Sample Category Title

GBP/USD Trying To Bounce

GBP/USD is starting a recovery phase following its descent at 1.3782, currently trading at the 1.3820 range. The pair is trading between hourly support and resistance at 1.3678 (12/01/2018 low) and 1.3945 (19/01/2018 high). The technical structure suggests short-term increase.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Moving Sideways

EUR/USD is stabilizing at the 1.2310 range following recent decline from 1.2446 high. Hourly support and resistance are given at 1.2112 (12/01/2018 low) and 1.2475 (31/01/2018 high). The technical structure suggests further short-term sideway moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Market Update – European Session: Olive Branch By North Korea Helps Risk Appetite, Focus On US Jobs Report

Notes/Observations

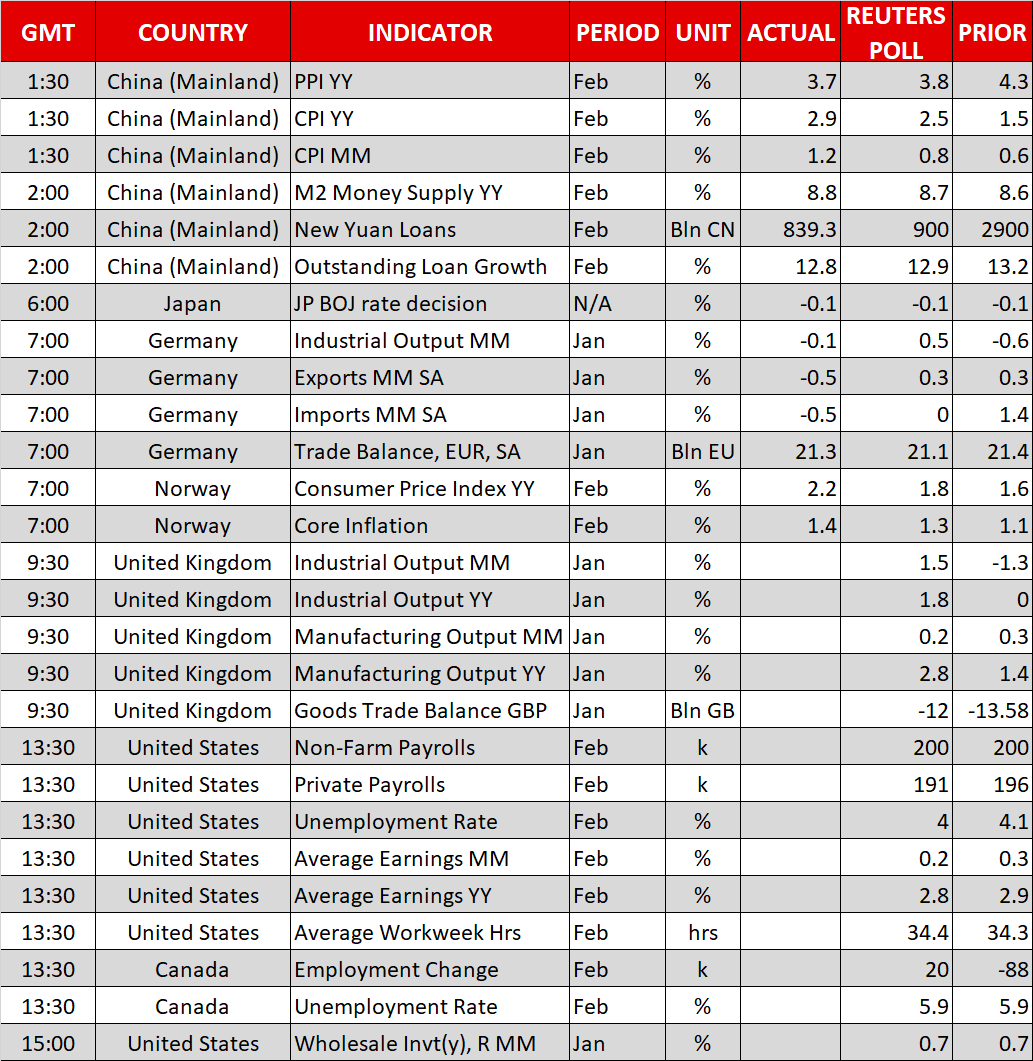

Norway Feb CPI moves back above target keeping rate hike hopes intact for 2018 while Czech CPI back with the target range for 1st time in 15 months

German Jan Industrial Production misses expectations; hinting that momentum might have peaked for the time being

UK data releases mixed in session (Industrial Production misses while Visible Trade Balance better than consensus)

President Trump has signed the new steel (25%) and aluminum (10%) tariffs bill taking effect in 15 days. The initial plan was for a global levy, but Trump made it clear that exceptions would be made; risk appetite picks up as a result

President Trump accepted an offer to meet North Korea leader Kim Jong Un; North Korea offered to suspend nuclear missile testing

US Feb jobs reports and hourly earnings in focus

Asia:

China Feb CPI data bests expectations and nears target with YoY reading of 2.9% being the highest since Dec 2013

China PBoC Gov Zhou: Recent FX reserve change mainly due to dollar rate change. China should watch inflation to measure monetary policy. Economy to rely less on quantitative stimulus; real interest rates had been steady, economic conditions to determine whether China would raise rates

BOJ left its Interest Rates on Excess Reserves (IOER) unchanged at -0.10% (as expected). Maintained 10-year JGB Yield Control (YCC) at 0.00% and its annual pace of JGB holdings unchanged at ¥80T. Voted 8 to 1 with member Kataoka dissenting for 5th straight meeting; Kuroda continued to convey his dovish stance during press conference

North Korea Leader Kim Jong Un said to invite US President Trump to meeting

Europe:

Internal ECB staff calculations on monetary policy assumed final €30B of QE purchases in Q4 (**Reminder: At the Oct 2017 ECB policy decision ECB QE bond buying program was downsize to €30B per month until Sept 2018 (9-month extension)

UK govt officials reportedly did not see reaching a Brexit deal until next year with Jan 2019 is the real deadline to reach an accord in time for exit day (**Reminder: EU chief negotiator Barnier had previously stated that he wanted the deal done by October 2018 so there would be time for a withdrawal treaty to go to European and UK parliaments for approval)

UK Foreign Min Johnson: UK govt was prepared for a "no deal" Brexit scenario. Believed that a no deal Brexit should not hold any terrors for UK because we'd 'do very well' under WTO rules

Americas:

President Trump signed steel and aluminum tariff proclamation (as expected). Open to modifying or removing tariffs for individual countries as long as find way to ensure products no longer threaten security; US Trade Rep Lighthizer to be in charge of accepting offers from countries seeking exemptions

Steel and aluminum tariffs reportedly to take effect in 15 days, with Mexico and Canada exempted indefinitely

Mexico Fin Min Gonzalez Anaya stated that it would not allow US tariff proposals to pressure NAFTA talks. Mexico had no plans to abandon NAFTA talks and to spend as much time as necessary for successful NAFTA talks

Fed George (hawk) reiterated important to continue gradual normalization of rates

Bank of Canada (BOC) Dep Gov Lane reiterated that higher rates were likely needed over time; key BOC rate was appropriately below neutral. BOC was not on a pre-set path to higher interest rates; every decision was a live decision

Economic Data:

(DE) Germany Jan Current Account: €22.0B v €17.2Be; Trade Balance: €17.4B v €18.1Be; Exports M/M: -0.5% v +0.3%e Imports M/M: -0.5% v -0.1%e

(DE) Germany Jan Industrial Production M/M: -0.1% v +0.6%e; Y/Y: 5.5% v 6.0%e

(DE) Germany Q4 Labor Costs Q/Q: 0.4 v 0.5% prior; Y/Y: 1.5% v 2.2% prior

(NO) Norway Feb CPI M/M: 0.9% v 0.7%e; Y/Y: 2.2% v 1.8%e (moves back above target)

(NO) Norway Feb CPI Underlying M/M: 0.8% v 0.7%e; Y/Y: 1.4% v 1.3%e

(NO) Norway Feb PPI including Oil M/M: -2.6% v +3.1% prior; Y/Y: 4.7% v 10.3% prior

(FI) Finland Jan Industrial Production M/M: 0.1% v 1.8% prior; Y/Y: 4.8% v 4.2% prior

(FI) Finland Jan Preliminary Trade Balance: -€0.2B v -€0.4B prior

(CN) Weekly Shanghai copper inventories (SHFE): 268.1K v 260.3K tons prior

(FR) France Jan Industrial Production M/M: -2.0% v -0.3%e; Y/Y: 1.2% v 3.8%e

(FR) France Jan Manufacturing Production M/M: -1.1% v +0.3%e; Y/Y: 3.3% v 4.8%e

(FR) France Jan YTD Budget Balance: -€10.8B v -€67.8B prior

(ES) Spain Jan Industrial Output NSA Y/Y: 4.0% v 3.1% prior; Industrial Output SA Y/Y: 1.2% v 5.1%e, Industrial Production M/M: -2.6% v 0.0%e

(CZ) Czech Jan National Trade Balance (CZK): 11.9B v 20.3Be

(CZ) Czech Feb CPI M/M: 0.2% v 0.2%e; Y/Y: 1.8% v 2.0%e (back with target range for 1st time in 15 months)

(CZ) Czech Q4 Average Real Monthly Wage Y/Y: 5.3% v 5.2%e

(HU) Hungary Jan Preliminary Trade Balance: €0.7B v €0.5Be

(SE) Sweden Feb Average House Prices (SEK): 3.114M v 3.188M prior

(SE) Sweden Jan Household Consumption M/M: -0.1% v -0.4% prior; Y/Y: 0.8% v 2.1% prior

(IS) Iceland Q4 GDP Q/Q: 0.6% v 3.1% prior; Y/Y: 1.5% v 3.4% prior

(IT) Italy Jan PPI M/M: 0.8% v 0.0% prior; Y/Y: 1.8% v 2.2% prior

(UK) Jan Visible Trade Balance: -£12.2B v -£11.9Be, Overall Trade Balance: -£3.1B v -£3.3Be, Trade Balance Non EU: -£3.9B v -£4.5Be

(UK) Jan Industrial Production M/M: 1.3% v 1.5%e; Y/Y: 1.6% v 1.9%e

(UK) Jan Manufacturing Production M/M: 0.1% v 0.2%e; Y/Y: 2.7% v 2.8%e

(UK) Jan Construction Output M/M: -3.4% v -0.5%e; Y/Y: -3.9% v -1.0%e

(IT) Bank of Italy (BOI) Jan Monthly Report `Money and Banks': Bad loans at €166.5B v €167.4B m/m

(GR) Greece Feb CPI Y/Y: +0.1% v -0.2% prior; CPI EU Harmonized Y/Y: 0.4% v 0.2% prior

Fixed Income Issuance:

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2033, 2038 and 2050 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 376.4, FTSE flat at 7201, DAX -0.5% at 12293, CAC-40 -0.2% at 5244, IBEX-35 flat at 9655, FTSE MIB -0.3% at 22662 , SMI -0.1% at 8892, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes: European Indices trade little changed in a quiet session this morning ahead of today Feb Non Farm Payroll report, in what has been a quiet morning on the corporate front. Notable earners related movers include French name CGG, trading higher on earnings; Lagadere trades ~7% lower on a subdued outlook and poor FCF. In the UK Inmarsat trades sharply lower after a decline in profits and cut dividend, with SIG also lower on earnings. Looking ahead notable earners include Big lots and American Woodwork.

Movers

Consumer Discretionary [ Lagadere [MMB.FR] -7.0% (Earnings), GVC [GVC.UK]+2.9% (Earnings)]

Consumer Staples [-Schouw {SCHO.DK] +1.2% (Earnings)]

Industrials [ Schweiter Tech [SWTQ.CH] +1.7% (Earnings), SFS [SFSN.CH] +2.6% (Earnings)]

Materials [SIG Plc [SHI.UK]+1.0% (Earnings)]

Financial [ UBS [UBSG.CH] -0.9% (Annual report) ]

Telecom [Inmarsat [ISAT.UK] -5.1% (Earnings)]

Energy [PCGG [CGG.FR] +9.1% (Earnings)]

Speakers

ECB's Vasiliauskas (Lithuania): Now a good time to make commun ication steps; dropping easing bias was a very logical step

German SPD party confirmed speculation that Scholz to become Finance Minister in the new government

Italy 5-star leader Di Maio: Prepared to talk to all parties about issues and program points but not about ministerial positions at this time

EU Trade Min Malmstrom: To seek exemption from US tariffs; reiterates EU threat to retaliate against US tariffs and file WTO case. Trump tariffs were the wrong policy

BOJ Gov Kuroda post rate decision press conference reiterated view that expected inflation to move towards the 2% target; to make adjustments as needed. Reiterated to make any adjustments to keep momentum as takes time to overcome the deflation mindset. Reiterated high chance of achieving the 2% inflation target in FY19/20 period but did not suggest any immediate exit (**Note clarified his comment from last Friday in Parliament). Would persistently continue with monetary easing

Indonesia Central Bank reiterated view that monetary policy stance to remain neutral; to consider development in economy and global in next rate meeting

Currencies

USD has held on to recent gains as markets perceived Trump had created loopholes in his tariff plan.

EUR/USD was little changed as dealers reassessed the recent tweak in the ECB language that it would drop explicit pledge to increase size of QE if needed. The move was generally viewed as the minimum necessary towards the overall path towards policy normalization. Some analysts remained positive of the Euro’s outlook with 1.28 seen in the cards before the end of the year. The 1.2550 remains the key resistance for now. German Jan Industrial Production missed expectations; hinting that momentum might have peaked for the time being (Factory orders recent missed)

USD/JPY was higher as safe-haven flows ebbed. JPY currency (Yen) was weaker on hopes for easing U.S.

North Korea tensions. President Trump accepted an offer to meet North Korea leader Kim Jong Un; North Korea offered to suspend nuclear missile testing. Analysts believe the USD/JPY pair could retest the 108 level quite soon.

GBP/USD was little changed as the economic releases in the session were mixed (IP miss while trade data was better than expected). Pair steady just above the 1.38 level just ahead of the NY morning

Fixed Income

Bund Futures trade 20 ticks lower at 157.02 with the focus on US nonfarm payroll report. Upside targets 157.50, while a return lower targets the155.75 level.

Gilt futures trade at 122.26 down 25 ticks with little reaction to UK Trade and production data. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Friday's liquidity report showed Thursday's excess liquidity rose to €1.886T from €1.884T prior. Use of the marginal lending facility stayed steady €0M.

Corporate issuance saw 10 issuers raise $9.3B in the primary market

Looking Ahead

(MX) Mexico Feb Nominal Wages: No est v 4.7% prior

06:00 (IE) Ireland Jan Retail Sales Volume M/M: No est v -0.1% prior; Y/Y: No est v 7.2% prior

06:00 (BR) Brazil Mar IGP-M Inflation (1st Preview): 0.2%e v 0.0% prior

06:00 (UK) DMO to sell combined £5.0B in 1-month, 3-month and 6-month Bills (£2.0B, £1.0B and £2.0B respectively)

06:30 (IS) Iceland to sell 2028 RIKB Bonds

06:30 (IN) India Weekly Forex Reserves

06:45 (US) Daily Libor Fixing

07:00 (UK) Feb NIESR GDP Estimate: 0.4%e v 0.5% prior

07:00 (BR) Brazil Feb IBGE Inflation IPCA M/M: 0.3%e v 0.3% prior; Y/Y: 2.8%e v 2.9% prior

07:00 (CZ) Czech Central Bank comments on inflation data

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond auction (held on Thurs)

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Feb Change in Nonfarm Payrolls: +205ke v +200K prior, Change in Private Payrolls: +205Ke v +196K prior, Change in Manufacturing Payrolls: +15Ke v +15K prior

08:30 (US) Feb Unemployment Rate: 4.0%e v 4.1% prior, Underemployment Rate: No est v 8.2% prior

08:30 (US) Feb Average Hourly Earnings M/M: 0.2%e v 0.3% prior; Y/Y: 2.8%e v 2.9% prior; Average Weekly Hours: 34.4e v 34.3 prior

08:30 (CA) Canada Feb Net Change in Employment: +21.0Ke v -88.0K prior; Unemployment Rate: 5.9%e v 5.9% prior

08:30 (CA) Canada Q4 Capacity Utilization Rate: 85.2%e v 85.0% prior

10:00 (US) Jan Final Wholesale Inventories M/M: 0.7%e v 0.7% prelim; Wholesale Trade Sales M/M: No est v 1.2% prior

11:00 (EU) Potential Sovereign ratings after European close: Hungary Sovereign Debt to be rated by Fitch

12:40 (US) Fed’s Rosengren (moderate, non-voter) on outlook

12:45 (US) Fed’s Evans (non-voter, dove) on monetary policy

13:00 (US) Weekly Baker Hughes Rig Count data

Technical Outlook: WTI OIL – Bears Are Pausing On Improved Sentiment, But Outlook Remains Negative

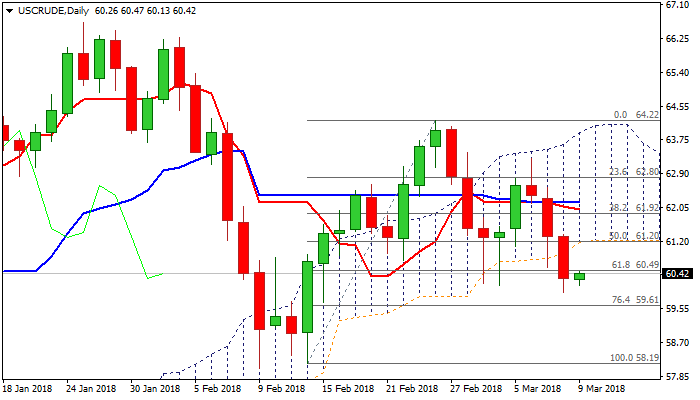

WTI oil ticked higher on Friday, taking a breather after strong three-day fall from $63.26 lower top resulted in brief probe below psychological $60 support on Thursday.

Improved market sentiment on news of US – NK talks lifted oil price on Friday, but risk of further weakness remains as concerns about production and rising US crude stocks keep oil price pressured.

Thursday’s fall generated bearish signal on close below $60.49 pivot (Fibo 61.8% of $58.19/$64.22 rally), which now acts as initial resistance and caps recovery attempts for now.

Stronger upticks through $60.49 barrier are not ruled out as slow stochastic is at the border of oversold zone, with base of thick daily cloud at $61.23, expected to cap and keep bears intact for fresh downside.

Res: 60.49, 60.86, 61.23, 61.57

Sup: 60.12, 59.94, 59.55, 59.10

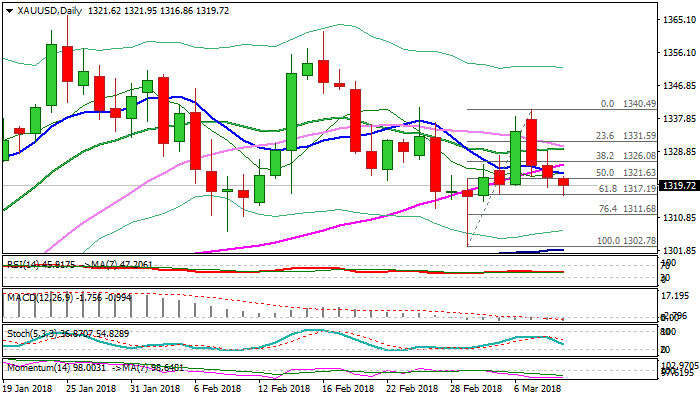

Technical Outlook: Spot Gold Remains Under Strong Pressure As Safe Haven Demand Eases

Spot Gold remains in red for the third straight day and extended bear-leg from $1340 high, to crack pivotal support at $1317 (Fibo 61.8% of $1302/$1340 rally).

News about meeting between leaders of the US and North Korea eased geopolitical tensions, with slight ease of concerns about global trade war, reduced demand for safe-haven assets, keeping the yellow metal under increased pressure.

Daily techs in firm bearish setup support scenario, which looks for close below $1317 Fibo support to generate further bearish signal.

Strong US jobs numbers today could help gold bears by boosting the dollar and sending gold price lower.

Bearish acceleration below $1317 would unmask key supports at $1302/01 (01 Mar spike low / base of thick daily cloud).

Falling 10SMA which created bear-cross with 55SMA offers initial resistance at $1322, followed by 55SMA at $1325 and 20SMA at $1329, which is expected to limit stronger upticks.

Res: 1322, 1325, 1329, 1332

Sup: 1316, 1311, 1307, 1302

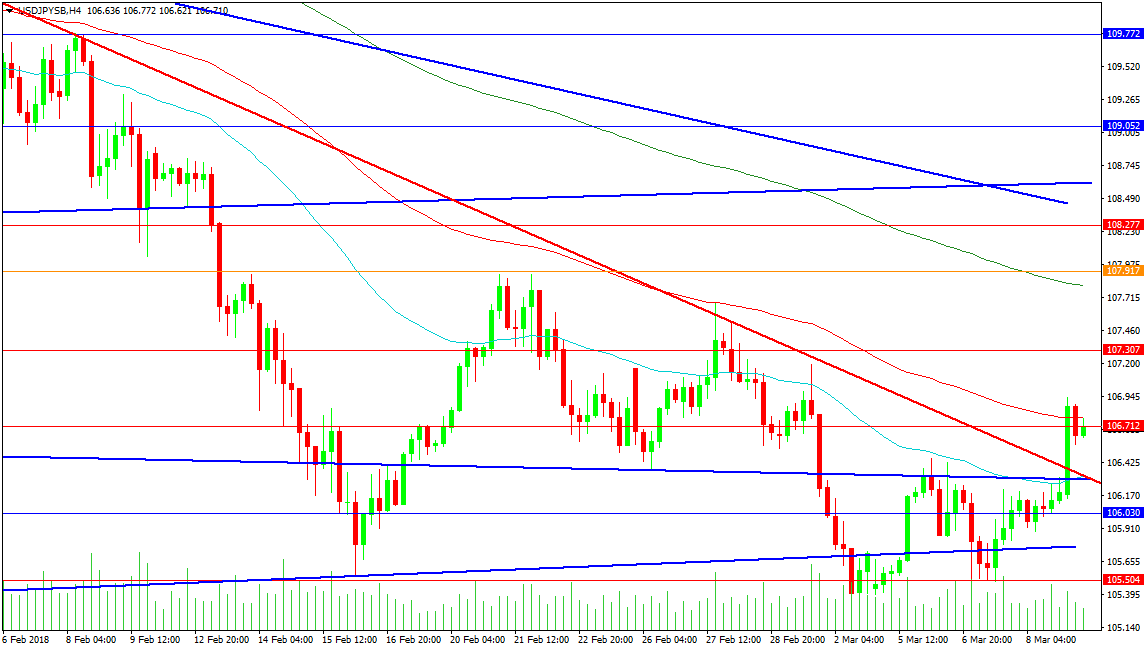

Forex Analysis: USDJPY And GER 30

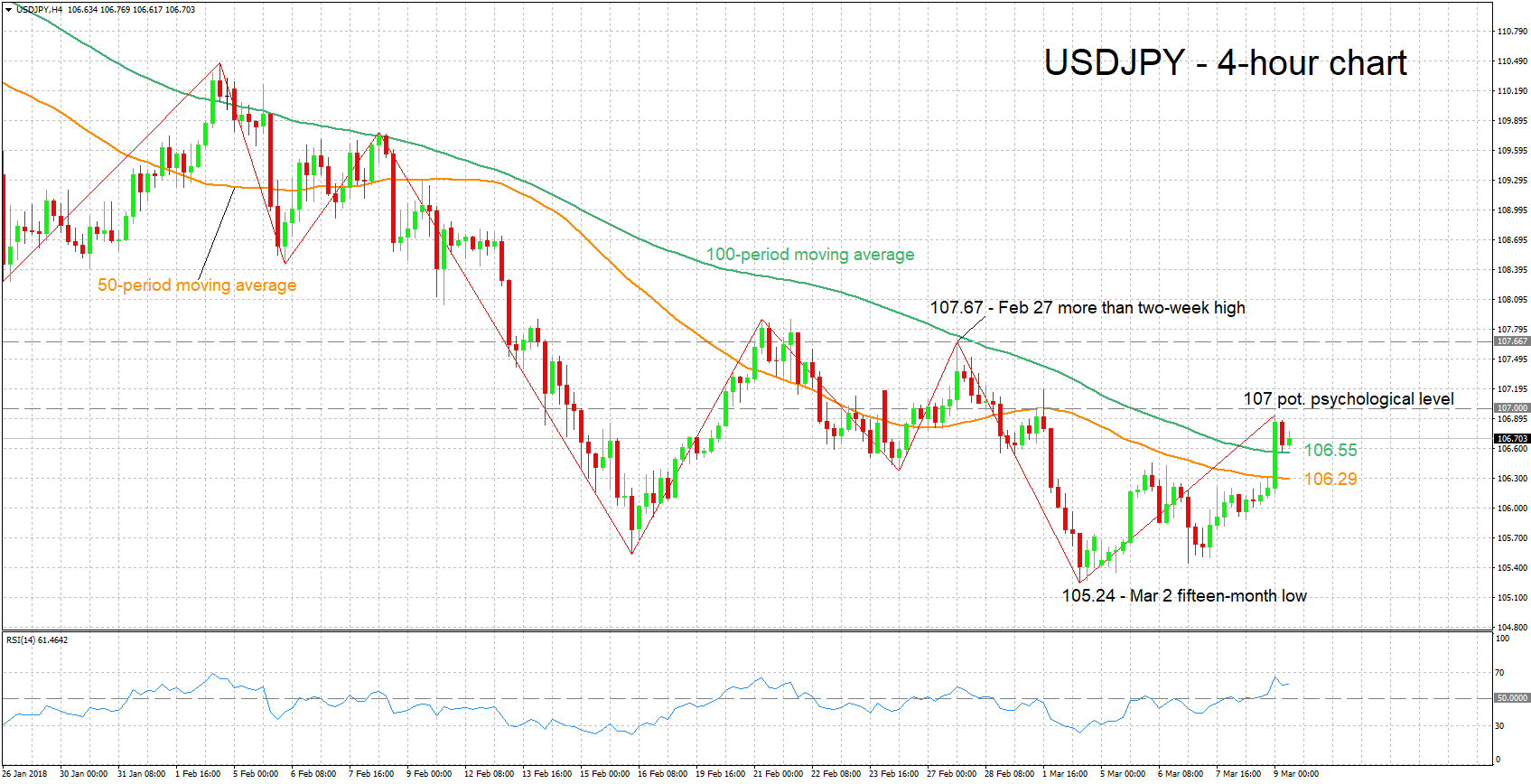

The USDJPY pair has broken higher overnight, with the easing of tensions with North Korea. The regime has softened its approach and reached out with a suspension of nuclear weapon and missile tests. The BOJ has left rates on hold and continues its yield targets for JGBs. This has led to a break above trend line resistance at 106.385 to test the 107.000 level. Momentum carried the price above the 100-period 4-hour MA at 106.778 but it has since moved back below this level, which is now being used as resistance. Price is currently testing 106.712, with a break below finding support at 106.300 and the 50-period MA combined with the two trend lines shown. A successful retest of this breakout level targets 108.277 and the trend lines at 108.440 and 108.600. There is further resistance at 109.052 and 109.772, followed by the 110.000 level.

Support can be seen at 106.030, with rising trend line support at 105.768. Wednesday’s low is found at the 105.504 level, with the previous low at 105.243. The 105.000 level is acting as a strong supporting area.

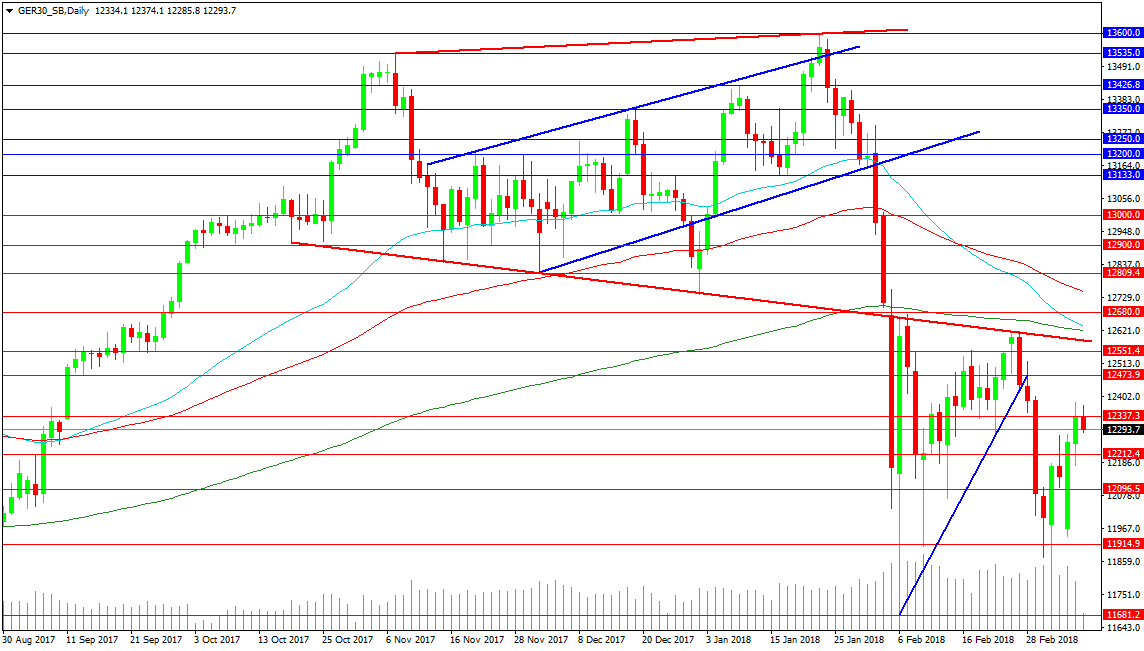

GER 30

The German Index has seen price rally higher from 11728.70 on Monday, putting in a strong reversal for the week. This, in the context of recent price action, unfortunately, means very little so far, as all major levels remain untested. From a resistance perspective, the falling trend line at 12583.00 needs to be tested and overcome to give the bulls hope of driving higher. Above this area, the 200-day MA is found at 12621.00, with the 50-day MA at 12633.6. The 100-day MA is at 12750.00 and a break above here targets the 13000.00 area. A strong push above this area, linked to global bullish sentiment, can support a move to the old highs at 13600.00.

Support is found at the 12000.00 area, with a loss of this area suggesting that a lower high has been formed and that there is potential for a lower low, with a break below 11681.2. Targets in extension below this area come in at 11444.00 and 11300.00.

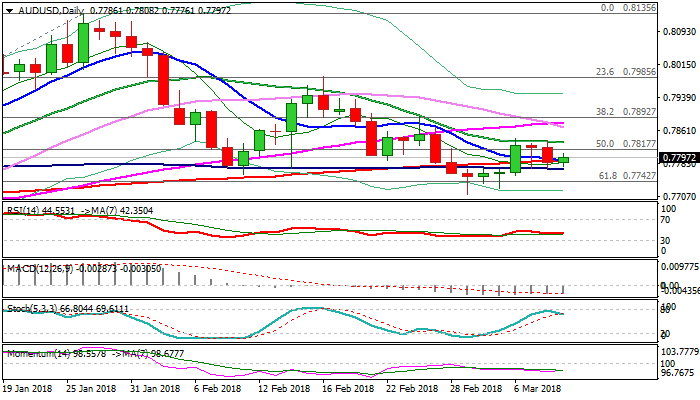

Technical Outlook: AUDUSD Remains In Range Between 100 And 20SMA’s, Awaiting Stronger Direction Signal

The Australian dollar moved higher on Friday after falling the previous day but remains without clear direction as near-term action continues to move in range between 100SMA (0.7771) and 20SMA (0.7834). Multiple attempts to break out of the range were so far unsuccessful, suggesting the pair needs stronger catalyst for fresh direction signal. Mixed signals from daily chart supports directionless near-term mode, however, strong bearish momentum and thick daily cloud which limited recent recovery attempts, keep the structure bearishly aligned. US jobs data are focused for firmer signal and could put the Aussie under increased pressure on strong release today. Bears need firm break below 100SMA to generate negative signal and spark fresh weakness towards pivots at 0.7742 (cracked Fibo 61.8% of 0.7500/0.8135 rally) and 0.7712 (01 Mar low). Bullish scenario requires penetration of daily cloud and firm break above 20SMA to spark stronger recovery.

Res: 0.7817, 0.7836, 0.7878, 0.7893

Sup: 0.7771, 0.7756, 0.7742, 0.7712

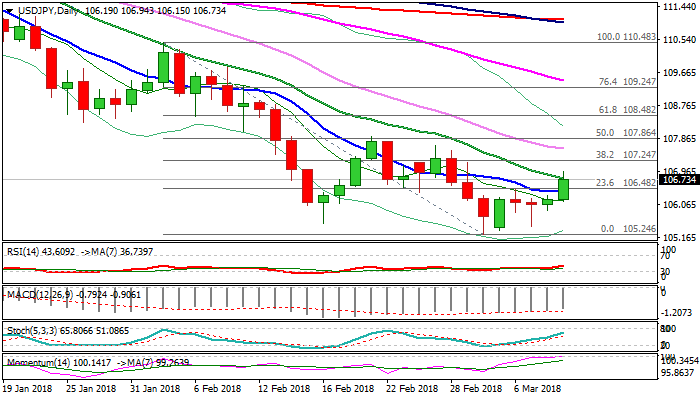

Technical Outlook: USDJPY – Near-Term Picture Improves On Fresh Rally

The pair bounced higher in Asia, breaking above three-day congestion and hitting one-week high at 106.94, on easing fears over North Korea. No significant reaction was seen on BOJ rate decision and remarks from BoJ chief Kuroda, who confirmed that the central bank will continue its ultra-light policy until inflation reaches target at 2.0%. Today's rally was positive signal and improved near-term structure, as fresh bullish momentum is building. Break above initial Fibo/10SMA barrier at 106.44 extended recovery and cracked next pivot at 106.76 (falling 20SMA/Fibo 61.8% of 17.67/105.24), signaling further advance. US jobs data could spark fresh bullish acceleration on strong numbers and could challenge lower tops at 107.67 (27 Feb) and 107.90 (21 Feb) on sustained break above 107.24 (Fibo 38.2% of 110.48/105.24 bear-leg). Broken 10 SMA now acts as initial support (106.41) which is expected to hold and keep fresh bulls in play.

Res: 106.94, 107.24, 107.67, 107.90

Sup: 106.41, 106.15, 105.89, 105.45

Yen Falls As Possible US-North Korea Talks Spur Risk Appetite, US Jobs Report Firmly In Focus

Here are the latest developments in global markets:

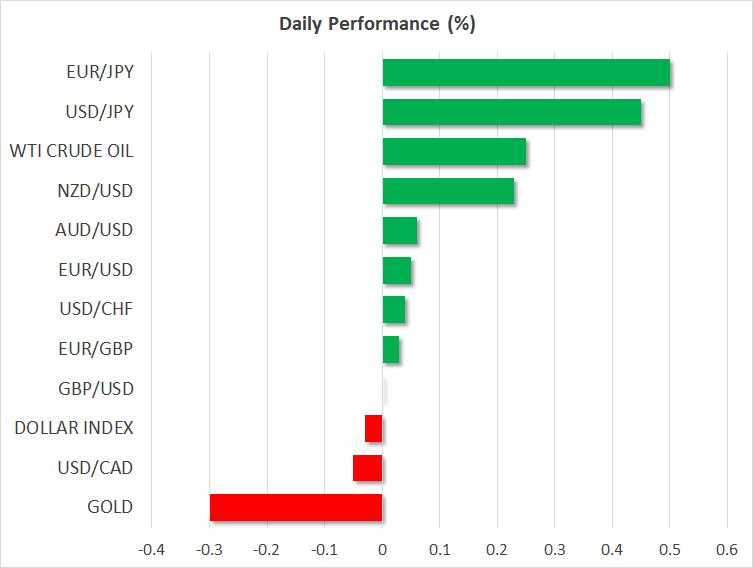

FOREX: The yen was recording significant losses versus other major currencies on the back of elevated risk sentiment spurred by a possible meeting between US President Donald Trump and North Korea’s Kim Jong Un.

STOCKS: US markets closed higher on Thursday, as the imposition of “watered down” US tariffs amplified expectations that the tensions will not escalate into a trade war, but may instead remain relatively contained. The S&P 500 led the charge, climbing 0.5%, while the Dow Jones and the Nasdaq Composite followed in its tracks, each gaining 0.4%. Futures tracking the S&P, Dow, and Nasdaq 100 are currently in negative territory, but only marginally so. Asian markets were a sea of green, as risk appetite was boosted by news that US President Trump agreed to meet with North Korea’s leader, helping to curb geopolitical risks. In Japan, the Nikkei 225 and the Topix rose by 0.5% and 0.3% respectively, while in Hong Kong, the Hang Seng was nearly 1.0% higher. In Europe though, futures tracking the major indices were all flashing red, with the exception of Spain’s IBEX 35.

COMMODITIES: Oil prices were a little higher on Friday, with WTI crude and Brent gaining 0.2% and 0.3% respectively, both benchmarks recovering some of the losses they posted on The fall in prices is being attributed to the gains the dollar posted yesterday, though concerns surrounding the surge in US production may have contributed to the down-move as well. Today, investors will look to the Baker Hughes oil rig count (1800 GMT) for a fresh indication on whether US supply continues to soar. In precious metals, gold was 0.2% lower on Friday, posting losses for the third consecutive day. The stronger dollar and the deescalating tensions in the Korean peninsula are likely the “culprits” behind the yellow metal’s pullback.

Major movers: Yen records losses on improving risk sentiment

The dollar was notably higher versus the safe-haven yen, touching an eight-day high of 106.94 at its peak. US President Donald Trump showing willingness to meet with North Korea’s Kim Jong Un by May was the catalyst behind the positioning by market participants, with the move seen as further easing tensions between the two parties and giving traction to the denuclearization talk from earlier in the week. At 0733 GMT, dollar/yen traded 25 pips below the aforementioned high and at a distance to last week’s 16-month low of 105.23.

Overall risk appetite got a boost on the news, with Asian equities rising across the board.

The Trump administration proceeded with the imposition of tariffs on steel and aluminum, exempting though Canada and Mexico though, and leaving the door open for other countries to be exempted. The administration’s stance was viewed by markets as more moderate than previously and was seen as reducing the odds for a global trade war.

Abating geopolitical worries seem to be driving sentiment for now, but trade concerns could well make a comeback.

Earlier on Friday, the Bank of Japan completed its meeting on monetary policy, keeping policy unchanged. The Japanese currency showed limited reaction to the decision. In the press conference that followed, BoJ Governor Haruhiko Kuroda recognized that the trade policy of the US poses risks to the global economy.

Euro/dollar was roughly flat at 1.2314 after losing 0.8% on Thursday in the aftermath of the ECB’s respective meeting on monetary policy. The Bank dropped its pledge to increase its asset purchases if needed, something which initially supported the euro. However, ECB chief Mario Draghi later played down the significance of the decision, while adding that inflation in the euro area remains muted. The euro was another currency posting considerably gains versus the yen during Friday’s trading. Euro/yen was 0.5% up at 131.41, making up for a significant portion of yesterday’s losses.

Elsewhere, pound/dollar was practically unchanged at 1.3813.

In emerging markets, the yuan didn’t react much versus the greenback to stronger-than-anticipated inflation figures that saw annual CPI rise to its highest in four years (PPI slightly surprised to the downside). It is interesting that markets shrugged off a warning by China that it will take “strong” measures against US tariffs. Dollar/yuan was 0.1% down at 6.3350 after previously recording a one-week high of 6.3526.

Day ahead: US payrolls & wage data and Canadian jobs figures on the agenda; potential tariff retaliations eyed

The main event today will be the US employment report for February at 1330 GMT. Nonfarm payrolls are anticipated to have risen by 200k, exactly as much as in the previous month, the unemployment rate is projected to have ticked down to 4.0%, while average hourly earnings are expected to have slowed to 2.8% in yearly terms, from 2.9% previously. Given the recent market narrative that US inflation may be set to pick up speed soon, investors may pay special attention to the earnings figures, as wage growth is broadly considered a precursor to inflation.

In case these data come out stronger than anticipated – particularly on the wages front – markets are likely to begin pricing in a higher probability that the Fed may deliver four quarter percentage point rate hikes this year, from the three that are already priced in. The dollar could come under renewed buying pressure in this scenario, as the yields on US bonds will likely surge. A disappointment, on the other hand, would likely dampen inflation concerns, and possibly generate some skepticism as to how many hikes the Fed will deliver this year, thereby weighing on the greenback.

Canada will also release its own employment data for February at 1330 GMT. The unemployment rate is forecast to have held steady at 5.9%, while the net change in employment is anticipated to have rebounded, following a sharp decline before. Such prints would likely be encouraging news for the Bank of Canada – which maintained a fairly cautious bias on Wednesday in the face of trade uncertainties – and could help the loonie to recover some of its recent losses.

In the UK, industrial output prints for January are due out at 0930 GMT and expectations are for the figure to have risen by 1.5% in monthly terms, following a 1.3% fall last month.

In equity markets, the “trade war” theme will probably continue to dominate price action. Following the official imposition of US tariffs yesterday, it will be interesting to see how major economies like the EU and China will respond, as both have already noted they will retaliate in kind. The magnitude and scope of these responses could well serve as a gauge of whether trade tensions are likely to escalate further, or whether they may subside somewhat.

In energy markets, investors will look to the release of the Baker Hughes oil rig count at 1800 GMT, for a fresh indication on whether US oil production continues to soar. Despite the latest EIA data showing that US output reached a fresh record high last week, the rig count has barely risen over the past couple of weeks, suggesting that the supply increase is slowing down. If that pattern continues today, then some of the downward pressure on oil prices could ease as investors might speculate that US production is close to peaking.

In terms of policymaker appearances, there are four on the agenda. In Europe, ECB Executive Board members Benoit Coeure and Sabine Lautenschlager will deliver remarks at 0830 and 0845 GMT respectively. A few hours later across the Atlantic, the Presidents of the Chicago Fed and the Boston Fed, Charles Evans and Eric Rosengren, will be speaking at 1340 and 1545 GMT respectively. Neither of them holds voting rights within the FOMC in 2018.

Technical Analysis: USDJPY records 8-day high; NFP report could fuel or bring to a halt the bullish sentiment

USDJPY recorded an eight-day high of 106.94 earlier on Friday. The RSI indicator has crossed above the 50 neutral-perceived level and continues rising, projecting a bullish picture in the near-term. The nonfarm payrolls report due later in the day has the capacity to dictate the pair’s short-term direction.

A stronger-than-expected report, especially on the front of wage growth, is expected to boost the pair. The range around the 107 handle which was congested in the past (with 107 potentially holding psychological significance as well) could act as a barrier to the upside in this case. A break above this area would turn the attention to the more-than-two-week high of 107.67 for additional resistance.

On the other hand, disappointing figures are anticipated to lead to losses for the pair. In this scenario, support might come around the current levels of the 100- and 50-period moving averages at 106.55 and 106.29 respectively.

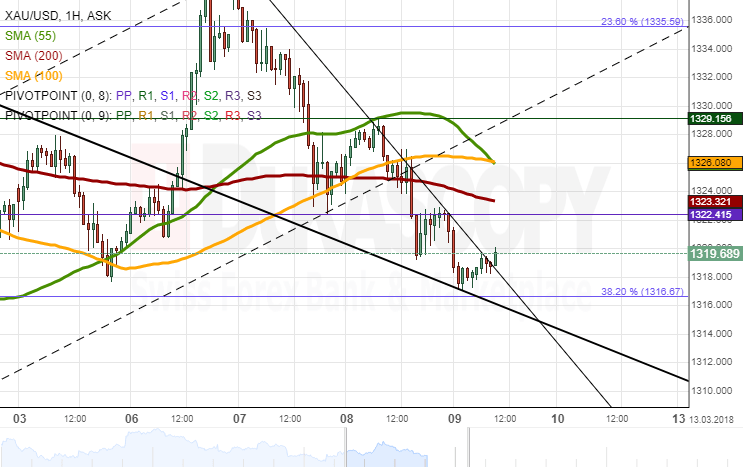

XAU/USD Analysis: Returns To 1,320.00

Bears have been guiding XAU/USD for the second consecutive session. This sentiment was strong enough to allow for a breakout of the 100– and 200-hour SMAs and the bottom boundary of a short-term channel up circa 1,325.00. By Friday morning, the pair had returned at a previously-breached channel and the 38.20% Fibo retracement. According to technical indicators, some downside potential could still be realised in this session. The ultimate daily low should be the 1,305.00 area where the lower line of the senior channel and the monthly S1 are located. Meanwhile, the pair has formed a minor falling wedge that could be soon breached to the upside, thus sending the yellow metal towards the aforementioned SMAs, with gains being capped near 1,330.00.