Sample Category Title

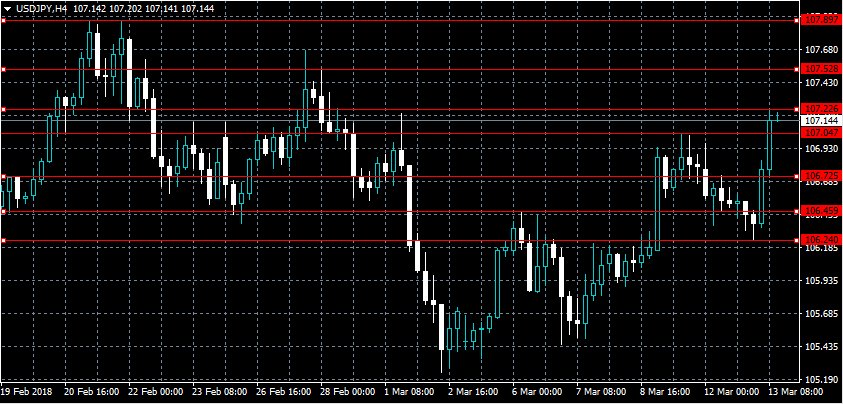

USDJPY Intraday Bullish Above 106.72 Level

The U.S dollar has recovered bullish upside momentum against the Japanese yen, with price-action so far trading to an intraday high of 107.22. The USDJPY pair has recently been moving in lockstep with the direction of U.S and Japanese equity markets, losing its correlation to the overall U.S dollar index. The release of today’s February CPI inflation report from the U.S economy, will likely be the catalyst for the next directional move in the USDJPY pair.

The USDJPY pair remains intraday bullish whilst trading above the key 106.72 level, further upside towards the 107.52 and 107.89 levels seem possible.

Should the USDJPY pair move below the 106.72 level, a correction back towards 106.45 and 106.22 support levels remains possible.

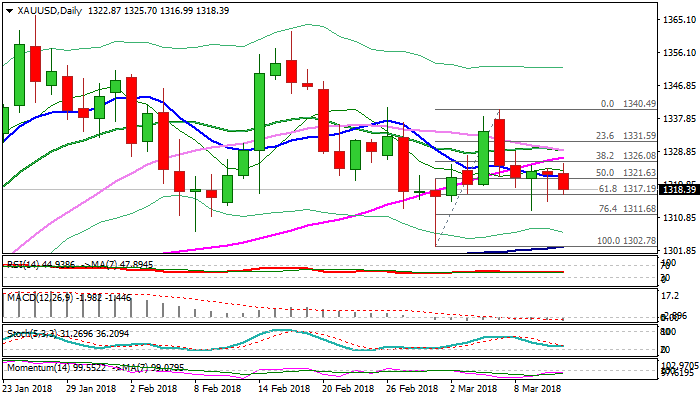

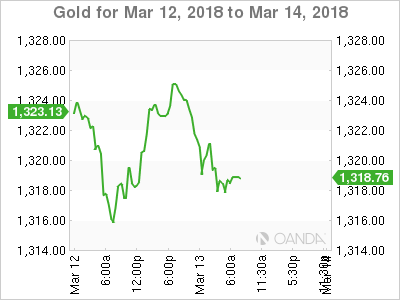

Technical Outlook: Spot Gold Looks For Direction Signal On Break Out Of $1313/26 Range

Spot Gold holds in red in European session on Tuesday after extension of previous day's recovery stalled at $1325 in early Asian trading. Fresh weakness pressures cracked support at $1317 (Fibo 61.8% of $1302/$1340 rally), firm break of which would generate fresh bearish signal for extension of bear-leg from $1340 (07 Mar high). Near-term price action is entrenched within $1313/26 range for the third straight day and requires direction signal on break of either side of the range. Repeated strong downside rejections in past two days suggest that downside attempts lack momentum for final break lower, while the upside was repeatedly capped by 55SMA and broken Fibo 38.2% level. Daily techs are bearishly aligned and keep negative near-term bias, however, require firmer signal for confirmation, which could be generated on today's US CPI data.

Res: 1324, 1326, 1330, 1332

Sup: 1317, 1313, 1311, 1307

US Futures Edge Higher Ahead Of Inflation Data

- Markets Gradually Recovering But Remain Vulnerable;

- CPI Data Key Ahead of Next Week’s Fed Meeting;

- UK Spring Statement Likely to Be a Very Forgettable Event.

Markets Gradually Recovering But Remain Vulnerable

The next 24 hours will be of particular interest to traders in what is otherwise expected to be a relatively quiet week, with US inflation and retail sales data in focus.

US markets continue to gradually recovery from the sharp sell off at the start of February, which at the time was triggered by fears over a faster pace of tightening from central banks. While investors appear to be coming to terms with the idea of more rate hikes, some caution remains, especially as this has also come at a time when Donald Trump is threatening a trade war with countries that don’t improve the terms of trade for the US.

Investors may be coming around to the idea of more rate hikes but as we have seen over the last month or so, with volatility remaining elevated and indices off their record highs, they’re not exactly thrilled with the idea. That should make next week’s Federal Reserve meeting all the more interesting, as we’ll get a better idea what policy makers are expecting this year, with new economic projections being released.

CPI Data Key Ahead of Next Week’s Fed Meeting

Today’s inflation release – while not being the Fed’s preferred measure – will offer some insight into the direction of travel for US prices at a time when the labour market is tight and tax reform is providing an additional stimulus. As we saw on Friday though, there may be more slack in the labour market than the central bank was factoring in and so traders and policy makers will be looking at wages and inflation data for clear signs that the data is confirming their forecasts.

I’m not sure a slight uptick in inflation to 2.2% and core inflation remaining at 1.8% will provide policy makers with much comfort or confidence next week but they may be encouraged that it is at least headed in the right direction. A miss on the other hand, on top of Friday’s report, may give policy makers reason to hold up on revising up interest rate expectations next week, which could weigh on the dollar and support stocks in the near-term.

UK Spring Statement Likely to Be a Very Forgettable Event

The other event of note today will be the Spring Statement in the UK, in which Chancellor Philip Hammond will provide new forecasts for the economy and an update on the public finances. While this has historically been the time of year when the Chancellor announces changes to spending and taxation, that’s changed as of this year and will now take place in the Autumn which will likely make today more of a forgetful affair.

Hammond is expected to announce that the UK grew more than previously expected and tax receipts have also been higher, something he’ll be keen to stress is a result of the government’s fiscal prudence. This is likely to be more of a self-congratulatory affair despite the hopefulness of some that the Chancellor will ease the austerity a little as a result of the better than expected financial situation. Those hoping for more money for public services which have been strained for years are likely to be disappointed, with any decision on this likely put off until the Autumn budget.

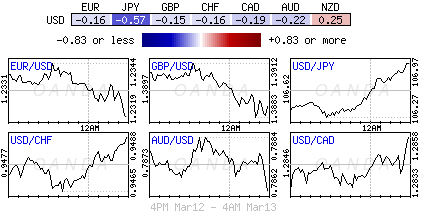

Into US session, Yen selling stays, Euro buying emerges

Yen is staying as the weakest currency for today and selling intensifies entering into European. Meanwhile, Euro is also showing much resilience. And buying also emerges at during the 4 hour period.

Markets Look For A Second Opinion On U.S Inflation

Tuesday March 13: Five things the markets are talking about

European equities are drifting following a mixed session in Asia and the ‘mighty' U.S dollar is steady as capital markets wait for this morning's U.S inflation report for clues on the pace of Fed policy-tightening. Treasury yields have nudged a tad higher, while oil has slipped again.

This morning's U.S CPI (08:30 am EDT) could confirm that U.S inflation remains tepid, even as the job market remains tight. Last Friday's Labor Department report showed that U.S wages rose +2.6% y/y in February, below expectations, while the annual wage gain in January was revised down to a +2.8% increase.

Note: The market will also be looking to reports on wholesale prices and retail sales (Mar 14) for guidance ahead of next week's FOMC meeting (Mar 20-21). The Fed is expected to hike rate +25 bps and is scheduled to release their updated forecasts for the path of monetary policy (dot plot) and economic growth.

Politics again is a market focus after President Trump issued an executive order blocking Broadcom from acquiring Qualcomm, thwarting a +$117B hostile takeover in the name of U.S national security.

On tap: China data on industrial production, retail sales and fixed-asset investment are all out on Wednesday and are expected to point to slower growth.

1. Stocks mixed results

In Japan, equities rallied for a fourth consecutive session overnight as a weaker yen (¥107.07) triggered buying, offsetting any weakness in steelmakers and automakers still battered by concerns about U.S tariffs on imported steel and aluminum. The Nikkei average gained +0.7%, while the broader Topix added +0.6%.

Down-under, Australia's S&P/ASX 200 slipped -0.4% on weakness in major mining and oil stocks, while in S. Korea, the Kospi closed out +0.4% higher, supported mostly by Samsung's +3.9% gain.

In Hong Kong, stocks ended little changed on Tuesday as investors considered the impact of a government reshuffle on the mainland. China is merging its banking and insurance regulators and giving new powers to policymaking bodies such as the People's Bank of China (PBoC) in the biggest government shake-up in years. At close of trade, the Hang Seng index was flat, while the Hang Seng China Enterprises index rose +0.4%.

In China, stocks broke a three-day winning streak and ended lower, weighed down by healthcare and consumer stocks and the impact of a government reshuffle. At the close, the Shanghai Composite index was down -0.5%, while the blue-chip CSI300 index was down -0.9%.

In Europe, regional indices trade higher across the board following the mixed session in Asia. Stateside, shares of Qualcomm will be in focus after receiving a presidential order prohibiting Broadcom's proposed takeover.

U.S stocks are set to open in the ‘black' (+0.2%).

Indices: Stoxx600 +0.1% at 379.6, FTSE flat at 7215, DAX +0.2% at 12437, CAC-40 +0.5% at 5301, IBEX-35 +0.8% at 9800, FTSE MIB +0.4% at 22846, SMI +0.1% at 8979, S&P 500 Futures +0.2%

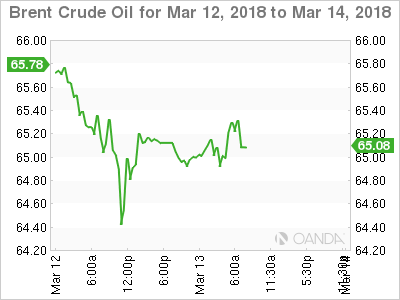

2. Oil prices dip on rise in U.S crude output, gold lower

Oil prices have dipped overnight, extending Monday's losses, as the relentless rise in U.S crude output continues to weigh on the market.

Brent crude futures are at +$64.77 per barrel, down -18c, or -0.3%. U.S West Texas Intermediate (WTI) crude futures are at +$61.18 a barrel, down -18c, or -0.3% from Monday's close.

Note: Both crude benchmarks dropped by around -1% in yesterday's session.

Nevertheless, global healthy demand and ongoing supply restraint by OPEC and Russia is preventing much deeper pullbacks presently. However, U.S production is expected to rise above +11m bpd by late 2018, taking the top spot from Russia, according to IEA.

In it's monthly report yesterday, the EIA noted that the rising U.S output comes largely on the back of onshore shale oil production. Production from major shale formations is expected to rise by +131k bpd in April from the previous month to a record +6.95m bpd.

Traders will take their cues form this week's U.S inventory reports.

Ahead of the U.S open, gold prices are under pressure on a firmer dollar as the market waits for this morning's U.S consumer price data to gauge the outlook for inflation and the Fed's rate hike stance. Spot gold is down -0.2% at $1,319.87 per ounce.

3. Sovereign yields look for guidance

Euro zone sovereign bond yields are little changed, as investors continue to brace themselves for this week's hefty bond supply as well as today's U.S inflation data that could provide clues on the pace of monetary tightening from the Fed.

European bond markets have been well supported since last Thursday's ECB, with policy makers stressing that interest rates will remain “low for some time” even as they take tentative steps towards exiting QE.

Today's inflation data is particularly important, as many analyst are forecasting the Fed will raise interest rates four times this year, compared with the three increases policy makers have penciled in at their December meeting.

Note: Should the Fed signal they intend to accelerate the pace of monetary tightening, it could give a boost to the dollar, which had declined -2.5% in 2018.

A headline print that misses or meets estimates is likely to reaffirm the case for three-rate hikes this year and give the green light to fresh appetite for risk assets.

The yield on U.S 10-year Treasuries has increased +1 bps to +2.88%. In Germany, the 10-year Bund yield has climbed less than +1 bps to +0.63%, while in the U.K; the 10-year Gilt yield is unchanged at +1.494%, the highest in a week.

4. Dollar looks for direction

The USD is little changed against G10 currency pairs with the focus turning to today's U.S CPI data.

GBP/USD (£1.3880) is a tad softer ahead of Chancellor of Exchequer Hammond “Spring Statement” (07:30 am today). Dealers note that the commentary would most likely influence Gilt prices the most, as less issuance is expected throughout the current fiscal year due to higher U.K tax receipts.

USD/JPY (¥107.16) is higher by +0.6% above the psychological ¥107 handle for its best session in five-months with the USD aided by yesterday's U.S Treasury auction results – the highest 3-year bond yield in 11-years.

The market remains on Japanese political watch – Japan's Fin. Min. Aso mighty skip the G20 finance minister meeting in Buenos Aires later this month with calls for his resignation following the recent shenanigans surrounding the cover-up of a government land sale.

Elsewhere, the EUR is little changed, trading atop of €1.2326, while the ZAR declined -0.2% to $11.8403.

5. U.S small business economy heats up

Data this morning from the NFIB (The National Federation of Independent Business) showed that U.S small business owners are showing strong confidence in the economy as the optimism index continues at record high numbers, rising to 107.6 in February vs. 107.1 (e).

The historically high numbers include a jump in small business owners increasing capital outlays and raising compensation. The federation supports +350k small U.S companies.

According to NFIB CEO, Juanita Duggan, “the historically high readings indicate that policy changes – lower taxes and fewer regulations – are transformative for small businesses. After years of standing on the sidelines and not benefiting from the so-called recovery, Main Street is on fire again.”

ECB Lane: Confidence on inflation improves

ECB Governing Council member Philip Lane:

"There's no concern about the current level,"

- "But if it moves a lot within a short time interval then you have to think about the implications."

- "As these factors convert into higher inflation readings, our confidence that inflation will converge to the target over the medium term improves,"

- "Whenever net asset purchases come to an end, there will still remain considerable monetary accommodation baked into the system,"

EU Barnier hopes to seal a transition Brexit deal this month

EU Chief Brexit negotiator Michel Barnier warned UK:-

- The EU and Britain are hoping to seal a deal this month on a transition period after Brexit, and start talks on the future relationship this spring.

- "One cannot have at the same time the status of a third country and demand at the same time the advantages of the (European) Union,"

- "It is time to face up to the hard facts,"

Earlier today, European Commission President Jean-Claude Juncker in European Parliament on Brexit:-

- "There is increasing urgency to negotiate this orderly withdrawal."

- "As the clock counts down, with one year to go, it is now time to translate speeches into treaties, to turn commitments into agreements."

- "It is obvious that we need further clarity from the UK if we are to reach an understanding on our future relationship."

DAX Ticks Higher, Investors Eye German CPI

The DAX index has posted slight gains in the Tuesday session. Currently, the DAX is trading at 12,434.53, up 0.13% on the day. In economic news, there are no eurozone or German indicators for a second straight day. On Wednesday, ECB President Mario Draghi will speak at an ECB conference in Frankfurt and Germany releases Final CPI.

Despite the turbulence surrounding US President Trump’s controversial decision to slap tariffs on steel imports, eurozone stock markets enjoyed a strong week, and the DAX surged with a 4.4% gain. There was concern on the part of investors over the tariffs, which generated harsh criticism from the EU. However, Trump has exempted Canada and Mexico from the tariffs, and has said that Washington could ease the duties on other countries as well. Importantly, there is strong domestic opposition to Trump’s move, including senior Republican lawmakers who have said they will work to overturn the tariffs, which could spark an all-out trade war. So far, the markets are confident that a solution to the tariff tussle will be found.

Is the German industrial sector in trouble? Last week’s numbers were surprisingly soft. Factory Orders in January plunged 3.9%, worse than the estimate of -1.9%. This marked the second decline in the past three months. This was followed Industrial Production, marking a second straight decline. Still, the German economy has performed well, and has led the impressive recovery in the eurozone.

EUR/USD – Euro Trading Sideways, US Inflation Report Next

It continues to be a quiet week for the euro. Currently, EUR/USD is trading at 1.2439, up 0.05% on the day. On the release front, there are no eurozone or German indicators on the schedule. The US will release CPI and Core CPI, both of which are expected to slow to 0.2%. On Wednesday, ECB President Mario Draghi will speak at an ECB conference in Frankfurt and Germany releases Final CPI. The US will release key inflation and consumer spending reports.

US employment numbers were a mix on Friday. Wage growth dropped to 0.1% in February, down from 0.3% a month earlier. This missed the estimate of 0.2%, and marked the lowest gain in four months. The news was much better from nonfarm payrolls, which soared to 313 thousand, crushing the estimate of 205 thousand. The mixed readings have eased concerns about the Fed raising rates four times in 2018.

Is the German industrial sector in trouble? Last week's numbers were surprisingly soft. Factory Orders in January plunged 3.9%, worse than the estimate of -1.9%. This marked the second decline in the past three months. This was followed Industrial Production, marking a second straight decline. Still, the German economy has performed well, and has led the impressive recovery in the eurozone.

Are Britain and the European Union heading towards a showdown? Last week, Donald Tusk, president of the European Council, advised Prime Minister May to 'pink' her red lines on Brexit, if Britain wants to maintain a close economic relationship with the bloc. May has insisted that there will be no customs union, and the European Court of Justice will have no jurisdiction over the UK. May set out these positions after the EU published its draft negotiating guidelines for Brexit, and the guidelines warned of 'negative economic consequences” if Britain does not soften its position. Tusk added that he does not want to build a wall with Britain, and the EU could offer Britain a free trade agreement, with zero tariffs. At the same time, Tusk warned that Brexit will make trade between the two sides 'complicated and costly” and the EU would not allow Britain to cherry pick in any future trade arrangement. EU members are expected to sign off on the negotiating guidelines at a summit in late March, which could trigger a nasty response from the May government.

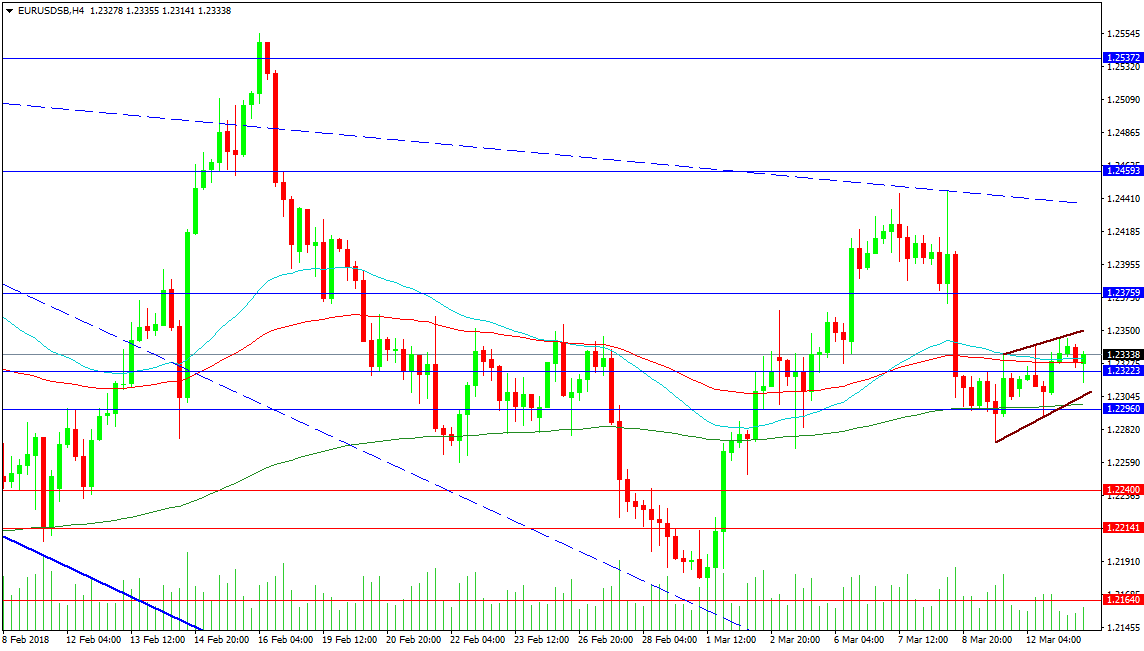

Forex Analysis: EURUSD And GBPJPY

The EURUSD pair has managed to find support and resistance at previously broken trend lines and has pulled back to the 1.23000 level, forming what looks to be wedge across it. This can happen around important levels as sellers and buyers battle for control. The wedge can be a continuation pattern but can also cause a reversal. Until price breaks the pattern and points out its intentions patience is required to avoid being caught in a position against the move. US Consumer Price Index data later today, at 12:30 GMT, is a possible trigger for a breakout. The resistance trend line is found at 1.23492 currently, with the 1.23759 level beyond. The previously broken trend line is found at 1.24380, with the 1.24593 level above. Recent highs are found at 1.25549.

Support is found at the pattern bottom (1.23037). On the 4-Hour chart, the moving averages are quite flat, suggesting that price is building energy for a break out at some point in the future. The 200-period MA is at 1.22993, with the 1.22960 level close by. Further support is found at 1.22400 and 1.22141, with the 1.21640 beyond.

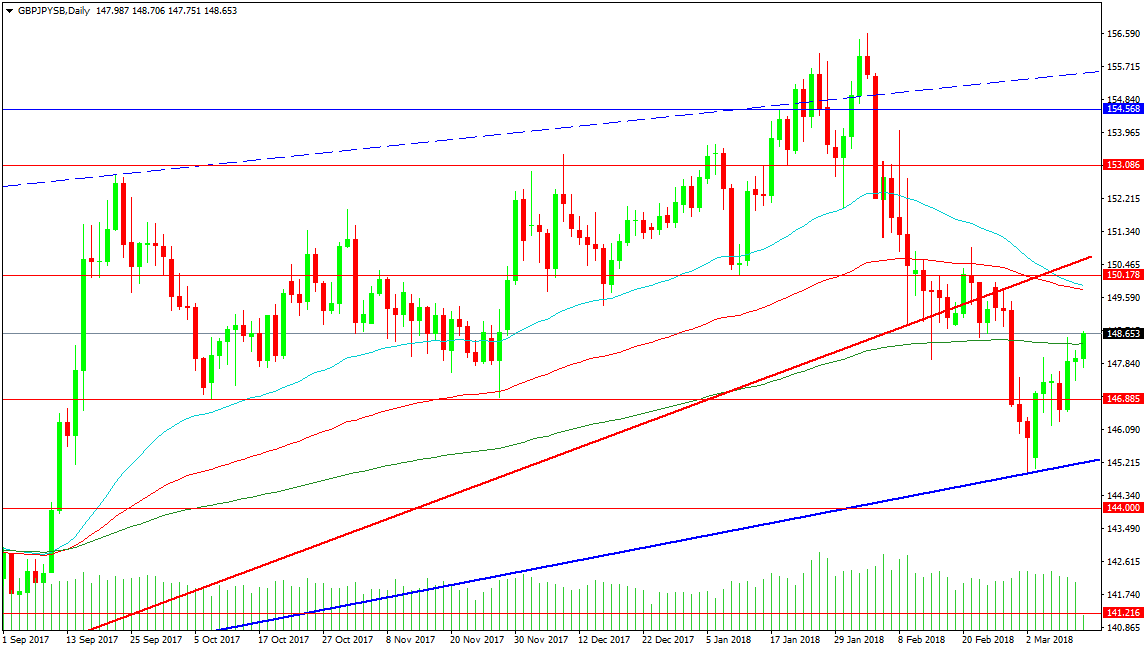

GBPJPY

This pair is moving higher after finding support at the rising blue trend line at 144.842. Support can be seen at the 200 DMA at 148.365, with 146.885 below. The supportive trend line is found at 145.213, with the 144.000 area underneath. A drop below this area would see price move towards 141.216.

Resistance at the 50 and 100 DMAs is found around 149.816 on the daily chart. The 150.178 level is reinforcing the rising red trend line at 150.537. The next key resistance level comes at 153.000, with 154.568 on the way to the broken trend line at 155.500. The 2018 highs are located at 156.597.