OCR unchanged at 1.75 percent

Statement by Reserve Bank Governor Adrian Orr:

The Official Cash Rate (OCR) remains at 1.75 percent.

We expect to keep the OCR at this level through 2019 and into 2020. The direction of our next OCR move could be up or down.

Employment is around its sustainable level and consumer price inflation remains below the 2 percent mid-point of our target, necessitating continued supportive monetary policy. Our outlook for the OCR assumes the pace of growth will pick up over the coming year, assisting inflation to return to the target mid-point.

Our projection for the New Zealand economy, as detailed in the August Monetary Policy Statement, is little changed. While GDP growth in the June quarter was stronger than we had anticipated, downside risks to the growth outlook remain.

Robust global economic growth and a lower New Zealand dollar exchange rate is expected to support demand for our exports. Global inflationary pressure is expected to rise, but remain modest. Trade tensions remain in some major economies, increasing the risk that ongoing increases in trade barriers could undermine global growth. Domestically, ongoing spending and investment, by both households and government, is expected to support growth.

There are welcome early signs of core inflation rising towards the mid-point of the target. Higher fuel prices are likely to boost inflation in the near term, but we will look through this volatility as appropriate. Consumer price inflation is expected to gradually rise to our 2 percent annual target as capacity pressures bite.

We will keep the OCR at an expansionary level for a considerable period to contribute to maximising sustainable employment, and maintaining low and stable inflation.

Meitaki, thanks.

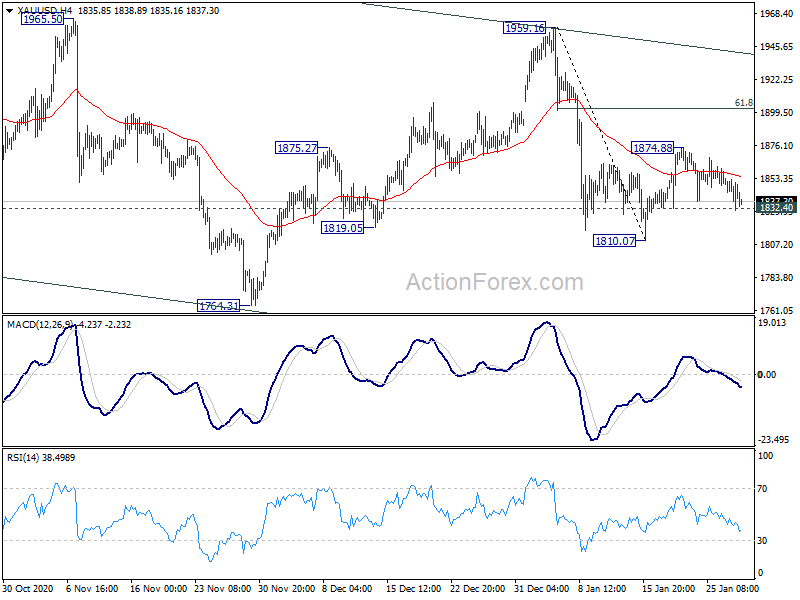

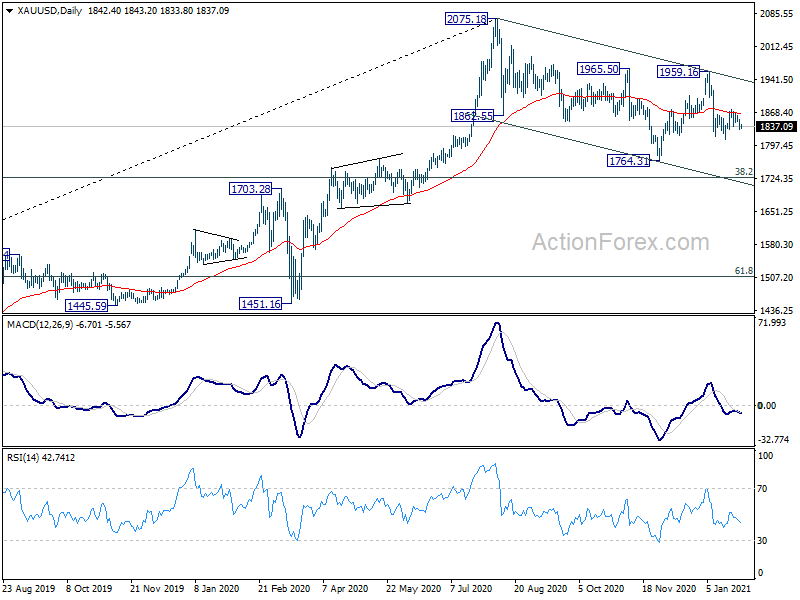

China Shanghai Composite down but not out, AUDUSD attempts down trend resumption

Following selloff in Asia, Major European indices are all trading in red in initial trading. At the time of writing, DAX is down -1.4%, CAC down -1.2%, FTSE down -1.3%. But they are kept well above last week’s low, suggesting that selling is not too serious.

The China SSE composite closed down -49.85 pts, or -1.76% at 2777.77. While SSE lose 2800 handle again, it’s kept well above last week’s low at 2691.02. We’ve mentioned a number of times that 2638.30 – 2700 zone represents important support level. Judging from the fact that SSE close just slightly lower than open at 2780.70, there was no panic selling. We’re holding on to the case that 2691.02 is at least a short term bottom and there should be another rise through 2848.37 to extend the corrective rebound.

In the currency markets, Australian Dollar remains the weakest one for today, with AUD/USD as the biggest loser.

From Action Bias point of view, the string of downside red bar in H Action Bias is hinting at down trend resumption. The break of 0.7414 minor support today is another signal on it. But we’d wait for 6H Action Bias to turn red too to give us more confidence on it. After all, we see 0.7328 as an important medium term support that takes some determination to break.