Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2257; (P) 1.2351 (R1) 1.2406; More....

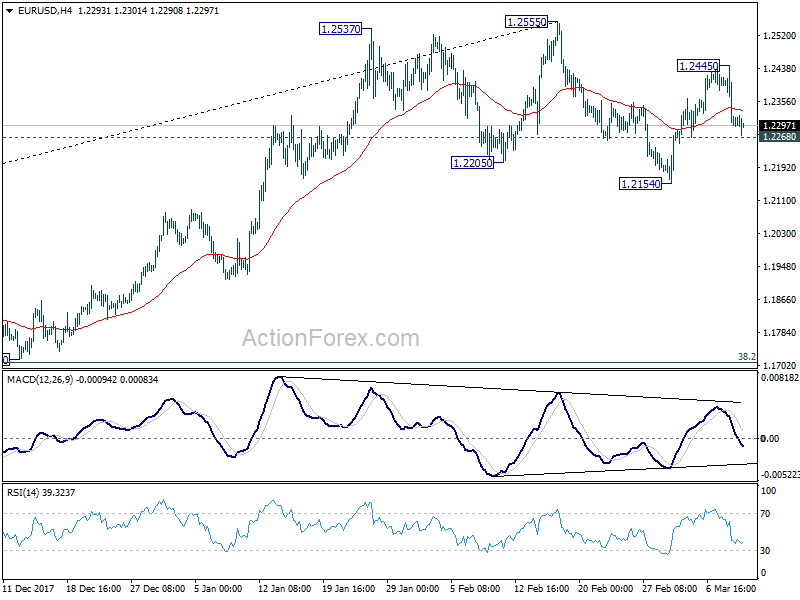

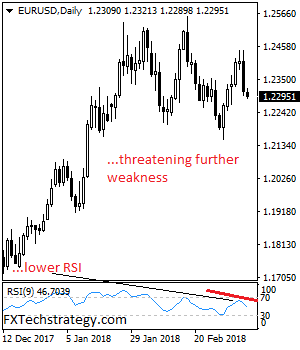

EUR/USD dips in early US session but is still staying above 1.2268 minor support. Intraday bias remains neutral at this point. On the downside, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below. Om the upside, above 1.24455 will turn bias to the upside for retesting 1.2555 key resistance.

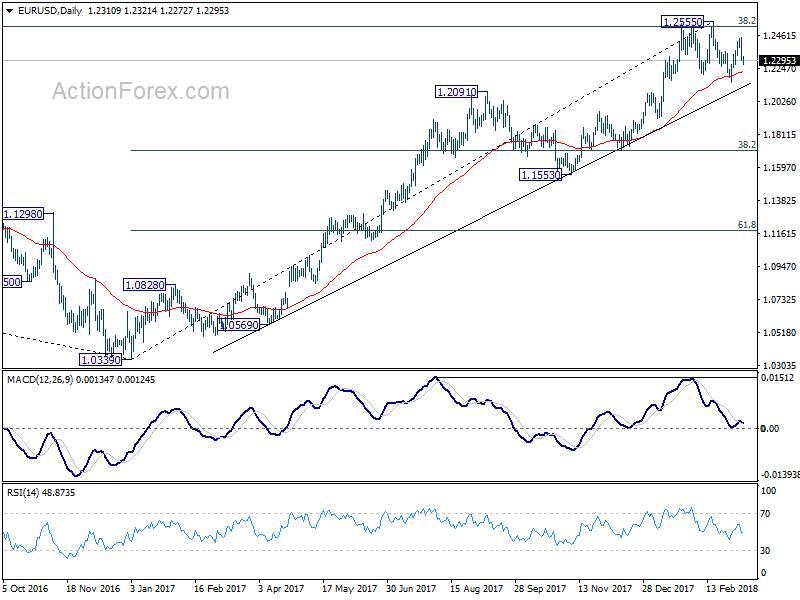

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Fails to Ride on Stellar 313k NFP Growth, Sluggish Wage Drags

Despite stellar report of job growth, Dollar fails to secure upside momentum so far due to sluggish wage growth. Non-farm payrolls report showed 313k growth in February, much better than expectation of 205k. Prior month's figure was also revised up from 200k to 239k. Unemployment rate was unchanged at 4.1%, above expectation 4.0%. Most disappointingly, average hourly earnings rose 0.1% mom only, below expectation of 0.2% mom, slowed from prior months 0.3% mom. The set of data is a repeat of the mystery that many Fed officials have pointed out. That is, strong job growth exists without wage pressure. The report does nothing to secure the chance of a fourth hike by Fed this year.

Released from Canada, the economy added 15.4k jobs in February, below expectation of 21.0k. But unemployment rate dropped to 5.8%, versus expectation of 5.9%.

DOW to take on 25000 again on improved sentiments

There were talks that market sentiments were boosted by breakthrough in tension between the US and North Korea. Politically, the agreement on meeting between US President Donald Trump and North Korean leader Kim Jong-un is welcomed globally. But Nikkei gained a mere 0.47% today. European index are mixed with FTSE trading up 0.25%, DAX Up 0.15% and CAC up 0.42% at the time of writing. Nonetheless, US futures point to higher open and DOW might have another go at 25000 handle.

NAFTA collapse could cost Canada 0.5% reduction in growth in first year

The Conference Board of Canada warned that failure to resolve the difference with the US and ending NAFTA could cost -0.5% reduction in real GDP growth in the first year. And that's even taken a lower exchange rate and easing in monetary policy into consideration. The Canadian economy could also lose as many as 85k jobs the first year.

In case of a NAFTA collapse, Conference Board predicts CAD 3.3b drop in real business spending in the first year. Real exports and imports will decline by -1.8%. Tariffs are predicted to revert to WTO most-favored nation rates. That is, Canadian exports to US would face 2.0% tariff. US exports to Canada would face 2.1% tariff.

Little reaction to European economic data

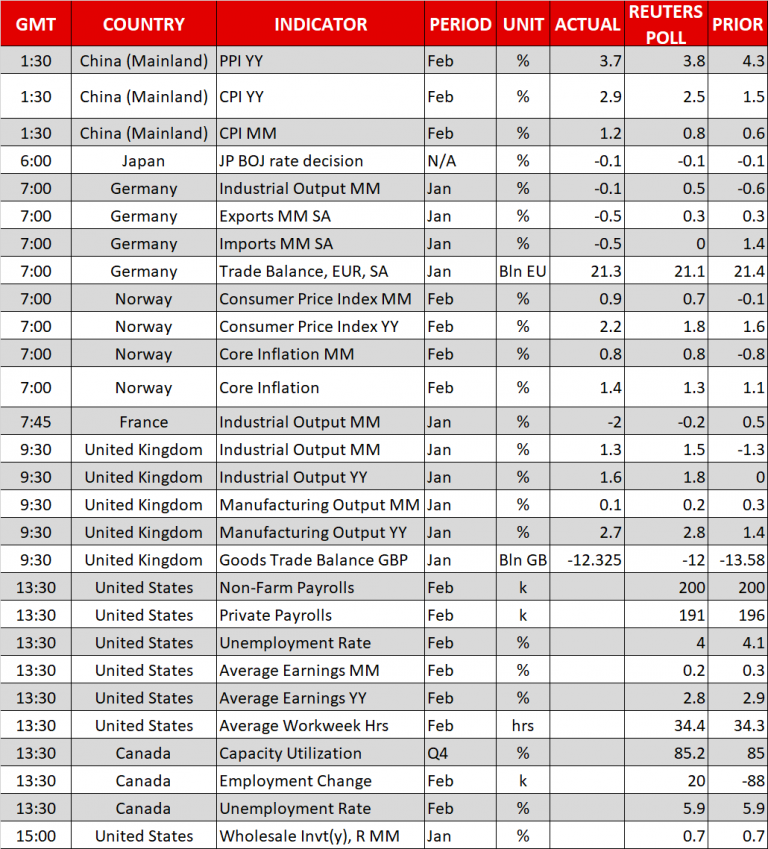

Markets have little reaction to economic data released in the European session. Released in European session, UK trade deficit narrowed to GBP -12.3b in January, slightly larger than expectation of GBP -12.0b. UK industrial production rose 1.3% mom, 1.6% yoy, vs expectation of 1.5% mom, 1.8% yoy. Manufacturing production rose 0.1% mom, 2.7% yoy, versus expectation of 0.2% mom, 2.8% yoy. UK construction output dropped -3.4% mom in January versus expectation of -0.5% mom. NIESR GDP estimate rose 0.3% in February versus expectation of 0.4%. German trade surplus narrowed slightly to EUR 21.3b in January. German industrial production dropped -0.1% mom in January.

BoJ stands pat. Moderate economic expansion to continue

BoJ left monetary policy unchanged today as widely expected. Short term policy rate is kept at -0.1%. BoJ will continue to purchase assets at a pace of JPY 80T per annum to keep 10 year JGB yields at around 0%. Goushi Kataoka dissented again, continued his push to lower yields on JGBs with maturities longer than 10 years. In the statement, BoJ noted that the economy is "expanding moderately, with a virtuous cycle from income to spending operating". And it expects such "moderate expansion" to continue. Core CPI is expected to "continue on an uptrend and increase toward 2percent". Risks to the outlook include US policies, outcome and Brexit negotiation and geopolitical risks. BoJ maintained the pledge on "continuing expanding the monetary base." until core CPI exceeds 2% and stays above in a "stable manner.

Japan household spending rose 2.0% yoy in January versus expectation of -0.8% yoy. M2 rose 3.3% yoy in February. Labor cash earnings rose 0.7% yoy versus expectation of 0.6% yoy.

From China, CPI jumped sharply to 2.9% yoy in February, up from 1.5% yoy and beat expectation of 2.4% yoy. PPI slowed to 3.7% yoy, down from 4.3% yoy and below expectation of 3.8% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2257; (P) 1.2351 (R1) 1.2406; More....

EUR/USD dips in early US session but is still staying above 1.2268 minor support. Intraday bias remains neutral at this point. On the downside, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below. Om the upside, above 1.24455 will turn bias to the upside for retesting 1.2555 key resistance.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BOJ Monetary Policy Statement | |||||

| 23:30 | JPY | Overall Household Spending Y/Y Jan | 2.00% | -0.80% | -0.10% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Feb | 3.30% | 3.30% | 3.40% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Jan | 0.70% | 0.60% | 0.70% | |

| 01:30 | CNY | CPI Y/Y Feb | 2.90% | 2.40% | 1.50% | |

| 01:30 | CNY | PPI Y/Y Feb | 3.70% | 3.80% | 4.30% | |

| 07:00 | EUR | German Trade Balance Jan | 21.3B | 21.1B | 21.4B | |

| 07:00 | EUR | German Industrial Production M/M Jan | -0.10% | 0.60% | -0.60% | |

| 09:30 | GBP | Visible Trade Balance (GBP) Jan | -12.3B | -12.0B | -13.6B | |

| 09:30 | GBP | Industrial Production M/M Jan | 1.30% | 1.50% | -1.30% | |

| 09:30 | GBP | Industrial Production Y/Y Jan | 1.60% | 1.80% | 0.00% | |

| 09:30 | GBP | Manufacturing Production M/M Jan | 0.10% | 0.20% | 0.30% | |

| 09:30 | GBP | Manufacturing Production Y/Y Jan | 2.70% | 2.80% | 1.40% | |

| 09:30 | GBP | Construction Output M/M Jan | -3.40% | -0.50% | 1.60% | |

| 12:00 | GBP | NIESR GDP Estimate Feb | 0.30% | 0.40% | 0.50% | 0.40% |

| 13:30 | CAD | Net Change in Employment Feb | 15.4K | 21.0K | -88.0K | |

| 13:30 | CAD | Unemployment Rate Feb | 5.80% | 5.90% | 5.90% | |

| 13:30 | USD | Change in Non-farm Payrolls Feb | 313K | 205K | 200K | 239K |

| 13:30 | USD | Unemployment Rate Feb | 4.10% | 4.00% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.10% | 0.20% | 0.30% | |

| 15:00 | USD | Wholesale Inventories M/M (JAN F) | 0.70% | 0.70% |

NAFTA collapse could cost Canada 0.5% reduction in growth in first year

The Conference Board of Canada warned that failure to resolve the difference with the US and ending NAFTA could cost -0.5% reduction in real GDP growth in the first year. And that's even taken a lower exchange rate and easing in monetary policy into consideration. The Canadian economy could also lose as many as 85k jobs the first year.

In case of a NAFTA collapse, Conference Board predicts CAD 3.3b drop in real business spending in the first year. Real exports and imports will decline by -1.8%. Tariffs are predicted to revert to WTO most-favored nation rates. That is, Canadian exports to US would face 2.0% tariff. US exports to Canada would face 2.1% tariff.

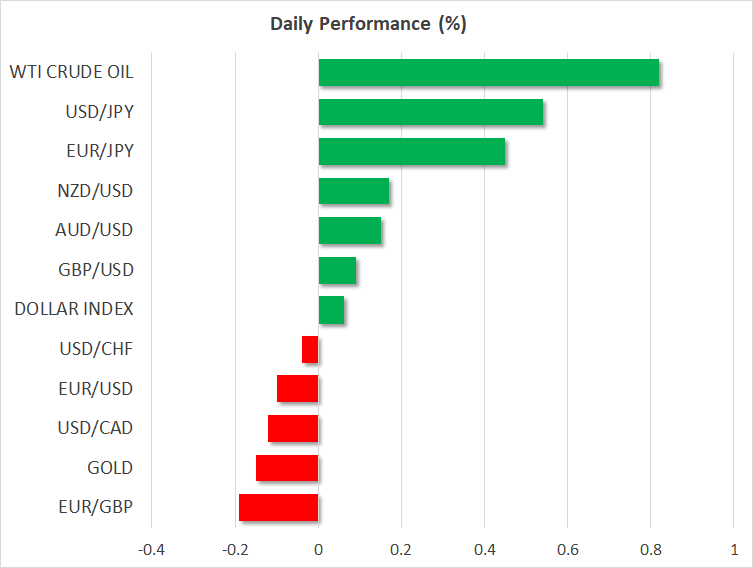

Dollar spikes higher on stellar 313k NFP, back down on sluggish wage growth

Dollar spikes higher after stellar 313k NFP growth in Feb. But traders quickly realize that wage growth disappoints. Dollar then reverses the gains. On the other hand, strong buying is seen in CAD as unemployment rate unexpectedly fell.

US job data:-

- NFP Feb: 313k vs exp 205k vs prior 239k (revised up from 200k)

- Unemployment rate Feb: 4.1% vs exp 4.0% vs prior 4.1%

- Average hourly earnings Feb: 0.1% mom vs exp 0.2% mom vs prior 0.3% mom

Canada job data:-

- Employment change: 15.4k vs exp 21.0k vs prior -88.0k

- Unemployment rate Feb: 5.9% vs exp 5.9% vs prior 5.9%

Canadian Dollar Ticks Higher, Key Job Reports Loom

USD/CAD is showing slight losses in the Friday session. In the North American session, USD/CAD is trading at 1.2878, down 0.15% on the day. On Friday, employment data will be in focus on both sides of the border. Canada releases employment change, and the US publishes wage growth and nonfarm payrolls.

Is President Trump baiting his trading partners into an all-out global trade war? After declaring that trade wars are a “good thing”, Trump made good on his tariff threat on Thursday, and signed an order imposing 25% tariffs on steel imports. Canada is the largest exporter of steel to the US, accounting for some 16% of US steel imports. The move could have severely impacted on the Canadian steel industry, but Trump has exempted Canada and Mexico from the tariffs, at least temporarily, drawing a huge sigh of relief from Ottawa. Still fears of an all-out global trade war remain a serious concern for Canada and the resignation of Gary Cohn, a senior economist in the White House who opposed the tariffs, will only dampen investor risk appetite.

The Federal Reserve is widely expected to raise rate four times in 2018, but the Bank of Canada will likely be unable to compete with that kind of pace. The BoC is concerned with economic growth, which slowed in the fourth quarter, as well as uncertainty over NAFTA, which could fall apart if the Trump administration makes good on its threat to withdraw if its demands for more favorable treatment for US goods is not met. The Bank is not expected to raise rates before May, and if the Fed outpaces the BoC on the rate front, the Canadian dollar could lose ground to a more attractive US currency.

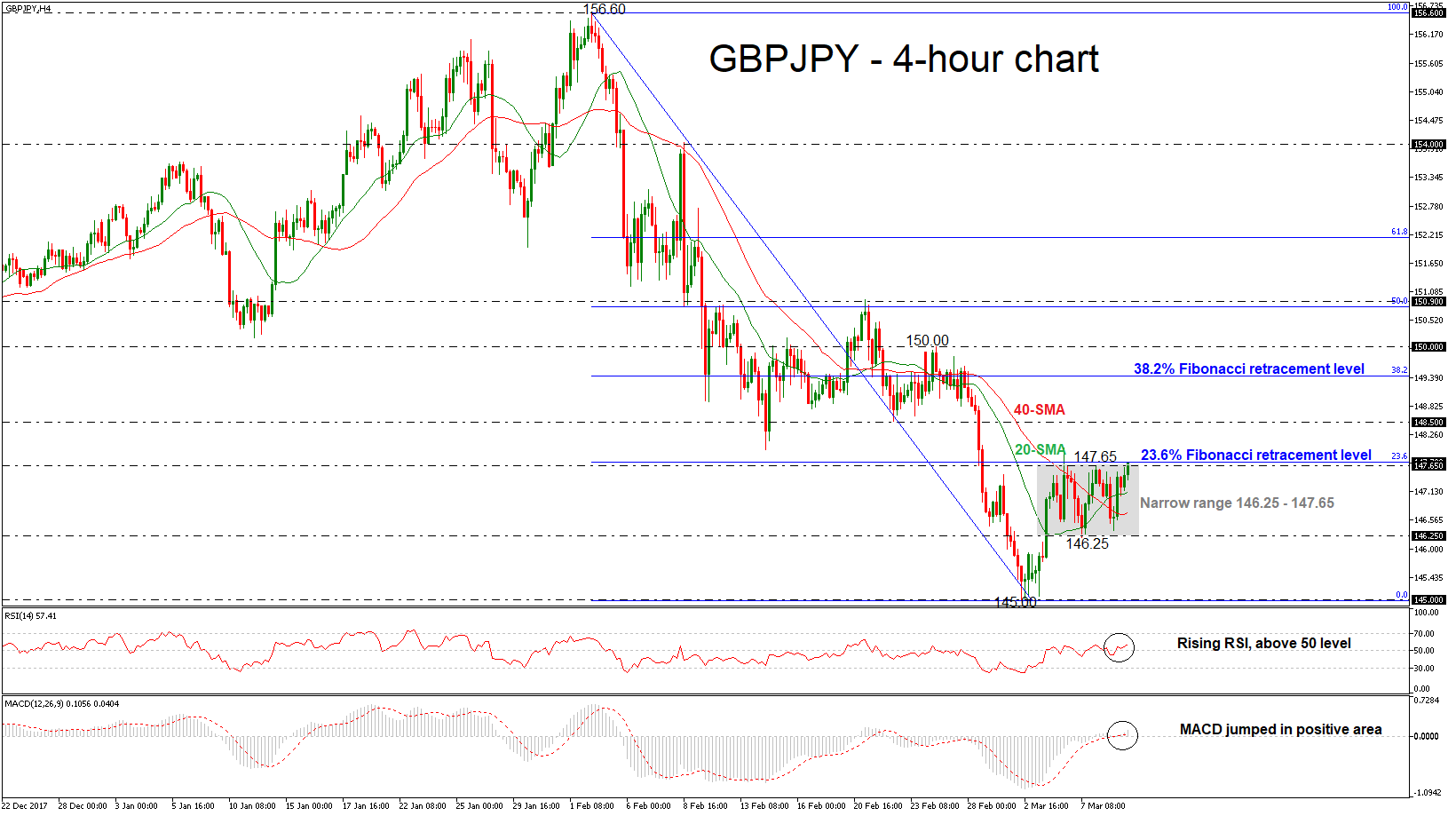

GBPJPY Trades in Narrow Range; Bullish Move is Expected Yntil 148.50

GBPJPY is creating a bullish recovery over the last sessions after it hit a 6-month low near the 145.00 psychological level. The prices jumped above the 20 and 40 simple moving averages in the 4-hour chart and are standing below the 148.00 handle. As a side note, the pair has been holding within a narrow range of 146.25 – 147.65 since March 5 and is trying to jump above this area at the time of writing.

From the technical point of view, the market could increase positive momentum in short-term. The Relative Strength Index (RSI) is sloping up in the bullish territory, while the MACD oscillator entered the positive zone and climbed above its trigger line.

If price action remains positive and rises above the 23.6% Fibonacci retracement level near 147.65 of the downleg from 156.60 to 145.00, the next major resistance to watch is the 148.50 barrier. Further gains could push GBPJPY towards the 38.2% Fibonacci level of 149.40.

Conversely, if the price creates a bearish movement again, then the focus could shift to the downside until the lower boundary of the range at 156.25. If this level is breached, it could increase bearish pressure until the price hits 145.00.

Dollar Enjoys Support from Risk appetite ahead of NFP Report; European Stocks Weaker

Here are the latest developments in global markets:

FOREX: Trump’s decision to exempt the US’ close trade allies Canada and Mexico from hefty import tariffs on steel and aluminum yesterday, while leaving the door open to other countries, and the announcement that he has accepted the invitation to meet the North Korean leader, Kim Yong Un, continued to support the dollar during the European trading session. The dollar index retained its gains from yesterday, last trading at 90.24 (+0.07%), whilst dollar/yen was enjoying gains at 106.77 (+0.54%) ahead of the eagerly awaited nonfarm payrolls report as risk appetite returned to the markets. The BoJ’s decision to maintain its ultra-easy monetary policy until inflation reaches 2.0% didn’t bode well for the yen either. Euro/dollar was stuck at today’s lows, last seen at 1.2298 (-0.08%) as the response out of the EU regarding the US’ import tariff implementation ranged from threats of retaliation to hopes of exemption. Pound/dollar was lacking direction at 1.3817 (+0.04%) after hitting a low of 1.2779 late yesterday since neither Britain was exempted from the US’ protectionist measures. British industrial figures were not good news either today, with all relevant indicators coming in worse than expected. Euro/pound extended losses to 0.8898 (-0.19%). The antipodean currencies were in the green despite China’s warnings to impose strong measures to counter US tariffs, with aussie/dollar and kiwi/dollar changing hands at 0.7802 (+0.15%) and 0.7272 (+0.17%) respectively, however, versus the yen both currencies posted larger gains. Dollar/loonie was fluctuating near today’s lows, last seen at 1.2881 (-0.14%).

STOCKS: European stock indices opened lower on Friday as EU industries dependent on aluminum and steel would potentially feel the pain arising from US import tariffs if the bloc fails to secure an exemption. Still, optimism that the region could eventually be granted an exemption by the US restricted steeper declines. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.05% and 0.12% respectively, led by losses in industrials and financials. The German DAX 30 tumbled by 0.45%, with industrial output data failed to improve sentiment. Particularly, German industrial production decreased by 0.1% in January, less than in December but missed expectations for an expansion of 0.5%. The Italian FTSE MIB dropped by 0.47%, the French CAC 40 retreated by 0.20%, while the British FTSE 100 edged down by 0.04%. US stock futures on major Wall Street indices were slightly weaker.

COMMODITIES: Oil prices were up on the day, underpinned by the progress in the Korean story which lifted Asian equities and overall sentiment. Yet, the market was on track to post losses for the second week. WTI crude rose to $60.62/barrel (+0.88%) and Brent climbed to $64.21/barrel (+1.0%). In precious metals, gold was trading weaker at $1319.76/ounce (-0.18%).

Day ahead: US nonfarm payrolls next to challenge dollar; Canadian labor data also in focus

Day ahead: US nonfarm payrolls next to challenge dollar; Canadian labor data also in focus

The US nonfarm payrolls report will come into center stage at 1330 GMT to move the dollar amid eased geopolitical risks in the Korean peninsula and easing worries over trade. Analysts predict the economy to have added 200,000 new job positions both in the public and private sectors in February (excluding the farm industry), the same as in January, while they expect the unemployment rate to inch down to 4.0%, hitting a fresh 17-year low. However, as in previous releases, the focus will turn to wage numbers as the Fed is eagerly waiting for higher wage growth to pick up and boost inflation before it continues with its pace of gradual rate increases. Growth in average hourly earnings, though, is expected to slow down to 2.8% y/y from 2.9% seen in the preceding month.

In case the data surprise to the upside, especially on the wage front, the chances that the Fed may deliver four rate hikes before the year’s end could increase, raising long positions on the dollar and consequently pushing the currency higher. On the other hand, if the NFP report disappoints, traders could doubt whether inflation has the strength to reach the Fed’s 2.0% target anytime soon, sending the dollar lower.

The US will also see the release of wholesale inventories and the weekly Baker Hughes oil rig count at 1500 GMT and 1800 GMT respectively.

In Canada, employment figures will also attract attention at 1330 GMT. After a deep fall of 88,000 in the number of employees in January, forecasts are now for a rise of 20,000. The unemployment rate though is expected to stay unchanged at 5.9%.

On the trade front, it would be interesting to see the US’ plans for countries such as China and the EU, given their recent warnings for a tit-for-tat retaliation against US protectionism.

Turning to today’s public appearances, the Presidents of the Chicago Fed and the Boston Fed, Charles Evans and Eric Rosengren, will be speaking at 1340 and 1545 GMT respectively. Neither of them holds voting rights within the FOMC in 2018.

EURUSD: Vulnerable, Remains On The Defensive

EURUSD: With the pair retaining its corrective pullback threaten, more weakness is likely. On the upside, resistance comes in at 1.2350 level with a cut through here opening the door for more upside towards the 1.2400 level. Further up, resistance lies at the 1.2450 level where a break will expose the 1.2500 level. Conversely, support lies at the 1.2250 level where a violation will aim at the 1.2200 level. A break of here will aim at the 1.2150 level. Below here will open the door for more weakness towards the 1.2100. All in all, EURUSD faces further bear threats on correction.

DAX Gains Ground on Dovish Draghi

The DAX index has posted slight losses in the Friday session, after sharp gains on Thursday. Currently, the DAX is trading at 12,320.00, down 0.29% since the Thursday close. On the release front, German industrial data continues to disappoint. Industrial Production declined 0.1%, missing the estimate of 0.6%. This marked the fourth decline in the past five months. In the US, the focus is on employment reports. Wage growth is expected to tick lower to 0.2%, while Nonfarm Payrolls are forecast to improve to 205 thousand.

The ECB didn’t change the benchmark interest rate, which remained pegged at 0.00%. Still, the Thursday meeting had plenty of drama, as policymakers removed a long-standing clause known as ‘easing bias’, which stated that monthly asset purchases could be increased if economic conditions were to worsen. The removal of easing bias can be seen as a small step towards winding up the asset program, which is scheduled to end in September. However, Mario Drahgi dampened the party, saying that that eurozone inflation could remain subdued, so the Bank’s monetary policy would remain ‘reactive’. Investors took the comments as a sign that the ECB is no rush to tighten monetary policy, which boosted the German stock markets, while sending the euro sharply downwards.

US President Trump may have said that trade wars are a “good thing”, but his enthusiasm for upheaval in global markets is certainly not shared by investors. On Thursday, US President Trump made good on his threat, and signed an order imposing 25% tariffs on steel imports. EU policymakers have threatened to retaliate with tariffs on US goods, and European Commission President Jean-Claude Juncker was particularly blunt, saying “we can also do stupid”. Fears of an all-out global trade war are weighing on the US dollar and the stock markets, and the resignation of Gary Cohn, a senior economist in the White House who opposed the tariffs, will only dampen investor risk appetite. The ball is now in the EU court, and if the Europeans retaliate and Trump responds with further tariffs, we could see some sharp movement in the stock markets.

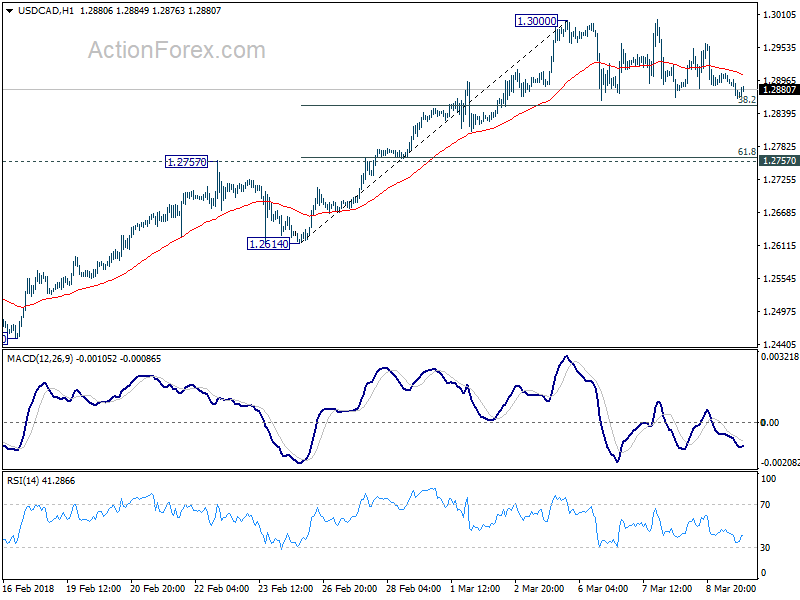

NFP and Canada employment preview, 1.3000 key in USD/CAD

Job data from US and Canada are the two main focuses in US session.

NFP market expectations: -

- Headline NFP number: 205k

- Unemployment rate 4.0%

- Average hourly earnings: 0.20% mom

Other job released data includes ADP at 235k. ISM manufacturing employment rose from 54.2 to 59.8. ISM services employment dropped from 61.6 to 55.0. Initial claims and continuing claims were both at historically low level during the month. Hence, it's more likely for headline NFP to deliver, or even surprise to the upside. The key is again on wage growth, which will determine the chance of the fourth Fed hike this year.

Canada employment, market expectations: -

- Net change in employment: 21k

- Unemployment rate: 5.9%

Being exempted temporarily from Trump's steel and aluminum tariffs is a relief for BoC. But the neverending NAFTA renegotiation is still a risk. Adding to that, if NAFTA talks fail, the tariffs will more likely come back than not. So BoC will likely stand pat until the picture because clearly. Risks will be more skewed to the downside for CAD on today's release.

USD/CAD is staying in consolidation from 1.3000, holding quite well above 38.2% retracement of 1.2614 to 1.3000. This 1.3000 level will be the key to watch as a break could trigger upside acceleration when rise from 1.2246 resumes.