted. The decline was mainly due to the hawkish Fed cut overnight. Corrective recovery from 0.6269 should have completed at 0.6450 already. As long as 0.6362 minor resistance holds, further fall should be seen to retest 0.6269 next.

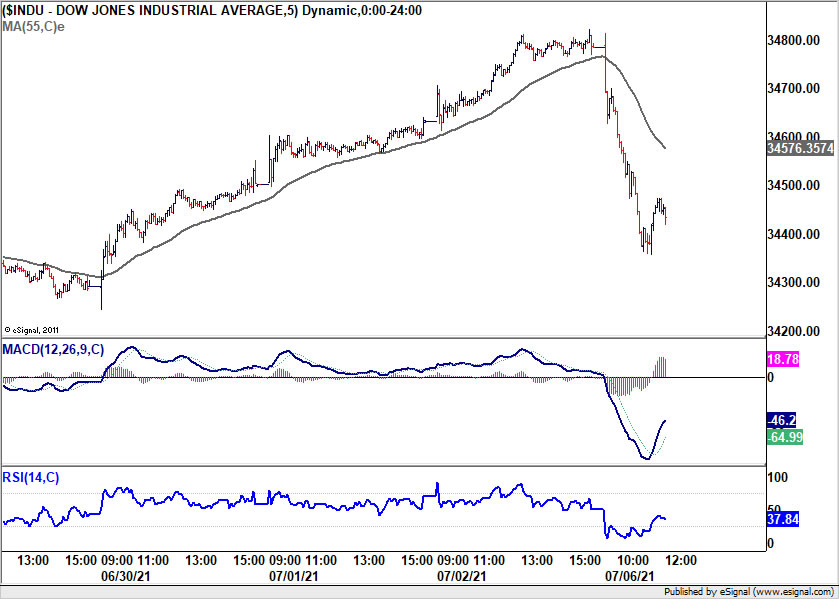

Yen surges broadly while Dollar is under some pressure as US stocks are in steep selloff. Industrial giant 3M is the key driver in the markets as it slashed 2019 full-year guidance and announce 2000 job cuts. It’s more than enough to offset the lift by Microsoft, which reported healthy quarterly results yesterday.

At the time of writing, DOW is already down -253 pts, or 0.95%. S&P 500 is down -0.40%. NASDAQ made new record high at 8151.84 but quickly retreated and is down -0.27%.

We’d noted before that we’re not convinced that US stocks are ready to resume long term up trend. Risk of reversal, at least for near term, is high with S&P 500 and NASDAQ close to record highs. Break of 2891.90 support in S&P 500 will bring pull back to 55 day EMA (now at 2825.33). Similarly, break of 7950.97 in NASDAQ will bring pull back to 55 day EMA (now at 7710.88.

We’d noted before that we’re not convinced that US stocks are ready to resume long term up trend. Risk of reversal, at least for near term, is high with S&P 500 and NASDAQ close to record highs. Break of 2891.90 support in S&P 500 will bring pull back to 55 day EMA (now at 2825.33). Similarly, break of 7950.97 in NASDAQ will bring pull back to 55 day EMA (now at 7710.88.

DOW has been the under performer comparing with the other two major indices. With today’s gap down, focus will be on 26070.83. Break will be the first sign that rise from 21712.53 has completed, ahead of 26951.81 record high, on bearish divergence condition in daily MACD. Deeper fall should then be seen, at least, to 38.2% retracement of 21712.53 to 26695.96 at 24792.29. Such development would drag down USD/JPY, as well as other Yen crosses. But we wouldn’t expect it to prompt deep selling in Dollar elsewhere.

Oil price continues to surge on US withdrawal of Iran deal, WTI hit as high as 71.17 so far before retreat slightly to 70.9. US 10 year yield also follows and is back above 3% now.

In the currency markets, today’s trend continue with USD and CAD trading as the strongest ones. Meanwhile, JPY is trading as the weakest one. The is in line with the development of surging oil and yield.

Dollar is trading above last week’s high except versus JPY and GBP. Note that Yen’s strength last week was due to falling yields in US and, more so in Europe. Rebound in US yield could now put 110.02 resistance in USD/JPY back into focus.

Action Bias of USD/JPY is looking promising. H row is all upside blue with the current rebound. D action also turned from neutral to upside blue already.

Action Bias of USD/JPY is looking promising. H row is all upside blue with the current rebound. D action also turned from neutral to upside blue already.

Nonetheless, we’d stay cautious in the pair first, at least until either 110.02 is taken out, or when 6H action bias also turns upside blue.

Nonetheless, we’d stay cautious in the pair first, at least until either 110.02 is taken out, or when 6H action bias also turns upside blue.

US ISM Services dropped -2.4 pts to 59.9 in January, above expectation of 58.7. Looking at some details, business activity/production dropped -8.4 to 59.9. New orders dropped -0.4 to 61.7. Employment dropped -2.4 to 52.3. Supplier deliveries rose 1.8 to 65.7. Prices dropped -1.6 to 82.3.

ISM said: “The past relationship between the Services PMI® and the overall economy indicates that the Services PMI® for January (59.9 percent) corresponds to a 3.5-percent increase in real gross domestic product (GDP) on an annualized basis.”

Canada’s GDP rose 0.1% mom in September, matched expectations. Goods-producing industries grew 0.3% mom, leading the growth with a first increase in six months. Services-producing industries were essentially unchanged. Overall, 10 of 20 industrial sectors increased. Advance information indicates that GDP rose 0.2% mom in October.

In Q3, GDP fell -0.3% qoq, reversing Q2’s 0.3% qoq growth. The decrease in international exports and slower inventory accumulation were partially offset by increases in government spending and housing investment. Final domestic demand increased 0.3%, following a similar increase in the second quarter.

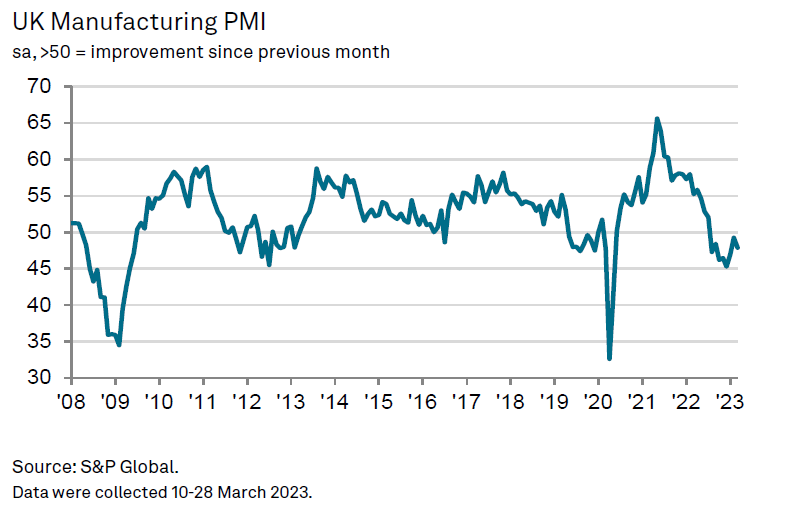

UK PMI Manufacturing was finalized at 47.9 in March, down from February’s 7-month of 49.3. The index has stayed below the neutral 50 mark for eight successive months.

Rob Dobson, Director at S&P Global Market Intelligence, highlighted that UK manufacturing production “fell back into contraction” at the end of the first quarter due to subdued market conditions. While total new orders saw a slight increase after a nine-month contraction, order book levels remain low. New export order declines continue to impact demand, despite a modest recovery in the domestic market.

However, Dobson pointed to positive developments in pricing and supply during March. Input price inflation reached its lowest level since June 2020, and although selling prices decelerated, they remained higher than input costs, offering some relief for manufacturers’ margins. Supply chains continued to recover, with March witnessing the greatest improvement in average vendor lead times in the survey’s 31-year history. Dobson noted that this development “should hopefully filter through to further cost reductions and lessen the disruption to production workflows in the coming months.”

The US Trade Representative released an update on Section 301 IP investigation on China yesterday. Less than two weeks ahead of the Trump-Xi meeting as sideline of G20 summit in Argentina, USTR is piling more pressure on China for reforms. In short, the report complained that “China has not fundamentally altered its unfair, unreasonable, and market-distorting practices that were the subject of the March 2018 report on our Section 301 investigation.”

The report also noted that “despite repeated U.S. engagement efforts and international admonishments of its trade technology transfer policies, China did not respond constructively and failed to take any substantive actions to address U.S. concerns.” And, China, “made clear – both in public statements and in government-to-government communications – that it would not change its policies in response to the initial Section 301 action.” The report also said “China largely denied there were problems with respect to its policies involving technology transfer and intellectual property”.

Australia employment grew 29.1k to 12.9m in January, slightly below expectation of 30.2k. That’s also the fourth consecutive monthly growth in jobs. Full time employment rose 59k to 8.82m. Part-time employment dropped -29.8k to 4.12m.

Unemployment rate dropped to 6.4%, down from 6.6%, better than expectation of 6.5%. But that was still 1.1% higher than a year ago. Participation rate dropped -0.1% to 66.1%. Monthly hours worked dropped -4.9%, or -86m hours, to 1667m.

Sterling rises notably after comments from European Commission President Jean-Claude Juncker. He told Sky News that he didn’t have “an erotic relation” to the so-called Irish backstop. As long as alternative arrangements are in place to achieve all main objectives of the backstop, he’s prepared to remove it from the Brexit withdrawal agreement.

He also said that no-deal Brexit would have “catastrophic consequences” and he was doing “everything to get a deal Juncker believed that a Brexit deal can be reached by October 31.

In a speech, Fed Vice Chair Richard Clarida said neutral interest rates appear to have fallen in the US and abroad. And, “this global decline in r* is widely expected to persist for years”. He emphasized the importance of the trend as “all else being equal, a fall in neutral rates increases the likelihood that a central bank’s policy rate will reach its effective lower bound (ELB) in future economic downturns. ” And that in turn “could make it more difficult during downturns for monetary policy to support household spending, business investment, and employment, and keep inflation from falling too low.”

Clarida pointed to another key development in decreasing responsiveness of inflation to resource slack. That is, “short-run Phillips curve appears to have flattened, implying a change in the dynamic relationship between inflation and employment”. He warned that a flatter Philips curve increases the cost of reversing unwelcome increase in long-run inflation expectations. And “a flatter Phillips curve makes it all the more important that longer-run inflation expectations remain anchored at levels consistent with our 2 percent inflation objective.”

Brexit hardliner Jacob Rees-Mogg reiterated his backing to Prime Minister Theresa May’s deal as it’s better than no Brexit. He tweeted that “The choice seems to be Mrs May’s deal or no Brexit.” Also, Rees-Mogg explained in the Monday Moggcast podcast that “I’ve always thought that no deal is better than Mrs. May’s deal, but that Mrs. May’s deal is better than not leaving at all.” While May’s deal is “in no way a good deal, Rees-Mogg said: “against that there are the threats of a long delay, and many people in Parliament who want to frustrate the result of the referendum.”

By loading the video, you agree to YouTube’s privacy policy.

Learn more

Conservative MP Michael Fabricant echoed as that it’s the “dreadful conclusion” he came to too. And “a new PM can then negotiate a better and more distanced relationship with the EU after Brexit. (Of course this is the least worst option but the only practical way forward for now.)”

Fabricant also said: “The practical alternatives are far worse that the Withdrawal Agreement including keeping us in the Customs Union and Single Market indefinitely so no control of immigration or having to obey EU directives.”

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

By loading the tweet, you agree to Twitter’s privacy policy.

Learn more

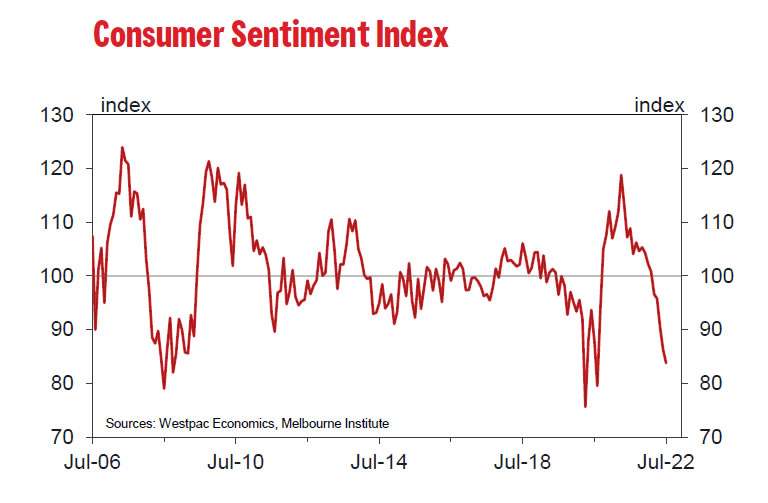

Australia Westpac Consumer Sentiment Index dropped from 86.4 to to 83.8 in July. The confidence has been falling every month this year, and it’s now -19.7% below December’s level.

Westpac said that both level and pace of deterioration are “comparable to previous major shocks”. It added that rate fears were intensifying, with 73% polled expecting rates to rise more than 1%.

As for RBA policy, Westpac expects another 50bps rate hike on August 2, taking interest rate to 1.85%. That would be near to Westpac’s assessed “neutral zone” of 1.5-2.0%. It expects RBA to adopt a “more cautious approach” once policy moved to “neutral”, and pause the tightening first after August’s hike.

Yen and Dollar staged a strong rebound in early US session after stocks unexpectedly tumbled deeply. DOW was once down as much as -431 pts and it’s down nearly -1% at the time of writing. Slightly weaker than expected ISM services shouldn’t be that big an impact. However, both ISM manufacturing and services employment were back in contraction in June.

There might also be speculations that Fed would be forced to tightening the tap a bit, as global central banks are starting to do so. Speculation might have intensified after RBA’s tapering and speculation of RBNZ rate hike, given that BoC has already cut down bond purchases.

China’s way of crackdown on technology companies is also a source of concern. Ride-hailing giant Didi has just had a massive IPO lost week, but the Chinese government was quick to launch a so-called cyber security investigation, forcing the app down the shelves. Two smaller recent listings, Full Truck Alliance and Kanzhun are also believed to be under review.

Technically, DOW’s steep pull back today doesn’t alter the near term bullish path yet. As long as 34186.13 support holds, it will still more likely to break through 35091.56 high to resume larger up trend. However, break of 34186.13 will likely extend the consolidation pattern with another falling leg towards 33271.93 support, in the less bearish case.

Australia NAB Business Confidence was unchanged at 3 in December. However, Business Conditions dropped sharply by -9 pts from 11 to 2. That’s the largest monthly fall since the global financial crisis. And the deterioration was “relatively broad-based across states and industries”.

NAB also noted that “at face value, the fall over the past 6 months suggests a significant slowing in the momentum of activity in the business sector – especially from the highs seen earlier in the year.”

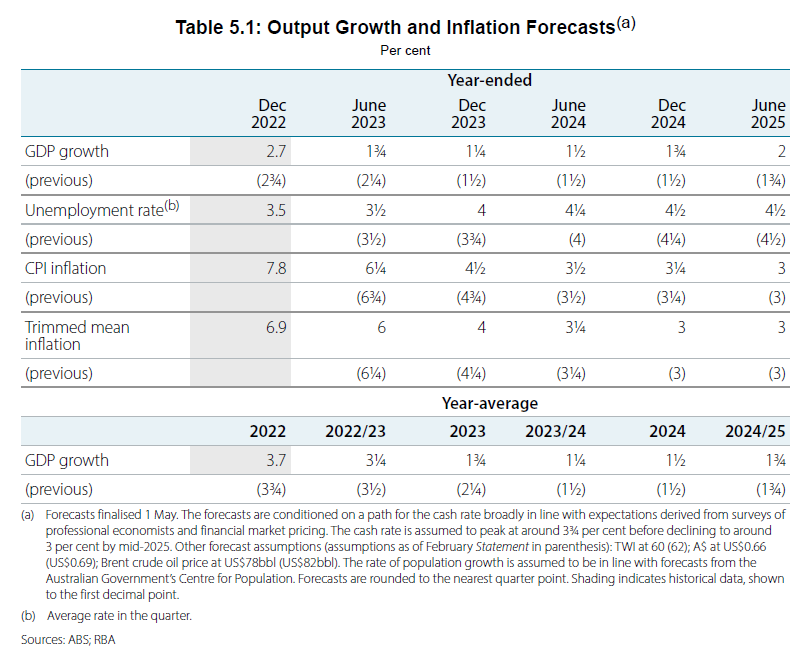

In the quarterly Statement on Monetary Policy, RBA reiterated that “some further tightening of monetary policy may be required” to ensure that inflation returns to target in a “reasonable timeframe”. But that will depend upon “how the economy and inflation evolve.”

The new economic projections show both headline and trimmed mean inflation slowing more rapidly in 2023. However, both measures are only expected to reach the top of target range by mid-2025. Additionally, the central bank downgraded its GDP growth forecasts for 2023 and predicts a higher unemployment rate. The evolving economic landscape will be key in determining the RBA’s future policy moves.

Year-average GDP growth forecast:

Unemployment rate forecast:

Headline CPI forecast:

Trimmed mean CPI forecast:

ECB Governing Council member Martins Kazaks has suggested that a smaller rate hike of 25 basis points in May is possible, although a 50 basis point increase should not be dismissed entirely.

In an interview with Latvian news service Leta, Kazaks stated, “At some points, it’s only natural that the step size is reduced. For example, the increase could be not 50 basis points, but 25 basis points.”

Regarding the upcoming ECB Council meeting in May, Kazaks commented, “Should we move to a lower step already at the ECB Council meeting in May? I think there is every possibility for that, but a 50 basis point increase is not an option that can be ignored.”

Kazaks remains optimistic about the Eurozone’s economic outlook, pointing out that “the economy is still resilient, there will probably not be a recession in the Eurozone this year, the labor market remains strong, the pressure on wages is still very high and in some cases even increasing. Therefore, in my opinion, a rate increase is necessary.”

ActionForex.com was set up back in 2004 with the aim to provide insightful analysis to forex traders, serving the trading community for over a decade. Empowering the individual traders was, is, and will always be our motto going forward.

Contact us: contact@actionforex.com

© ActionForex.com © 2024 All rights reserved.

WTI crude oil resumes recent free fall

WTI crude oil’s recent free fall resumes today by taking out 54.84 low and reaches as low as 53.65 so far. Near term outlook will now stay bearish as long as 58.04 resistance holds even in case of recovery.

Fall from 77.06 is at least correcting the up trend from 27.69 to 77.06. Based on current momentum, it could indeed be an impulsive move rather than a corrective move. In either case, deeper decline should be seen to 61.8% retracement of 27.69 to 77.06 at 46.54 in medium term.

Also, a net effect in the currency markets is a drag on the Canadian Dollar.