Sample Category Title

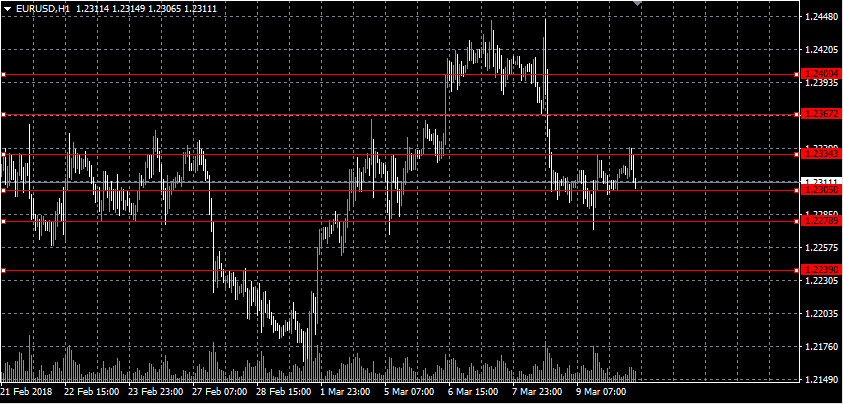

EURUSD Only Intraday Bearish Below 1.2305

The euro currency has slipped lower against the greenback, after buyers failed to gain traction above the 1.2334 level during the European trading session. The EURUSD pair now trades back towards crucial daily technical support, with buyers so far defending the key 1.2305 support region. Moving into the U.S session, traders now look to the release of the U.S Budget Statement and a clear breach of the 1.2305 to 1.2334 trading range.

The EURUSD pair is likely to turn intraday bearish below the 1.2305 level, with key support then found at the 1.2278 and 1.2239 levels.

Should the EURUSD pair hold above the 1.2305 level, buyers will likely target the 1.2334 and 1.2367 resistance levels.

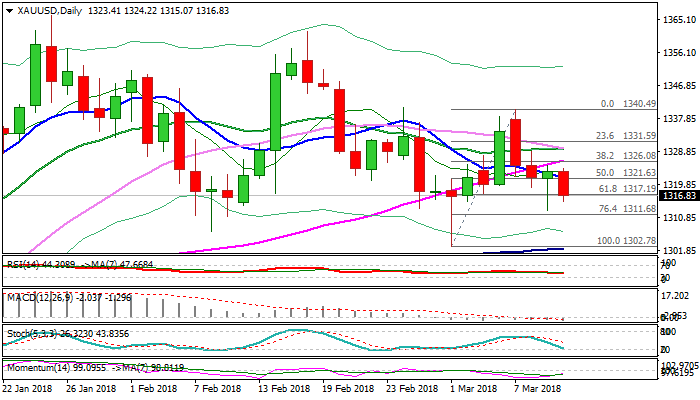

Technical Outlook: Gold Moves Lower On Monday As Dollar Firms After Being Hit By US Jobs Data

Spot Gold moved lower in European trading on Monday after holding within narrow range in Asia, as dollar shows signs of regaining ground after being hit fading hopes of stronger US rate hikes pace in 2018 on mixed US jobs data.

Fresh weakness of yellow-metal’s price signals continuation of near-term downmove from $1340 (07 Mar high), as the price extends below cracked $1317 support (Fibo 61.8% of $1302/$1340 upleg).

Close below the latter would be fresh bearish signal in addition to weakening daily techs (MA’s returned to bearish configuration, RSI turns south from neutrality zone, while momentum remains firmly in negative territory).

Bearish scenario on daily close below $1317 pivot would expose key near-term support at $1302 (01 Mar spike low, reinforced by 100SMA).

Broken descending 10SMA offers solid resistance at $1321, which should keep the upside protected.

Conversely, bullish signal will be generated on close above $1326 (broken 55SMA/broken Fibo 38.2% of $1302/$1340 upleg).

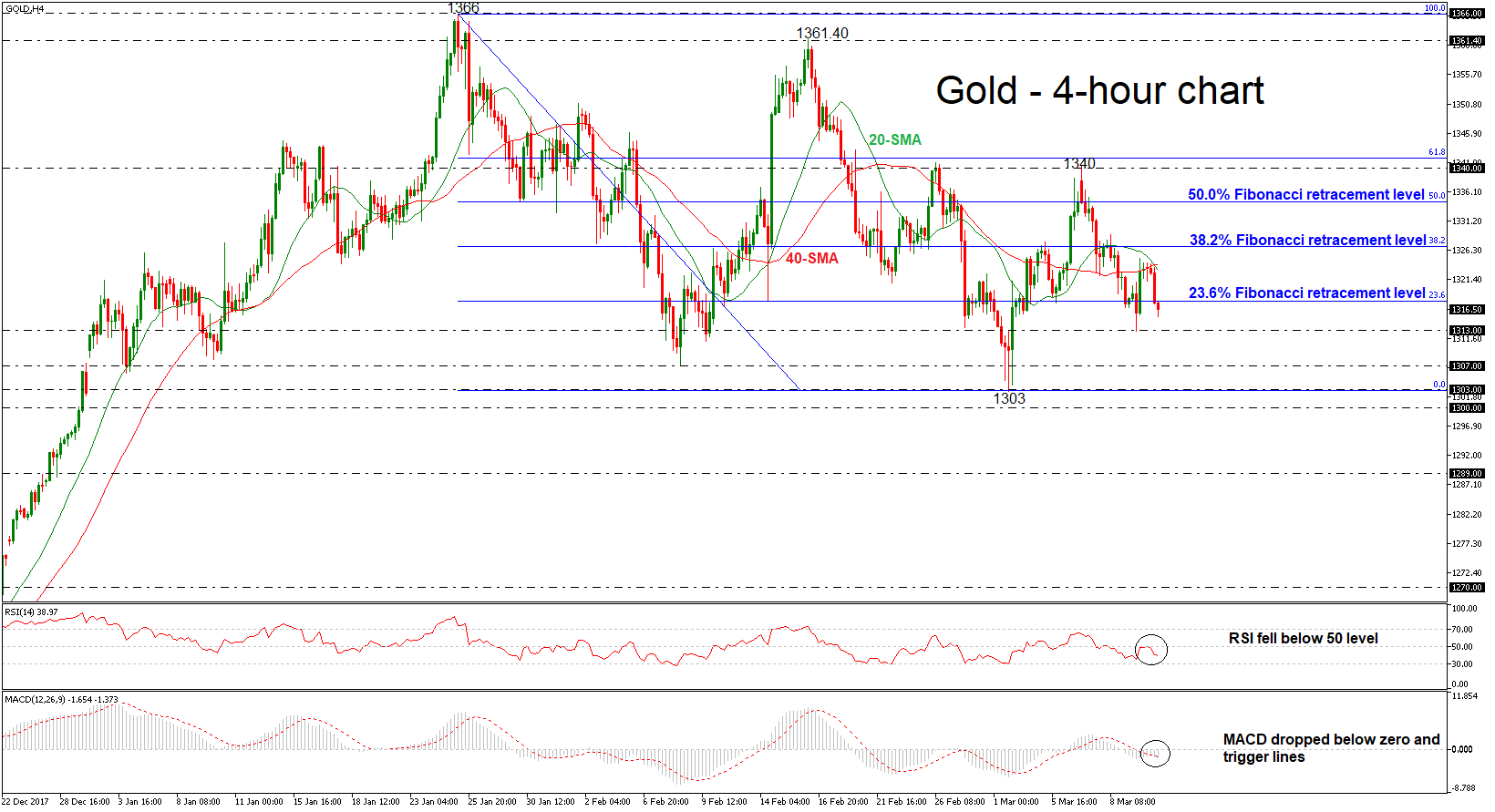

Res: 1321, 1326, 1330, 1332

Sup: 1313, 1311, 1307, 1302

Dollar Little Changed, Awaits Fresh Drivers, Stoxx 600 Records Near 2-Week High

Here are the latest developments in global markets:

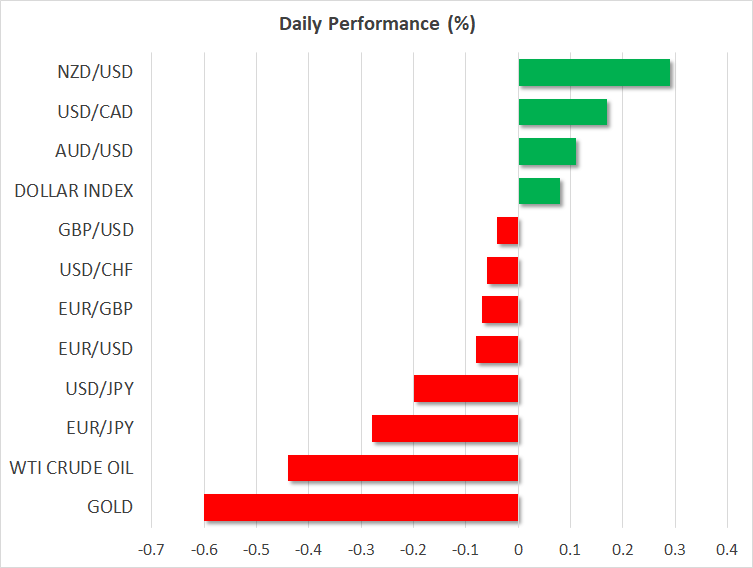

FOREX: The dollar was slightly higher versus a basket of currencies, recovering from losses recorded earlier in the day – the dollar index rose back above the 90 level. Dollar/yen was 0.2% lower at 106.55 amid a suspected cronyism scandal in Japan implicating Finance Minister Taro Aso. Euro/dollar and pound/dollar were little changed in anticipation of fresh catalysts. The aussie and the kiwi remained elevated versus their US counterpart, though they gave up on a significant part of earlier gains that saw them rise to two-week high levels. Ausie/dollar and kiwi/dollar were up by 0.1% and 0.3% respectively, being supported in part by positive risk sentiment on the back of abating worries over a trade war occurring.

STOCKS: European equities were broadly in the green, though gains were limited for the most part. The pan-European Stoxx 600 that more widely gauges equity performance in the continent was up by 0.3% at 1145 GMT, rising to 380.11 earlier in the day, its highest since February 28. The blue-chip Euro Stoxx 50 traded higher by 0.5%. Leading German utility companies announcing an overhaul in the sector boosted sentiment and contributed to the rise in equities; utilities were the leading gainer within the Stoxx 600. The German DAX outperformed relative to other blue-chip European indices, being up by 0.6%. The UK’s FTSE 100 was the only major European benchmark that was trading lower, being weighed by lower commodity stocks, albeit its losses were marginal. Meanwhile, the French CAC 40 was up by 0.2%. The Stoxx Europe 600 Automobiles and Parts sub-index traded higher by 0.5% despite a tweet by US President Donald Trump in which he threatened to impose taxes on European vehicles imported into the US in case the EU retaliates in response to his administration’s decision to proceed with the imposition of tariffs on steel. German carmaker Volkswagen (up 1.1%) was among the sub-index’s lead gainers. Futures on the Dow, S&P 500 and Nasdaq 100 were higher by 0.3%, 0.3% and 0.5% respectively, pointing to a higher open on Wall Street.

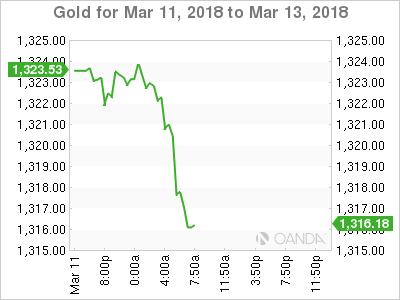

COMMODITIES: WTI and Brent crude were giving up part of Friday’s gains that saw them close the day higher by around 3.0%; the rise came on the back of a decrease in the number of US oil rig counts for the first time in seven weeks and improved risk sentiment following stronger-than-expected jobs growth figures out of the US. Expectations, though, that US output will eventually rise in 2018 are exerting pressure on prices, with WTI and Brent crude trading lower on Monday by 0.45% and 0.6% at $61.76 and $65.10 per barrel respectively. Gold was 0.6% lower at $1,316.06. This compares to Friday’s 11-day low of $1,312.99 that came on the back of rising appetite for risk and acting to the detriment of the perceived safe-haven’s allure.

Day ahead: In the absence of data focus falls on rest of the week

Monday’s economic calendar seems to be lacking traditional market moving releases. Consequently, market participants’ attention is falling on upcoming releases, such as Tuesday’s inflation figures for the month of February out of the US, for positioning moving forward.

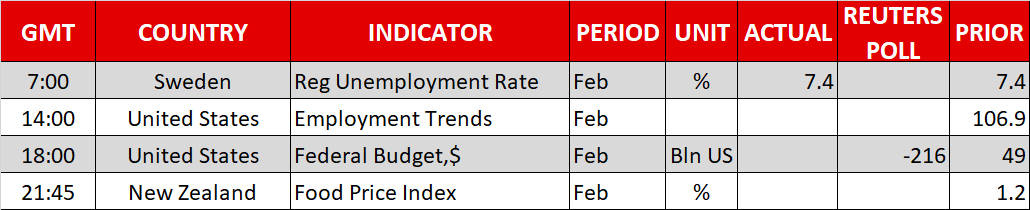

In the absence of other releases, the Conference Board’s employment trends index for February, as well as data on the US Federal Budget for the same month scheduled to go public at 1400 GMT and 1800 GMT respectively might attract some interest.

A meeting of eurozone finance ministers is taking place today. While typically such meeting are not market movers, the fact the current one is taking place in the aftermath of the Trump administration’s decision to impose tariffs on imported steel and aluminum could render any remarks on trade of importance. Any comments on the exchange rate are likely to generate attention as well.

In equities, companies continue to release quarterly results though overall sentiment is expected to be continued to be driven by developments on trade or any breakthrough on the political front, for example in relation to the Italian elections held in early March or the upcoming meeting between Trump and North Korea’s Kim Jong Un.

Gold Bearish Structure Remains In Focus, Slips Below 23.6% Fibonacci Retracement Level

Gold is posting a bearish day after finding resistance at the 40-simple moving average in the 4-hour chart. Moreover, the price dropped below the 23.6% Fibonacci retracement level at 1317.80 of the downleg from 1366 to 1303, endorsing the scenario for further losses.

Looking at the 4-hour chart, the Relative Strength Index (RSI) is sloping to the downside in the negative territory, while the MACD oscillator created a bearish cross within its moving averages below the zero line, signaling the downside movement is continuing.

The bearish phase remains in play especially if gold price continues to trade below the 23.6% Fibonacci mark and the next immediate support stands at 1313. Further decline could open the door for the 1307 barrier taken from the low on February 8. Falling below this area could see the 1303 support level is acting as a strong obstacle for the bears.

On the flip side, in case of a jump above the 38.2% Fibonacci level near 1327 could drive the precious metal towards the 50.0% Fibonacci barrier at 1334. Further gains could lead the way towards the 1340 significant resistance level.

Markets Buoyed By Jobs Data And US Tariff Update

US equity markets are on course to open around half a percentage point higher on Monday, adding to Friday’s gains which came following an encouraging jobs report for February.

The numbers we saw on Friday provided the perfect balance of strong job creation and softer wage growth which does not necessarily trigger faster rate hikes. The much higher participation rate was a clear reminder that, while unemployment is at a 17-year low, there is still some slack in the economy which may take longer to sort out and explain why wage growth and inflation is so muted.

Dollar Lower on Risk Appetite Recovery

This is why we didn’t see the kind of knee jerk reaction in the markets that we saw a month ago. Policy makers will likely be looking at the data and see it as evidence that slack still remains and no additional tightening is needed as a result of the strong employment gains. Of course, this is just one jobs report and future reports could show stronger wage growth but for now, investors are comfortable with the numbers.

Another apparent softening in Donald Trump’s stance on trade tariffs is also providing a small boost to sentiment this morning. Trump is clearly using these tariffs to force the hand of those allies that he believes are taking advantage of the US. Whether this is the best way to get more cooperation is another matter but investors are becoming more encouraged by his recent acknowledgement that a reduction could be imposed for some countries.

Goldilocks is back at the table

This week is looking a little quieter than the last couple but there are some notable things that traders will have an eye on. The inflation and retail sales data from the US over the next couple of days stands out, particularly following those jobs numbers on Friday. Tomorrow’s CPI number isn’t the Fed’s preferred measure but, coming a week before the March Fed meeting when another rate hike is expected, as well as new economic projections, it will be monitored very closely.

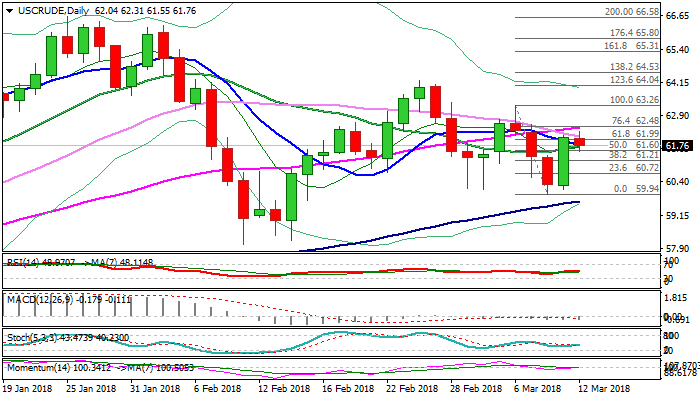

Technical Outlook: WTI – Friday’s Bullish Outside Day Was Bullish Signal But Recovery May Consolidate Further Before Resuming

WTI oil eased after attempts to extend Friday's strong rally ran out of steam at $62.31 on Monday.

Bullish signal was generated on Friday's strong rally which formed bullish outside day on the biggest one-day rally since 14 Feb.

Daily techs are gaining fresh momentum on probes through a batch of MA's, as recent gains retraced over 61.8% of $63.26/$59.94 bear-leg.

Close above here is needed for fresh bullish signal for extension of recovery from $60.00 zone, where last week's fall was rejected.

Cut in US oil rigs which came for the first time in nearly two months also helped oil price to rise, however, fears of increase of US oil output keeps gains limited for now.

Near-term price action is holding in thick daily cloud and broken cloud base ($61.23) marks strong support which is expected to hold and maintain positive near-term structure.

Res: 62.31, 62.56, 62.77, 63.26

Sup: 61.55, 61.23, 60.72, 60.13

Market Update – European Session: Risk Appetite Continues To Be Revived

Notes/Observations

Asia:

Japan LDP Moriyama: Finance Ministry (MOF) admits that the related Moritomo land sale documents were altered. PM Abe's Wife, Akie Abe, said to be among the names of those deleted from the MOF documents (**Note: Moritomo involved the sale of certain state-owned land at a discount)

MOF Official: there were alterations on 62 out of 78 pages related to controversial land sale

Japan Fin Min: no intention to resign over alterations in land sale document

China Commerce Min Zhong Shan: Any trade war with the United States will only bring disaster to the world economy; China does not want a trade war and will not initiate one

Australia PM Turnbull confirmed that Australia would be exempt from the US tariffs on steel and aluminum

Europe:

Bank for International Settlements (BIS) March 2018 Quarterly Review: Central banks should continue to normalize policy

ECB's Draghi and German Bundesbank members said to expect to back Ireland's Lane for the post of chief economist at the ECB when it comes up for renewal next year

'No-deal' Brexit, companies in the UK and EU could face £58B in extra annual costs. EU 27 countries (outside of the UK) will have to pay £31B/year in tariff and non-tariff barriers. In return, exporters in the UK may also have to pay £27B/year to the EU

UK consumer spending suffers weakest start since 2012 as British consumers tightened their belts – Visa. Inflation-adjusted consumer spending in February was 1.1 percent lower than a year earlier, after a 1.2 percent decline in January.

Americas:

Fed’s Bullard (dove, non-voter) reiterated 4 interest rate hikes in 2018 could slow the economy

North Korea Kim Jung-un and US President Trump likely to meet in border truce village of Panmunjom for May meeting

Energy:

Iran Oil Minister Zanganeh said OPEC could agree in June to begin reducing oil output cuts in 2019. Wanted OPEC to attempt to keep oil prices near $60/bbl to contain shale producers

Economic Data:

(NL) Netherlands Jan Manufacturing Production M/M: -0.4% v 0.8% prior; Y/Y: 7.1% v 5.6% prior, Industrial Sales Y/Y: 5.5 v 0.9% prior

(JP) Japan Feb Preliminary Machine Tool Orders Y/Y: 39.5% v 48.8% prior

(DK) Denmark Jan Current Account (DKK): 9,4 v 14.28B prior; Trade Balance: 6.0B v 6.1B prior

(DK) Denmark Feb CPI M/M: 0.7% v 0.8%e; Y/Y: 0.6% v 0.7%e

(DK) Denmark Feb CPI EU Harmonized M/M: 0.6% v 0.7%e; Y/Y: 0.5% v 0.6%e

(TR) Turkey Jan Current Account Balance: -$7.1B v -$6.9Be

(SE) Sweden Mar SEB Housing Price Indicator: +4 v -7 prior

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.4% at 379.6, FTSE fat at 7225, DAX +0.8% at 12440, CAC-40 +0.3% at 5289, IBEX-35 0.5% at 9737, FTSE MIB +0.3% at 22813 , SMI +0.5% at 8979, S&P 500 Futures +0.4%]

Market Focal Points/Key Themes: European Indices trade mostly higher across the board tracking strong gains in Wallstreet overnight and positive futures this morning following a strong Feb NFP reading. The Dax outperforms this morning after EON reached agreement to acquire Innogy stake from RWE, with Innogy trading over 10% higher. Elsewhere GKN trades higher after receiving a final increased offer from Melrose. In earnings news Aryzta, Bavarian Nordic trade lower after results, while Clarkson trades higher. Sixt trades higher after announces a special dividend, while Air France also outperforms after press reports on interest to acquire Air India.

Movers

Consumer Discretionary [ Arzyta [ARYN.CH] -2.9% (Earnings), Air France [AF.FR] +2.7% (consortium reportedly considering Air India acquisition)]

Industrials [GKN [GKN.UK] +1.1% (Raised offer from Melrose), Leonardo [LDO.IT] +1.2%, Hochtief [HOT.DE] +1.2% (Consortium contract win)]

Energy [EON [EOAN.DE] +5.2%, Innogy [IGY.DE] +13%, RWE [RWE.DE] +8.5% (EON to acquire RWE's Innogy stake), EDF [EDF.FR] +1.0% (Reportedly final agreement for sale of 6 EPR's in India may complete by year end)]

Speakers

ECB's Coeure (France) reiterated view that inflation is yet at the point where they want it to be for the Euro Zone; growth is strong and robust. Growth is too dependent on monetary policy at this time

Norway Finance Ministry: 2018 GDP growth already above trend and saw it picking up over the coming two years

Norway PM Solberg: Good economic times demanded moderation in the budget. Too much spending could push the NOK currency (Krona) stronger

Poland Central Bank March Staff Projections cut its 2018 CPI from 2.3% to 2.1% while maintaining the 2019 CPI at 2.7%. It set 2020 CPI at 3.0%. Raises 2018 GDP growth from 3.6% to 4.2% and 2019GDP growth from 3.3% to 3.8% and set 2020 GDP growth at 3.6%

Japan PM Abe stated that he wanted Finance Minister Aso to take responsibility for Moritomo land investigation. The PM added the he felt responsible and apologized to the people

Indonesia Finance Min Indrawati: To curb budget deficit at a safe level. To monitor exchange rates and oil prices

Canada Fin Min Morneau: Wanted existing trade relationship with UK to be the framework for its future ties with the country after Brexit

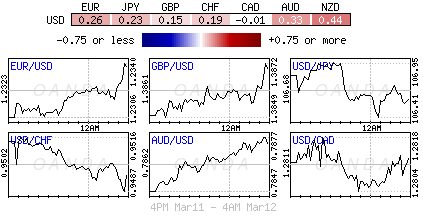

Currencies

USD was marginally softer in quiet trading on Monday.

EUR/USD in the mid-point of its 2018 4 big figure range as dealers have the impression that the ECB was in no rush to hike rates once it potentially stopped its QE-related balance sheet expansion in September. Pair at 1.2330 just ahead of the NY morning.

GBP/USD was firmer as analysts now forecasted its expectations for Gilt issuance of £98.2B for current fiscal year (was £115.1B back in Nov statement) as the Chancellor of the Exchequer prepared to announce the smallest deficit in a decade during his Spring Statement on Tuesday. GBP/USD trying to edge back towards the 1.39 area.

USD/JPY was slightly lower as global risk appetite seemed to have new legs. The JPY managed to shrugged off a scandal simmering within Japan on a land transaction. Finance Ministry (MOF) admitted that the related Moritomo land sale documents were altered. PM Abe's wife said to be among the names of those deleted from the MOF documents. Pair in the mid-part of the 106 handle ahead of the NY morning.

Fixed Income

Bund Futures trade 4 ticks higher at 157.09 trading in a tight range on a quiet start to the week. Upside targets 157.50, while a return lower targets the 155.75 level.

Gilt futures trade at 122.31 up 3 ticks as markets prepare for Gov'ts half-yearly update on public finances. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Monday's liquidity report showed Friday's excess liquidity rose to €1.898T from €1.886T prior. Use of the marginal lending facility stayed steady €0M.

Looking Ahead

(IL) Israel Central Bank (BOI) Feb Minutes

(MX) Mexico Feb ANTAD Same-Store Sales Y/Y: No est v 3.9% prior

06:00 (GR) Greece Jan Industrial Production Y/Y: No est v 0.2% prior

06:00 (IT) Bank of Italy (BOI) Publishes '2017 Households Income and Wealth' Report

06:00 (EU) Daily Euribor Fixing

06:00 (IT) Italy Debt Agency (Tesoro) to sell €6.5B in 12-month Bills

06:30 (DE) Germany to sell €2.0B in 6-Month BuBills

07:00 (PT) Portugal Jan Trade Balance: No est v -€1.4B prior

07:00 (PT) Portugal Feb Final CPI M/M: No est v -0.7% prelim; Y/Y: No est v 0.6% prelim

07:00 (PT) Portugal Feb Final CPI EU Harmonized M/M: No est v -0.6% prelim; Y/Y: No est v 0.7% prelim

07:25 (BR) Brazil Central Bank Weekly Economists Survey

07:30 (CL) Chile Central Bank Economists Survey

07:45 (US) Daily Libor Fixing

08:00 (IN) India Feb CPI Y/Y: 4.7%e v 5.1% prior

08:00 (IN) India Jan Industrial Production Y/Y: 6.4%e v 7.1% prior

09:00 (IN) India announces details of upcoming bond sale (held on Fridays)

09:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming auctions

09:05 (UK) Baltic Dry Bulk Index

09:55 (FR) France Debt Agency(AFT) to sell combined €6.0-7.2B in 3-month, 6-month and 12-month BTF Bills

10:00 (EU) Euro area finance ministers (Eurogroup) meet in Brussels

10:30 (EU) ECB announces Covered-Bond Purchases

10:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:45 (UK) BOE back back 3-7-year Gilts

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

11:30 (US) Treasury to sell 3-Year Notes

12:00 (IS) Iceland Feb International Reserves (ISK): No est v 671B prior

13:00 (US) Treasury to sell 10-Year Notes Reopening

14:00 (US) Feb Monthly Budget Statement: -$216.0Be v $49.2B prior

Dollar Lower On Risk Appetite Recovery

Monday March 12: Five things the markets are talking about

Global equities have advanced overnight as 'trade-war' concerns take a back seat to economic optimism following last Friday's U.S jobs report.

The 'mighty' U.S dollar has eased a tad along with U.S treasury prices and most commodities.

On Tuesday, the OECD will release new forecasts for growth in the major economies, and likely will raise its projections for the U.S in response to the tax and spending packages passed in recent months. In the U.K, Treasury chief Philip Hammond is due to present fresh forecasts for their economy and public finances in a statement to Parliament. In the U.S, headline inflation may have edged up to +2.2% in February, though consensus for core inflation is to remain at +1.8%.

In China, data on industrial production (IP), retail sales and fixed-asset investment all out on Wednesday and are likely to point to slower growth. While in the U.S, retail sales for February will be released.

On Thursday, Norway's Norges Bank releases its policy statement along with the Swiss National Bank's (SNB) libor rate release.

Note: In December, Norway's central bank governor appeared to turn more bullish on the Norwegian economy, with inflation picking up in Q4, 2017.

On Friday, the U.S will release housing starts data for February. Market expectations are looking for a decline after January's robust growth print.

Note: Daylight saving time began on Sunday, March 11, while British Summer Time begins on March 25.

1. Stocks trade in the 'black'

In Japan, the Nikkei share average rallied to a two-week high overnight helped by tech stocks, but early gains were trimmed as a suspected political scandal dampened sentiment. The Nikkei ended +1.7% higher, while the broader Topix rallied +1.5%.

Note: Questions over the sale of state-owned land at a huge discount to a school operator with ties to PM Abe's wife became public last year.

Down-under, Aussie shares rallied on Monday as Friday's U.S jobs report has boosted global investor sentiment while material stocks finished strong on news that Australia could be exempted from new U.S trade tariffs on steel and aluminum imports. The S&P/ASX 200 index rose +0.6% at the close of trade. In S. Korea, the Kospi allied +1%.

In Hong Kong, benchmark stock index traded atop of their five-week highs as fears of a global trade war, and faster U.S rate hikes eased. The Hang Seng index rose +1.9%, while the China Enterprises Index gained +2.1%.

In China, stocks climbed for a third consecutive session. At the close, the Shanghai Composite index was up +0.6%, while blue-chip CSI300 index was up +0.5%.

In Europe, regional indices trade mostly higher across the board tracking the strong gains in Asia following Friday's robust U.S job numbers.

U.S stocks are set to open in the 'black (+0.4%).

Indices: Stoxx600 +0.4% at 379.6, FTSE fat at 7225, DAX +0.8% at 12440, CAC-40 +0.3% at 5289, IBEX-35 0.5% at 9737, FTSE MIB +0.3% at 22813, SMI +0.5% at 8979, S&P 500 Futures +0.4%

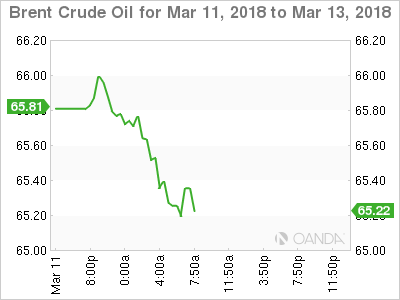

2. Oil eases on output projections, gold lower

Oil prices have eased on expectations that U.S output will rise this year, erasing earlier gains buoyed by lower weekly U.S rig counts.

Brent crude futures are at +$65.11 per barrel, down -38c from Friday's close, while U.S West Texas Intermediate (WTI) crude futures fell -27c to $61.77 a barrel.

Baker Hughes data on Friday showed that U.S energy companies last week cut oil rigs for the first time in almost two-months, with drillers cutting back four rigs, to 796.

Note: Despite the lower rig count, activity remains much higher than a year ago – 617 rigs were active. The U.S is now the world's no. 2 crude oil producer (+10.37m bpd), ahead of top exporter Saudi Arabia. Only Russia pumps more, at nearly +11m bpd.

Gold prices have eased, pressured by a stronger equity market on easing fears of inflation and faster U.S rate hikes. Spot gold is -0.3% lower at +$1,316.10 per ounce.

3. Yields little changed in quiet trading

On Thursday, Norway's central bank (Norges) is widely expected to keep its benchmark interest rate at +0.50%, but some analysts are debating that the recent reduction of the bank's inflation target to +2% from +2.5% and robust economic activity support the case for a rate hike in Q3/Q4.

Elsewhere, German Bund yields held within sight of their recent lows after the ECB's Benoit Coeure said short-term interest rates are to stay at “very low levels,” supporting market consensus any exit from stimulus will be slow. German 10-year yield is unchanged at +0.65%.

The yield on U.S 10-year Treasury notes has backed up +1 bps to +2.90%, the highest in more than two weeks, while in the U.K, the 10-year Gilt yield has decreased -1 bps to +1.489%

4. Dollar lower on risk appetite recovery

The USD is a tad softer in quiet trading.

EUR/USD (€1.2310) trades in the middle of this years four big figure range on market expectations that the ECB is in no hurry to hike rates once it potentially stops its QE-related balance sheet expansion in six-months.

Sterling (£1.3855) is a tad firmer as dealers forecast their expectations for Gilt issuance of +£98.2B for current fiscal year (was +£115.1B back in Nov statement) as the Chancellor of the Exchequer prepares to announce the smallest deficit in a decade during his Spring statement on Tuesday.

USD/JPY (¥106.58) is slightly lower as global risk appetite improves. At the moment, the JPY has managed to shrug-off PM Abe's land transaction scandal – the Finance Ministry (MOF) admitted that the related Moritomo land sale documents were altered. PM Abe's wife said to be among the names of those deleted from the MOF documents.

5. New Zealand CPI gauge falls on lower college fees

New Zealand consumer prices fell last month, with ANZ's monthly gauge down -0.3% in February from January on an -18% plunge in university fees.

Ex-college fees, growth would have been +0.1% last month. Meanwhile, the overall number was +3.1% higher than a year earlier.

Digging deeper, impacting the February's inflation print the most was rent and home buying.

Nevertheless, in line with global expectations, analysts believe that New Zealand's broad-based inflation pressures are still lacking and that the data does not suggest that a sustained lift in price growth will appear any time soon.

ECB Smets: Inflation pressures could take more time to build

ECB Governing Council member Jan Smets

- "It will take somewhat more time to get to the objective than we thought earlier,"

- "The level of potential output may have become higher due to structural reforms and... slack may be bigger."

- "It may take more than we thought and inflation pressures could take more time to build,"

- "(But) it is absolutely crucial that we meet our price stability objective and not accept a level below that; the objective is what it is and we are not there yet."

- "We expect exchange rate movements to correspond to fundamentals,"

- "It would be too early to conclude that growth is plateauing,"

- "Some soft indicators have been a bit weaker but the recovery is on solid footing and we are in a clear, expansionary period."

EUR/USD – Lack of Indicators Leaves Euro Subdued

The euro has edged higher in the Monday session. Currently, EUR/USD is trading at 1.2298, down 0.07% on the day. On the release front, it’s a very light calendar, with no major releases in the eurozone or the US. On Tuesday, the US releases CPI, which is expected to drop to 0.2%.

Is the German industrial sector in trouble? Last week’s numbers were surprisingly soft. Factory Orders in January plunged 3.9%, worse than the estimate of -1.9%. This marked the second decline in the past three months. This was followed Industrial Production, marking a second straight decline. Still, the German economy has performed well, and has led the impressive recovery in the eurozone.

The EU is seeing red after US President Trump made good on his threat, and signed an order imposing 25% tariffs on steel imports. EU policymakers have threatened to retaliate with tariffs on US goods, and European Commission President Jean-Claude Juncker was particularly blunt, saying “we can also do stupid”. Fears of an all-out global trade war are weighing on the US dollar and the stock markets, and the resignation of Gary Cohn, a senior economist in the White House who opposed the tariffs, will only dampen investor risk appetite. The ball is now in the EU court, and if the Europeans retaliate and Trump responds with further tariffs, we could see some sharp movement from EUR/USD.