Sample Category Title

Australia NAB business condition rose to record 21

Australia NAB business condition jumped 3 pts to 21 in February, hitting a record high. However, business confidence dropped 3 pts to 9.

Quote from the release:

- "The record level for the NAB Monthly Business Survey business conditions index indicates that business activity in Australia is robust. Moreover, the strength in conditions is broad based across industry groups."

- "The fall in confidence may reflect the turbulence seen in international financial markets in early February, but confidence remains above average suggesting that the impact was relatively limited".

- "Forward orders have been on a rising trend for several years now signalling an improved outlook for the non-mining economy."

- "Capacity utilisation is trending higher which is a positive for both future investment and employment"

- "We expect by late 2018 the RBA will feel relaxed enough about the domestic fundamentals to cautiously start withdrawing the stimulatory policy stance it is currently running. However, it will depend heavily on the data flow and the risk is that the RBA will delay rate rises until early 2019"

RBNZ Spencer hailed macroprudential policy

RBNZ Governor Grant Spencer hailed the success of macroprudential tools in a speech to finance industry professional today. The policy infrastructure including the LVRs (loan to value restrictions). helped limit the risks of surge hour prices. It also helped keep interest low to boost inflation. And, after adopting the policy for five years, Spencer suggested a review would be run with the Treasury to consider ways to expand it. He also suggested to introduce a new committee on macroprudential policy alongside the monetary policy committee.

Investor Caution Lingers

Investor Caution Lingers

In spite of the anaemic volumes overnight, the USD was broadly weaker. Most are attributing the lower volumes to the start of spring break which is traditionally a time for many US traders to head south with their families. But the miss on last Friday’s AHE and easing of overall inflation expectations has seen traders subtly downgrade of the Fed’s interest rate path and the dollar has weakened in consort.

Equity investors are finding it difficult to ignore the gnawing concerns about trade wars and are adopting a defence first strategy despite the Goldilocks jobs number. Keep in mind the spotlight will be on US CPI tonight, and it was only one month ago a surprise inflation print sent the market into a tailspin, so likely some caution ahead of the critical US inflation data. Overall investors remain very cautious as sentiment recovers.

Speaking of trade wars and protectionism, President Donald Trump issued an order Monday evening blocking any merger of the chipmaking giants Broadcom and Qualcomm, saying it was necessary to protect national security. There is “credible evidence,” the order says, that if the Singapore-based Broadcom took control of the US-based Qualcomm that the company “might take action that threatens to impair the national security of the United States.” Pretty clear the president is setting sights on Asia using what seems to be an arbitrary national security provision.

Oil prices

Oil prices moved lower in NY after Energy Information Administration published a report that Crude production from seven major U.S. shale plays is expected to see a climb of 131,000 barrels a day in April to 6.954 million barrels a day with the Permian Basin to see the most significant play with production increasing 80,000 barrels per day. Both the surge in US production along with rising US exports gaining a bigger slice of the Asian pie continue to weigh on OPEC compliance. On cue, media reports are suggesting another fissure forming on OPEC compliance. On one side is Saudi Arabia, which wants oil prices at $70 a barrel or higher, and on the other is Iran, which wants them around $60 fearing that US shale production will continue to ramp up production as prices near $70.00

Prices bounced off overnight lows the bearish signals continue to form which should weigh in top side momentum ahead of this week’s critical inventory data.

Gold Prices

Gold prices were stable to higher overnight as the USD nudged lower as higher US interest rates fears have abated after the lower wage report on Friday. But gold traders are adopting a more neutral stance as we enter Fed blackout period.While a March hike if fully priced in, traders usually get a bit anxious awaiting the Fed statement and key forward guidance, so we should expect interest rate uncertainty to weigh on prices over the short term.

Currency Markets

The Japanese Yen

The dollar traded either side of 106.50 levels overnight, but we’re probably nearing a short-term inflexion point after the markets failed to move above the 107 level when risk appetite blossomed on the lower wages inflation print and US -North Korea headline. Global uncertainty and risk aversion continue to linger, but overall markets remain very sticky within the 106 handle.

I’m confident traders were holding onto USDJPY shorts by a thread at yesterday weekly Asia open, but the top side was tempered with the developments in the Moritomo scandal.

The escalation of Japan political risk tops all and will continue to push USDJPY lower as these headlines evolve around this deepening scandal.

The Euro

The Euro seems very content to trade around the 1.2300 levels, and traders are showing little interest in any direction. Likely a function of the recent softer run of economic data but the Euro remain very much an inflow and policy normalisation play, and traders continue to buy the dips expecting stronger output growth to re-emerge.

The Australian Dollar

The Australian dollar is still enjoying the bounce in risk sentiment while the softer US wages continues to weigh US bond yield. However, commodity markets are showing some stress as oil prices fell on US supply concerns.Given the Aussie dollar strong proclivity to commodity prices, top side momentum will be tempered even more so with interest rate rates as playing an insignificant role in AUD fortunes.

The Malaysian Ringgit

The market remains a range play as investors remain very cautious as the EM FX Asia point of view recovers. Stronger Jobs headline with subdued wage inflation should continue to prove supportive for the Ringgit this week. However, the potential escalation in trade tension continues to loiter.

Given the constant barrage of US increasing oil production headlines weighing on oil prices, the MYR is getting little support energy prices, but at these current levels, minor sell-offs are not denting overall sentiment but a more profound move below WTI 60.00 could.

Pound Improves To 1.39, UK Budget Next

The British pound has started the week with gains. In North American trade, GBP/USD is trading at 1.3899, up 0.35% on the day. In economic news, there are no British indicators. The US releases the federal budget, with an estimate of a $222.3 billion deficit. On Tuesday, the UK releases the annual budget. The US will release CPI reports.

The UK ended the week on a disappointing note, as Manufacturing Production slowed to 0.1% in February, down from 0.3% a month earlier. This reading was shy of the estimate of 0.3% and marked a 4-month low. In the US, employment numbers were a mix on Friday. Wage growth dropped to 0.1% in February, down from 0.3% a month earlier. This missed the estimate of 0.2%, and marked the lowest gain in four months. The news was much better from nonfarm payrolls, which soared to 313 thousand, crushing the estimate of 205 thousand. The mixed numbers have eased concerns about the Fed raising rates four times in 2018. At the same time, a rate hike is very likely at next week’s Fed meeting, with the CME Group pegging the odds of a hike at 86%.

Are Britain and the European Union heading towards a showdown? Last week, Donald Tusk, president of the European Council, advised Prime Minister May to “pink’ her red lines on Brexit, if Britain wants to maintain a close economic relationship with the bloc. May has insisted that there will be no customs union, and the European Court of Justice will have no jurisdiction over the UK. May set out these positions after the EU published its draft negotiating guidelines for Brexit, and the guidelines warned of “negative economic consequences” if Britain does not soften its position. Tusk added that he does not want to build a wall with Britain, and the EU could offer Britain a free trade agreement, with zero tariffs. At the same time, Tusk warned that Brexit will make trade between the two sides “complicated and costly” and the EU would not allow Britain to cherry pick in any future trade arrangement. EU members are expected to sign off on the negotiating guidelines at a summit in late March, which could trigger a nasty response from the May government.

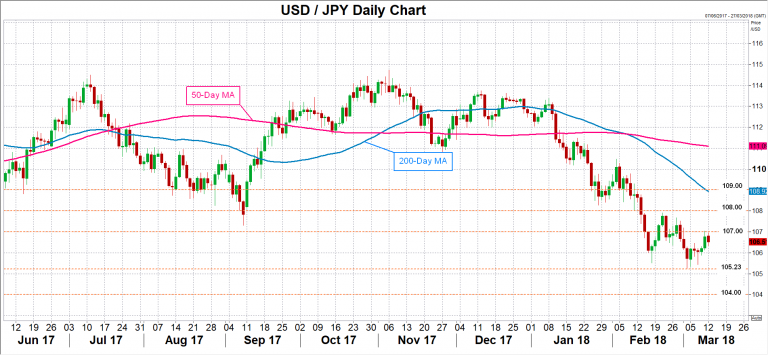

Japanese Yen Edges Lower, Investors Eye BoJ Minutes

The Japanese has edged lower to start the week. In North American trade, USD/JPY is trading at 106.55, down 0.25% on the day. In economic news, Japanese BSI Manufacturing Index dropped sharply to 2.9, well short of the estimate of 10.3 points. There are no major US releases on the schedule. On Tuesday, the US publishes CPI reports and the BoJ releases the minutes of the January meeting.

The Bank of Japan held the course on interest rates at its Thursday meeting, as it kept short-term rates at -0.1% and 10-year government bonds at around zero percent. The Bank sounded optimistic about economic growth, which has been moderate but steady, thanks to a strong export sector. However, BoJ Governor Haruhiko Kuroda was decidedly dovish in his remarks, saying that the BoJ would consider further easing if inflation did not reach the bank’s target of around 2% by 2020. These comments mark a 180-degree turn from remarks just a week earlier, in which Kuroda talked about the possibility of an exit from stimulus, which sent the yen upwards.

In the US, employment numbers were a mix on Friday. Wage growth dropped to 0.1% in February, down from 0.3% a month earlier. This missed the estimate of 0.2%, and marked the lowest gain in four months. The news was much better from nonfarm payrolls, which soared to 313 thousand, crushing the estimate of 205 thousand. The mixed numbers have eased concerns about the Fed raising rates four times in 2018. At the same time, a rate hike is very likely at next week’s Fed meeting, with the CME Group pegging the odds of a hike at 86%.

Tensions have eased somewhat regarding the tariffs which President Trump imposed on Thursday. Trump has exempted Canada and Mexico from the tariffs, and has said that Washington could ease the duties on other countries as well. Importantly, is strong domestic opposition to Trump’s move, including senior Republican lawmakers who have said they will work to overturn the tariffs, which could spark an all-out trade war. So far, the markets are confident that a solution to the tariff tussle will be found.

Eyes on US CPI as Inflation Fears Could Return

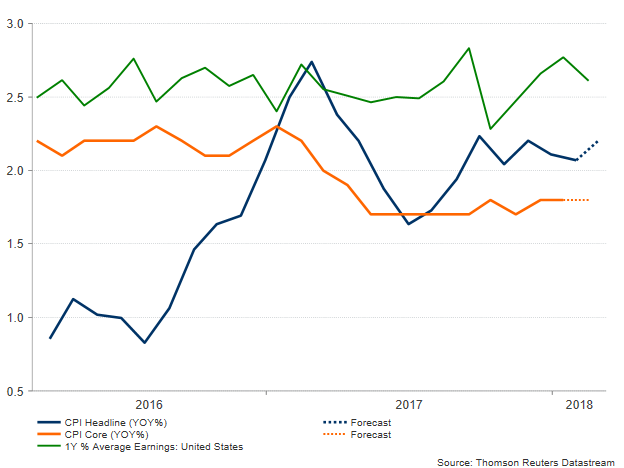

Flashing back a month earlier, an upward surprise in consumer prices caused a sharp but temporary reaction to the markets, with stocks sinking and government bond yields surging. While the consumer price index is not the Fed’s favorite inflation measure, and someone could expect the figures to be more informative rather than a market-driver, the numbers popped up in times when investors were already worrying that the economy would start generating more noticeable inflation. Indeed, in February, speculation that price growth could pick up speed increased after the Nonfarm Payrolls (NFP) wage component reached its highest pace since 2009 in yearly terms. Therefore, an upbeat CPI at that time was enough to add fuel to the fire and cause another market turbulence. This time, however, things are different, as Friday’s NFP report did not raise inflation fears but lifted risk appetite as wage growth eased. Therefore, it would be interesting to see whether CPI figures will gain further positive momentum as the forecasts suggest, reviving concerns over inflation ahead of the FOMC policy meeting next week.

According to analysts, the headline CPI due on Tuesday at 1230 GMT is expected to have risen by 2.2% year-on-year in February, above the 2.1% growth seen in January when price pressures were indicated in almost every single industry included in the index. In monthly terms, however, the gauge is expected to lose steam, falling from 0.5% to 0.2%. Excluding volatile items such as food and energy, the core measure is anticipated to remain steady at 1.8% y/y and slip from 0.3% to 0.2% m/m. Although, the index is not the one affecting monetary decisions – that would be the Personal Consumption Expenditure Index – is still a key indicator of inflation trends and any unexpected spike in the numbers on Tuesday could give an early indication of what the February PCE index could be, when it is released at the end of March. Still, the PCE would only be available days after the FOMC members conclude their policy meeting on March 21. Hence, the CPI numbers could affect discussions on inflation during the two-day gathering.

On the monetary front, markets are widely pricing a rate hike coming next week with a probability of 88.8% based on the CME FedWatch tool. They are also betting on two more rate rises by the end of this year, probably delivered in June and September, while the Fed chief Jerome Powell’s rosy outlook on the US economy, expressed recently in front of the US Congress, opened the door for a fourth rate hike this year before Friday’s slowdown in wages curbed somewhat those expectations. Other Fed members also had optimistic views on the US economic performance and the path of future interest rates following Powell’s testimony, with the Dallas Fed President, Robert Kaplan, saying last Tuesday that three rate increases is a “reasonable” base case as the economy is right around full employment which should add further pressures on inflation. Esther George, the Kansas Fed President and a reliable hawk argued a few days later that “given the economic momentum, the Fed should continue to raise interest rates and carefully calibrate its policy to lean against a potential buildup of inflationary pressure or financial market imbalances”. However, it is worth noting that these comments were made before Trump signed the implementation of import tariffs on steel and aluminium on several countries (except Canada and Mexico) last week, therefore policymakers might reconsider their growth prospects given that government’s levies on materials and a potential tit-for-tat retaliation from other countries could dent benefits arising from the corporate tax cuts. On the consumers’ front, higher import tariffs could translate into higher prices. While this is what policymakers want at the moment, they would not welcome the measures if these weigh on consumer spending.

Turning to forex markets, in the wake of stronger than expected CPI readings which could raise inflation expectations, dollar/yen could revisit the 107 handle and even touch the previous high of 107.90 posted on February 21. If there is a significant deviation above the forecasts, the 108 and the 109 psychological levels could also come into view. In the alternative scenario, disappointing CPI prints could send the market down to the 106 key-mark, while in the worst case the pair is not unlikely to cross below the 16-month trough of 105.23, opening the way towards the 104 key-level.

Sunset Market Commentary

Markets:

Global core bonds traded marginally higher in this week’s opening trading session. Volumes were low amid an empty eco calendar. Dovish comments by ECB Coeuré and ECB Smets contributed to an outperformance of the German Bund. Both indicated that inflation is not yet where the ECB wants. Smets even added that it may take longer to reach the inflation goal. The comments come after last week’s dovish interpreted ECB meeting and ahead of speeches by Draghi, Praet, Constancio and others on Wednesday. Tonight’s start of the US Treasury’s mid-month refinancing operation probably also explains the US note future’s lagging behind. German yields decline by 1.7 bps (30-yr) to 2.2 bps (5-yr) at the time of writing. The US yield curve flattens with yield changes ranging between +0.4 bps (2-yr) and -1.6 bps (30-yr). 10-yr yield spread changes versus Germany are broadly unchanged. Resigning centre-left (PD) party governor Renzi ruled out supporting M5S in government. He backed his call to remain in opposition. For now, the Italian political deadlock remains complete, without impacting BTP’s. Tomorrow’s auction could be a good test for investor demand.

Risk sentiment remained constructive in the wake of Friday’s almost perfect payrolls. However, the dollar still didn’t find a clear directional trading pattern. A political scandal in Japan initially weighted on USD/JPY. The dollar was also slightly under pressure against the euro at start of European trading. The pair filled offers in the 1.2340 area. However, the EUR/USD rebound didn’t run into resistance soon. We didn’t see a specific driver, not from the USD side nor from the dollar side of the story. Interest rate differential widened marginally in favour of the dollar, but we doubt that this was an important factor. The topside in EUR/USD is apparently rather well protected as the market, after last week’s ECB meeting, assumes that any ECB normalization will develop in a very gradual way. This was confirmed by soft comments from ECB Smets today. Smets also indicated that FX/the euro remains on the radar of the ECB. At the same time, Friday’s payrolls report might be rather neutral for the Fed (and for the dollar). EUR/USD hovers in the 1.23 area. USD/JPY is holding in the mid 106 area. Tomorrow’s US CPI report is probably the next milestone for USD trading.

Sterling’s trading dynamics was quite similar to Friday. There were no negative headlines on Brexit anymore after last week’s ‘bickering’ between the UK and the EU on their future relationship. With few UK eco data on agenda this week, GBP-traders, amongst others, might give some more attention to the UK spring budget statement which UK Fin Min Hammond will present tomorrow. The picture on the ST UK fiscal performance might not be too bad, potentially supporting a further ST technical rebound of sterling. UK junior Brexit Minister Walker also indicated that a deal on the Brexit implementation period might be close. Whatever the reason, EUR/GBP drifted further south in the 0.88 big figure today (currently 0.8865 area). Cable also rebounded close to the 1.39 big figure.

US equities extended Friday’s post-payrolls rebound, opening with gains between 0.3% and 0.5%. European equities gain modest ground after a strong performance of WS on Friday and of Asian equity markets this morning.

News Headlines:

EMU inflation may need more time to rise than anticipated as spare capacity is taking longer to exhaust but the ECB should not accept price growth below its target, Belgian ECB member Jan Smets said in Reuters interview. The ECB has not even started the discussion about revising its monetary policy framework or even its so-called forward guidance, as the current setup serves the currency bloc well according to Jan Smets.

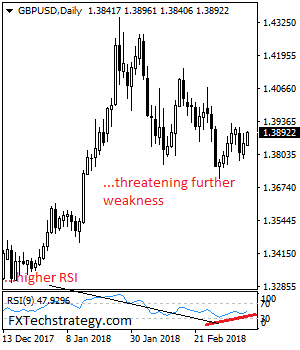

GBPUSD: Sees Price Follow Through Higher

GBPUSD - The pair continues to retain its upside pressure on recovery extending its Friday gain. Support lies at the 1.3850 level where a break will turn attention to the 1.3800 level. Further down, support lies at the 1.3750 level. Below here will set the stage for more weakness towards the 1.3700 level. Conversely, resistance stands at the 1.3950 levels with a turn above here allowing more strength to build up towards the 1.4000 level. Further out, resistance resides at the 1.4050 level followed by the 1.4100 level. On the whole, GBPUSD looks to follow through higher.

Canadian Dollar Inches Higher, US CPI Next

USD/CAD has ticked higher in the Monday session. In North American trade, USD/CAD is trading at 1.2830, up 0.15% on the day. On the release front, it’s a quiet start to the week. There are no Canadian indicators on the calendar. The US releases the federal deficit, with an estimate of $222.3 billion. On Tuesday, Canada releases Ivey PMI and the US publishes CPI reports.

The Canadian dollar ended the week on a high note, posting gains on Friday. The Canadian economy added 15.4 thousand jobs in February, after a sharp decline of 88 thousand a month earlier. This was below the estimate of 21.3 thousand, but investors were pleased with the strong turnaround. In the US, US employment numbers were a mix on Friday. Wage growth dropped to 0.1% in February, down from 0.3% a month earlier. This missed the estimate of 0.2%, and marked the lowest gain in four months. The news was much better from nonfarm payrolls, which soared to 313 thousand, crushing the estimate of 205 thousand. The mixed numbers have eased concerns about the Fed raising rates four times in 2018, which is good news for the Canadian dollar.

Tensions have eased somewhat regarding the tariffs which President Trump imposed on Thursday. Trump has exempted Canada and Mexico from the tariffs, and has said that Washington could ease the duties on other countries as well. Importantly, is strong domestic opposition to Trump’s move, including senior Republican lawmakers who have said they will work to overturn the tariffs, which could spark an all-out trade war. So far, the markets are confident that a solution to the tariff tussle will be found.