Sample Category Title

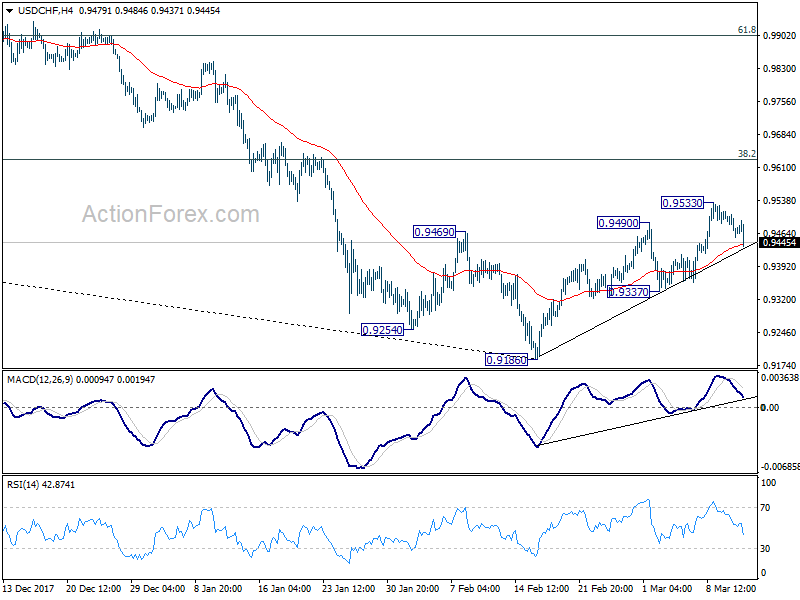

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9452; (P) 0.9482; (R1) 0.9505; More...

USD/CHF drops sharply in early US session, but stays above 0.9337 minor support. Intraday bias remains neutral first. Another rise is expected as long as 0.9337 support holds. Above 0.9533 will target 0.9626 fibonacci level. However, break of 0.9337 will indicate that the rebound has completed. In such case, intraday bias will be turned back to the downside for retesting 0.9186 low.

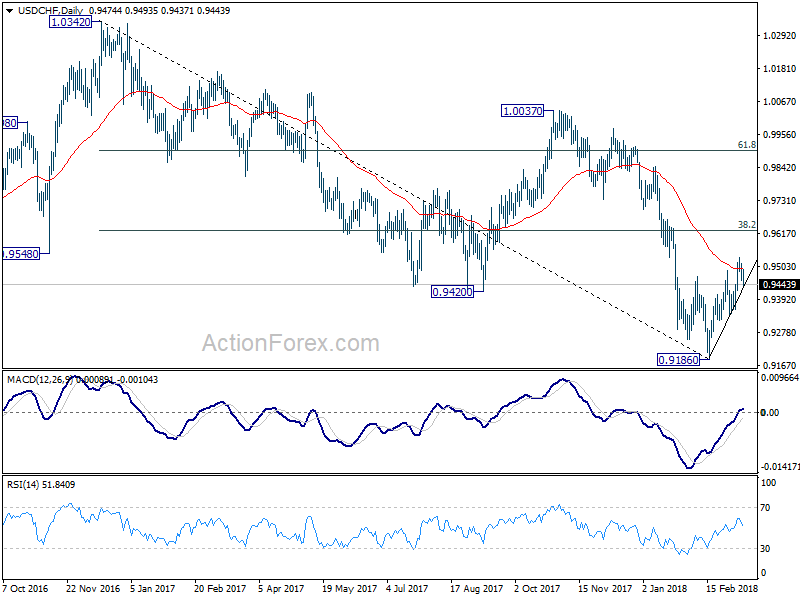

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

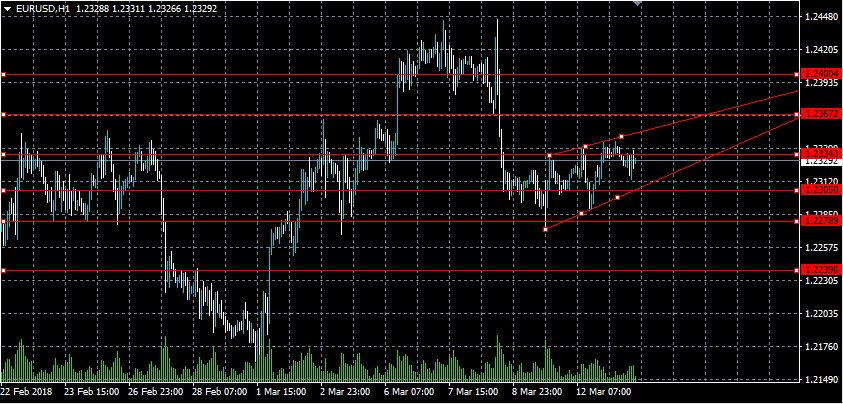

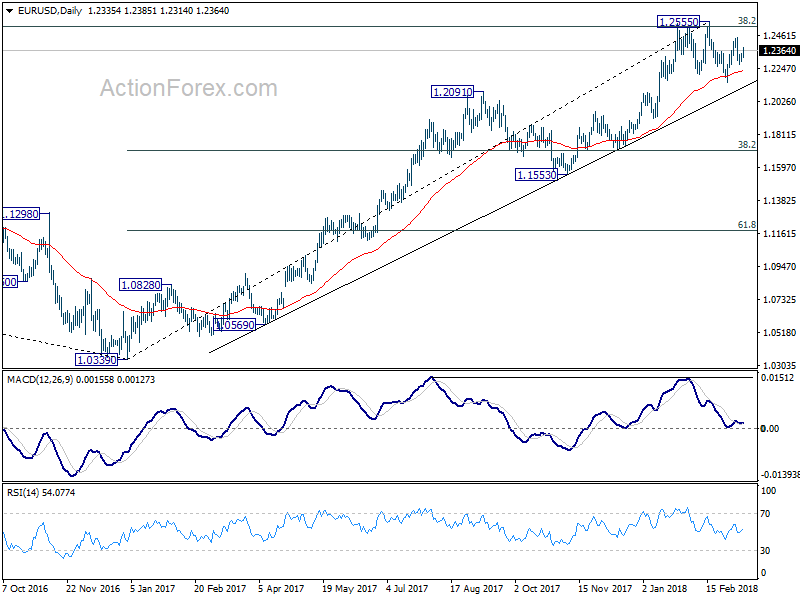

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2302; (P) 1.2323 (R1) 1.2357; More....

EUR/USD rebounds above 1.2268 minor support today. While intraday bias remains neutral, focus is back on 1.2445. Break there will turn bias back to the upside for 1.2555 high. Decisive break there will carry larger bullish implication. But again, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below.

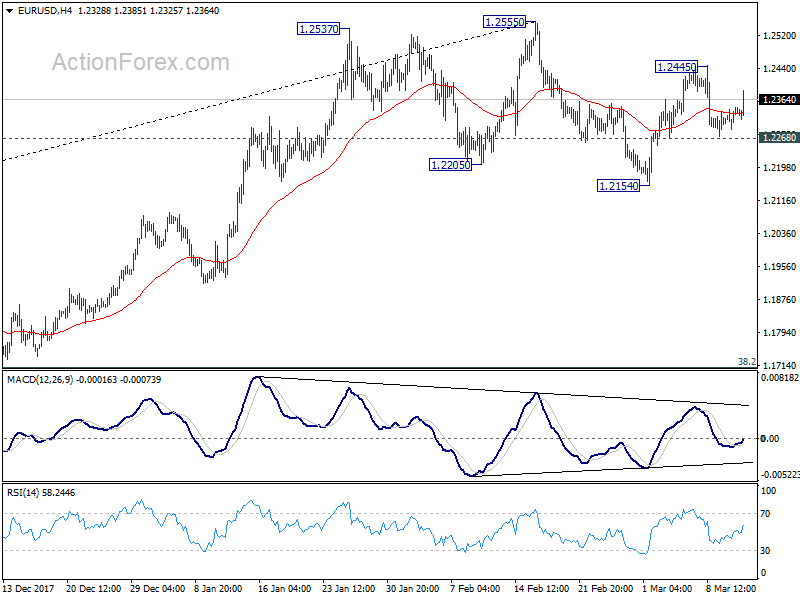

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

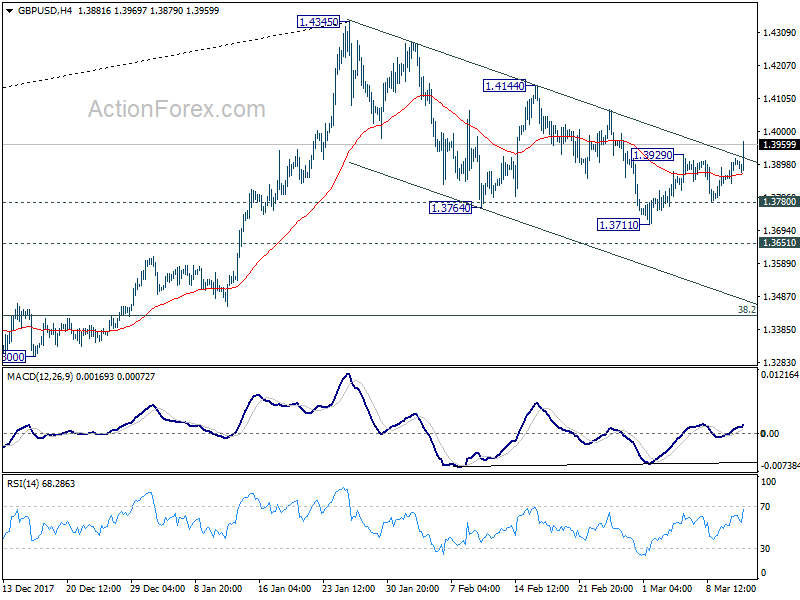

GBP/USD Mid-Day Outlook

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3858; (P) 1.3887; (R1) 1.3935; More....

GBP/USD's break of 1.3929 indicates resumption of rebound from 1.3711. The break of near term trend line resistance suggests that corrective pull back from 1.4345 has completed at 1.3711 already. Intraday bias is back to the upside for 1.4144 resistance first. Break should confirm this bullish case and target 1.4345 high and above. On the downside, below 1.3780 minor support will turn bias to the downside to extend the corrective fall from 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Dollar Selloff Restarts as CPI Just Met Expectation, Trump Fired Tillerson

Dollar suffers broad based selling in early US session as in-line with expectation CPI data is a relieve to market participants. Additional, the greenback is weighed down by political turmoil in the White House. Headline CPI accelerated to 2.2% yoy in February, up from 2.1% yoy and met expectation. Core CPI was unchanged at 1.8% yoy, also met expectation. The data will not change Fed's path to hike in March, likely in June too. But it doesn't give Fed any support to hike the fourth time in December.

Separately, it's reported that US Secretary of State Rex Tillerson is fired by President Donald Trump after clashes. Trump confirmed by tweeting "Mike Pompeo, Director of the CIA, will become our new Secretary of State. He will do a fantastic job! Thank you to Rex Tillerson for his service! Gina Haspel will become the new Director of the CIA, and the first woman so chosen. Congratulations to all!"

Technically, it now looks like EUR/USD has defended 1.2268 minor support and maintained mild near term bullishness. 1.2555 high is back in radar. GBP/USD took out 1.3929 resistance which affirms the case of near term reversal. AUD/USD's breach of 0.7892 minor resistance also adds to the case of near term bullish reversal in the pair.

ECB Lane expressed confidence on inflation hitting target

In Eurozone, ECB Governing Council member Philip Lane expressed his optimism that " our confidence that inflation will converge to the target over the medium term improves." While there are always talks of ECB stimulus exit in the markets, Lane emphasized that "whenever net asset purchases come to an end, there will still remain considerable monetary accommodation baked into the system." Regarding the Euro's exchange rate, he has "no concern about the current level". But Lane warned that " if it moves a lot within a short time interval then you have to think about the implications."

EU Barnier urged UK to "face up to the hard facts"

EU Chief Brexit negotiator Michel Barnier warned UK that "One cannot have at the same time the status of a third country and demand at the same time the advantages of the (European) Union." And UK should "face up to the hard facts". Meanwhile, Barnier is still hoping to seal a deal this month on a transition period after Brexit, and start talks on the future relationship this spring.

European Commission President Jean-Claude Juncker said in European Parliament that "there is increasing urgency to negotiate this orderly withdrawal." He added that "as the clock counts down, with one year to go, it is now time to translate speeches into treaties, to turn commitments into agreements." Meanwhile, he urged UK to provide "further clarity" regarding the future relationship.

Australia NAB business confidence jumped to record

Australia NAB business condition jumped 3 pts to 21 in February, hitting a record high. However, business confidence dropped 3 pts to 9. NAB noted in the release that "business activity in Australia is robust" and "strength in conditions is broad based across industry groups." The fall in confidence was seen as reactions to global market "turbulence" back in early February only. But the impact of those turbulence was "relatively limited".

Overall, NAB maintained that view that RBA will hike by late 2018, but may delay till early 2019. It noted that "we expect by late 2018 the RBA will feel relaxed enough about the domestic fundamentals to cautiously start withdrawing the stimulatory policy stance it is currently running. However, it will depend heavily on the data flow and the risk is that the RBA will delay rate rises until early 2019".

Also fro Australia, home loans dropped -1.1% mom in January.

RBNZ Spencer hailed macroprudential policy

RBNZ Governor Grant Spencer hailed the success of macroprudential tools in a speech to finance industry professional today. The policy infrastructure including the LVRs (loan to value restrictions). helped limit the risks of surge hour prices. It also helped keep interest low to boost inflation. And, after adopting the policy for five years, Spencer suggested a review would be run with the Treasury to consider ways to expand it. He also suggested to introduce a new committee on macroprudential policy alongside the monetary policy committee.

OCED warned: Avoid escalation on global steel excess problem

OECD forecast global economy to strengthen in 2018 and 2019. And, global GDP growth is projected to climb to 4%, up from 3.7% in 2017. US tax cuts and government spending, together with fiscal stimulus in German are the key drivers of the upward revision. However, inflation is expected only to "rise modestly". And there are risks from monetary policy normalization on exchange rates and capital flow, in particular in emerging markets. OECD also said that "Safeguarding the rules-based international trading system will help to support growth and jobs. Governments should avoid escalation and rely on global solutions to resolve excess capacity in the global steel industry."

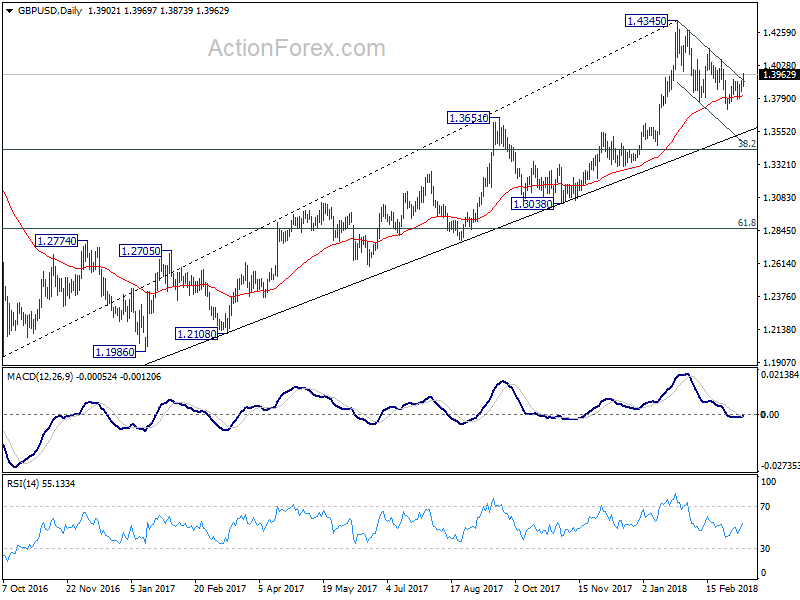

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3858; (P) 1.3887; (R1) 1.3935; More....

GBP/USD's break of 1.3929 indicates resumption of rebound from 1.3711. The break of near term trend line resistance suggests that corrective pull back from 1.4345 has completed at 1.3711 already. Intraday bias is back to the upside for 1.4144 resistance first. Break should confirm this bullish case and target 1.4345 high and above. On the downside, below 1.3780 minor support will turn bias to the downside to extend the corrective fall from 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Feb | 2.50% | 2.50% | 2.70% | |

| 00:30 | AUD | Home Loans M/M Jan | -1.10% | -0.20% | -2.30% | |

| 00:30 | AUD | NAB Business Conditions Feb | 21 | 18 | ||

| 00:30 | AUD | NAB Business Confidence Feb | 9 | 12 | ||

| 04:30 | JPY | Tertiary Industry Index M/M Jan | -0.60% | -0.30% | -0.20% | 0.00% |

| 12:30 | USD | CPI M/M Feb | 0.20% | 0.20% | 0.50% | |

| 12:30 | USD | CPI Y/Y Feb | 2.20% | 2.20% | 2.10% | |

| 12:30 | USD | CPI Core M/M Feb | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Feb | 1.80% | 1.80% | 1.80% |

More turmoil for USD, Rex Tillerson fired by Trump

More selling is seen in Dollar on news that US Secretary of State Rex Tillerson is fired by Trump.

Trump also tweeted:-

"Mike Pompeo, Director of the CIA, will become our new Secretary of State. He will do a fantastic job! Thank you to Rex Tillerson for his service! Gina Haspel will become the new Director of the CIA, and the first woman so chosen. Congratulations to all!"

Dollar selling starts as bears relieved by CPI data

US CPI met market expectation. Dollar bears seem to be "relieved" and fresh selling seen after the release

US CPI Jan: 0.2% mom vs exp 0.2% mom vs prior 0.5% mom

US CPI Jan: 2.2% yoy vs exp 2.2% yoy vs prior 2.1% yoy

US CPI core Jan: 0.2% mom vs exp 0.2% mom vs prior 0.3% mom

US CPI core Jan: 1.8% yoy vs exp 1.8% yoy vs prior 1.8% yoy

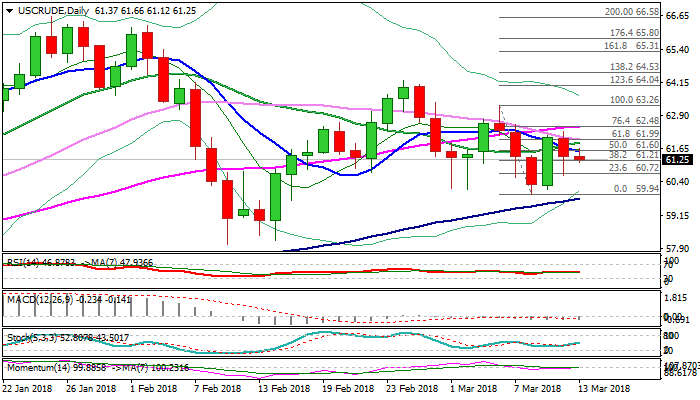

WTI OIL – Bearish Alignment But Daily Cloud Base Holds for Now; Supply Data in Focus

WTI oil maintains negative tone on Tuesday, pressured by news of another increase in US oil production.

Today’s action was so far contained by the base of thick daily cloud at $61.20 and is shaped in tight Doji candle.

Cloud base acts as solid support as Monday’s break below cloud on spike to daily low at $60.65, proved to be short lived, as the day closed above cloud base.

Daily techs re mixed, with MA’s holding above the price in bearish setup while Momentum and RSI are neutral.

Today’s action was so far capped by falling 10SMA which marks initial resistance at $61.57, followed by 20&30SMA’s at $61.87/$62.00, break of which will be more bullish. Negative scenario sees close below the cloud as bearish signal for extension towards cracked strong supports at $60.00 zone.

Oil supply data are in focus, with API crude stocks report due late today and EIA weekly crude stocks report due on Wednesday.

Res: 61.57; 61.87; 62.00; 62.49

Sup: 61.12; 60.72; 60.12; 59.94

Dollar Climbs ahead of US CPI Figures; European Stocks Edge Up

Here are the latest developments in global markets:

FOREX: Political scandals surrounding the Japanese Finance Minister regarding a discounted sale of state-owned land continued to pressure the yen during the European afternoon, sending dollar/yen to 107.60 (+0.80%) ahead of the release of US CPI figures which have the potential to alter risk appetite in the market. The dollar index edged up to 89.98 (+0.13%). Pound/dollar was moving sideways around 1.3880 (-0.12%), shrugging off remarks expressed by the EU Brexit negotiator Michel Barnier who said that the EU is open to UK ideas on avoiding a hard Irish border, but Theresa May’s stance keeps many EU doors closed. Euro/dollar gained a little, touching 1.2551 after the ECB’s board member, Philip Lane, talked down any concerns on the currency level, though, the gains were temporary, and the pair returned immediately to 1.2337 (+0.03%). Meanwhile, the President of the EU commission, Jean Claude Junker reiterated threats of retaliation against Trump’s protectionism, claiming that more clarity is expected from the US side in the coming days. Dollar/loonie stretched higher to 1.2867 (+0.23%) and aussie/dollar was flat at 0.7864 (-0.09%). Kiwi/dollar picked up speed towards a fresh two-week high of 0.7320 before it slipped to 0.7320 (+0.34%) following encouraging comments by the RBNZ acting governor, Grant Spencer, who backed the central bank’s current macroprudential policy, explaining that the usage of those tools limited risks of a hot housing market.

STOCKS: European stocks inched higher as of 1030 GMT. The pan European STOXX 600 and the blue-chip Euro STOXX were up by 0.06% and 0.10% respectively, with energy sectors leading the gains. The German DAX 30 rose by 0.16%, the French CAC 40 improved by 0.46%, the Italian FTSE MIB climbed by 0.40% and the Spanish IBEX 35 surged by 0.83%. The UK’s FTSE 100 was steady, while US stock futures were pointing to a positive open.

COMMODITIES: Oil prices edged higher at 1045 GMT following a suspension of crude loadings in a key port in Libya, despite concerns over rising US oil production. Yesterday, the US Energy Information Administration said in its monthly report that the US oil shale production is expected to reach a record high in April. WTI crude and Brent were last trading at $61.58 (+0.40%) and $65.09 (+0.25%) per barrel respectively. In precious metals, gold stood at $1318.30 (-0.29%) per ounce, near intraday lows.

Day ahead: US CPI data to warn on inflation; UK’s Finance Minister issues Spring Statement

US consumer prices will be in focus later today at 1230 GMT in the absence of any other major economic releases. The headline CPI rate for the month of February is expected to inch up to 2.2% in yearly terms compared to 2.1% seen in January and the core equivalent which excludes volatile products such as food and energy is anticipated to remain steady at 1.8% y/y. While this is not the Fed’s preferred inflation measure – that would be the Personal Consumer Expenditure index – it would be the only evidence on prices ahead of the two-day FOMC policy meeting next week. Therefore, any upside surprise in the numbers could revive inflation fears and increase chances for four rate increases compared to three currently priced in the markets. In this case, the dollar could extend today’s gains. On the other hand, if CPI misses predictions, investors could doubt any significant rise in inflation pressures, pushing the dollar lower. Note that Friday’s NFP wage component came in below estimations, spreading speculations that inflation could remain below the Fed’s 2.0% target for longer.

In other data releases, the Westpac Banking Corporation will report on Australia’s consumer confidence for the month of March at 2330 GMT, while a few minutes later, at 2350 GMT Japan will publish readings on core machinery orders at 2350 GMT. After a sharp fall in December, analysts see a strong rebound in January’s manufacturing orders with the yearly gauge surging by 5.3% y/y. At the same time, the Bank of Japan will issue minutes of its policy meeting held on January 22-23.

In the UK, the Finance Minister, Philip Hammond, will unveil the latest economic forecasts in front of the Parliament at 1230 GMT as part of his Spring Statement. Expectations are for Hammond to give an upbeat tone on the country’s financial health, but he may postpone providing many details until the more important Autumn statement later this year. Traders will keep a close eye on any Brexit comments after the UK’s junior Brexit minister said that the EU and the UK are very close to reaching an agreement on the transition period.

In energy markets, investors will look to the private API inventory data at 2030 GMT, in order to gauge whether US production has really peaked, for the time being, something signaled by the decline in the Baker Hughes oil rig count on Friday.

In politics, all eyes will be turned to the US, where a special election will be held in Pennsylvania for an open seat in the House of Representatives. While a single House seat is usually not very important in US politics, this time is different. Back in 2016, Trump and the Republicans won this district by a landslide, but opinion polls now suggest that the Republican and Democratic candidates are running neck and neck. If the Democratic contender wins or comes close to winning, that would be a clear sign that the Republicans are at risk of losing districts they won easily in 2016. Such an outcome could heighten speculation that the Republicans may lose control of Congress at the mid-term elections later this year.

Canadian Dollar Slightly Higher Ahead Of US PPI Reports

USD/CAD has ticked higher in the Tuesday session. In North American trade, USD/CAD is trading at 1.2869, up 0.20% on the day. On the release front, there are no Canadian indicators for a second straight day. Bank of Canada Stephen Poloz will speak at an event in Kingston, Ontario. The US publishes CPI and Core CPI for February, both of which are forecast to slow to 0.2%.

The Canadian dollar had a winning week, boosted by strong job numbers on Friday. The Canadian economy added 15.4 thousand jobs in February, after a sharp decline of 88 thousand a month earlier. This was below the estimate of 21.3 thousand, but investors were pleased with the strong turnaround. South of the border, employment numbers were a mix on Friday. Wage growth dropped to 0.1% in February, down from 0.3% a month earlier. This missed the estimate of 0.2%, and marked the lowest gain in four months. The news was much better from nonfarm payrolls, which soared to 313 thousand, crushing the estimate of 205 thousand.

The markets are keeping a close eye on the Federal Reserve, which holds its next policy meeting next week. The Fed is widely expected to raise rates for the first time this year, but the real question is how many hikes we’ll see in 2018. The Fed projection remains at three rate hikes, but strong economic data, especially from inflation indicators, could push the Fed to raise its forecast. Higher US interest rates makes the greenback more attractive to investors. With the Canadian economy showing more slack than its neighbor, and the uncertainties swirling around the future of NAFTA, it’s unlikely that the Bank of Canada will be able to match the Fed pace of rate hikes, meaning that strong headwinds could lay ahead for the Canadian currency.

EURO Breakout Looms On U.S CPI Report

The euro currency remains in consolidation mode against the U.S dollar, ahead of today’s key monthly CPI inflation report from the United States economy. The EURUSD pair is moving in an increasingly tight trading-range, with price-action likely to soon perform a clear technical breakout. EURUSD buyers look for continued gains above the 1.2334 technical level, whilst EURUSD sellers look for sustained losses below the 1.2305 support level.

The EURUSD pair is likely to see further buying above the 1.2334 level, upside targets are found at the 1.2367 and 1.2400 levels.

If the EURUSD pair moves below the 1.2305 level on a sustained basis, a deeper sell-off towards the 1.2278 and 1.2239 support level seem likely.