Sample Category Title

Sunset Market Commentary

Markets

Core bonds traded with a tentatively negative bias this morning. The scheduled talks between the US and North Korea caused a positive risk momentum on Asian markets. The impact of the Trump import taxes was considered as modest as US allies including the EU and Japan advocated that their exports were no security issue for the US. Bond markets settled in some kind of wait-and-see modus, counting down to the US payrolls. US job growth was strong (313 k + an upward revision of the January figure). However, the data series that really matters from markets, the AHE wage growth series, printed at a disappointing 0.1% M/M and 2.6% Y/Y (from 2.9% Y/Y, 2.8% was expected). Core bonds spike briefly up and down looking for direction. Bond yields finally trended slightly higher. However, the moves remain very modest. The combination of good job growth and modest inflationary pressure propelled US equities. The US yield curve bear steepens with yields between 2.5 (2-y) and 4.4 (bp) higher at the time of writing. Increases in German Bund yields are more modest ranging between unchanged for the 2-year yield and +2.2 bp for the 10-y yield. Spreads of intra-EMU bonds versus German Bunds were little changed today.

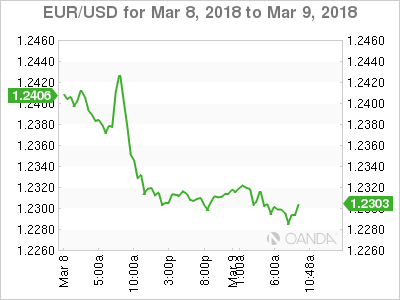

No big story to tell on USD trading today. EUR/USD preserved yesterday’s post-ECB decline, but there was little follow-through price action. Interest rate differentials widened a bit further in favour of the dollar, but didn’t help the US currency. This pattern didn’t change after the US payrolls. Job growth was very strong but wages again disappointed. This caused only a subdued market reaction both on interest rate markets and in the USD price action. EUR/USD filled bids in the 1.2275 area around the time of the publication of the payrolls, but the decline was blocked. The pair hovers again in the 1.23 area. USD/JPY tries to further extend intraday gains. The pair is additionally supported by a positive stock market reaction and soft BoJ talk. The pair tries to regain the 107 barrier, but it is a tough battle.

Sterling trading was again driven by technical considerations. UK data were mostly weaker than expected. The UK January trade deficit widened again on a monthly basis. Manufacturing production grew a meager 0.1% M/M and 2.7% Y/Y, below consensus. Construction output was also weaker than expected. Even so, sterling gained gradually further ground against the euro. Underlying euro softness after yesterday’s ECB press conference was maybe still at work. The rejected topside test of the EUR/GBP 0.8930/50 resistance was probably also in play. EUR/GBP is currently trading in the 0.8970 area. Cable is changing hands just in the 1.3850 area.

News Headlines

US job growth was very strong in February. The US economy added a stellar 313 000 jobs in February. The market only expected job growth of about 205 000. Data off the previous months were also upwardly revised. Still, the unemployment rate was unchanged at 4.1%. However, the most important part of the report for markets, wage growth, disappointed again. Average hourly earing rose only 0.1% M/M and 2.6% Y/Y. A rise of 0.2% M/M and 2.8% Y/Y was expected. So for now, there is no confirmation yet that a buoyant labour market is already resulting in a sustained acceleration of wages and prices as was suggested last month.

UK January activity disappointed again, suggesting a slow start for the UK economy in 2018. Manufacturing production rose a meagre 0.1% M/M and 2.7 % Y/Y (0.2% M/M was expected). Overall industrial production rebound 1.3%M/M and 1.6% Y/Y, reversing December decline due to the closure of the Forties pipeline. Still, overall production was below consensus. UK construction activity also tumbled 3.4% M/M to be 3.9% lower compared to the same month last year. The UK goods trade deficit widened again to 12.325 bln from 11.771 bln in December.

DOW breaks 25000, Dolllar weak after wage disappointment

DOW opens with triple digital gains and is trading above 25000 handle. This represents prior resistance at 24995.24, and 50% retracement of 25800.35 to 24217.47 at 25008.91. Rebounds from 2418.47 has resumed and should now target 61.8% retracement at 25195.68 and above.

But, for the moment, rise from 24217.47 doesn't have impulsive look. So, it will likely start to feel heavy above 25195.69.  In FX, after wage growth disappointment, Dollar is in red for today except versus Yen and Euro. Aussie and Kiwi are the strongest ones, followed by Sterling and then CAD.

In FX, after wage growth disappointment, Dollar is in red for today except versus Yen and Euro. Aussie and Kiwi are the strongest ones, followed by Sterling and then CAD.

Jobs, Wages, Labor Force Growth: Fed on Path to Raise Rates

Another month of job and wage gains support the case for better growth (2.5-3.0 percent) for 2018 and continued consumer spending. The long view remains for job gains to outpace labor force growth.

February Jobs at 313,000: Solid Sign for Income and Growth

Nonfarm payrolls rose 313,000 in February with the three-month average at a solid 242,000 jobs. Job gains are consistent with 2.5-3.0 percent economic growth in the first half of 2018, with steady consumer spending, better business investment and a likely FOMC March rate hike, soon followed by another one in June.

Jobs gains appeared in many sectors including business services, trade & transportation as well as education & health (top graph). Only information services jobs have declined in each of the past three months due to drops in jobs in telecommunications and motion pictures. Over the past three months, aggregate hours worked are up 3.1 percent – very solid and consistent with continued growth in personal income and consumption.

Inflation Leads Wages—Not Wages Lead Inflation

Contrary to the casual rhetoric, Granger causality tests reveal that inflation leads wages—not vice versa. This statistical result follows the theoretical model that workers and employers respond to higher inflation. Workers respond to inflation by trying to negotiate higher nominal wages to maintain a real wage standard. Employers find that higher inflation gives them the flexibility to raise wages and maintain profit margins.

Nominal average hourly earnings rose 0.15 percent in February and are up 2.6 percent over the year—slower than the January pace. While job growth remains strong, the gradual rise in earnings over the past six months signals higher incomes but also pressure on profits as firms have modest top-line pricing power. Longer term, subdued inflation readings and weak productivity numbers suggest limited gains in nominal wage growth.

The Long Game

Despite a strong labor force participation number in today's report, the overall trend for labor force growth has slowed more recently, compared to 2014-2016 rates. In February, the labor force jumped 0.5 percent, month over month, but is up just 1.2 percent over the past year. The trend slowdown reflects the ongoing demographic shifts that run quietly in the background of the month to month changes in the labor market. Growth in the working age population (ages 16+) has slowed to 0.6 percent per year, less than half the pace registered in the 2000s. Excluding workers over the age of 65, population growth has stalled over the past year.

Rising labor force participation among prime-age workers has offered some support, but the participation rate for workers 25-54 remains more than a point and a half below its pre-recession level and almost two and a half points below the high set in 1999. Unless participation rates continue to rise as solidly as this month, we expect payroll growth to slow and the unemployment rate to decline over the course of the year as businesses have increasing difficulty finding workers.

US: The Hits Just Keep On Coming!

U.S. payrolls surged ahead in February, up 313k against expectations for a 200k increase. Gains were largely in the private-sector hiring (+287k), and upward revisions to the prior two months added another 54k jobs.

The unemployment rate remained unchanged at 4.1% as increased numbers of new workers entered the labor force. The labor force participation rate rose to 63.0% in February, re-attaining it's post-recession peak. Overall participation in the labor force has been fairly steady since early 2016, but that hides an encouraging upward trend for core-age workers (25-54 yrs.), which is being offset by the large cohort of baby boomers entering retirement.

All eyes were on wage growth, which rose a moderate 0.2% m/m in February. That left average hourly earnings up 2.6%, a slight deceleration from 2.8% in January. Still, wages have advanced at a 3% annualized pace over the past three months.

Payroll gains were broad based, with hiring in both good and services sector accelerating. In the lead were construction (+61k), retail trade (+50k), professional and business services (+50k), manufacturing (+31k), financial activities (+28k) mining(+9k) and health care (+19k).

Key Implications

The job market has certainly got off to a roaring start in 2018. Hiring has picked up in recent months, driven by an acceleration in goods sector hiring, and the mining and manufacturing sectors in particular. Still, the unemployment rate has remained steady at 4.1%, as growth in the labor force has also gained speed.

While some might be a bit disappointed in the step back in wage growth, the trend over the past few months has been positive. And, with hiring growth like this, wage pressures are bound to accelerate further over the coming months, which should continue to draw people off the sidelines and into the workforce. On top of tax cuts, recently announced government spending increases will add further fuel to this fiery labor market.

There is little debate that the Fed will hike in March. Our latest forecast calls for three hikes in total over 2018, but if this momentum continues, there is certainly an upside risk to this view.

Modest Canadian Employment Gains in February

February saw the Canadian economy add 15.4k jobs on net, only slightly offsetting January's 88k loss. The participation was effectively unchanged, resulting in a drop in the unemployment rate to 5.8%.

In another reversal from January, it was part-time jobs that drove the gains, up 54.7k (January: -137k). Full-time employment declined 39.3k net positions, ending a five month streak of net job additions.

The bulk of the gains were seen in the public sector (+50.3k), while the private sector added 8.4k net jobs. Holding back the overall pace of gains was a decline in self-employment, down 43.3k in February after four months of net increases.

By industry, net job additions came from the service-producing sectors (+25.9k), with notable increases in health care (+24.5), other services (+16.6k), and transportation (-12.6k). Trade stood out on the negative side, shedding 22k net positions. Goods-producing industries subtracted 10.4k from the total, led by a 16.5k net decline in manufacturing employment.

On a regional basis, Ontario led the way, adding 15.7k net positions – not enough to offset January's 50.9k net loss. Performances were mixed across the remaining provinces. Of note, Alberta's unemployment rate fell to 6.7%, a 1.5 percentage point decline relative to its year-ago level, as the provincial participation rate fell slightly in February.

Wages decelerated a tick in February, to 3.1% year-on-year (from 3.3% in January). Despite part-time work driving the net job gains, aggregate hours worked were up 3.2% year-on-year, supported by a month-on-month gain of 0.6%.

Key Implications

Canada's monthly jobs market roulette wheel landed on 15.4k this month, a positive development but not enough to reverse January's losses. Beneath the headline were relatively encouraging details. Part-time employment may have led the gains as full-time pulled back, but gains in employees led the way as self-employment declined. What's more, hours worked gained nicely in February, and wage growth remained above 3%. With a tight labour market, headline job gains are likely to trend around or slightly below February's pace going forward – what will matter more are these underlying details.

With the monthly variation a casino game, yearly changes matter: Overall employment was up 282.5k on net relative to last February, entirely due to full-time job gains. To be sure, the pace of yearly gains is moderating (having peaked at 427k in December), but this is to be expect given that economic and labour market slack has largely been absorbed.

At a 3.1% pace in February, wage growth marked a fourth straight month above its longer-term average of 2.6%. This would normally be suggestive of a tight labour market. However, as expressed earlier this week, the Bank of Canada still sees wage growth as being below what they would expect in an economy without any labour market slack (at least up to this point: this was the second month of >3% wage gains, while the national accounts data reported a 4.9% y/y gain in 2017Q4). It thus seems that the Bank of Canada has set the wage gains of 2007/2008 as their guideline (wage growth at the time exceeded 4%, or more than 7% in national accounts measures). This suggests that today's solid wage numbers, while welcome, are unlikely to change the Bank's cautious stance.

Fed Evans prefers to wait “a little bit longer” before rate hike

Chicago Fed Charles Evans:

- Still concerned with low inflation

- "My own preference would be to wait a little bit longer, let the March anomalous inflation rate from a year ago fall out."

- "Let's make sure these sort of Amazon, disruptive kind of pricing models aren't continuing to find their way into keeping inflation lower than that."

- When inflation starts to show sign of heading to 2% target, he would be "much more confident" to continue "a gradual upward adjustment of the funds rate."

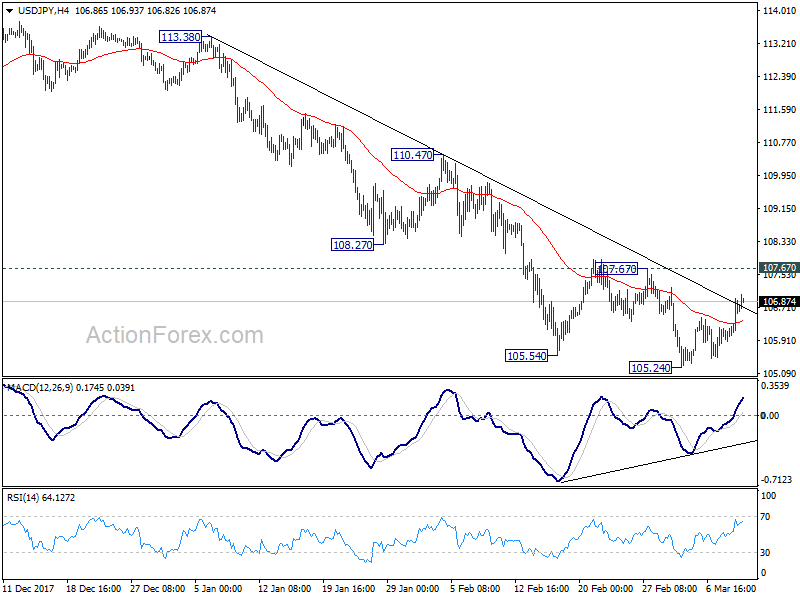

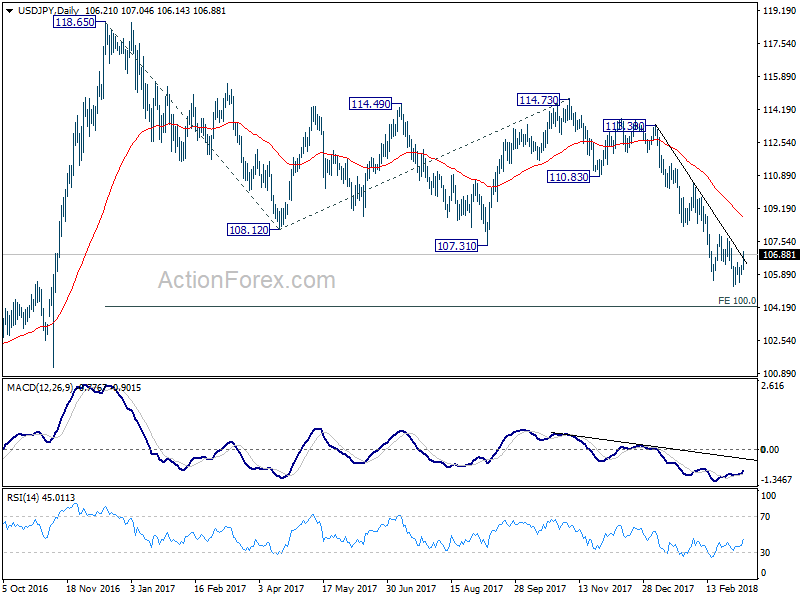

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.95; (P) 106.13; (R1) 106.37; More...

USD/JPY strengthens mildly today but stays well below 107.67 near term resistance. Intraday bias remains neutral first. Considering bullish convergence condition in 4 hour MACD, decisive break 107/67 will indicate near term reversal. In such case, outlook will be turned bullish for 110.47 resistance next. But before that, another decline is still mildly in favor. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

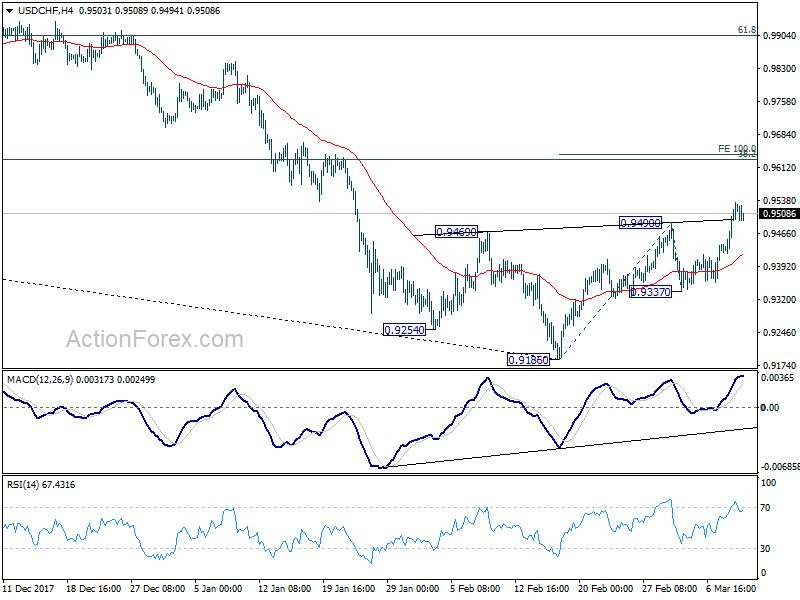

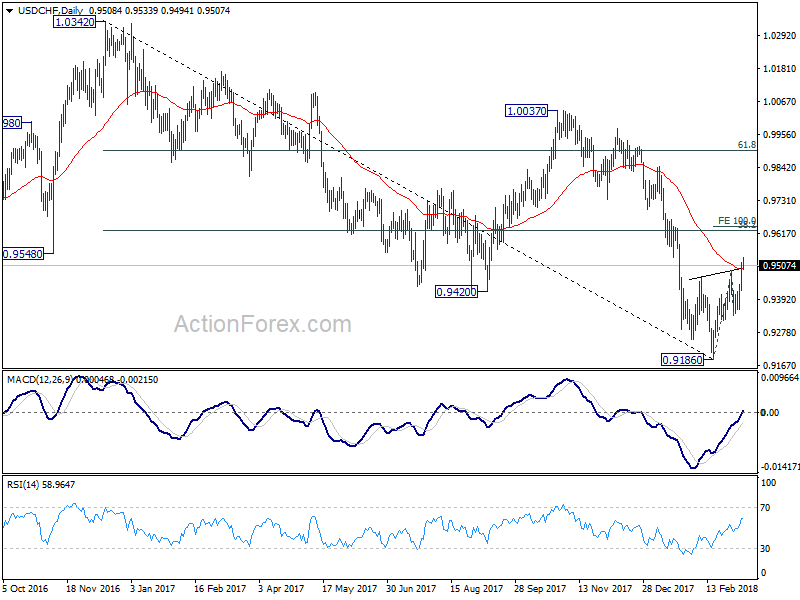

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9448; (P) 0.9484; (R1) 0.9546; More...

No change in USD/CHF's outlook. Intraday bias stays on the upside for further rally. As noted before, prior break of 0.9490 resistance indicates near term reversal. This is supported by bullish convergence condition in 4 hour MACD. Also, there is a head and shoulder bottom pattern (ls: 0.9254, h: 0.9186, rs: 0.9337). USD/CHF should target 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9641 first. On the downside, break of 0.9337 minor support is needed to indicate completion of the rebound. Otherwise, near term outlook will be cautiously bullish even in case of retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

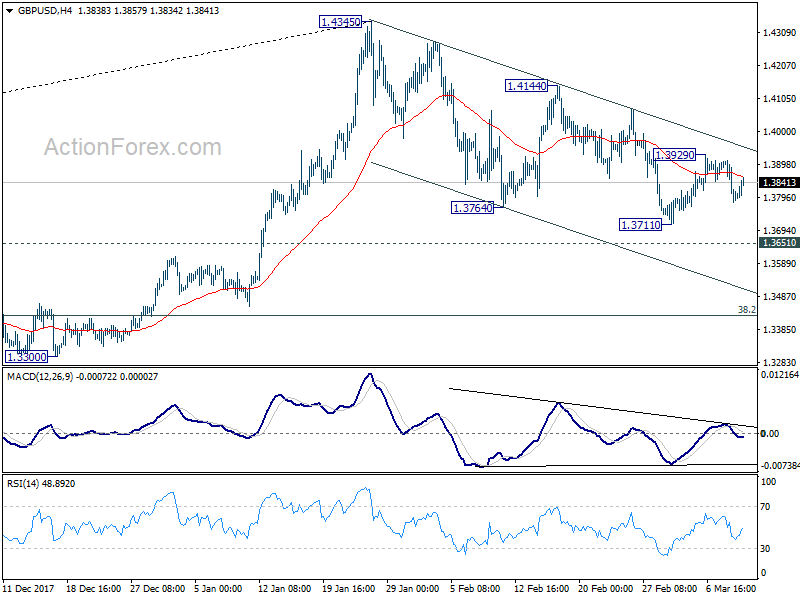

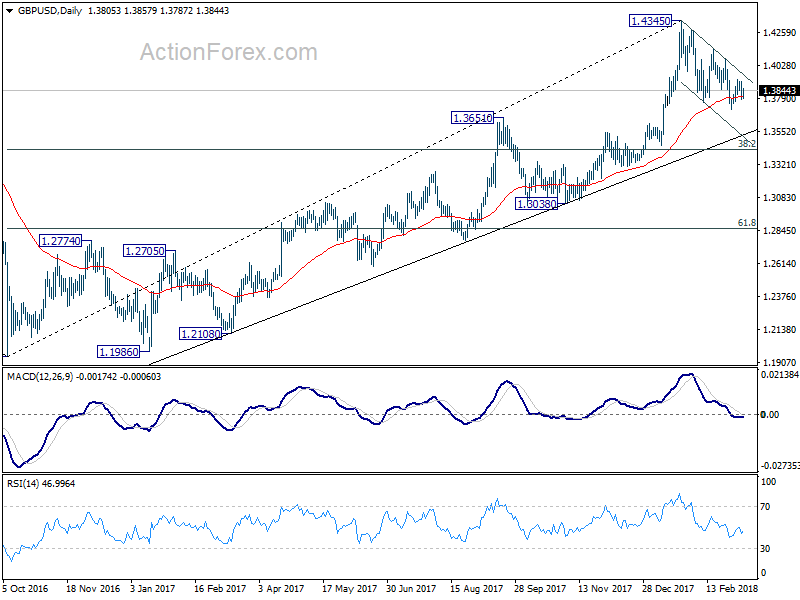

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3757; (P) 1.3833; (R1) 1.3888; More....

GBP/USD recovers today as sideway trading between 1.3711/3929 continues. Intraday bias remains neutral first. Fall from 1.4345 is in favor to extend and break of 1.3711 will target 1.3651 resistance turned support and below. At this point, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound. This will be the favored case as long as 1.3929 holds.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

U.S and Canada Payrolls Strong

Non-farm payroll (NFP)

U.S payrolls rose a seasonally adjusted +313k last month, while the unemployment rate held steady atop of its five month consecutive low of +4.1%.

Note: Market expectations were looking for a +205k headline print and a +4% unemployment rate.

Digging deeper, construction firms’ added +61k, the biggest increase in nearly 11 years for the sector. Hiring also picked up at retailers, manufacturers and local governments, including schools.

The share of Americans participating in the labor force rose by +0.3% to +63.0% m/m.

Revised figures show employers added +239k jobs in January and +175k in December, a net upward revision of +54k.

A tad disappointing were wages – average hourly earnings increased +4c to $26.75. Wages rose +2.6% from a year earlier in February. The annual wage gain in January was revised down to +2.8% increase.

Canada Jobs

Canada Jobs

Canada added a net +15.4k jobs in February on a seasonally adjusted basis, following a net loss of -88k in January. Market expectations were looking for a net gain of +21k. The unemployment rate fell to +5.8% m/m from January’s +5.9%.

Average hourly wages also advanced at a +3% y/y for the second consecutive month.

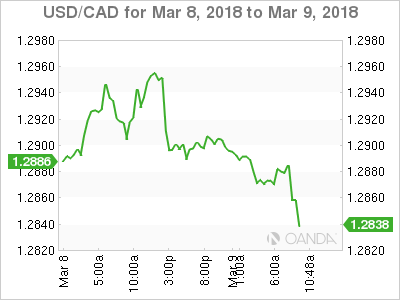

The loonie is off its highs but still up +0.22% at C$1.2866.