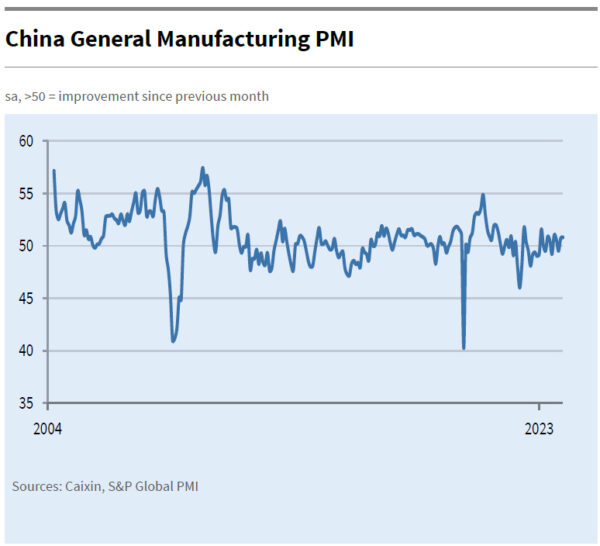

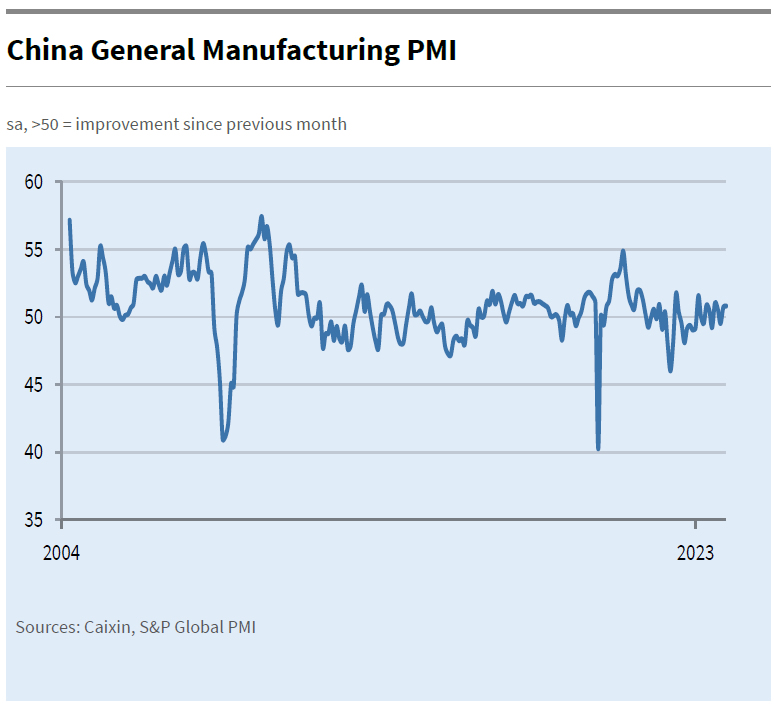

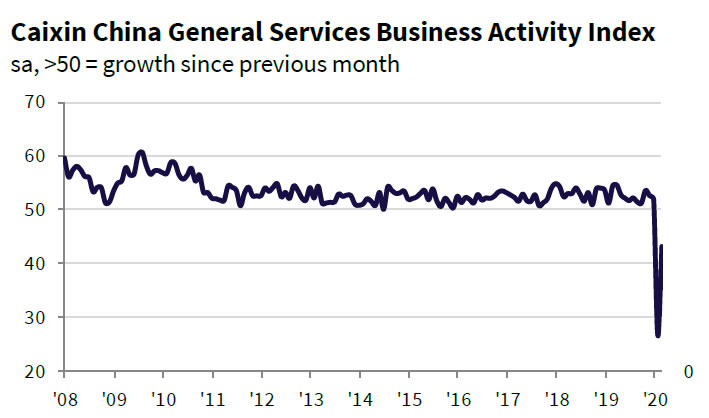

December brought mixed signals from China’s manufacturing sector, as indicated by two key indices: Caixin PMI and official NBS PMI. Caixin PMI Manufacturing slightly increased from 50.7 to 50.8, surpassing expectations of 50.4, suggesting a marginal yet steady expansion in the manufacturing sector. Notably, Caixin highlighted that both output and new orders are rising at faster rates, indicating increased production and demand within the industry.

However, the same period saw a dip in official PMI Manufacturing, which fell from 49.4 to 49.0. This decline suggests contraction in the sector, contrasting with optimism reflected in Caixin PMI data. The difference between these two indices can be attributed to their varied focus groups; Caixin PMI typically surveys small and medium-sized enterprises, while NBS PMI is more reflective of larger, state-owned companies.

Wang Zhe, Senior Economist at Caixin Insight Group, emphasized the improved economic outlook for the manufacturing sector, with expanding supply and demand, and stable price levels. Yet, he also pointed out significant challenge in employment, highlighting businesses’ cautious approach in areas like hiring, raw material purchasing, and inventory management.

On the other hand, NBS PMI Non-Manufacturing showed a slight improvement, rising from 50.2 to 50.4. This marginal increase suggests a modest expansion in China’s services sector.

Full China Caixin PMI release here.

Fed Daly: Balance sheet rolloff and interest rate shouldn’t work at cross purposes

San Francisco Fed President Mary Daly said the economy is slowing faster than she expected. And, tighter financial conditions, slower growth abroad, and rising uncertainty are also threatening to slow US growth. Though, she added that “there’s nothing on the radar that says we’re slipping into recession.”

Daly also said interest rates are now within a “hair’s breadth” of neutral. And she support a pause in rate hikes until there are signs of overheating. At the same time, she said Fed should align the balance sheet policy with the “patient” interest rate stance. “Those two are meant to work together and not at cross purposes,” she said.