Sample Category Title

Asian markets down on conerns of US-China trade war, Dollar down

Asian markets are broadly lower on concerns of full-blown trade war between US and China. At the time of writing:

- Nikkei down -0.7%

- HK HSI down -1.3%

- China SSE down -0.5%

- AU all ordinaries down -0.57%

- KOSPI down -0.51%

Another globalist Rex Tillerson is now gone, just short after Gary Cohn. There are reports that Trump is considering a USD 60b taiff package for China.

Dollar is trading under broad based selling today.

Elliott Wave Analysis: USDCAD Potential Upside To 1.324

USDCAD Short Term Elliott Wave view suggests the rally from 1/31 low (1.2247) remains in progress as a triple three Elliott Wave Structure. A triple three is labelled as WXYZ and each leg in this structure is corrective, so we have 3-3-3-3-3 structure. Up from 1.2247, Intermediate wave (W) ended at 1.2689, Intermediate wave (X) ended at 1.2445, Intermediate wave (Y) ended at 1.3 and second Intermediate wave (X) is proposed complete at 1.2801. Pair still needs to break above Intermediate wave (Y) at 1.3 to add validity to this view and avoid a double correction.

Up from 1.28, the rally is unfolding as a zigzag Elliott Wave Structure where Minute wave ((a)) ended at 1.2984. A zigzag is a 5-3-5 structure and thus we could see the internal subdivision of Minute wave ((a)) unfolded as 5 waves impulse Elliott Wave structure. Minutte wave (i) of ((a)) ended at 1.2877, Minutte wave (ii) of ((a)) ended at 1.2828, Minutte wave (iii) of ((a)) ended at 1.2947, Minutte wave (iv) of ((a)) ended at 1.2914, and Minutte wave (v) of ((a)) ended at 1.2984. Minute wave ((b)) pullback is currently in progress to correct cycle from 3/12 low in 3, 7, or 11 swing before pair resumes higher again with potential target of 1.324 to end cycle from 1/31 low. A break above Intermediate wave (Y) at 1.3 will be the final confirmation that the next leg higher in Intermediate wave (Z) has started.

USDCAD 1 Hour Elliott Wave Chart

BoJ Kuroda – Same message, long way from hitting inflation target

BoJ Governor Haruhiko Kuroda repeated his rhetorics that Japan is still long way from meeting the 2% inflation target. Therefore, it's too early to talk about stimulus exit. But he assured the parliament that the central bank has the tools to smoothly exit from the ultra-loose monetary policy when needed. Kuroda added that "by combining various tools, it's possible to shrink the BoJ's balance sheet at an appropriate pace while keeping markets stable." Meanwhile, he also hailed that while keeping long term yield low with the policy, BoJ also managed to maintain markets' trust in JGBs. He noted "If market trust over Japan's debt is eroded, it will be difficult for us to keep interest rates low with our yield curve control policy."

Release earlier, minutes of BoJ January meeting showed that some board members were concerned with the impact of the loose monetary policy, especially on banks. The minutes showed "some members said it was important to continue to monitor and assess the positive impacts and side-effects of the current monetary easing policy, including its effects on Japan's banking system." Some member suggested to raised the yield target as economy improves. But another member (obviously Goushi Kataoka), called for ramping up the stimulus.

Asian session data wrap up: China posted solid Feb data

Asian session data wrap up:-

New Zealand

- Current account Q4: NZD -2.77b vs exp -2.45b vs prior -4.83b

Australia

- Westpac consumer confidence Mar: 0.2% vs prior -2.3%

Japan

- Machine orders Jan: 8.2% mom vs exp 5.2% mom vs prior -9.3% mom

China

- Retail sales Feb: 9.7% yoy vs exp 10.0% yoy vs prior 9.4% yoy

- Industrial production Feb: 7.2% yoy vs exp 6.3% yoy vs prior 6.2% yoy

- Fixed assets investment Feb: 7.9% yoy vs exp 7.0% yoy vs prior 7.2% yoy

Upcoming

- German CPI

- Eurozone industrial production

- Eurozone employment

- US retail sales

- US PPI

- US business inventories

Fundamentals: Forex, Gold, Oil & Cryptos

US core CPI inflation holding at 1.8%

Dollar defensive against most currencies

Gold was able to make strong bullish gains up to $1328/ounce

Forex

Friday's non-farm payrolls did show higher than anticipated US job gains for the month of February, but subdued wage inflation meant that overall, economic data failed to move the dial in favour of faster rate hikes. With the rate of US core CPI inflation holding at 1.8%, the likelihood of more than three FED rate rises in 2018 has become unlikely, turning the dollar defensive against most currencies. Despite Draghi putting a dovish spin on the ECB's decision to drop its easing bias in last week's meeting, the Euro still succeeded in crawling up 0.2% against the dollar. However, with Trump's new secretary of state Mike Pompeo, seen by investors as more hawkish than his predecessor Tillerson, traders may have jumped the gun when hedging against the dollar.

The Sterling started the week on firmer footing, supported by renewed optimism over ongoing Brexit negotiations. It was up 0.5% against the greenback.

Against the Japanese Yen, which tends to perform well when markets are anxious, the dollar was up 0.1%. Controversy between two key Japanese political figures Shinzo Abe and Finance Minister Taro Aso may be offsetting the dollar bears.

Gold

The precious metal flourished today after a Cronyism scandal between Japanese PM Shinzo Abe and his close ally Finance Minister Taro Aso emerged. With US equities struggling to stay afloat and the dollar weakening, Gold was able to make strong bullish gains up to $1328/ounce. However, the Whitehouse's new Secretary of State coupled with tomorrow's USD retail sales release could make the tide turn in favour of the hawks, which could potentially add severe headwinds to Gold's bullish rally.

Oil

A surge in American shale oil output, reduced Oil's relative competitiveness causing traders to turn bearish. Investors further compounded the move towards the downside due to a pullback in US equity markets, reducing the demand for Oil. Overall, WTI Crude Oil was down 1.3% over the day.

Market Morning Briefing: Pound Breached 1.395 Yesterday

STOCKS

Dow (25007.03, -0.68%) is trading near important levels just now. Resistance near 25200 on the 3-day candle is holding well and there is scope of a fall to 24400-24000 in the medium term. While below 25500, view is bearish towards 24000.

Dax (12221.03, -1.59%) fell sharply in line with our expectation and while below 12500, there is room on the downside towards 12000-11800 in the coming sessions.

Nikkei (21748.30, -1.00%) is trading along the resistance as mentioned yesterday also. Trade within 22000-21400 is possible in the next couple of sessions. A fall below 21400, if seen could take it further down towards 21200-21000. For now the index is likely to remain stable or see a short corrective dip.

Shanghai (3294.85, -0.48%) seems to be holding below 3350 resistance as mentioned yesterday. While below 3350, the price could fall towards 3250-3200 in the coming sessions.

Nifty (10426.85, +0.05%) and Sensex (33856.78, -0.18%) both tried to move up a bit yesterday but came off to close at slightly higher levels. If the upside momentum continues, the indices could move up towards 10500 and 34500 as our initial target; else a short dip back towards 10380 and 33500 could be seen in the near term.

COMMODITIES

Brent (64.7) is trading below 66 and stuck between the narrow 66-63 region just now. Some more trade within this region is possible in the near term. Near term looks sideways to bearish.

59.50-60.0 is the trade region for WTI (60.80). Stable movement is likely to continue this week.

Gold (1329.0) is likely to move up gradually towards 1340/50. Near term looks bullish.

Copper (3.1485) is slowly truing to rise but may again face a short rejection from 3.1750 before coming off again towards 3.1000-3.0750. Only if a break above 3.1750, if seen could ensure a rise towards 3.20 or higher.

FOREX

As mentioned yesterday, the data releases in USA this week would be important for the course followed by major currency pairs and bond yields. The US CPI data yesterday could not exceed market expectations, thereby decreasing likelihood for quicker rate hikes by the US Fed this year. This has led to Dollar weakening against majors.

The Dollar Index (89.58), against our expectation, has broken immediate support on daily candles near 89.75 and might now move further down towards support near 89.2-89.0 on weekly line chart. This is a crucial support level seen on a trendline coming from Mar’14, a break of which could lead to medium term bearishness. The movement in the next few sessions could depend on US Retail Sales data (due later today), EU CPI data (on Friday), US Housing Starts data (Friday) and US Industrial Prodn data (Friday).

Euro (1.2409): Against our expectation, the Euro has breached resistance that was being provided by the 21 days moving average on daily line chart. There is some resistance that could still be provided near 1.24 by earlier support (now resistance) trendline on the daily line chart. However, in case of a breach of the same, the Euro should test resistance near 1.25-1.255 on 3 day and daily candles. The EU CPI data release on Friday would be vital – a higher than expected figure would be bullish for Euro.

Dollar-Yen (106.44) yesterday saw a high near 107.29 after news of a political scandal involving the Prime Minister broke out, lowering confidence in the Yen. However, it proved to be a temporary blip as there was strong resistance provided by moving average lines on the daily line chart near those levels. Moreover, global Dollar weakness helped in bringing Dollar Yen back below 106.5. We could now see a resumption of the downmove towards crucial support near 105.5-105.0 in the coming sessions -a break of the same would confirm medium term bearishness.

The Euro-Yen (132.05) against expectations has moved back up beyond 132 as the Euro strengthened against the Dollar. If the Euro strength pauses for the next few days while the Yen regains strength against the Dollar, we could see the Euro Yen resume its earlier downmove towards 130-129. A testing of 130 however implies 105 on the Dollar Yen (if Euro stays near 1.24) – if this happens, Dollar Yen might drop further, taking Euro Yen below 130-129.

Pound (1.3986) breached 1.395 yesterday, which was seen as immediate resistance level on daily candles. There is higher resistance now near 1.4 which should lead to a dip in the Pound in the next couple of sessions.

Dollar-Rupee (64.90): Dollar Rupee is likely to come down towards 64.80/75 today before pausing. The RBI in a move late last evening banned LOUs for Imports, thereby creating some uncertainty regarding where the Dollar Rupee might open today. Whether banning of LOUs will lead to less USD borrowings leading to lesser demand or whether it will lead to importers buying more Dollars to clear payments would have to be seen.

INTEREST RATES

The US CPI data couldn’t exceed expectations yesterday thereby decreasing likelihood for quicker rate hikes by the US Fed this year. This has led to a drop in US yields.

US 10 Year Yield (2.83), US 30 year Yield (3.08), US 5 year yield (2.61), US 2 year yield (2.25) : US yields are seeing a significant dip in their respective set ranges around their long term resistance levels. Yesterday we wrote about how US yields might drop to keep the German – US Yield spread about crucial long term support near -2.26%. The same is happening currently. Last week, we had also said that there might just be some drop in US yields in this week, after which the week of the US Fed meeting might then see volatility return.

Lets wait and watch how further US data releases this week impact yields. Currently, the likelihood of a significant rise in yields due to the Fed meeting next week is seen to be decreasing. (Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively )

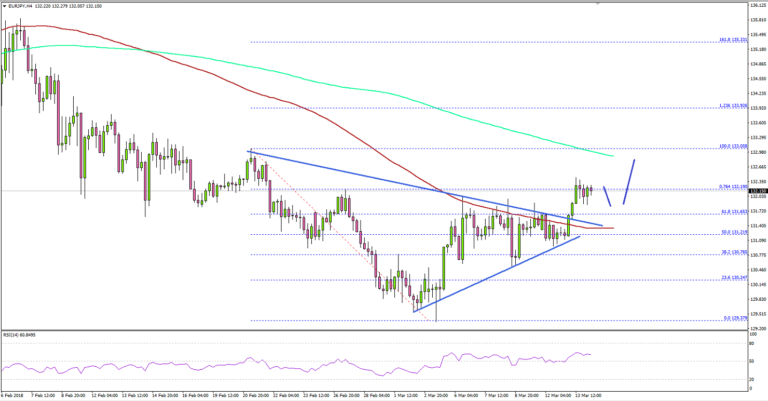

EUR/JPY: Is This Upside Break In Euro To Yen?

Key Highlights

- The Euro started a nice upside move from the 130.50 swing low against the Japanese Yen.

- There was a break above a crucial contracting triangle with resistance at 131.60 on the 4-hours chart of EUR/JPY.

- The pair could gain traction if it continues to find support near 131.50.

- Today, the German CPI figures for Feb 2018 will be released, which is expected to rise 0.5% (MoM).

EURJPY Technical Analysis

The Euro moved higher after consolidating around the 130.00 handle against the Japanese Yen. The EUR/JPY pair broke a major resistance near 131.50 to move into a positive zone.

Looking at the 4-hours chart of EUR/JPY, the pair succeeded in forming a support base above 130.50 and moved higher. It broke the 50% Fib retracement level of the last decline from the 133.05 high to 129.37 low.

Moreover, there was a break above a crucial contracting triangle with resistance at 131.60, which opened the doors for more gains. Most importantly, the pair settled above 131.50 and 100 simple moving average (red, 4-hour).

On the upside, the next major hurdle is near the last high of 133.05 since it is close to the 200 simple moving average (green, 4-hour).

If the pair starts a downside correction from the current levels, the broken resistance near 131.50 may perhaps as a support. Below 131.50 and 100 simple moving average (red, 4-hour), the pair could move back in the bearish zone.

Economic Releases to Watch Today

- German Consumer Price Index for Feb 2018 (YoY) – Forecast +1.4%, versus +1.4% previous.

- German Consumer Price Index for Feb 2018 (MoM) – Forecast +0.5%, versus +0.5% previous.

- Euro Zone Industrial Production for Jan 2018 (MoM) – Forecast -0.4%, versus +0.4% previous.

- US Retail Sales for March 2018 (MoM) – Forecast +0.3%, versus -0.3% previous.

- US Producer Price Index for Feb 2018 (MoM) – Forecast +0.1%, versus +0.4% previous.

- US Producer Price Index for Feb 2018 (YoY) – Forecast +2.8%, versus +2.7% previous.

You’re Fired: Episode # 35 ‘Rexit’

You're Fired: Episode # 35 'Rexit.'

President Trump showed Rex Tillerson the Whitehouse' revolving door overnight – notching up the thirty-fifth departure of a senior official from the Trump Administration. Not sure, this should be interpreted as a huge surprise given their tenuous relationship over foreign policy as Trump and Tillerson seldom saw eye to eye. In fact, Tillerson's impending removal has been feeding the Foggy Bottom Rumour mill for some time, but the timing of the move along with his replacement, Mike Pompeo, current CIA Director, is what's significant to markets.

Predictably, there was not a considerable amount of follow-through regarding the markets initial reaction. But not to be underestimated, the significance of a shift to a global trade and foreign policy hawk with the US on course for a trade showdown with China and diplomatic negotiations with North Korea, is very significant suggesting the US is readying for hardball negotiations.

The “Rexit-Pompeo'headline was followed up with a Goldilocks US CPI print which triggered a fall in the DXY with moves lower in equities, yields and oil. The dollar sell-off can be attributed to the combination of lower CPI and the Whitehouse revolving door syndrome that exudes little confidence in the administration. While the moves in equities suggest investors are bracing for more worrying protectionist headlines

Equity Markets

Despite the tepid CPI inflation print US equity markets closed lower. And while the game of revolving chairs in Washington plays on, there is more risk aversion creeping into play as geopolitical uncertainty ratchets higher with the more hawkish foreign policy leaning, Mike Pompeo, now the face of US foreign policy. Equity investors remain extremely cautious about trade war escalations.

Oil Markets

The sell-off in oil markets is creating a lot of noise on the desk this morning. And while there was a bit of a reprieve as weaker short positions covered on yet another Libyan supply disruption, the broader macro conditions continue to weigh on prices. Also notable is that the April-May spread is in contango, dropping to -3c from +3c Monday for the first time since the March contract expiration on February 20. But price action was very choppy overnight while traders were immersed in numerous narratives

The market remains focused on EIA newsflow as the ever-expanding US supply continues to pose significant downside risk to oil prices. Also, the differing views on price targets between Saudia Arabia and Iran continue to highlight growing division within OPEC compliance.

But the market's turned incredibly choppy on the 'Rexit'headline and should remain so throughout today session.

Tillerson was viewed pro-oil given his tenure as a well-respected energy executive, which could be considered a small negative for the US industry. Nevertheless, more significantly on the geopolitical landscape, it brings some doubt into the Iran nuclear deal and the apparent escalation of US oil sanctions.

However, despite the evolving narratives, risk aversion is starting to factor into the equation as the market braces for possibly more market-unnerving protectionist headlines as the trade hawks now are in charge.

Gold Markets

Gold has been a little more than USD wager these days, and with a likely extension of USD dollar weakness as traders start to temper their expectations on the Fed rate hike curve after a soft CPI print, gold could make a move to recent higher $ 1336-41 levels.

However, there are growing reasons beyond the USD to increase haven hedges. The Whitehouse revolving door installs little confidence in US politics combined with a potentially hawkish shift on foreign policy could accelerate global geopolitical tensions. Also, with a US protections rhetoric likely to ring equity market alarm bells, gold should continue to be an ideal hedge in this highly unpredictable environment.

Currency Markets

The combination Tillerson -Pompeo and soft CPI report lead to broader US dollar losses on massive turnover.

The Japanese Yen

The USDJPY moved lower as risk turned lukewarm after the Tillerson -Pompeo announcement. While the dovish CPI should weigh on dollar sentiment, the possible hawkish escalation on trade war have investors playing their best defence in early Aisa as risk wobbles once again. Volumes were massive as the markets dropped from 107.27 to 106.46.

The Euro

ECB's Lane suggested that current EURUSD levels are not too concerning which sparked the initial move to 1.2435-50, but the “Rexit'CPI headline dictated the pace of the flow bias into the EUR which was extremely heavy as the market peaked just above 1.2400

View: In addition to the lack of confidence in the USD due to Washington's political quagmire, the Scope for more aggressive central bank tightening than the market has currently factored in will continue to support the JPY and EUR near-term

The Malaysian Ringgit

The weaker US CPI, softer US yields and a robust 7 Year MSG auction yesterday has seen favourable demand for the MYR overnight despite the fact Malaysia's January industrial output came in below forecast. However, the softer US CPI and the negative implications on US yields suggest the MYR bond carry trade is alive and well.

While the escalation of trade war rhetoric could weigh on regional sentiment, Malaysia is less exposed to US trade risk than regional peers are. However, the warning signs developing in oil markets that could be of concern as news flow continues to point to burgeoning US supply amidst expanding fissures in OPEC compliance.

Gold Edges Upwards As US Consumer Inflation Slips

Gold has edged higher in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1326.52, up 0.27% on the day. In economic news, CPI and Core CPI both slowed to 0.2%. On Wednesday, the US releases key inflation and consumer spending reports, so we could see stronger movement in gold prices.

In the US, CPI dropped from 0.5% to 0.2%, and Core CPI edged lower to 0.2%, down from 0.3%. Lower inflation could have a significant impact on the Federal Reserve’s monetary policy. if inflation does not move upwards, the Fed could maintain its projection of three rate hikes in 2018. If, however, inflation moves closer to Fed’s inflation target of 2 percent, there is a stronger likelihood of four rate hikes this year.

The markets are keeping a close eye on the Federal Reserve, which holds its next policy meeting next week. The Fed is widely expected to raise rates for the first time this year at that meeting, but the real question is how many hikes we’ll see in 2018. The Fed projection remains at three rate hikes, but strong economic data could push the Fed to raise its forecast. Higher US interest rates makes the greenback more attractive to investors, so the number of rate hikes could have a strong impact on gold prices, which tend to move inversely with interest rate levels.

No Chaos, Just Great Energy

Turmoil at the White House raises the risks of more interventionist trade and foreign policy. The euro was the top performer Tuesday while the Canadian dollar lagged. The BOJ minutes, the RBA's Kent and Japanese machine orders are up next; along with a US special election. Below is the Premium video, highlighting 11 existing trades ahead of US retail sales.

The departures of Secretary of State Rex Tillerson and two low level officials shook up the White House ranks on Tuesday. Tillerson had long been rumored to be leaving but Trump made it official with a tweet and appointed CIA head Mike Pompeo to the position at the same time.

Separate rumors were that national security advisor H.R. McMaster will be next to go be replaced by John Bolton. While the departures aren't a shock, the replacements are major hawks, especially on Iran and North Korea.

On the trade front, a report said Trump was preparing a series of China-directed tariffs to be released in the coming weeks. The news overshadowed the CPI report, which was in-line with estimates but contained a number of soft details that suggest a deceleration in the months ahead.

The S&P 500 had been as high as 2801 but skidded to 2765 at the close. Along with that, USD/JPY fell to 106.56 from 107.25 and the US dollar was broadly weaker.

One big exception was the Canadian dollar. It's increasingly vulnerable to an aggressive White House trade agenda but it was a domestic speech that sank it on Tuesday. The BOC's Poloz said the country will be able to handle more growth without inflation than believed and that the central bank wanted to allow firms to build capacity without choking out the recovery. USD/CAD is back close to the 1.30 level it flirted with last week.

The upcoming calendar features a few notable events starting with the RBA's Kent at 2210 GMT. The Australian dollar fell late on Tuesday but finished close to unchanged. Japan is in focus at 2350 GMT with the minutes of the latest BOJ meeting and January machine orders, which are forecast to rise 5.2% m/m.

However it will be politics continuing to dominate. The Abe government has been swept up in a document forgery scandal and in Pennsylvania voters will put Trump to the test. A House district he won by 20 points in 2016 is up for grabs and could go to a Democrat. There are no immediate implications for markets but it could pit him against Congressmen who are afraid of losing elections in November.