Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

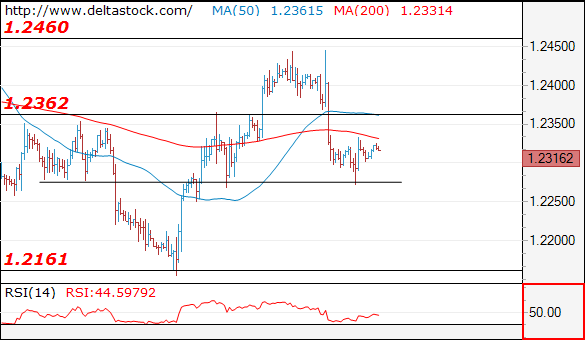

EUR/USD

Current level - 1.2316

Intraday allow a test of 1.2360 resistance before drowning towards 1.2160.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2360 | 1.2460 | 1.2280 | 1.2160 |

| 1.2460 | 1.2560 | 1.2160 | 1.2090 |

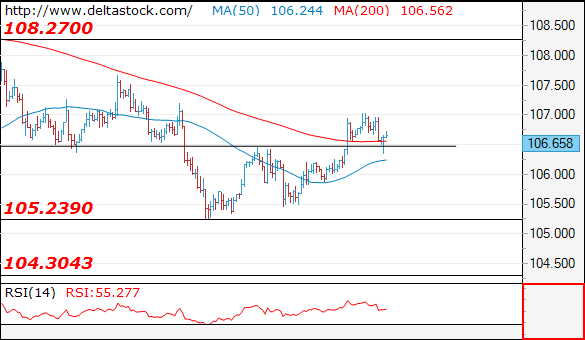

USD/JPY

USD/JPY

Current level - 106.65

The outlook remains positive above 106.30 area and a break through 107.00 will challenge 107.60.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.00 | 108.30 | 106.30 | 105.20 |

| 108.00 | 110.40 | 105.85 | 102.40 |

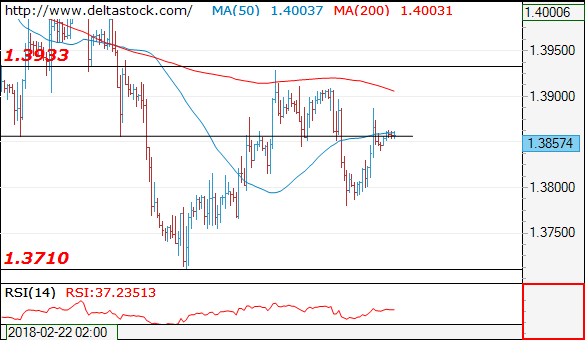

GBP/USD

Current level - 1.3857

The rebound after 1.3780 has neutralized the bearish bias and the intraday outlook is neutral. Minor support is projected at 1.3840.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3930 | 1.4060 | 1.3830 | 1.3710 |

| 1.3930 | 1.4280 | 1.3780 | 1.3620 |

EUR/USD Topside Better Protected Post-ECB?

Rates: Underperformance US T-Note on US supply?

Today's eco calendar is empty apart from a (heavy) start to the US's mid-month refinancing operation. That could cause more underperformance of the US Note future against the Bund in an otherwise slow trading session. Trump's protectionist trade policy remains a wildcard.

Currencies: EUR/USD topside better protected post-ECB?

On Friday, the payrolls failed to give clear guidance for the dollar. This week, the US data (CPI and retail sales) might be slightly USD supportive. We also keep an eye at ECB comments. More indications on ECB tapering beyond September might temporary take some shine off the euro.

The Sunrise Headlines

- US stock markets rose by 1.75% on Friday after the “goldilocks” US payrolls report. Asian stock markets trade around 1% higher this morning with Japan outperforming (+1.5%).

- Japanese FM Aso is coming under pressure to resign as a scandal over alleged favors to a school with connections to Japanese PM Abe deepened. He apologized and said that he is not thinking about resigning.

- American and European officials are planning new trade talks this week as US allies seek ways to avoid steel and aluminum tariffs. China signaled it is poised to retaliate if President Trump implements his “America first” economic action.

- The recent volatility in global financial markets should not deter top central banks from lifting interest rates or ending years of unprecedented stimulus, the Bank for International Settlements said.

- Philip Hammond said Britain may soon start to see the beginning of the end of austerity, as he prepares to announce the smallest deficit in a decade during his spring statement on Tuesday.

- Australia has secured an exemption from metals tariffs announced last week by US President Trump, PM Turnbull told the media.

- Today's eco calendar only contains US auctions. The Treasury sells $28bn 3-yr Notes and $21bn 10-yr Notes

Currencies: EUR/USD Topside Better Protected Post-ECB?

US payrolls fail to give USD clear direction

On Friday morning, there was little follow-through action in EUR/USD after Thursday's ECB meeting. US payrolls (strong job growth, but soft wages) caused only a subdued market reaction. EUR/USD filled bids in the 1.2275 area around the time of the publication, but the decline was blocked. EUR/USD closed at 1.2307. Strong US equities were basically neutral for EUR/USD, but kept USD/JPY well supported (close at 106.82).

Overnight, Asian equities join the post-payrolls rally from WS on Friday. In Japan there are plenty of headlines on a scandal regarding a land sale where PM Abe, his wife and the finance Ministry might to be involved. The headlines tempered initial market euphoria. Japanese equities returned part of the gains. The yen gained slightly ground, but remains within established ranges. The Australian dollar (AUD/USD 0.7869 area) rebounded after US president Trump gave the country an exemption to the steel and aluminum tariffs.

Today's eco calendar is thin, but the US treasury will sell 3 and 10-yr bonds. Last month, US bond auctions were a factor of volatility for global markets. The potential impact on the dollar was/is ambiguous. The context now looks a bit less tense. Decent auctions shouldn't be too bad for the dollar. US CPI and the retail sales might be important for the dollar later this week. Expectations for price data might be rather cautious after Friday's wage data. Maybe there is room for some further dollar gains in case of decent US data. We also keep an eye at ECB comments. Will they give some hints on a tapering of APP after September? If so, it might cause some downscaling of euro longs. The US tariffs' debate remains a wildcard for USD trading. Last week, EUR/USD showed no clear trend. The post ECB price action suggests that the EUR/USD topside is rather well protected for now. Constructive US eco data might cause a renewed EUR/USD test of the 1.2155 area.

At the end of last week, sterling succeeded a technical rebound as Brexit noise again subsided. The UK eco calendar is thin this week. For now there is no trigger for a clear directional move in EUR/GBP. Some further range trading near current levels might be in the cards

EUR/USD: topside better protected post-ECB?

Dollar Falls With Inflation Figures The Next Catalyst, Equities On The Rise

Here are the latest developments in global markets:

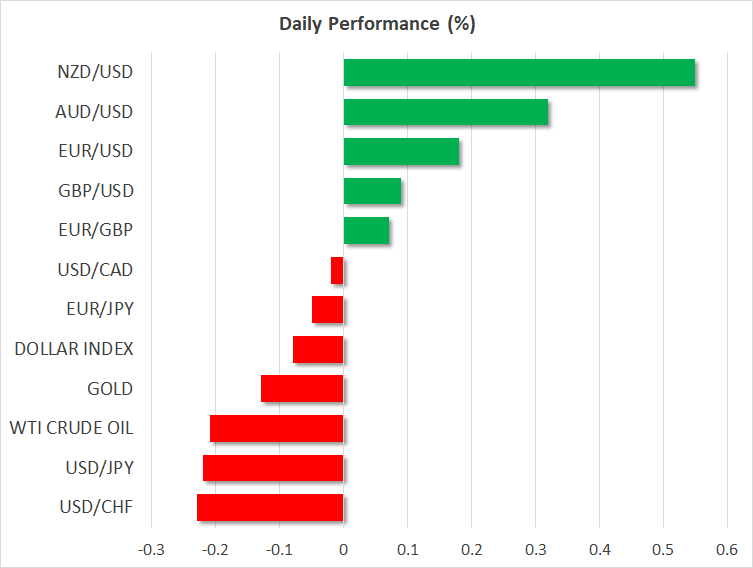

FOREX: The dollar was losing some ground versus a basket of currencies on Monday after recording its highest since March 1 last Friday, the day February’s US employment data showed stronger-than-anticipated jobs growth.

STOCKS: US markets surged on Friday on the back of the US employment report, which showed that wage growth remains subdued. The disappointing earnings figures suggest that there is little pressure on the Fed to raise rates aggressively, a factor that boosted risk appetite. The Nasdaq Composite and the Dow Jones both climbed by 1.8%, while the S&P 500 lagged slightly behind, still gaining a robust 1.7%. Importantly, the Nasdaq closed at a record high. Futures tracking the S&P, Dow, and Nasdaq 100 are all flashing green as well. The positive sentiment rolled over into Asian trading on Monday, with Japan’s Nikkei 225 and Topix indices rising by 1.7% and 1.5% respectively, while Hong Kong’s Hang Seng index was up by 1.8%. Europe appears set to follow suit, with futures tracking all the major indices being a sea of green.

COMMODITIES: Oil prices traded lower on Monday, with WTI and Brent crude being down 0.2%, both benchmarks giving back some of the notable gains they posted on Friday. The risk-on sentiment in equity markets in combination with the drop in the number of active US oil rigs helped the precious liquid to rally. The lower rig count is a very encouraging sign for the supply side of the oil market, as it signals that US production may have peaked, for now at least. In precious metals, gold was lower on Monday but not by much, last seen near the $1321/ounce mark. The yellow metal has been under pressure lately as risk appetite staged a comeback, and in case of further declines, the recent lows near $1312 could offer some immediate support.

Major movers: Dollar eases a bit; antipodeans on the rise on improved risk appetite

The dollar index was 0.1% down, falling marginally below the 90 handle after rising to 90.36 on Friday, this being its highest since March 1. Following Friday’s NFP report that showed jobs growth exceeding expectations, the focus for short-term direction for the dollar now turns to Tuesday’s inflation figures for the month of February. It remains to be seen whether tomorrow’s figures will mirror Friday’s wage growth numbers.

Equities were on the rise as worries over a trade war further receded in investors’ minds and Friday’s jobs report out of the US showed wage growth cooling, failing to spur expectations for higher inflation as was the case in the previous month’s report that led to an equity selloff. Market participants for the most part currently expect the Federal Reserve to deliver three quarter percentage point interest rate hikes in 2018.

Politics are at play in Japan, partly dampening risk sentiment and supporting the safe-haven perceived yen. The Finance Ministry altered documents in relation to a controversial land sale and this raises questions about the future of Finance Minister Taro Aso, who is seen as a key person in PM Abe’s government. Aso himself said that he does not intend to resign. At 0731 GMT, dollar/yen was 0.2% down at 106.56.

Euro/dollar was 0.2% up at 1.2330. Eurozone’s common currency recorded losses versus the greenback last week, after ECB chief Mario Draghi noted that inflation in the euro area remains muted following the Bank’s meeting last week, whilst also making reference to the risk of rising protectionism.

The antipodeans were on a positive footing on Monday: aussie/dollar and kiwi/dollar traded higher by 0.3% and 0.55% respectively, both rising to their highest since late February. Positioning was seen as coming on the back of overall elevated risk sentiment, due to easing concerns over trade and rising inflation that could have pushed the US central bank to proceed with a faster pace of monetary policy tightening.

Day ahead: Quiet Monday in a relatively busy week

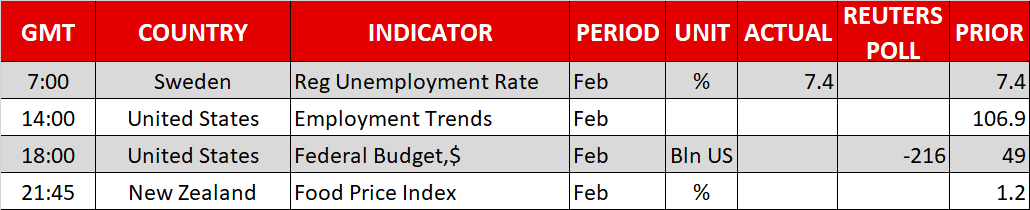

In terms of economic data releases, the calendar is practically empty today. The only indicator that could attract some attention is the US Conference Board’s employment trends index for February, due out at 1400 GMT, though this is usually not a major market mover.

In Europe, the Eurogroup – a term which refers to the finance ministers of the 19 nations that make up the eurozone – will meet to discuss developments in Greece, deepening the Economic and Monetary Union, as well as developments around the exchange rate and inflation. While these meetings typically do not produce much movement in the euro, any comments on the exchange rate will still be closely monitored by traders, especially given the absence of other events today.

The rest of the week is much more interesting as on Tuesday, we will get the all-important US CPI figures for February. Wednesday will see the release of US and Chinese retail sales prints, while on Thursday, the Swiss National Bank (SNB) and the Norges Bank will both announce their rate decisions.

In equity markets, the inflation and the trade-war narratives will likely remain at the forefront. Major stock indices surged on Friday, after the US employment data showed that despite robust jobs growth, wages have still not picked up. The subdued wage figures suggest that there is little pressure on the Fed to raise rates quickly, and if tomorrow’s CPI data confirm this narrative, then we may see more gains in equities. At the same time, investors are likely to keep one eye on any retaliation measures by the EU and China to the US tariffs. The magnitude and the scope of any responses could be a signal of what happens next. If these major economies reply in harsh fashion, that may provoke more US action and increase further the risk of a vicious protectionist cycle, whereas calmer responses could pave the way for a de-escalation in trade tensions.

In politics, developments in Italy could continue to be in focus. On Friday, the leader of the 5-Star Movement (M5S) Luigi Di Maio said that his party was preparing policy proposals for other parties, in order to reach common ground and form a government.

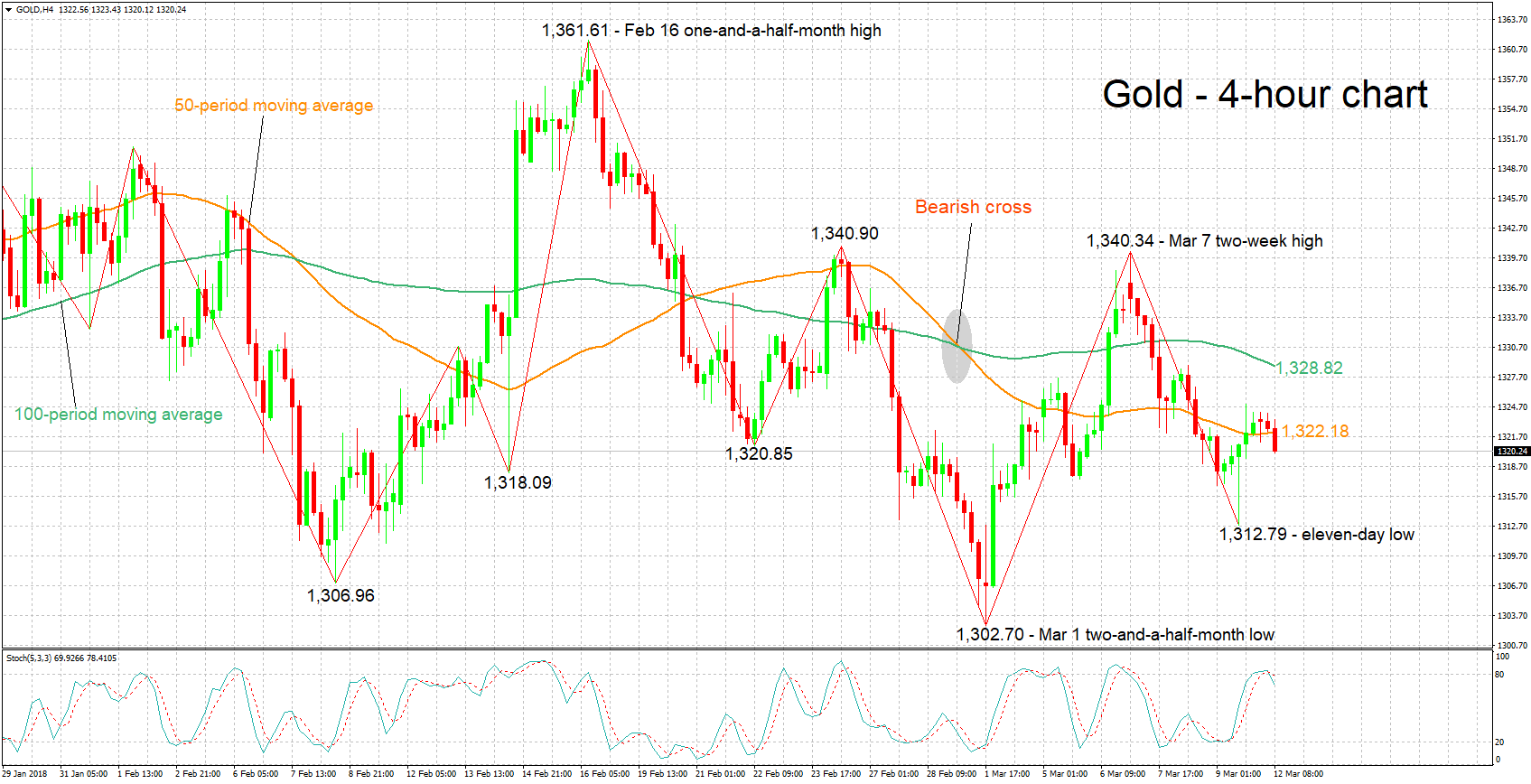

Technical Analysis: Gold rises from 11-day low though stochastics give bearish signal in very short-term

Gold has recovered somewhat after hitting an 11-day low of 1,312.79 during Friday’s trading. It is retreating though at the moment, with the stochastics giving a bearish signal in the very short-term: the %K line has crossed below the slow %D line, with both lines heading lower.

Should the greenback weaken further, then the dollar-denominated metal stands to potentially gain. Resistance in case of rises could come around the current level of the 50-period moving average at 1,322.18. The area around this also encapsulates a couple of bottoms from the recent past. A break to the upside would turn the attention to the 100-period MA at 1,328.82.

On the other hand, a stronger US currency is likely to lead to losses for gold. The range around Friday’s 11-day low of 1,312.79 might offer support. Further below, the focus would increasingly start turning to the two-and-a-half-month low of 1,302.70 from March 1, while the area around a previous bottom at 1,306.96 could also act as support.

Rising or abating trade risks also have the capacity to offer direction to the safe-haven perceived asset.

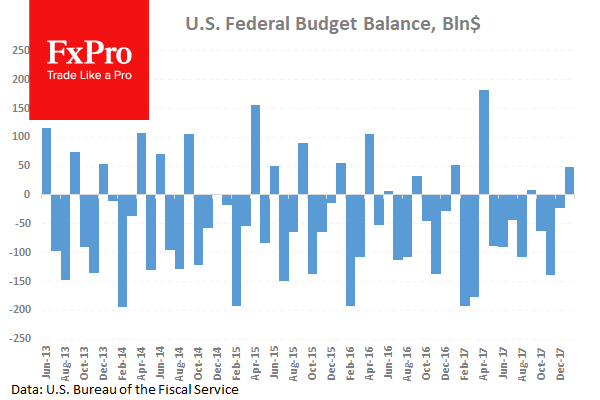

US Monthly Budget Statement In Focus

At 18:00 GMT, the US Monthly Budget Statement (Feb) is expected to fall to $-216B against a reading of $49B in the prior month. This data represents the balance of the federal government’s income and spending. The February number has been negative and in the range of $-234B to $-185B since 2010, due to variation in payments and expenditures that fall during the month. If the reading comes in at or below expectations, it will be the biggest decline in the budget since February of 2014. USD pairs could experience volatility because of this data release.

Major data releases for the week:

On Tuesday, at 11:30 GMT, the UK Budget Report will be released.

At 12:30 GMT, US Consumer Price Index data will be released.

At 14:30 GMT, Bank of Canada Governor Poloz will give a speech titled “Today’s Labour Market and the Future of Work” at Queen’s University, in Ontario.

On Wednesday, at 07:00 GMT, German Consumer Price Index data will be released.

At 08:00 GMT, ECB President Draghi will speak at the ECB conference hosted by the Institute for Monetary and Financial Stability, in Frankfurt.

At 12:30 US Retail Sales data will be released.

On Thursday, at 08:30 GMT, the Swiss National Bank will release it Interest Rate Decision.

On Friday, at 10:00 GMT, Eurozone Consumer Price Index data will be released.

US Earnings And Jobs Data Hit A Sweet Spot For Markets

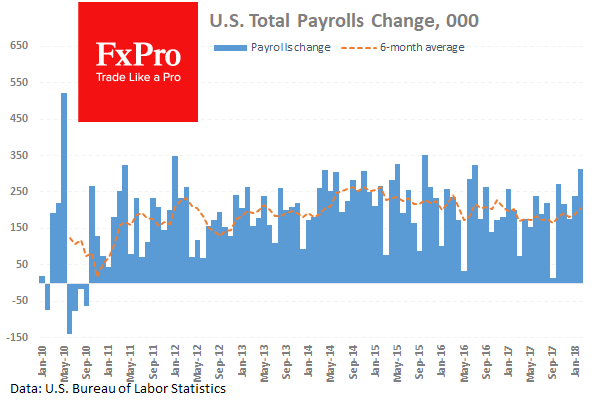

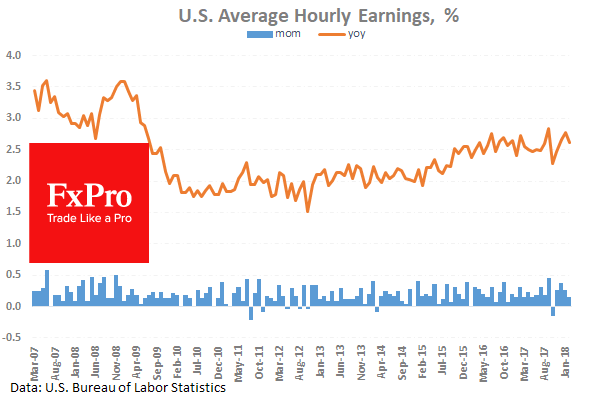

The US Nonfarm Payrolls data released on Friday showed a strong increase in job creation and, combined with the lower than expected increase in Hourly Earnings, sent the markets into risk-on mode. This was a complete reversal of the previous month’s reaction to this data series when positive sentiment evaporated as fears of inflation and interest rate hikes took over. This time, data indicated that the labour market, despite being the tightest it has been in decades, is not putting pressure on wages and, therefore, keeping inflation low. US stock markets roared higher with the Dow up 440 points or 1.77%, the NASDAQ up 1.79% and S&P 500 up 1.74%. Treasury Yield moved higher, as the expectation of 4 rate hikes increases but at a gradual pace. The US dollar was weaker against the AUD, NZD, CAD and GBP but managed to gain against the JPY.

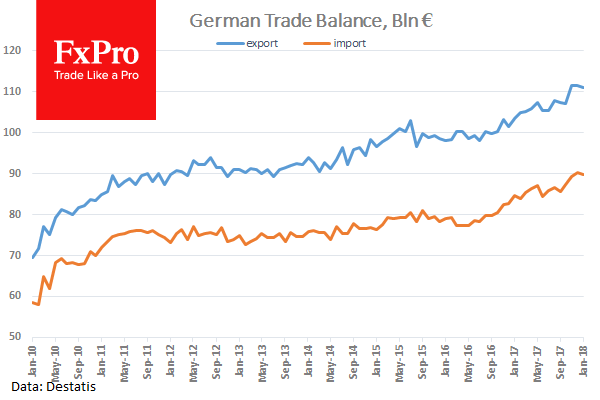

German Current Account n.s.a. (Jan) was €22.0B v an expected €17.2B against a previous €27.8B. Exports (MoM) (Jan) were -0.5% v an expected 0.3%, against 0.3% previously. Imports (MoM) (Jan) were -0.5% v an expected 0.0%, against 1.4% previously. Trade Balance s.a. (Jan) was €21.3B v an expected €21.1B, against a prior €21.4B. The trade balance is showing a slight fall but is inside normal range, with imports down and exports steady. EURUSD fell from 1.23209 to 1.23108.

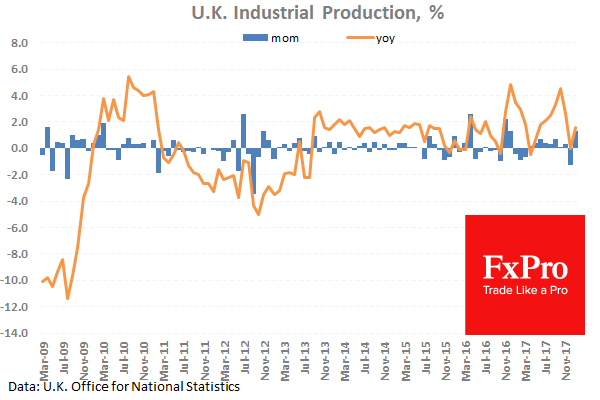

UK Industrial Production (YoY) (Jan) was 1.6% v an expected 1.8%, against a previous 0.0%. Manufacturing Production (MoM) (Jan) was 0.1% v an expected 0.2%, against 0.3% previously. This figure had been less volatile during much of 2017, with readings staying positive but close to zero. Industrial Production (MoM) (Jan) was 1.3% v an expected to be 1.5%, against -1.3% previously. Seasonally, there is generally a downturn in this figure, with a drop in negative territory early in the New Year. This month’s number shows strong performance and is one of the best March readings on record, even if it did miss expectations. Manufacturing Production (YoY) (Jan) was 2.7% v an expected 2.8%, against 1.4% previously. GBPUSD moved between a high of 1.38152 and a low of 1.38014 because of this data release.

UK NIESR GDP Estimate (3M) (Feb) was as expected at 0.3%, against 0.5% prior, which was revised down to 0.4%. The data point has been moving closer to 0.0% since hitting a high of 1.0% in May 2014. However, it has managed to remain positive in that time, with a 0.4% average. GBPUSD reached a high of 1.38407 but fell to a low of 1.38426 after this data release.

US Non-Farm Payrolls (Feb) beat the consensus, coming in at 313K against an expected 200K, from a prior 200K, which was revised up to 239K. The Unemployment Rate (Feb) was 4.1% v an expected 4.0%, with a prior of 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during February. Average Hourly Earnings (YoY) (Feb) was 2.6% v an expected 2.8%, against 2.9% previously, which was revised down to 2.8%. Average Weekly Hours (Feb) was 34.5 v an expected 34.4, against a previous 34.3. Labour Force Participation Rate (Feb) was 63.0% v an expected 62.5%, against a prior reading of 62.7%. Average Hourly Earnings (MoM) (Feb) was 0.1% v an expected 0.2%, against 0.3% previously. It was this data release on the 2nd of February that resulted in the pullback in equity markets last month. On Friday, the opposite occurred, as the combination of strong job creation but low hourly earnings hit a sweet spot for markets and eased fears of higher inflation. EURUSD tested lows at 1.22732 before moving higher to 1.23339, while the S&P 500 rallied from 2733.60 to close the day at highs of 2783.70 due to these data releases.

Canadian Unemployment Rate (Feb) was 5.8% v an expected 5.9%, against a previous 5.9%. Participation Rate (Jan) was 65.5% v an expected 65.6%, against 65.5% prior. Net Change in Employment (Dec) was 15.4K v an expected 20.0K, against a prior -88.0K. Unemployment in Canada is hovering around the lowest levels in ten years. GBPCAD fell from 1.77960 to a low of 1.77374 after this data came out.

Baker Hughes US Oil Rig Counts was released with a headline number of 796, down from last week’s number of 800. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

EURUSD is up 0.13% overnight, trading around 1.23197.

USDJPY is down -0.17% in early session trading at around 106.634.

GBPUSD is up 0.08% this morning, trading around 1.38603.

Gold is largely unchanged in early morning trading at around $1,322.90.

WTI is unchanged this morning, trading around $61.85.

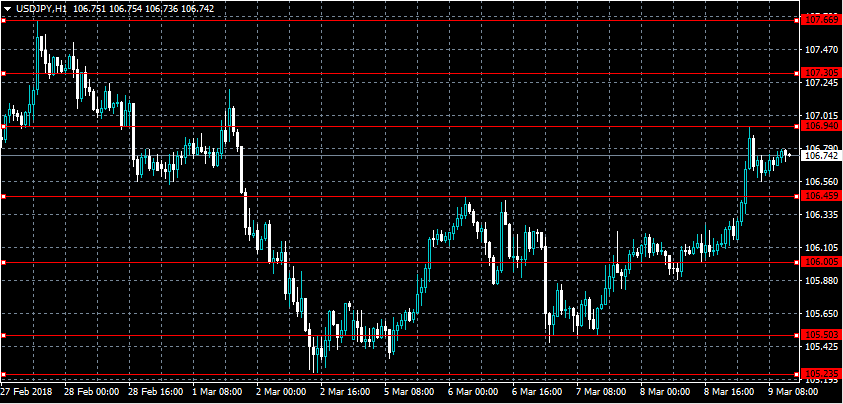

USDJPY Bullish Recovery Above 106.45 Level

The U.S dollar has surged higher against the Japanese yen currency, hitting 106.94, as the Bank of Japan policy meeting revealed Japanese policy makers commitment to monetary easing. The USDJPY pair currently trades around the 106.70 level, with risk-sentiment buoyant after U.S President Donald Trump agreed to meet North Korean leader Kim Jong-Un. Traders now look to the release of the U.S Non-farm payrolls job report this afternoon, with market participants expecting 200,000 new U.S jobs were creating during the month of February.

The USDJPY pair is likely to see further upside whilst trading above the 106.45 level, further gains towards 107.30 and 107.66 seem possible.

If the USDJPY pair moves below the 106.45 level, a technical correction back towards the 106.00 handle may occur.

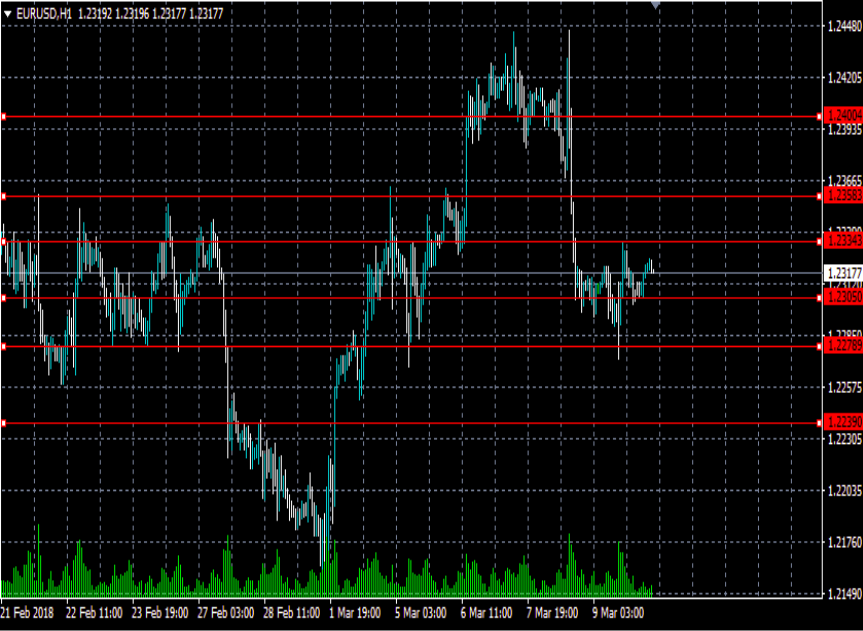

EURUSD Further Bullsh Above 1.2334 Level

The euro continues to trade in a tight range against the U.S dollar, with price-action still largely struggling to find a strong directional bias. The EURUSD pair currently trades around the 1.2320 level, with European investors still digesting Friday’s solid U.S job report and the potential implications of U.S Trade Tariffs. The macroeconomic calendar remains quiet on Monday, EURUSD buyers will look for gains above the 1.2334 level, whilst sellers await a sustained breach of the 1.2305 support level.

The EURUSD pair is likely to see further gains above the 1.2334 level, intraday upside targets remain 1.2358 and 1.2400.

Should the EURUSD pair move below the 1.2305 level for a sustained period, sellers will likely target the 1.2278 level, with further intraday support found below, at 1.2239.

Quiet Monday Kicks Off Active Week In The Market

After a hectic first week of March, the economic calendar will see a much lighter schedule on Monday. However, action will pick up 24 hours later and continue throughout the week, giving market participants the latest information on the US and European economies.

The European release schedule begins at 10:00 GMT with a report on Greek industrial production for February. The January data set showed a 0.2% annualized increase.

One hour later, Portugal will report on the global trade balance as well as the consumer price index (CPI).

Shifting gears to North America, the US Financial Management Service will release its monthly budget statement. The February statement is expected to show a deficit of $222.6 billion, following a surplus of $49 billion the month before.

A relatively quiet release schedule on Monday will allow traders to digest last Friday's US nonfarm payrolls report. The report showed the creation of 313,000 jobs in February, the fastest in a year-and-a-half. Wage inflation was relatively subdued compared to the previous month as unemployment held steady at 4.1%.

The stronger than expected jobs report all but assures traders that the Federal Reserve will raise interest rates at its forthcoming policy meeting on 20-21 March. The rate statement will also be accompanied by a quarterly summary of economic projections.

On Tuesday, market participants can expect headline CPI data from the United States, as well as a key monetary policy speech from Bank of Canada (BOC) Governor Stephen Poloz.

In currency news, the US dollar was relatively unchanged against a basket of its main competitors Monday. The DXY index was last seen trading at 90.04, where it was down 0.1% from the previous close.

EUR/USD

Europe's common currency lost momentum on Friday, reversing a high of 1.2439 all the way back down to the low 1.2300 region. At the time of writing, the EUR/USD exchange rate was up 0.1% at 1.2318. The pair is supported at 1.2273, which corresponds with the 50-day simple moving average. On the upside, immediate resistance is located at the psychological 1.2400 level.

GBP/USD

Cable also backtracked on Friday following the upbeat nonfarm payrolls data. However, the pullback wasn’t nearly as severe as the one seen in the EUR/USD. The GBP/USD hovered in the mid-1.3800 region at the start of Asian trading on Monday. The pair remains well supported above the March low of 1.3712.

USD/JPY

After two days of recovery, the USD/JPY was trading slightly lower on Monday, falling 0.2% to 106.61. The bulls are eyeing a break of the 108 handle to keep the rally alive, although that could prove to be a difficult sell. The pair faces an immediate resistance band around 107.20

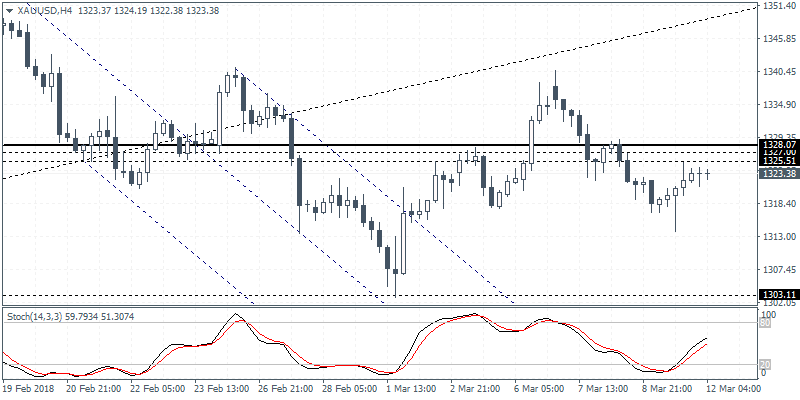

XAUUSD Intraday Analysis

XAUUSD (1323.28):Gold prices continue to drift close to the 1328 level, with Friday's price action seeing the precious metal erasing the intraday losses. We expect this consolidation around 1328 to continue in the near term but the bias remains to the downside for a re-test of 1303 level of support. Gold prices are likely to maintain the range within these levels with further gains or losses coming only on a breakout from either of these levels.

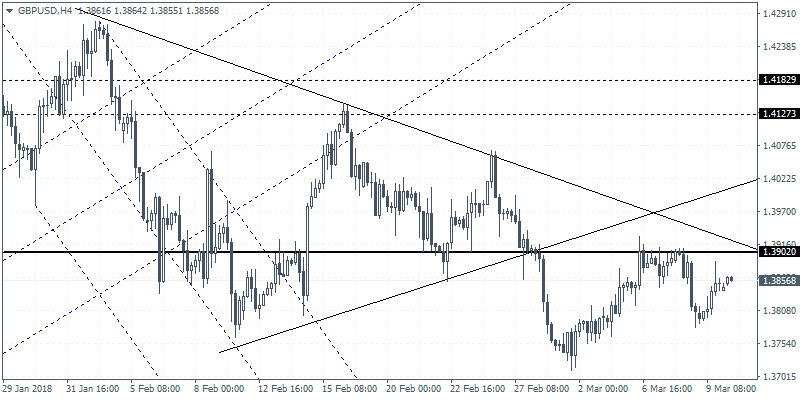

GBPUSD Intraday Analysis

GBPUSD (1.3856):The British pound was seen closing with gains on Friday but price action was seen trading below the 1.3902 level which is acting as support. Failure to breakout above this level on the daily basis could keep GBPUSD biased to the downside. The retest of support level near 1.3611 - 1.3590 is expected but this could change in the event of a close above 1.3902 which could see GBPUSD pushing higher to test 1.4060 level.