Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.15; (P) 106.56; (R1) 106.82; More...

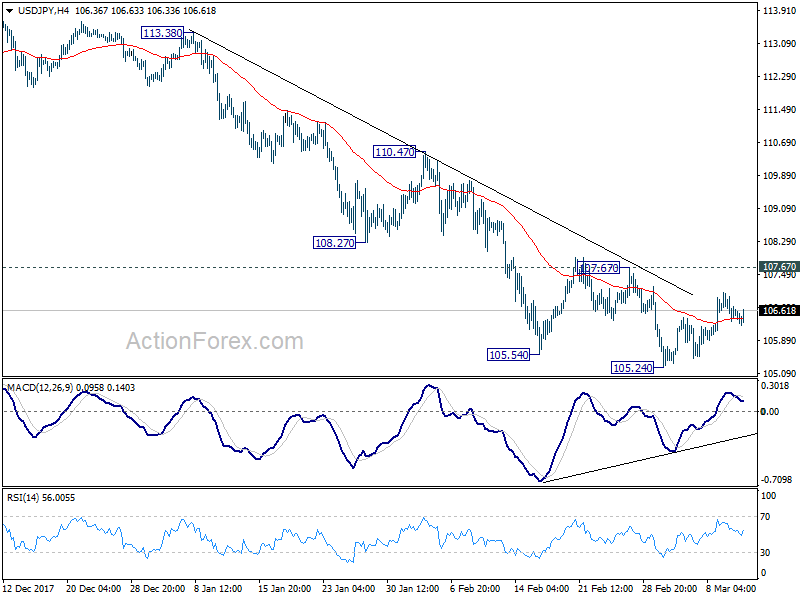

USD/JPY is still bounded in consolidative trading from 105.24. Intraday bias remains neutral first. Note again that bullish convergence condition is seen in 4 hour MACD. On the upside, decisive break 107.67 resistance will indicate near term reversal. In such case, outlook will be turned bullish for 110.47 resistance next. But before that, another decline is still mildly in favor. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

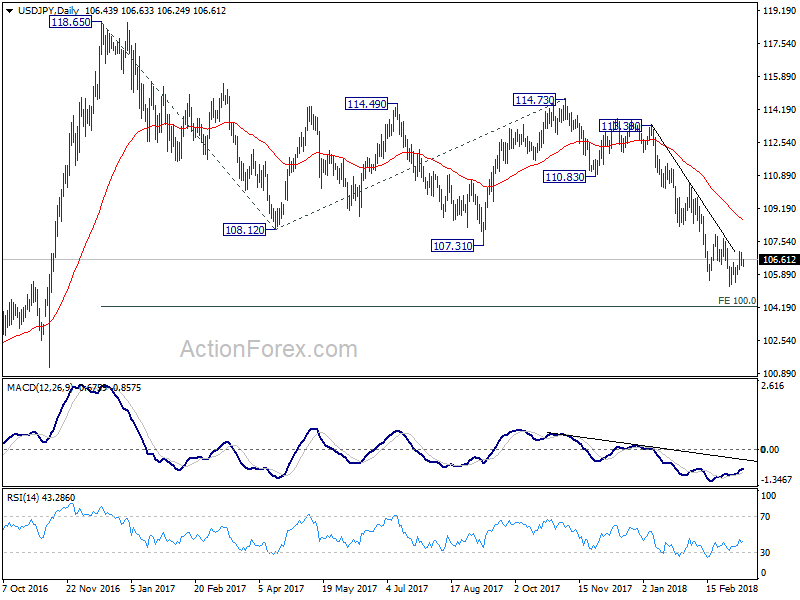

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9452; (P) 0.9482; (R1) 0.9505; More...

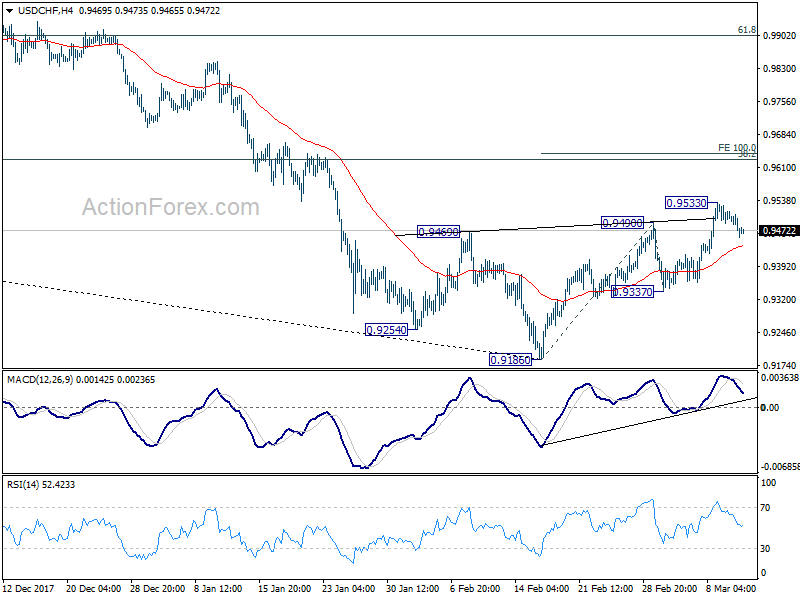

Intraday bias in USD/CHF remains neutral for consolidation below 0.9533 temporary top. Another rise is expected as long as 0.9337 support holds. Above 0.9533 will target 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9641 first. On the downside, break of 0.9337 minor support is needed to indicate completion of the rebound. Otherwise, near term outlook will be cautiously bullish even in case of retreat.

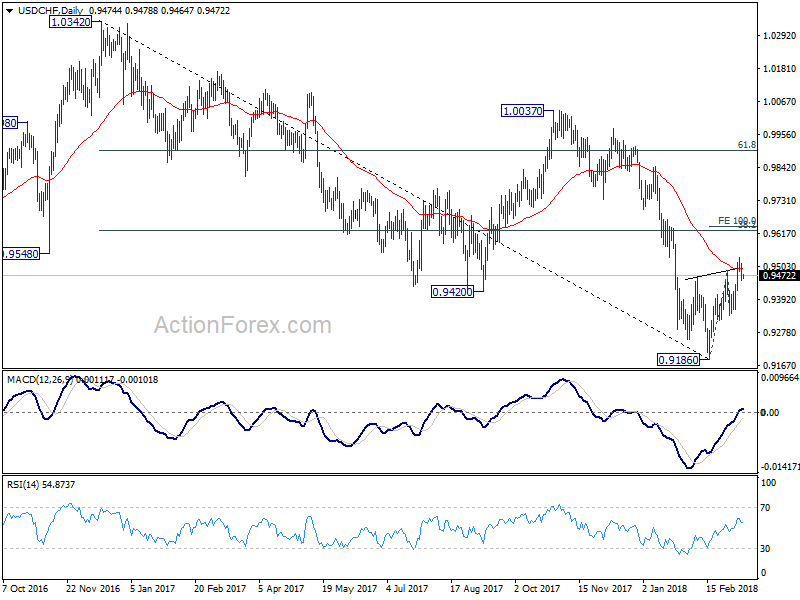

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

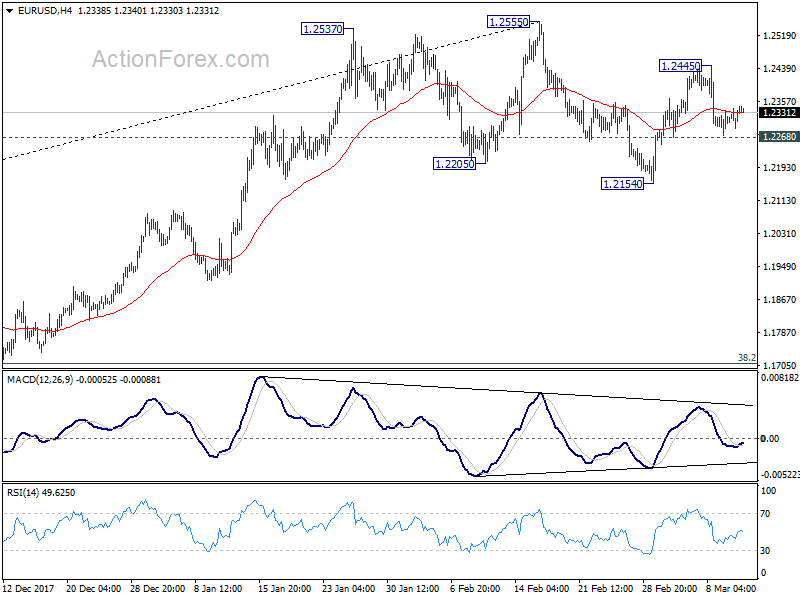

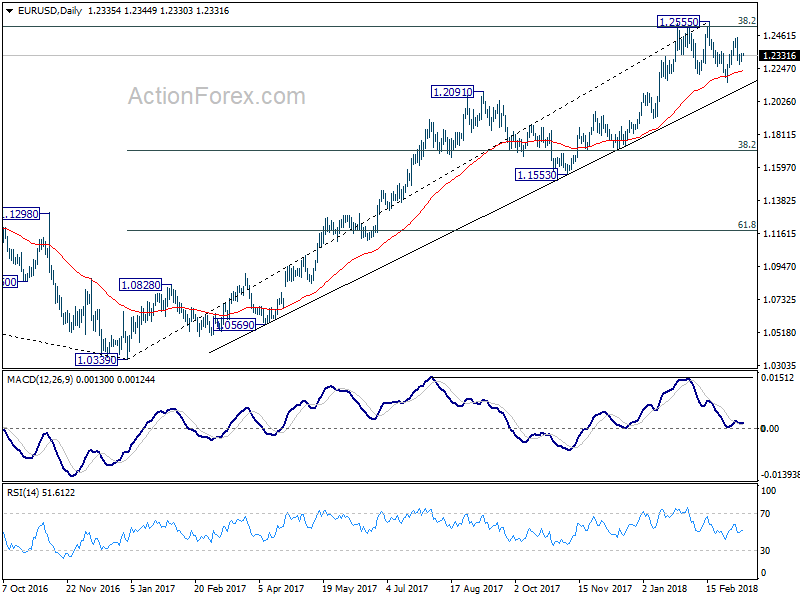

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2302; (P) 1.2323 (R1) 1.2357; More....

No change in EUR/USD's outlook. Intraday bias remains neutral with focus staying on 1.2268 minor support. On the downside, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below. On the upside, above 1.2445will turn bias to the upside for retesting 1.2555 key resistance.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

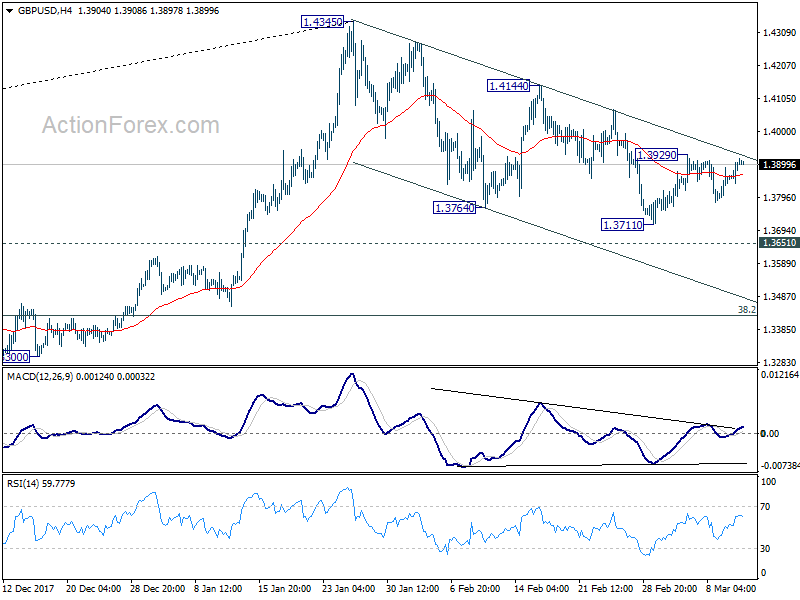

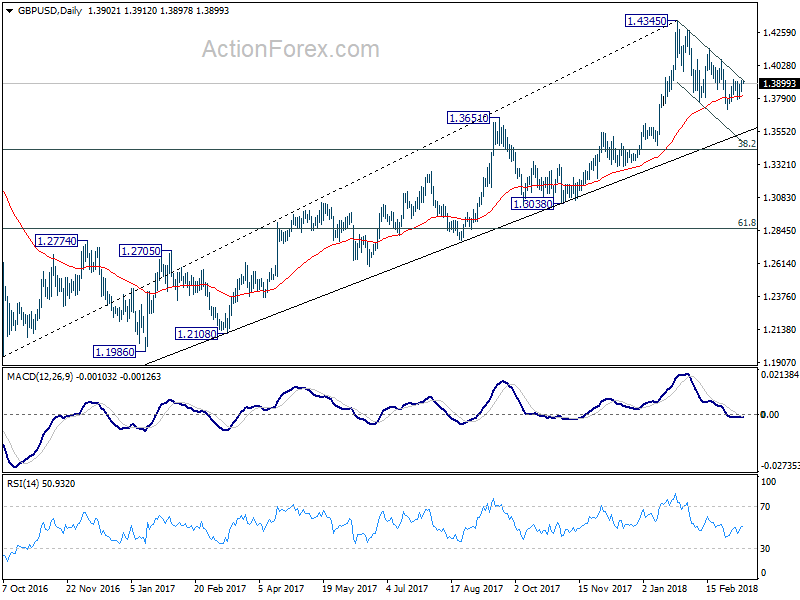

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3858; (P) 1.3887; (R1) 1.3935; More....

At this point, GBP/USD is still limited below 1.3929 minor resistance, and bounded below near term falling trend line. Intraday bias remains neutral first. On the upside, firm break of 1.3929 will be the first sign of reversal. That is, the choppy pull back from 1.4345 could have completed at 1.3711 already. In this case, intraday bias will be turned back to the upside for 1.4144 resistance for confirming this bullish view. On the downside, break of 1.3711 will resume the decline from 1.4345 through 1.3651 resistance turned support. At this point, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Market Morning Briefing: The Euro-Yen Has Moved Down Only Slightly

STOCKS

Dow (25178.61, -0.62%) dipped slightly instead of moving higher to 25500. Trade within 25000-25500 is likely to be seen in the next few sessions.

Dax (12418.39, +0.58%) moved up in line with our expectation but may pause in the 12400-12550 region just now. If no rejection is seen from levels near 12500, the index could indicate medium term bullishness. Watch price action near 12500-12550 levels.

Nikkei (21789.57, -0.16%) is trading along the resistance and while it holds, a rejection towards 21400-21000 is possible in the near term. Only on a break above current levels, we may negate an immediate fall towards 21000 and expect some bullish trades in the near term. Watch price action near current levels.

Shanghai (3323.47, -0.10%) is almost stable with no major movement. While the medium term resistance near 3350 holds, a fall to levels near 3250-3200 looks possible.

Nifty (10421.40, +1.9%) rose above 10400 contrary to our expectation of a rejection from 10380-10400 levels. I f the current rise sustains, the index may move higher towards 10500-10620 in the coming sessions.

Sensex (33917.94, +1.83%) is exactly at the interim resistance level and if it manages to break on the upside, it could test 34500; else a rejection from here could indicate a short corrective fall from here.

COMMODITIES

Brent (64.80) is testing resistance near 66 and while that holds, the price could come off towards 63-62 on the downside. Upside seems limited for the coming sessions.

WTI (61.21) is likely to trade within 59.50-63.00 region in the next few sessions. Near term is likely to remain sideways.

Gold (1323.30) is trading above immediate support level on the daily candles and while above the support near 1310-1315, the price is likely to move up slowly towards 1340/50.

Copper (3.1220) may trade in the 3.1750-3.0750 region for a few sessions before moving higher towards 3.20/25 levels in the medium term.

FOREX

There are some important data releases in the coming week for the US (US CPI, US Retail Sales, US PPI etc) which might have some impact on Dollar Index and the Euro.

The Dollar Index (89.918) after strengthening last week due to the ECB chief’s dovish stance is now dropping, contrary to our expectation. There is immediate support on daily candles near 89.75 which could be tested in the next 1 or 2 sessions before a bounce back to retest levels near 90.25.In the next 1-2 weeks, we could see the Dollar Index test resistance on 3 day candles near 91, before turning bearish in the medium term.

Euro (1.2335) : Against our expectation of a downmove towards support on daily candles near 1.225, the Euro seems to be respecting support on weekly candles near 1.228-1.23 for now. There is some likelihood that the Euro finds some resistance provided by the 21 days moving average on daily line chart and drop towards 1.225 gradually over this week and the coming week.

Dollar-Yen (106.41) as mentioned yesterday, is respecting immediate resistance near 107 on the daily line charts provided by 13 days and 21 days moving average lines. We repeat that Dollar Yen in this week could again move down towards 106.0-105.5 (there is crucial support at 105.5 and a break of the same would lead to medium term bearishness).

The Euro-Yen (131.24) has moved down only slightly and its downmove towards support near 129.75-129.50 on daily and 3 day candles might get extended into next week. If the Dollar Yen and Euro indeed test supports near 105.5 and 1.225, the corresponding rate for Euro Yen would be 129.23, which would be consistent with the predicted downmove towards support on the Euro yen daily chart.

As per expectation, the Pound (1.3902) after testing strong support near 1.38 has moved up towards 1.39 and could shortly test 1.395 (seen as immediate resistance level on daily candles).

Dollar-Rupee (65.04): Dollar Rupee likely to see a dip towards 64.80/75 before again moving up towards 65.20/25 in the coming sessions.

INTEREST RATES

The Japan 10 Yr yield (0.048%) after having bounced from support near 0.038% last week prior to the BOJ meeting in anticipation of some hawkishness by the central bank is now dropping again as we expected. It might move down towards support near 0.04% in the coming weeks.

The German 10 Yr – US 10 Yr has moved slightly up from support near -2.26% on the long term chart and is near -2.24% currently. With German 10 Yr Yield (0.632) seeing a further fall, the possibility of US yields dipping to keep the German-US yield spread above -2.26% seems more likely.

US 10 Year Yield (2.8736), US 30 year Yield (3.133), US 5 year yield (2.6435), US 2 year yield (2.27) : US yields have again dipped as they continue their oscillation in their respective set ranges. Above, we have written about how the US yields might actually follow German yields to keep the spread above support. This goes against our supposition till now, which was as follows:

“A rise in US yields beyond long term resistance levels is imminent in March. However, last week, we also said that there might just be some drop in US yields in this week, after which the week of the US Fed meeting might then see volatility return, taking yields higher in anticipation of a rate hike. (Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively – a decisive breach of these levels could happen in March 2nd half.)”

We still need to wait and watch on this as a lot could depend on the US data releases this week.

USD Grinds Lower Pre CPI

The ebb in the US dollar continued Monday as the fallout from non-farm payrolls continued to reverberate. CHF was Tuesday's top performer, while CAD. Australian home loans data highlights the Asia-Pacific session.

The absence of economic data for North American traders kept the focus on political drama in Japan and Brexit developments. Finance Minister Aso is embroiled in a real estate scandal and that's raised questions about his entire government, leading to some modest yen strength. Aso is considering not attending this month's G20 meeting.

Meanwhile, the ebb and flow of Brexit news gave the pound a lift and cable is now testing resistance at the two-week high.

Politics were largely a non-factor and US stock markets were flat. Trump is reportedly interviewing Larry Kudlow to lead his economic team. He is an unabashed free trader and is strongly anti-tariff so that would be a welcome development, albeit a confusing one.

Looking ahead, January Australian home loans data is due at 0030 GMT and expected to dip 0.2% after a 2.3% drop in December.

AUD has been a strong performer since Friday and is trading at a two-week high. The rebound comes after a miserable February but the RBA is slowly growing more optimistic and the solid uptrend since early 2016 is intact. The flipside is that commodities are beginning to struggle. Iron ore has fallen in seven consecutive sessions as uncertainty on steel mounts.

Forex Markets Indecisive, US CPI Awaited

Movements in the forex markets are not too decisive for the moment. Sterling made a bull run yesterday but there was no follow through buying. GBP/JPY is staying below 1.3929 near term resistance despite the rally attempt. GBP/JP's recovery since last week's low at 144.97 is also looking corrective. While Dollar is weak this week, Euro is not much better. EUR/USD's recovery ahead of 1.2268 minor support has been very weak so far. Aussie and Kiwi are the better performing ones. But while AUD/UD does managed to extend the near term rebound, it's starting to feel heavy ahead of 0.7892 resistance. Markets will look into US CPI today for more inspiration.

CPI unlikely to change Fed's path

Markets are expecting US CPI to accelerate from 2.1% yoy to 2.2% yoy in February. Core CPI is expected to be unchanged at 1.8% yoy. So far, barring any disaster, a Fed hike in March is like a done deal even though Chicago Fed President Charles Evans might dissent. The overall impression is that consensus among Fed policy makers is three hikes this year. Weak (or the lack of) inflationary pressure provides little reaction for Fed to hike a fourth time. The picture could change if the impact of the government's tax cut is passed through the economy later. But for now, a month of data is unlikely to alter Fed's path in March and even June.

Australia NAB business confidence jumped to record

Australia NAB business condition jumped 3 pts to 21 in February, hitting a record high. However, business confidence dropped 3 pts to 9. NAB noted in the release that "business activity in Australia is robust" and "strength in conditions is broad based across industry groups." The fall in confidence was seen as reactions to global market "turbulence" back in early February only. But the impact of those turbulence was "relatively limited".

Overall, NAB maintained that view that RBA will hike by late 2018, but may delay till early 2019. It noted that "we expect by late 2018 the RBA will feel relaxed enough about the domestic fundamentals to cautiously start withdrawing the stimulatory policy stance it is currently running. However, it will depend heavily on the data flow and the risk is that the RBA will delay rate rises until early 2019".

Also fro Australia, home loans dropped -1.1% mom in January.

RBNZ Spencer hailed macroprudential policy

RBNZ Governor Grant Spencer hailed the success of macroprudential tools in a speech to finance industry professional today. The policy infrastructure including the LVRs (loan to value restrictions). helped limit the risks of surge hour prices. It also helped keep interest low to boost inflation. And, after adopting the policy for five years, Spencer suggested a review would be run with the Treasury to consider ways to expand it. He also suggested to introduce a new committee on macroprudential policy alongside the monetary policy committee.

Canada PM Trudeau: No link between NAFTA and tariff exemptions

Canadian Prime Minister Justin Trudeau said that the exemptions on Trump's steel and aluminum tariffs were not a "magical favor being done". He pointed out that

"millions of jobs on both sides of the border depend on continued smooth flow of trades." And the tariffs would hurt both sides. He also expressed the willingness to work with the on NAFTA. But, he also emphasized that "we don't link together the tariffs and the negotiations for NAFTA."

Looking ahead

The economic calendar is not too busy today. UK annual budget release will be a major focus. US CPI will be another. BoC Governor Stephen Poloz's speech will also be watched.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3858; (P) 1.3887; (R1) 1.3935; More....

At this point, GBP/USD is still limited below 1.3929 minor resistance, and bounded below near term falling trend line. Intraday bias remains neutral first. On the upside, firm break of 1.3929 will be the first sign of reversal. That is, the choppy pull back from 1.4345 could have completed at 1.3711 already. In this case, intraday bias will be turned back to the upside for 1.4144 resistance for confirming this bullish view. On the downside, break of 1.3711 will resume the decline from 1.4345 through 1.3651 resistance turned support. At this point, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Feb | 2.50% | 2.50% | 2.70% | |

| 0:30 | AUD | Home Loans M/M Jan | -1.10% | -0.20% | -2.30% | |

| 0:30 | AUD | NAB Business Conditions Feb | 21 | 18 | ||

| 0:30 | AUD | NAB Business Confidence Feb | 9 | 12 | ||

| 4:30 | JPY | Tertiary Industry Index M/M Jan | -0.30% | -0.20% | ||

| 12:30 | USD | CPI M/M Feb | 0.20% | 0.50% | ||

| 12:30 | USD | CPI Y/Y Feb | 2.20% | 2.10% | ||

| 12:30 | USD | CPI Core M/M Feb | 0.20% | 0.30% | ||

| 12:30 | USD | CPI Core Y/Y Feb | 1.80% | 1.80% |

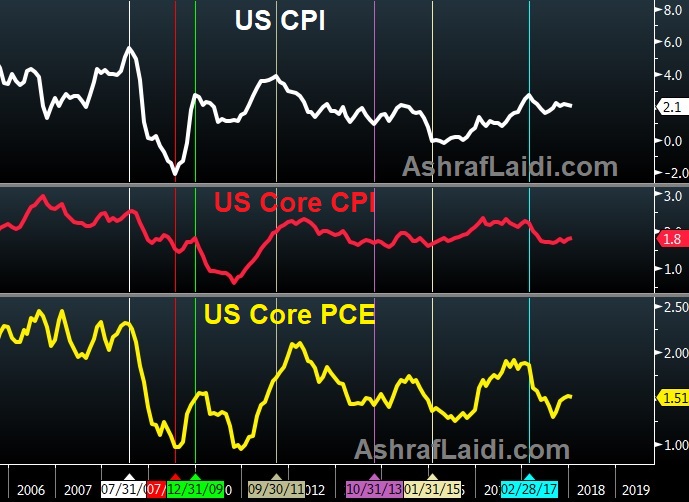

CPI Or PCE?

Non-farm payrolls gave a lift to risk assets on Friday another strong jobs number came with moderating wages. Early moves in the new week have been modest. CFTC positioning data generally showed a shift towards neutral. Ahead of Tuesday's release of US CPI, Ashraf posted a chart below, highlighting the course of US CPI, core CPI and the core PCE (Fed's inflation gauge). Which one leads the other? The answer is clear with the help of a few vertical lines. There are currently 11 Premium trades in progress; 7 in the green, 2 even and 2 in the red.

Non-farm payrolls rose 313K compared 205K expected in another sign of solid economic growth in the United States. A month ago, that was accompanied by a rise in wages that contributed to a wave of volatility throughout markets. This time, wages rose 0.1% m/m compared to +0.2% expected and 2.6% y/y versus the 2.8% consensus. More on the jobs/earnings report here.

The reaction was a jump in the S&P 500 climbing 1.7% and AUD/JPY positing its best day since July. It was the classic risk-on response and it hints that growth can continue to improve and the Fed doesn't need to quicken the gradual pace of rate hikes.

The response underscores how dominant the inflation theme is for markets right now. At the same time, geopolitics remains a constant risk as North Korea and the circus in the White House continues.

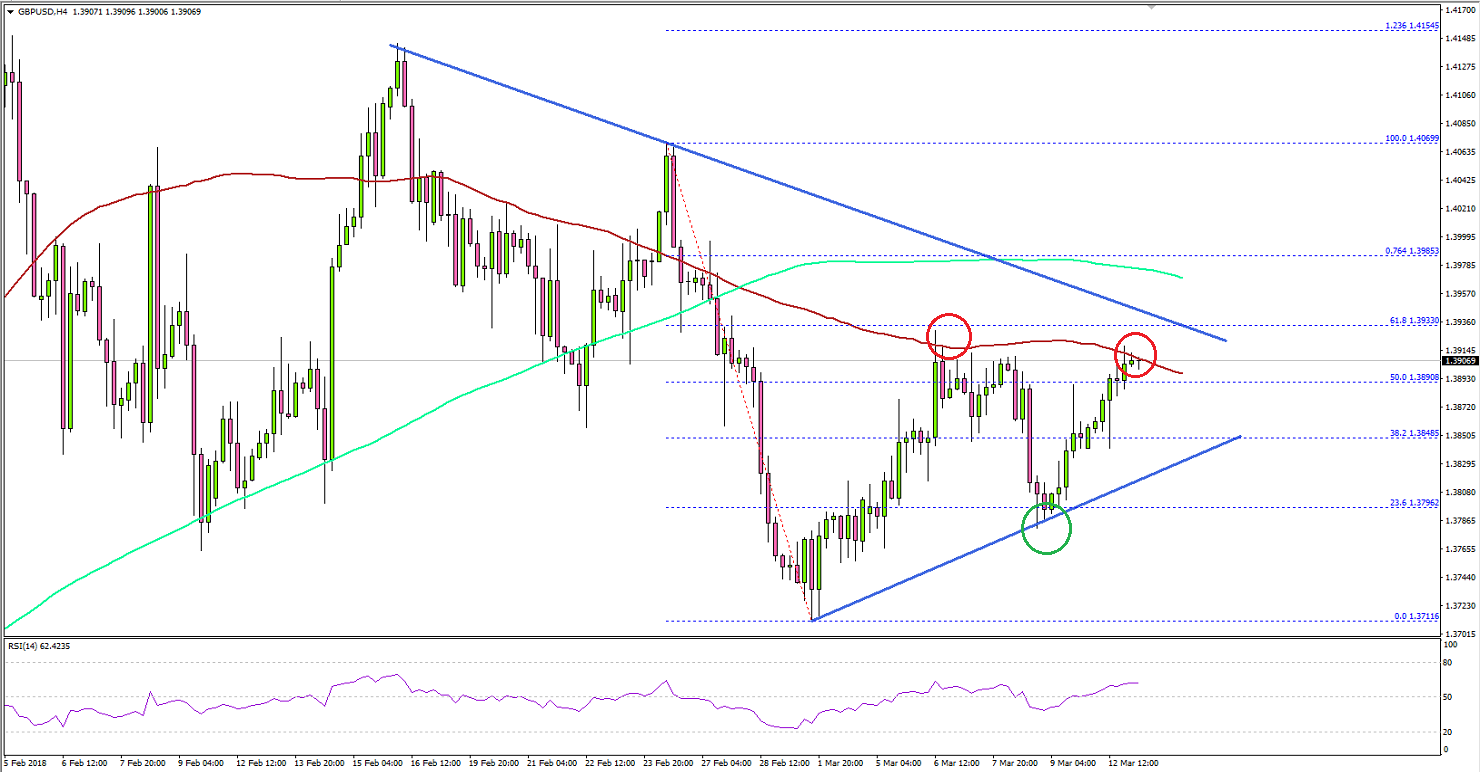

GBP/USD Approaching Key Break, UK’s Budget Next

Key Highlights

- The British Pound recovered nicely from the 1.3790 swing low against the US Dollar.

- There is a key contracting triangle forming with resistance at 1.3930 on the 4-hours chart of GBP/USD.

- The pair could make the next move either above 1.3930 or below 1.3840.

- Today, the UK Budget report will be released, which could ignite swing moves in GBP/USD.

GBPUSD Technical Analysis

The British Pound formed a support base just below 1.3800 against the US Dollar and recovered. The GBP/USD pair is now preparing for the next move with resistance at 1.3930 and support at 1.3840.

Looking at the 4-hours chart of GBP/USD, there is a key contracting triangle forming with resistance at 1.3930. The pair has moved above the 38.2% Fib retracement level of the last decline from the 1.4069 high to 1.3716 low.

However, it is facing a major hurdle on the upside near 1.3920-30. The stated zone is also close to the 61.8% Fib retracement level of the last decline from the 1.4069 high to 1.3716 low.

On the downside, the triangle support is at 1.3840. A break below 1.3840 could push the pair back towards 1.3800. On the other hand, a break above the triangle resistance at 1.3930 may perhaps call for a test of 1.4000.

The US Dollar is slightly under pressure this week, but any further gains in EUR/USD and GBP/USD won't be easy. Today's US Consumer Price Index released for Feb 2018 could impact the market a lot. Therefore, the next move in the greenback depends on today's CPI release.

Economic Releases to Watch Today

- US Consumer Price Index Feb 2018 (MoM) – Forecast +0.2%, versus +0.5% previous.

- US Consumer Price Index Feb 2018 (YoY) – Forecast +2.2%, versus +2.1% previous.

- US Consumer Price Index Ex Food & Energy Feb 2018 (YoY) – Forecast +1.8%, versus +1.8% previous.

- UK's Budget Report.

Canada PM Trudeau: No link between NAFTA and tariff exemptions

Canadian Prime Minister Justin Trudeau said that the exemptions on Trump's steel and aluminum tariffs were not a "magical favor being done". He pointed out that "millions of jobs on both sides of the border depend on continued smooth flow of trades." And the tariffs would hurt both sides. He also expressed the willingness to work with the on NAFTA. But, he also emphasized that "we don't link together the tariffs and the negotiations for NAFTA."