Sample Category Title

USD/JPY Bullish Consolidation

USD/JPY has now entered in a short-term bullish momentum, heading higher along the 106.70 range. Hourly support and resistance are given at 104.97 (11/10/2016 high) and 107.27 (25/02/2018 high). The bearish pattern started in January 2018 is maintained. The short-term technical structure suggests short-term increase.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades largely below its 200 DMA.

GBP/USD Lack Of Follow-Through

GBP/USD momentum is fading following its descent at 1.3782. The pair is trading between hourly support and resistance at 1.3678 (12/01/2018 low) and 1.3945 (19/01/2018 high). The technical structure suggests short-term increase.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Rising Slowly

EUR/USD keeps pushing higher and is now consolidating. Hourly support and resistance are given at 1.2112 (12/01/2018 low) and 1.2475 (31/01/2018 high). The technical structure suggests further short-term sideway moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Improving Risk Sentiment Weighs On Safe-Haven Assets

Quiet FX market ahead of US CPI

The CPI surprised to the upside in January as the headline gauge printed at 2.1%y/y versus 1.9% expected, while the core measure, which excludes the most volatile components came in at 1.8%y/y versus 1.7% median forecast. Investors reacted quite strongly as they adjusted their positioning in anticipation of a steeper monetary policy path. This surprise triggered a US dollar rally but it was ephemeral as retails sales came in well below expectation. However, today is another story.

According to the latest survey, market participants do not expect that those conditions have persisted in February. The core measure is expected to stabilise at 1.8%y/y, while the headline gauge should increase slight to 2.2%y/y from 2.1% in January. Unlike last month, February retail sales will not be released on the same day. It means that traders will most likely react strongly in case of a surprise reading. Indeed, February retail sales will be release tomorrow.

This is the last CPI report before the March FOMC meeting; it will therefore be closely monitored. We remain sceptical about another upside surprise in inflation reading. The risk to the core CPI is roughly balanced with slight downward skew. Since the beginning of the week, EUR/USD has been trading sideways around 1.2420. The closest resistance lies at 1.2446 (high from March 8th), while on the downside a support can be found at 1.2273 (low from March 9th). We maintain our bullish medium-term view on the pair. However, we expect that the greenback will appreciate against the Swiss franc and the Japanese yen as investors continue to load on risk.

Stronger CAD supported by a comforting job report

5.80%, a level that was not seen since the 1970s. February Net change in employment is estimated at 15’400 following January decline at -88’000, mainly boosted by an increase in part-time jobs and decline in full-time positions while Canadian hourly earnings remained solid, valued at 3.10% (previous: 3.30%), signalling a deceleration in the job market, just like the world economy.

As ongoing negotiations between Trump’s administration and its neighbour commercial partners concerning NAFTA trilateral agreements continue, we see the former as a key driver for the foreseeable future of Canadian economic health. In any case, if no agreements are found, Canada and Mexico will be subject to US tariffs on steel and aluminium, losing their privileged treatment.

Currently trading at 1.2855, USD/CAD remains stable since the beginning of the year (YTD: +2.47%), approaching its hourly resistance at 1.3015 (07/05/2017 high) and expected to become event-driven for the periods to come.

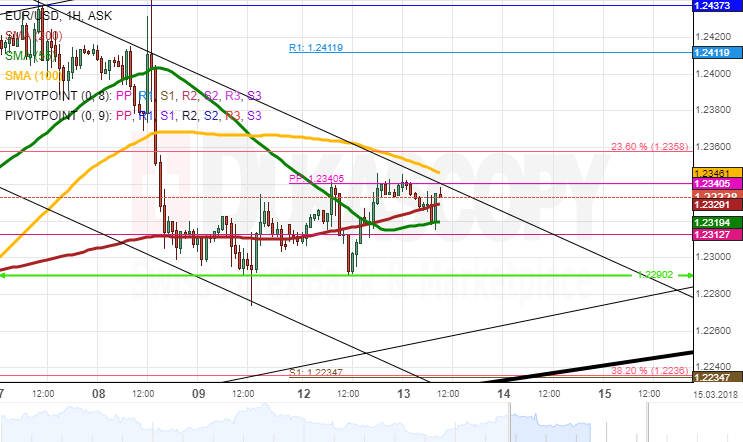

EUR/USD Analysis: Finds Support

The Euro was fluctuating in the 1.2343/1.2260 range on Tuesday, thus continuing its general movement sideways which began following weak US employment data last Friday.

The first part of today is likely to remain quiet, as traders are awaiting US inflation report released at 1230GMT. Thus, the Euro could trade in a narrow range between the 55-, 100– and 200-hour SMAs during this time. Resistance is likewise reinforced by the weekly PP.

A breakout is likely to determine the pair's subsequent direction until Wednesday morning. In case 1.2360 surrenders, the Euro should try pushing for the 1.24 area.

Conversely, the prevalence of the bearish sentiment could result in a test of the 1.2250 territory where the weekly S1, the 38.20% Fibo retracement and the senior channel are located.

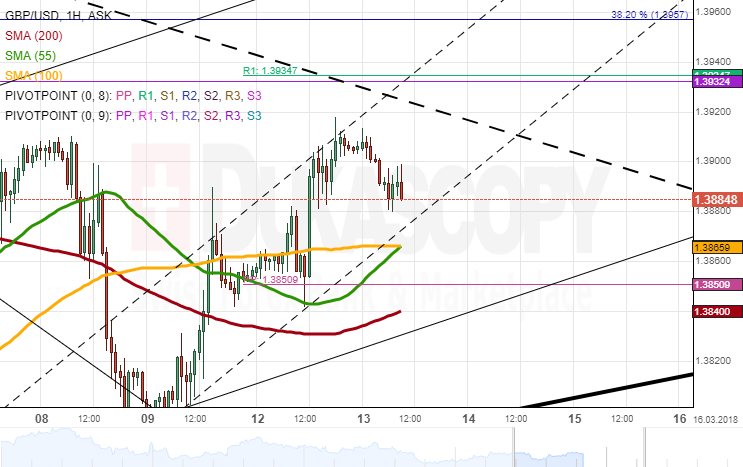

GBP/USD Analysis: Approaches Trend-Line

As previously expected, the Pound continues moving closer to a downward-sloping trend-line located near the 1.3910 mark for the third consecutive session. A 20-pip surge mid-Monday added some ground to the bullish sentiment, thus pushing the rate up to the 1.39 mark.

The Asian session began with a slight decline for the Sterling that is likely to continue until the British Annual Budget Report and the US CPI published at 1130GMT and 1230GMT, respectively, introduce changes to the overall market sentiment.

In general, it is likely that fundamentals, especially the second event, dominate the market during the second part of the day. A possible trading range is the 55– and 100-hour SMAs and the weekly PP at 1.3850 from below and the weekly R1 and the monthly PP at 1.3935 from above.

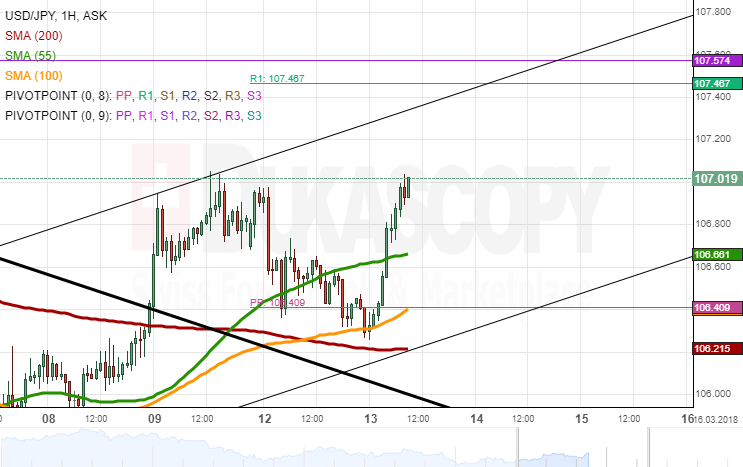

USD/JPY Analysis: Gains Momentum Early On Tuesday

Minor downside risks dominated the USD/JPY exchange rate on Monday, as it closed the session with a 60-pip fall.

The lack of bearish stimulus did not allow the Greenback to breach the combined support of the 100– and 200-hour SMAs circa 106.20. Thus, the Asian session started with a solid surge which erased all losses accumulated during the previous day.

The pair is currently trading in a two-week ascending channel. Given that its lower boundary was not reached yesterday, the pair could reverse significantly its current market sentiment and go for a test of this line, the weekly PP and the 100-hour SMA at 106.40 during the first part of the day. The remaining session is likely to be dominated by the US inflation data released at 1230GMT.

OECD: Global growth to strengthen in 2018, 2019

OECD Interim Economic Outlook: GETTING STRONGER, BUT TENSIONS ARE RISING

The world economy will continue to strengthen in 2018 and 2019, with global GDP growth projected to rise to about 4%, from 3.7% in 2017.

Stronger investment, the rebound in global trade and higher employment are helping to make the recovery increasingly broad-based.

New tax reductions and spending increases in the United States and additional fiscal stimulus in Germany are key factors behind the upward revision to global growth prospects in 2018 and 2019.

Inflation remains low, but is likely to rise modestly.

Still-elevated risk-taking and high debt levels in many countries raise financial vulnerabilities. Monetary policy normalisation could also result in greater volatility of exchange rates and capital flows, particularly in emerging market economies.

Medium-term growth prospects remain much weaker than prior to the financial crisis, reflecting less favourable demographic trends and a decade of sub-par investment and productivity.

Economic policies face several challenges:

- A gradual normalisation of monetary policy is needed, but to a varying degree across the major economies. Continued clear communication about the path to normalisation is essential to minimise the risk of financial market disruptions.

- Fiscal policy choices should avoid being excessively pro-cyclical and be clearly focused on measures that strengthen the prospects for sustainable and more inclusive medium-term growth.

- Structural reform efforts should be revived, seizing the opportunity of the stronger economy to help secure a more robust recovery of productivity, investment and living standards.

Safeguarding the rules-based international trading system will help to support growth and jobs. Governments should avoid escalation and rely on global solutions to resolve excess capacity in the global steel industry.

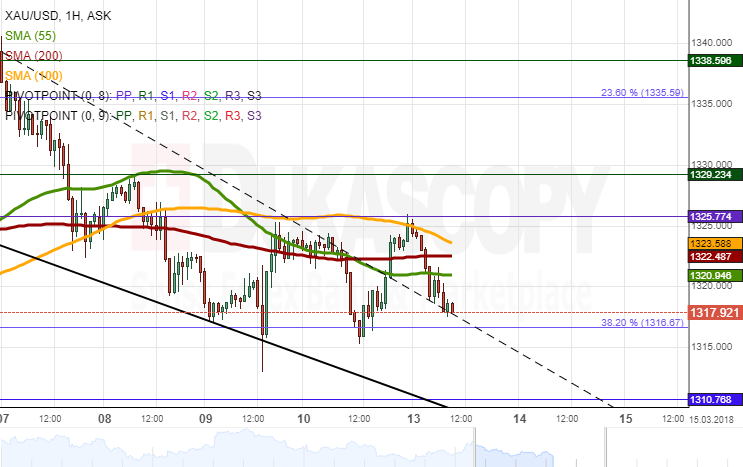

XAU/USD Analysis: Fails To Overcome 1,325.00

Following two sessions of decline, the yellow metal has allayed its bearish sentiment. The first part of Monday's session was very calm, as the bounds of the 55-, 100– and 200-our SMAs limited more extensive movements. Additional volatility was introduced later in the day; however, the aforementioned SMAs still remained the main limiting factor for the pair.

Technical indicators are strongly bearish, thus pointing to a possible decline in this session. The nearest southern barrier is 1,305.00 where the senior channel and a breached trend-line are located. In terms of resistance, Gold is restricted by the monthly PP and the 23.60% Fibo at 1,330.00 and 1,335.60, respectively.

Traders should be attentive when the US inflation data come out at 1230GMT.

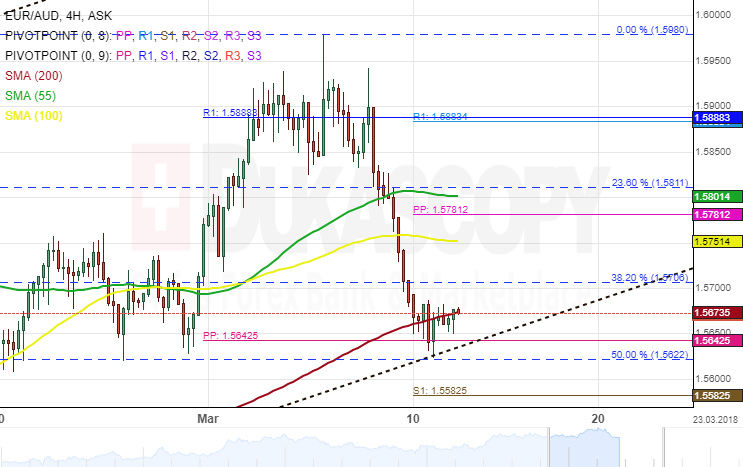

EUR/AUD 4H Chart: Restricted By SMA

The common European currency has been trading in an eight-month ascending channel against the Australian Dollar after it hit the lower boundary of a dominant channel.

After reaching the 50.00% Fibonacci retracement level, the Euro began to surge, however, the 200-hour simple moving average was pressuring the currency pair further south. This retracement can be measured by connecting the January low at 1.5264 and the March 7 high at 1.5980.

Everything being equal, the currency exchange rate is likely to decline further as technical indicators favour bears to continue their dominance.