Sample Category Title

EURUSD Intraday Analysis

EURUSD (1.2320): The EURUSD closed with a doji on Friday following Thursday's strong losses. With price action closing back below the price level of 1.2363 - 1.2333 level, we expect EURUSD to continue to push lower as a result. The downside target comes in at the previously established low of 1.2179, followed by a move towards 1.2090 - 1.2070 which could be tested as the markets head closer to next week's FOMC meeting. To the upside, a breakout above 1.2333 could signal near term gains but the upside bias seems to be easing.

Payrolls Fail To Lift USD

Friday's nonfarm payrolls showed a solid pace of job creation with the U.S. economy seen adding 313k jobs which beat estimates by a strong margin. However, the U.S. unemployment rate was unchanged at 4.1% which missed estimates of a decline to 4.0%. Although the jobs report was solid, the slow pace of wage creation saw average earnings rising just 0.1% on the month.

The U.S. dollar was seen weakening into Friday's close as a result. Elsewhere, Canada's jobs report showed that the unemployment rate fell from 5.9% to 5.8% while the economy was seen adding 15.4k jobs which were below estimates of a 21.3k job growth that was estimated.

Looking ahead, the economic calendar today is light with no major releases expected. The currency markets are expected to follow through from Friday's price action.

Bulls Are Back In Town, Thanks To U.S. Employers

The robust U.S. jobs report on Friday managed to offset concerns of a trade war, at least for now. The 313,000 additional jobs took economists and markets by surprise as the figure exceeded even the highest expectations of 300,000 noted in a Reuters survey. Although employees may not like the 0.1% rise in average hourly earnings, employers liked it and markets loved it. This is simply because the modest increase in wage growth indicates that the Federal Reserve will continue to have some sort of slack in the labor market to deal with and thus keep the Fed on course for three rate hikes in 2018 instead of four. After all, the combination of robust economic data and limited inflation has been a key factor in keeping the bull market alive.

The NASDAQ Composite Index climbed to a fresh record after the release of Friday's jobs report. The S&P 500 is 10% higher from the trough recorded on 9 February, and fixed income markets aren't showing any signs of anxiety, with U.S. 10-year bonds yields remaining well below the 3% critical level.

Appetite for risk spread to Asian markets today with the Nikkei 225, Hang Seng and Kospi all advancing more than 1%. Futures also indicate a positive start to Europe today.

Other factors that boosted appetite for risk last week were Mr. Trump's acceptance of a meeting with North Korea's Kim Jong Un, though I didn't see it as a game changer for equity investors. News that the U.S. has opened the way for more exemptions from its steel and aluminum tariffs on Friday may have indicated that we're still far from an all-out trade war. However, it seems now that Trump's target is not Canada, nor Mexico or the E.U., but China. China's Minister of Commerce, Zhong Shan, said China does not want a trade war and will not initiate one, but warned that any trade war with the U.S. would only bring disaster to the world economy.

This week, U.S. economic data will be closely scrutinized, particularly February's CPI report, as it's just a few days before next week's Federal Reserve meeting. Consumer prices are expected to have cooled down last month after surging 0.5% in January, but the headline CPI is still forecasted to rise 2.2% YOY, from 2.1%. Investors are likely to give more attention to the core CPI, and if it remained steady at 1.8% there would be no reason to think that the Fed will take an aggressive stance when it meets.

Retail sales are expected to rebound after falling for two consecutive months. If they met the anticipated 0.3% rise, this may suggest that the tax cuts are finally encouraging consumers to save less and spend more.

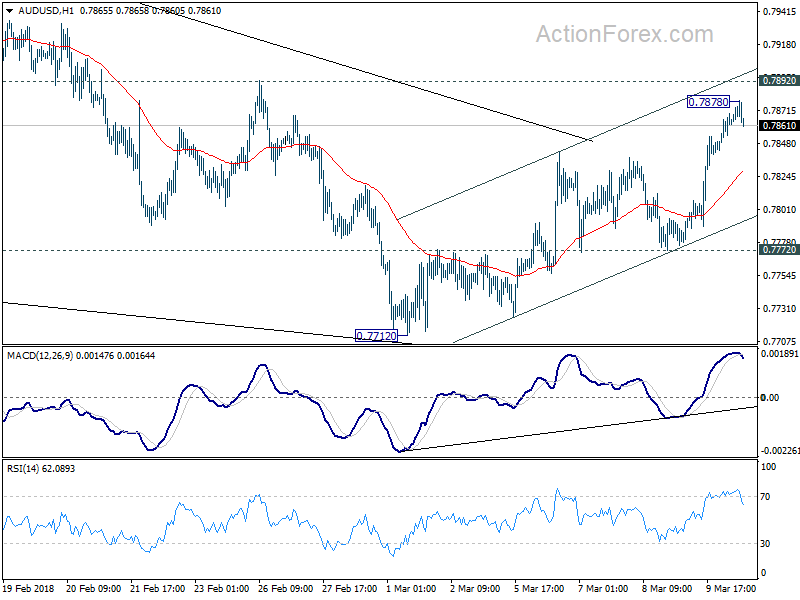

AUD/USD losing momentum ahead of 0.7892 resistance

AUD/USD is trading as one of the strongest currencies for today. But based on 4 hour heatmap, it's starting to lost momentum.

Hourly MACD also suggests that AUD/USD longs might be starting to take profit ahead of 0.7892 near term resistance. 0.7892 is seen as near term trend defining resistance. That is, as long as 0.7892 holds, the decline from 0.8135 is still in progress for another low below 0.7712. But decisive break of 0.7892 should add more credence to the case of near term reversal.

ECB Coeure: Interest rates to say at “very low levels” far beyond end of QE

ECB Executive Board Member Benoit Coeure said that interest rates will stay at "very low levels", "far beyond the end of QE.

He said in French radio BFM business:-

- "It is very clear to us that short term interest rates, the ones that are controlled by the central bank, will remain at very low levels, far beyond the horizon of our asset purchases,"

- "Inflation is not quite where we would like it to be,"

- There was no discussion on a first rate hike in mid-2019

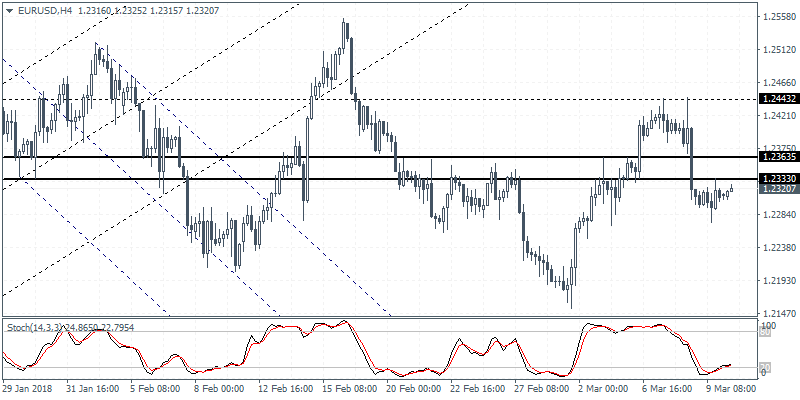

EURUSD Looks Neutral As It Holds In Narrow Range And Below SMAs

EURUSD remains under strong pressure and risk is still to the downside as prices continue to post neutral days after the significant bearish day last Thursday. The short-term technical indicators are flattening and point to more weakness in the market.

Looking at the daily timeframe, the prices are looking capped by the 20 and 40-simple moving averages which are negatively aligned while a bearish crossover is near. The RSI indicator holds near the 50 level with no clear signal and the MACD oscillator is slightly falling below its trigger line and above its zero line.

The next downside target is the 1.2200 psychological level and the 1.2160 support barrier. At this stage, the market would likely see a resumption of the short-term downtrend and touch the next support at 1.2080, which overlaps with the 23.6% Fibonacci retracement level of the upleg from 1.0560 to 1.2540.

Upside moves are likely to find resistance at 1.2445. Rising above this area could shift the focus to the upside towards the 1.2540 resistance level. Breaking this level could see a test of the 1.2570 high taken from the peak in December 2014.

In the short-term, the pair has been developing within a sideways channel since January 12 with upper boundary the 1.2540 barrier and lower boundary the 1.2160 support. In the bigger picture, the market is bullish as long as the ascending trend line since April 2017 holds.

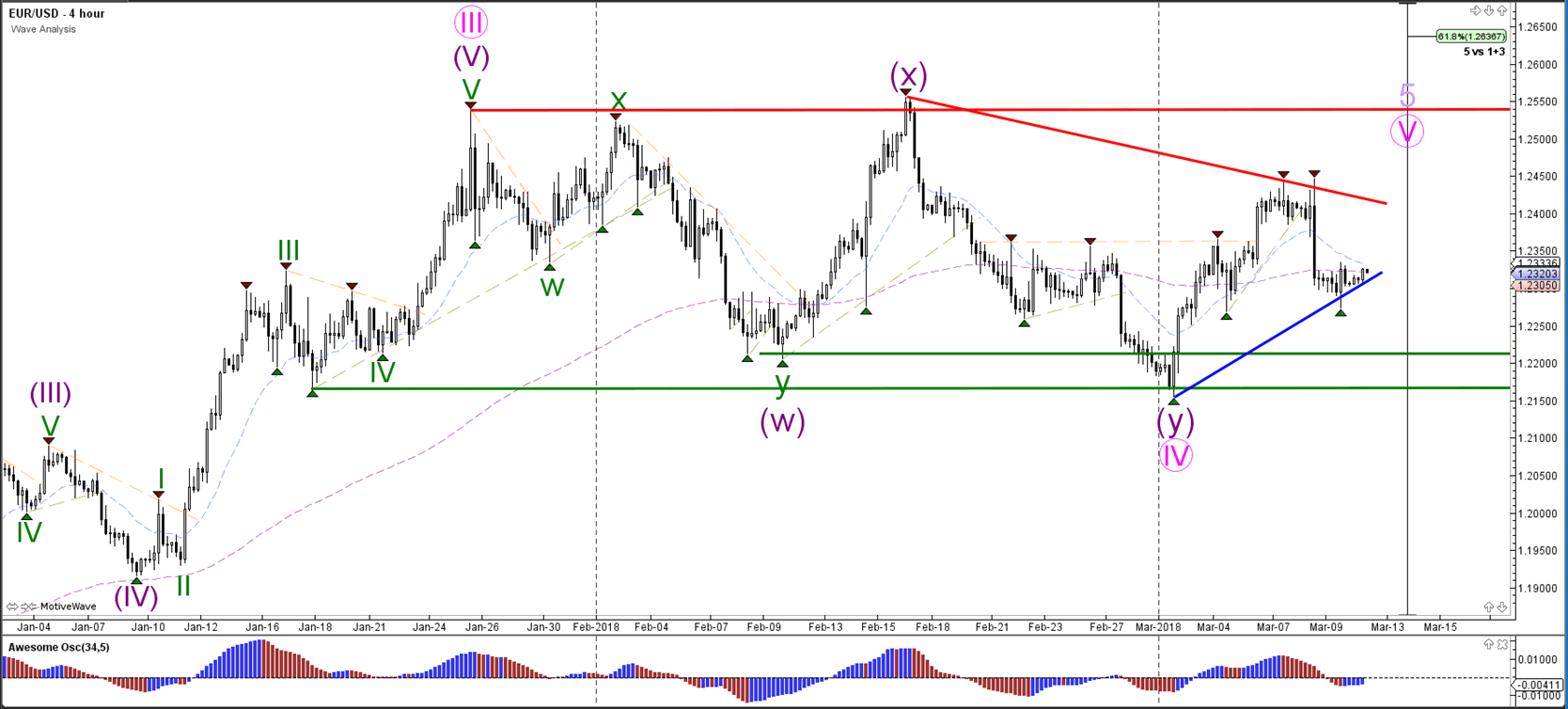

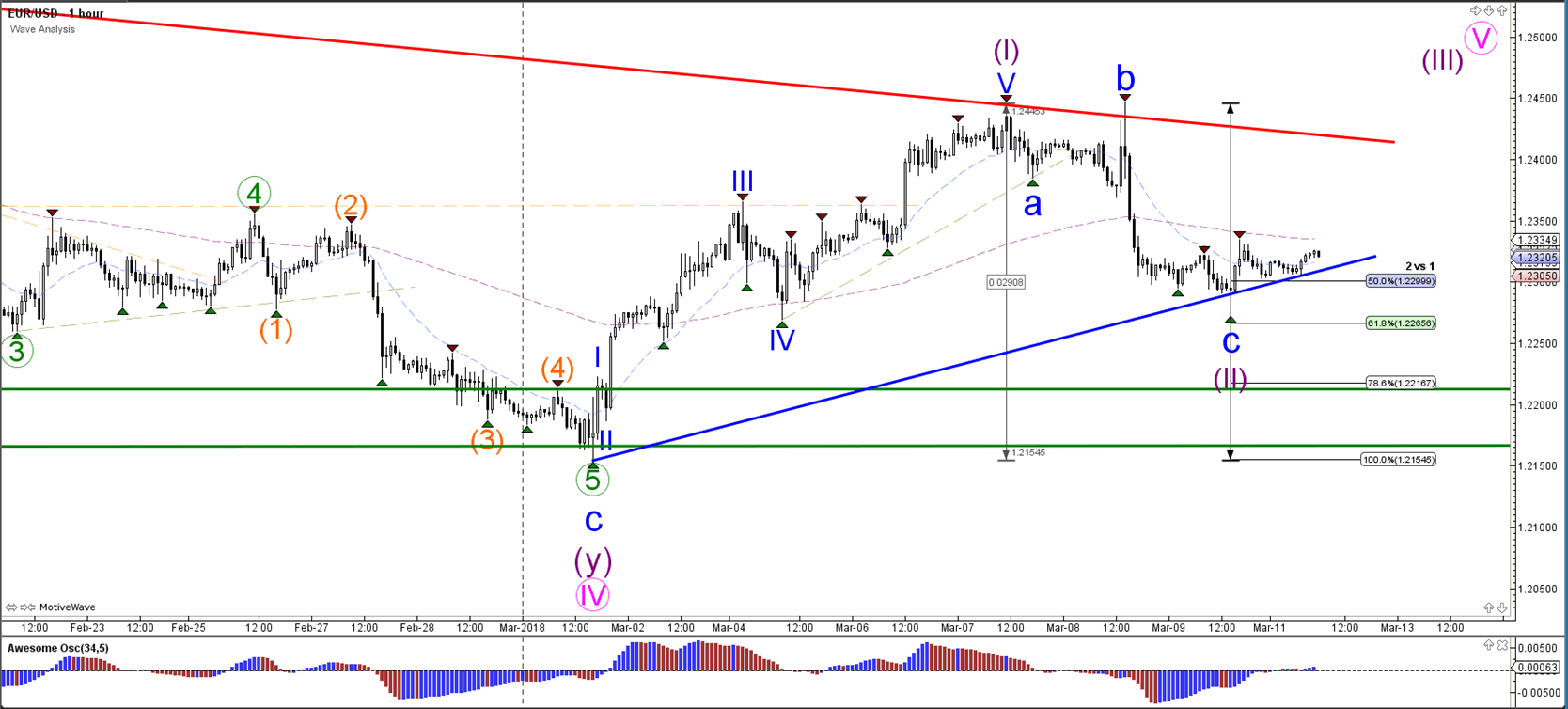

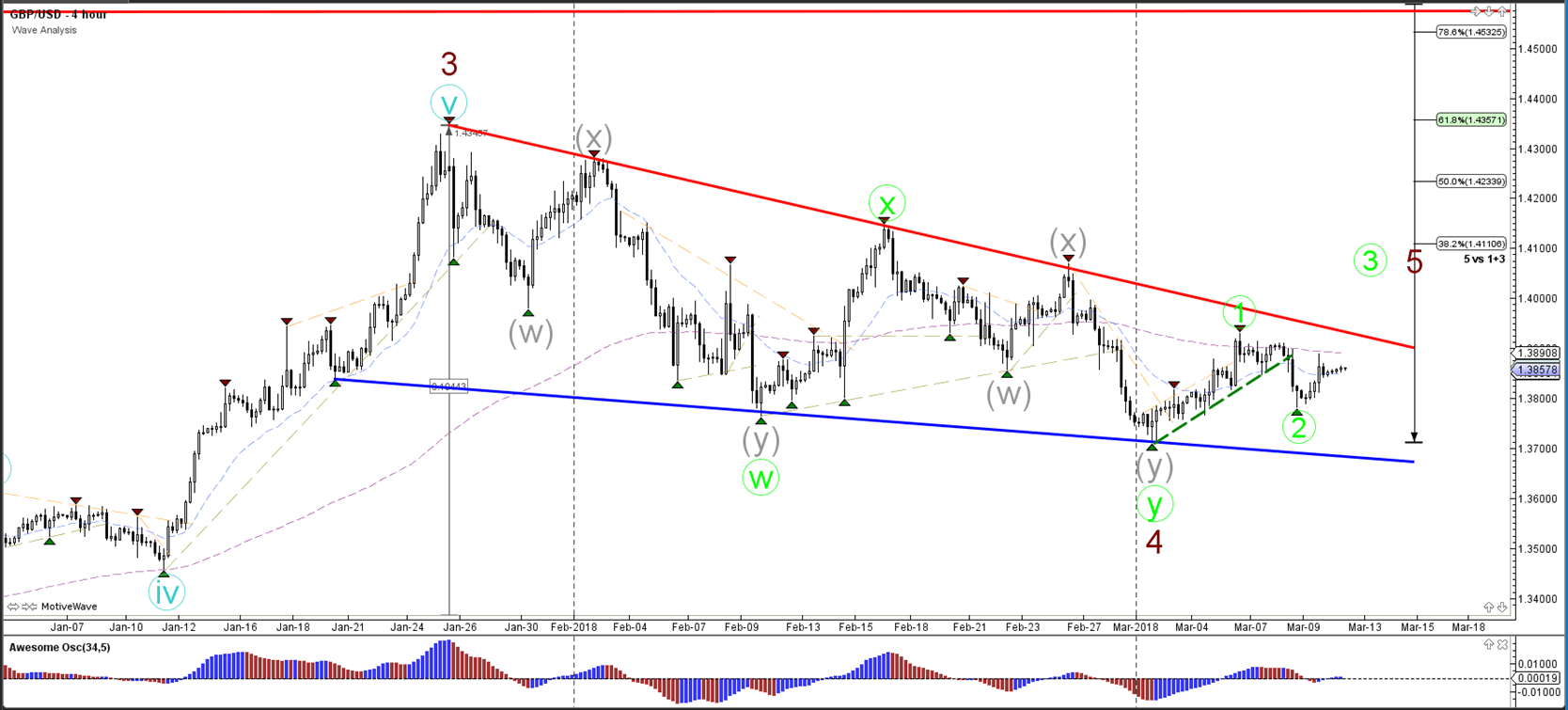

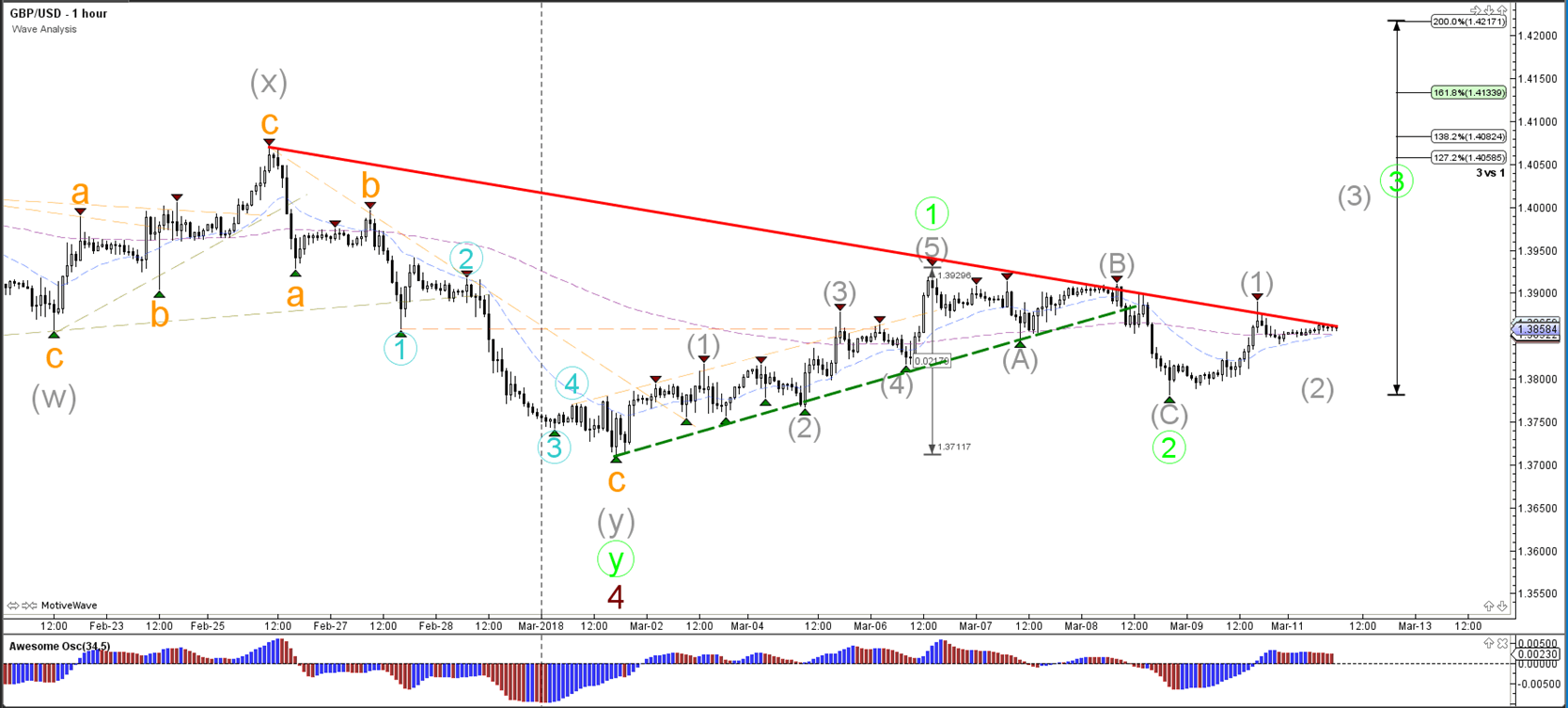

Daily Wave Analysis: EUR/USD, GBP/USD Complete ABC Zigzag Within Wave 2

Currency pair EUR/USD

The EUR/USD is staying in between support (green/blue) and resistance (red) levels, which is building a larger consolidation zone. The breakout above or below these S&R levels will determine the next direction and whether price will start an uptrend or downtrend.

The EUR/USD seems to have completed an ABC zigzag (blue) within wave 2 (purple). The wave 2 however could still be active if more ABC patterns occur. A break above resistance makes a wave 3 (purple) likely whereas a break below the 100% Fib invalidates wave 2.

Currency pair GBP/USD

The GBP/USD seems to be building a wave 1-2 (green)within wave 5 (brown) unless price breaks below the bottom of wave 4 (brown). A bullish break above resistance (red) could confirm wave 5 (brown).

The GBP/USD could have completed an ABC zigzag (grey) within wave 2 (green). A bullish breakout could confirm the potential waves 3.

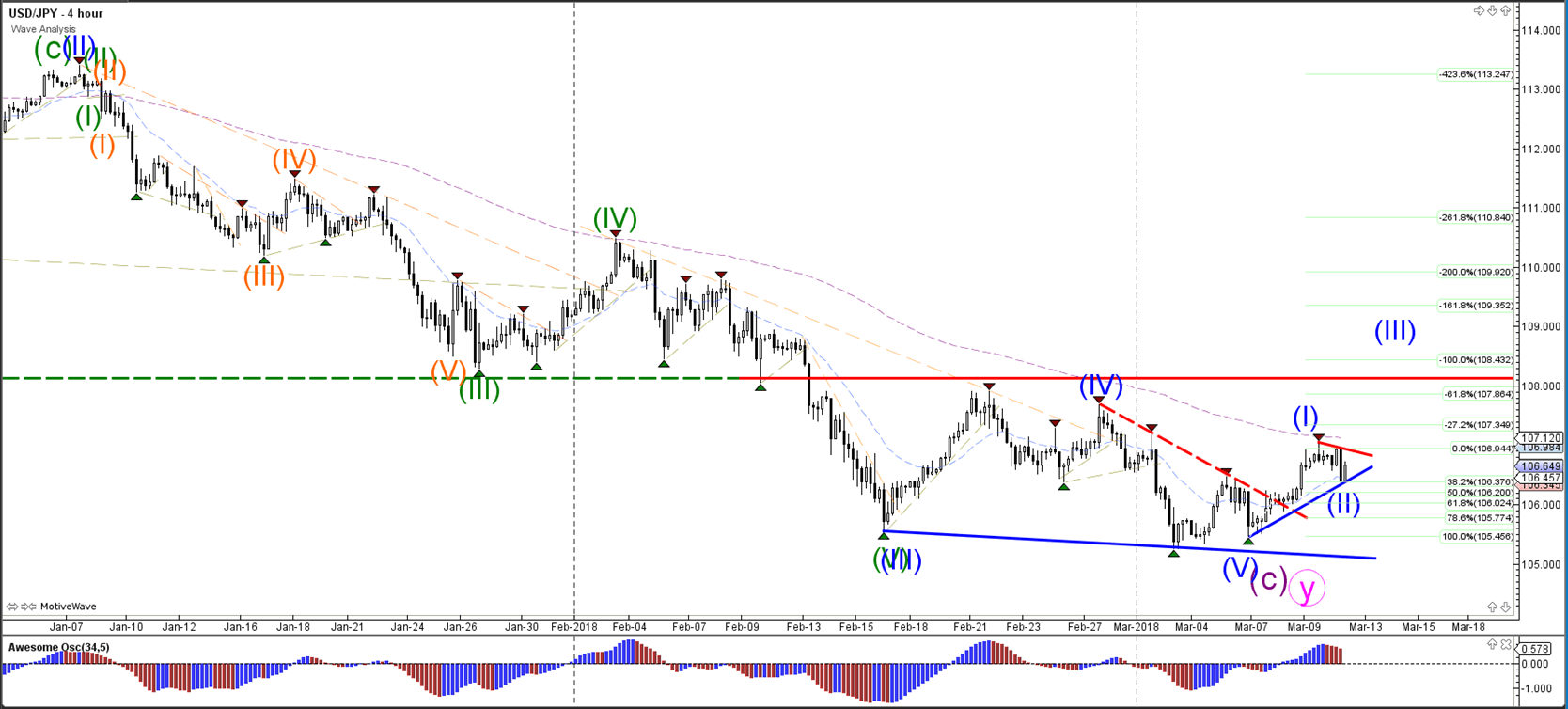

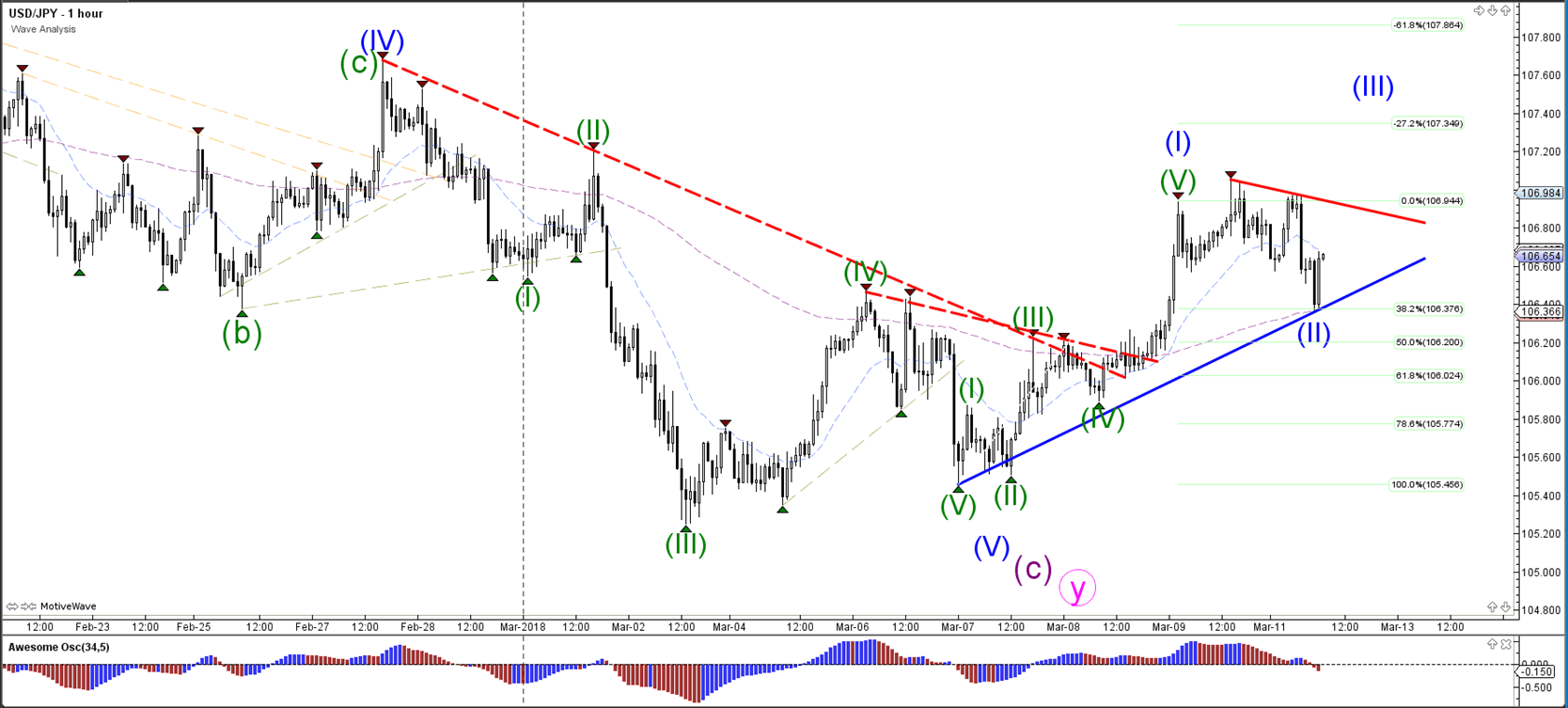

Currency pair USD/JPY

The USD/JPY could be building a bigger bullish breakout if it manages to push above the resistance trend lines (red).

The USD/JPY breakout seems to have completed wave 1 (blue) and the retracement could be part of wave 2 (blue). The alternative is that price is now completing a wave 4 (green) rather than a wave 2 (blue).

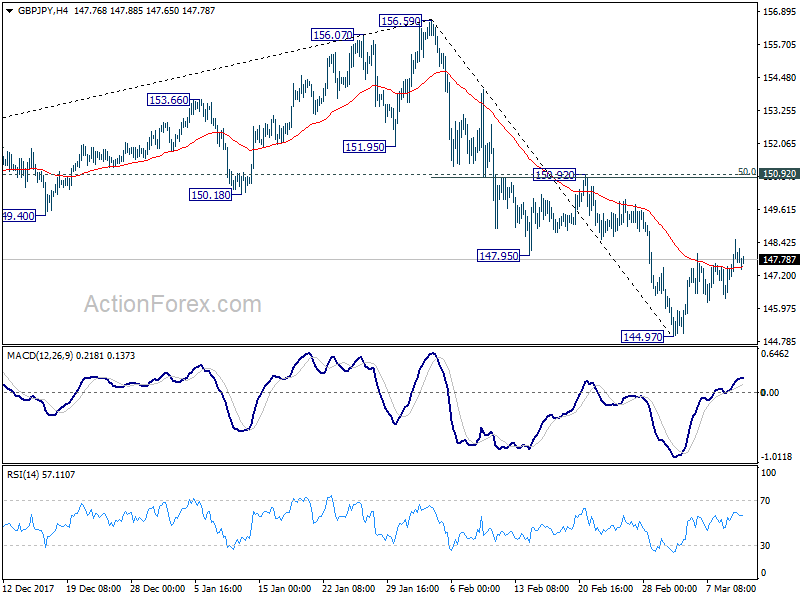

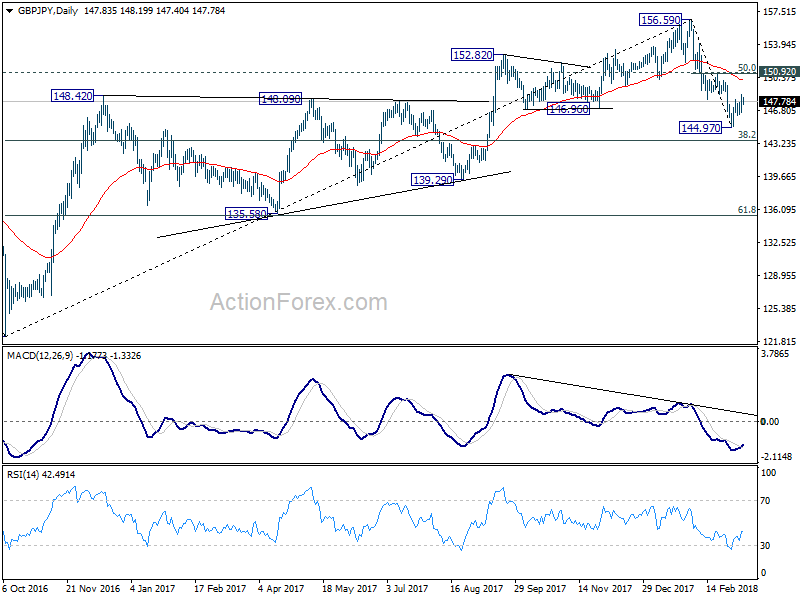

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.82; (P) 147.67; (R1) 148.75; More...

Intraday bias in GBP/JPY remains neutral as consolidation from 144.97 continues. In case of stronger rise, upside should be limited by 150.92 (50% retracement of 156.59 to 144.97 at 150.78 to bring fall resumption. Break of 144.97 will extend the decline from 156.59 to 143.51 medium term fibonacci level next.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

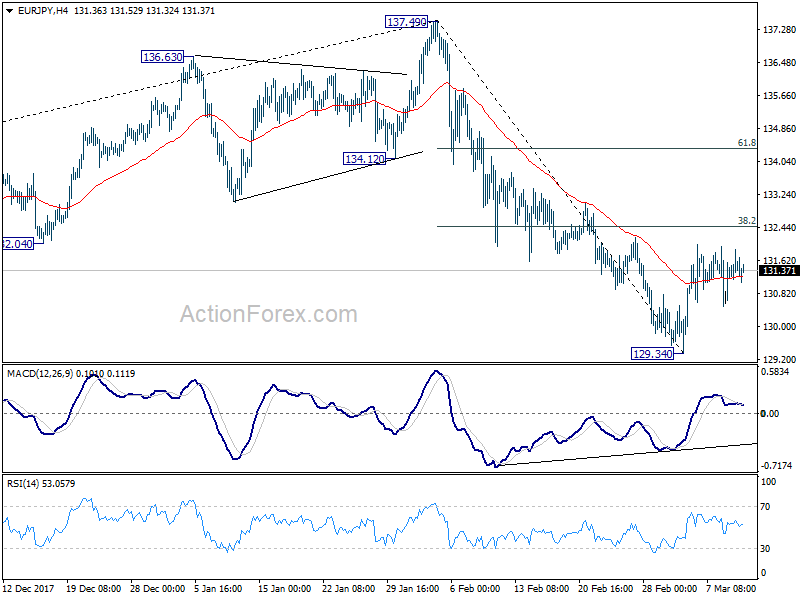

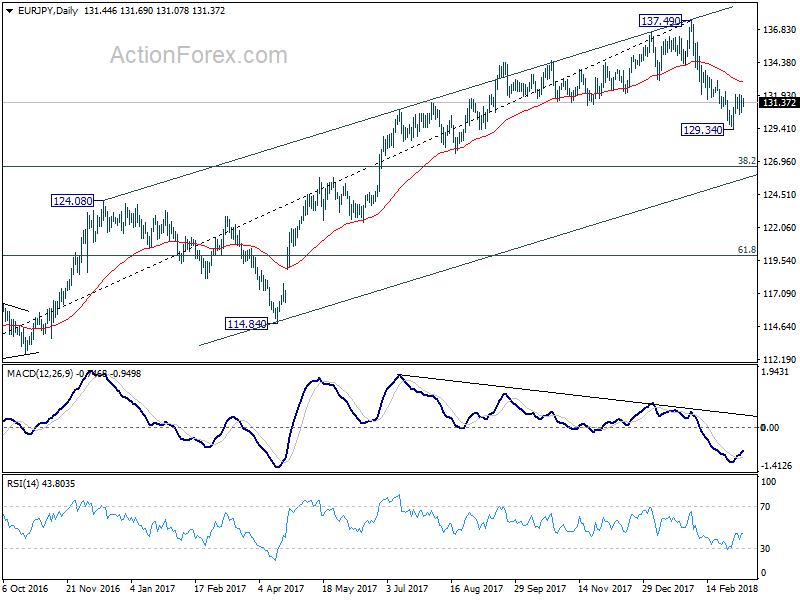

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.75; (P) 131.32; (R1) 131.97; More....

Intraday bias in EUR/JPY remains neutral at this point. Corrective rise from 129.34 might extend higher. But we'd be cautious on strong resistance from 38.2% retracement of 137.49 to 129.34 at 132.45 to limit upside. Break of 129.34 will resume the whole decline from 137.49 to 126.61 medium term fibonacci level. Nonetheless, sustained break of 132.45 will target 61.8% retracement at 134.37 first, before resuming the fall from 137.49.

In the bigger picture, current development argues that rise from 109.03 (2016 low) has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

Market Update – Asian Session: Equities Track Higher

Headlines/Economic Data

General Trend: Asian equities track Friday’s gains in US markets

Asian steelmakers trade generally higher

Australia’s Bluescope [BSL.AU] Steel gains over 3% on exemption from US tariffs

Commodity currencies gain after rise in equity markets

Shanghai Rebar Steel Futures extend losses amid US steel tariffs announcement

Japan

Nikkei 225 opened +1.7%; closed +1.7%

TOPIX Securities Index +1.8%, IRON & Steel +1.6%

Mega-banks track Friday’s gains in US financials

(JP) Japan Q1 BSI Large All Industry Q/Q: 3.3 v 6.2 prior; Large Manufacturing: 2.9 v 9.7 prior

(JP) Japan PM Abe and Finance Min Aso said to face pressure related to Moritomo Gakuen land transaction – financial press

(JP) Japan LDP Moriyama: Moritomo documents were altered. According to financial press that has seen Moritomo document, 14 places in the doc were altered. Japan PM Abe's name was removed, Fin Min Aso's wife's name was removed

(JP) Japan Fin Min Aso: confirms Moritomo documents were altered 14 times, apologizes; reiterates no intention to resign - speaking at press conf

(JP) JAPAN FEB PRELIMINARY MACHINE TOOL ORDERS Y/Y: 39.5% V 48.8% PRIOR

Korea

Kospi opened +1.1%

(KR) South Korea preparing to file WTO complaint against the US after request to withdraw its safeguard measures on Korean washers. This is amid intensifying tension over Trump’s decision to impose tariffs on imported steel products - Korean press

Kia Motors, 000270.KR South Korea tax offices has launched an investigation into the company - Korean press

(KR) South Korea to decided if it will join the CPTPP in the first half of this year - Korean press

(KR) Bank of Korea sells KRW800B in monetary stabilization bonds (MSBs): yield 1.96%

(KR) Bank of Korea (BOK) sells 3-month Monetary Stabilization Bonds (MSB); Yield 1.55% v 1.54% prior

China/Hong Kong

Hang Seng opened +1.7%, Shanghai Composite +0.4%

Hang Seng Energy Index +2.2%, Services +1.9%, Information Technology +1.8%, Financials +1.7% Materials +1.6%, Property/Construction +0.7%

Shanghai Composite Property index declines over 2%

(CN) China should prepare emergency plan for financial risks - China Daily

(CN) US government said to have asked China for a $100B plan to cut trade deficit - FT

(CN) China officially removed presidential term limits form the constitution on Sunday – press

(CN) China State Assets Supervision and Administration Commission (SASAC) chairman Yaqing: reducing debt and curbing risks remain priorities for China’s state owned enterprises (SOE), will continue with restructuring and deleveraging efforts - Chinese press

(CN) PBoC Gov Zhou: China has done most of what it takes to pave the way for expanded usage of yuan globally – Xinhua

(CN) China Foreign Min Wang: Time the China threat theory is permanently laid to rest; despite elements of competition China and US ties are defined more by partnership than rivalry – Xinua

(CN) PBOC sets yuan reference rate at 6.3333 v 6.3451 prior

(CN) China PBoC Open Market Operation (OMO): Injects CNY90B in 7 and 28-day reverse repos (first OMO in 6 sessions) :Net injection CNY90B v CNY40B drain prior

Prada [+19%], 1913.HK Reports FY17 Net €249.9M v €278.3M y/y, EBIT €360M v €431.2M y/y, Rev €3.01B v €3.18B y/y

Australia/New Zealand

ASX 200 opened +0.7%; closed +0.7%

ASX 200 Resources Index +1.7%, Financials +0.7%

Newcrest Mining, NCM.AU Reports limited breakthrough of tailings material was identified at Cadia northern tailings dam embankment; to adversely impact FY18 production

(AU) Australia PM Turnbull: Australia steel tariff exemptions from US a 'win-win'; will not take WTO complaint related to US tariffs

Woodside [+1.2%]; WPL.AU Enters into agreement with BHP on proposed development of Scarborough Gas Field; to offer 14.4M entitlements not taken up earlier

(NZ) New Zealand PM Ardern: Will seek exemption from US steel tariff

(NZ) New Zealand Debt Management Office: To offer NZ$1.5-2.0B in 3.0% April 2029 bond through syndication (on March 13th), pricing guidance is 16-19bps/April 2027 bond; cancels bond auction planned for March 15th

(NZ) RBNZ acting Gov Spencer to speak on Tuesday, March 13th; to focus on macro-prudential policy

North America

(US) Fed’s Bullard (dove, non-voter) reiterated 4 interest rate hikes in 2018 could slow the economy – FT

(US) White House: Refers issue of raising minimum age to buy rifles to 21 from 18 to commission led by Educational Sec Devos.

Broadcom [AVGO]: Reportedly Intel considering M&A, including possible bid for Broadcom - financial press

Europe

(UK) If there is a 'no-deal' Brexit, companies in the UK and EU could face £58B in extra annual costs - Report by Oliver Wyman and Clifford Chance

(IR) Iran Oil Minister Zanganeh said OPEC could agree in June to begin reducing oil output cuts in 2019 - US financial press

Deutsche Bank, DBK.DE Said to be planning to cut its retail unit by 20% over the next 4-yrs - German press

Innogy SE [IGY.DE]: RWE agreed in principle to sell 76.8% stake in co. to E.ON for total value of €40/share (~16% premium to prior close) in exchange for 16.67% stake in E.ON in addition to other business interests; E.ON to also receive €1.5B cash payment

(UK) Chancellor of Exchequer Hammond (Fin Min): to provide govt's half-yearly update of Britain's public finance figures on Tuesday, Mar 13th - financial press

Levels as of 02:00ET

Hang Seng +1.5%; Shanghai Composite +0.6%; Kospi +1.0%

Equity Futures: S&P500 +0.4%; Nasdaq100 +0.6%, Dax +0.6%; FTSE100 +0.1%

EUR 1.2325-1.2305; JPY 106.97-106.35; AUD 0.7873-0.7847;NZD 0.7323-0.7280

Apr Gold -0.1% at $1,323/oz; Apr Crude Oil +0.1% at $62.09/brl; May Copper -0.1% at $3.14/lb