Sample Category Title

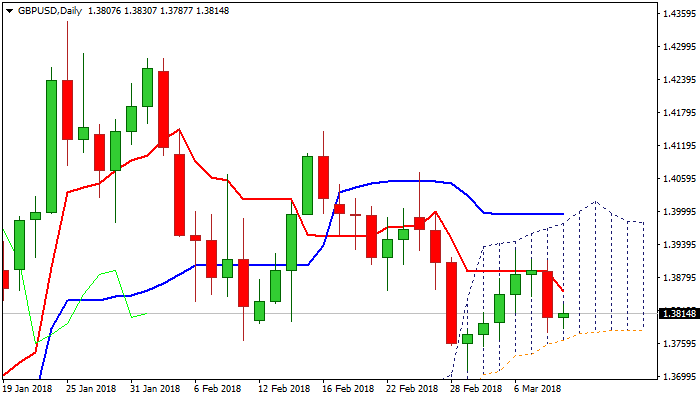

Technical Outlook: GBPUSD – Bearish Bias Suggests Further Weakness Through Daily Cloud Base, UK/US Data Eyed For Fresh Signals

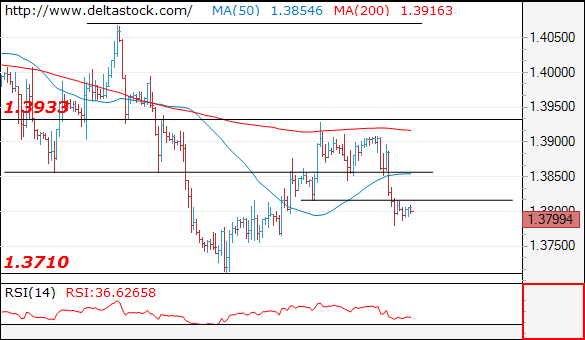

Cable is consolidating on Friday following strong fall on Thursday, which reversed the biggest part of four-day 1.3711/1.3929 rally and turned near-term bias to bearish mode.

Fresh bears are pressuring key near-term support at 1.3765 (daily cloud base).

Thursday’s fall completed reversal pattern on daily chart, which weighs on near-term action.

Daily MA’s are back to bearish setup and maintain pressure, along with negative momentum studies.

Daily cloud base is key and firm break lower would generate fresh bearish signal for retest of 1.3711 pivot and possible extension lower.

Batch of UK data are in immediate focus and miss would increase pressure, with US NFP data eyed for further signals.

Strong numbers from US labor sector would further pressure pound.

Broken 55 SMA (1.3830) is initial resistance and caps the upside for now, with stronger rally above 10SMA (1.3845) needed to sideline immediate bearish risk.

Res: 1.3830, 1.3845, 1.3890, 1.3905

Sup: 1.3780, 1.3765, 1.3711, 1.3660

EU Malmstrom: EU should be excluded from US steel and aluminum tariffs

Some responses from EU on Trump's steel and aluminum tariffs:

Trade Commissioner Cecilia Malmstrom: -

- "The EU is a close ally of the US and we continue to be of the view that the EU should be excluded from these measures."

- "Protectionism cannot be the answer, it never is."

Germany Economy Minister Brigitte Zypries: -

- "The 'national security' argument could set a precedent.

- "The fear is that a series of other countries could use the national security argument to shut off their markets.

- "That would risk undermining global trade rules thrashed out laboriously over decades.

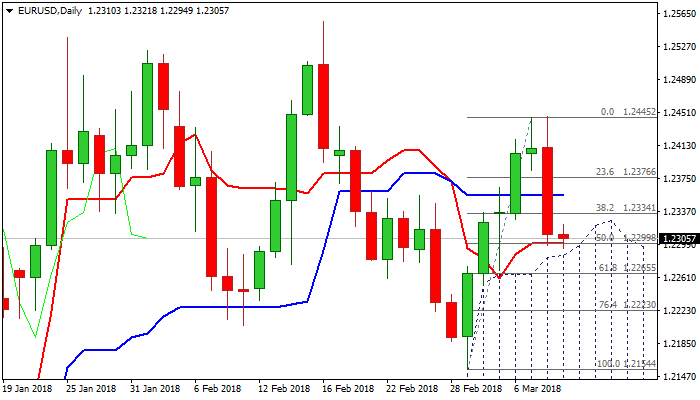

Technical Outlook: EURUSD Pressures Top Of Thick Daily Cloud After Post-ECB Sharp Fall, US Jobs Data In Focus

The Euro is trading within narrow consolidation on Friday after suffering heavy losses on 0.8% fall on Thursday, which marks the biggest one-day loss since 07 Feb.

The single currency came under strong pressure from remarks of ECB President Mario Draghi in the press conference after central bank’s policy meeting.

The ECB left interest rates unchanged as expected but Draghi pointed at underlying inflation which remains subdued and marks the main obstacle for the central bank to start tightening the policy, despite strong economic growth.

Focus turns today at US jobs data, due later today, for fresh signals about the strength of the US labor market, after release on Thursday showed weekly jobless claims increased more than expected last week.

US Non-Farm payrolls are forecasted at 200K, signaling unchanged number of new jobs from the previous month, but the figure is considered as strong and expected to send unemployment to multi-year low at 4.0%, from 4.1% in January.

Another closely watched indicator, average earnings, is expected to slow in February after strong increases in past three-months (Feb f/c 0.2% vs 0.3% in Jan).

Solid numbers from today’s jobs report is expected to generate further signals of economy strength and boost expectations for Fed’s more aggressive approach to interest rates in 2018.

Strong fall on Thursday weakened the structure and shifted near-term focus lower, as Thursday’s long bearish daily candle weighs and fresh bears pressure key near-term support at 1.2285 (top of thick daily cloud), as rising cloud strongly underpinned recovery rally from 1.2154 (01 Mar trough).

Bears may have difficulties to break into daily cloud which marks strong support and today’s close in relation to cloud would be the key signal for the near-term action.

Firm break into cloud would be bearish signal for extension of pullback from 1.2445 double-top, while stronger hesitation above cloud top would signal prolonged consolidation and possible stronger upticks.

Res: 1.2321, 1.2334, 1.2354, 1.2400

Sup: 1.2285, 1.2265, 1.2223, 1.2187

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

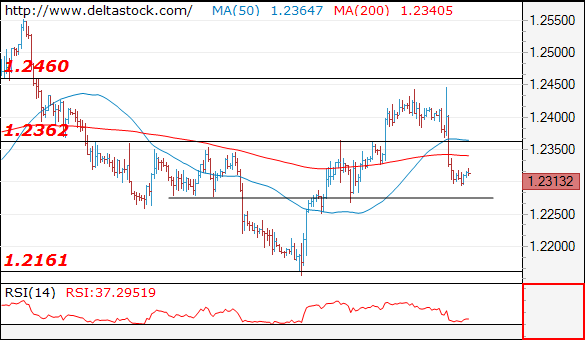

EUR/USD

Current level - 1.2313

Yesterday's consolidation above 1.2360 was followed by a brief rise to 1.2450, finalizing the whole rise since 1.2160 low. The outlook is bearish below 1.2360, for 1.2250, en route to 1.2160.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2360 | 1.2460 | 1.2250 | 1.2160 |

| 1.2460 | 1.2560 | 1.2160 | 1.2090 |

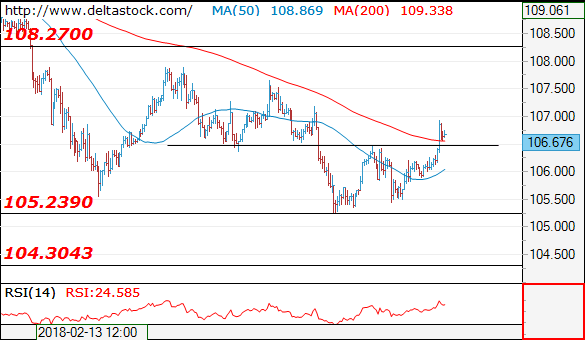

USD/JPY

Current level - 106.76

The violation of 106.50 resistance signals a positive bias, for 108.00 area. Crucial on the downside is 105.85 and initial support lies at 106.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.20 | 108.30 | 106.50 | 105.20 |

| 108.00 | 110.40 | 105.85 | 102.40 |

GBP/USD

Current level - 1.3799

Yesterday's slide shows a completion of the whole rise since 1.3710 low and the outlook is bearish, for 1.3620 major support area. Initial intraday resistance lies at 1.3850.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3850 | 1.4060 | 1.3710 | 1.3710 |

| 1.3930 | 1.4280 | 1.3710 | 1.3620 |

Historic Moment For US | Trump Answered Draghi’s Question | ECB’s Effect Continues

- Give Some Credit To Trump

- A New Tier Level of Friendship To Avoid US Tariff

- ECB's Effect Continues

Give Some Credit To Trump

Today is the day that investor may have to continue to praise Trump because his strategies have brought North Korea to the table for peaceful discussions and this by no means is a small event. Kim Jong-un, from North Korea, has invited Donald Trump, from the US, to meet him.

Trump may see and play this event as a victory. However, in reality there may be no change in North Korea's stance towards their nuclear program or abandoning their nuclear program. Nonetheless, his fiery statements have brought North Korea and the US to a historic moment which for traders, indicates less geopolitical uncertainty- at least for now.

Risk on trade is back in play as investors have reacted to North Korea and US peace talks and the gold price is under pressure- a pure risk of trade.

A New Tier Level of Friendship To Avoid US Tariff

Draghi raised a question yesterday by saying if Trump wants to put tariffs on his allies who are his friends? President Trump raised the bar today by suggesting a near tier of friendship which is called “real friends”. Both Mexico and Canada are exempt from the new tariffs which trump introduced. If new NAFTA agreement becomes a reality between US, Mexico and Canada, there is no need to introduce new tariffs. The reason is simple because in the new agreement Mr Trump has designed the deal which puts America first or what he calls a fair deal.

So, the idea behind this is that he wants to introduce similar agreement with other countries and exempt them from new tariffs. Regardless, market participants are paying close attention to this strategy and they want to see if Trump who is known in making the deals can develop something which may initially send a message of destruction but at the end, you have a deal which doesn't look so bad if you compare it to the worst case scenario.

ECB's Effect Continues

Currency traders are digesting the new development from the ECB under which the ECB dropped its pledge to continue to buy bonds if needed. The ECB has taken a remarkable step in their decision to close the liquidity tap this year because the bank sees no significant threat for economic crisis. The Euro has been over sold since yesterday as Draghi balanced his hawkish statement with dovish stance.

Sunrise Market Commentary

Markets

Yesterday, German bunds showed quite some sharp intraday swings. Yields jumped up to four basis points higher after the publication of the ECB policy statement. The ECB omitted its easing bias as it didn’t repeat its intention to increase bond buying if necessary. However, the rise in yields was reversed during the ECB press conference as ECB’s Draghi indicated that a big step to policy normalization was still quite some distance away. For an in depth analysis of the ECB decision . At the end of the day, German yields even declined between 1.6bp (2yr) and 2.7 bp (10-y). On the intra-EMU bond markets, yield spread chances versus Germany mostly narrowed slightly further with Greece (-6bp) outperforming and Italy (+6bp) underperforming. The swings in US Treasuries were much more modest. The US yield curve bear flattened with yields declining up to 2.8 bp at the long end of the curve. Today, global political developments will continue to have in important place in the headlines. However, global bond traders will turn their focus to the US payrolls. A solid report is again expected. January job growth is expected at 205 000. The unemployment rate is expected to decline to a cycle low of 4.0%. After last month’s rise & market reaction, wage growth data (expected at 0.2% M/M and 2.8% Y/Y from 2.9%) will take center stage. Of late, the rise in US yields took a breather. However, another positive surprise, especially from the wage data, will rekindle market expectations that the pace of Fed rate hikes might accelerate later this year.

Yesterday, the dollar initially gained modest ground against the euro and yen. The euro jumped temporary higher as the ECB dropped its indication that it could still raise the amount of asset purchases if needed. However, the euro strength was short-lived as president’s Draghj’s assessment at the press conference remained soft. In line with EMU yields, the euro reversed initial gains even closed the day substantially lower at 1.2312. Intra-day market reaction also suggests that markets were positioned long euro going into the ECB decision. USD/JPY closed the session little changed at 106.23 as markets still pondered the impact Turmp’s import tariffs. This morning, the BOJ as expected left its policy unchanged. A positive risk sentiment keeps USD/JPY better bid. Later today, the focus for USD trading will also shift to the US payrolls report. Yesterday’s price action in EUR/USD suggests that some further downside in the pair is possible in case of a good US payrolls report. The ECB indicating no substantial change in its policy communication anytime soon might also cap the topside of the euro overall. A break of EUR/USD 1.2155 is still need to improve the technical picture of the dollar against the euro.

Sterling trading was mostly driven by global factors. EUR/GBP mostly followed the intraday swings of the euro. In line with EUR/USD, the pair traded marginally lower on a daily basis. Today, the UK trade balance data, production and construction output will be published. We expect the data to be only of intraday significance. The broader euro moves might again be the driver for EUR/GBP trading.

News Headlines

U.S. President Trump agreed to meet North Korean leader Kim Jong Un. The announcement followed after South Korea's National Security Office head Chung Eui-yong told reporters at the White House that Kim had committed to denuclearisation and to suspending nuclear and missile tests. The meeting is expected to take place in May.

The BOJ keep its policy unchanged as expected, maintaining its commitment guiding short-term interest rates at minus 0.1 percent and the 10-year government bond yields around zero percent. “Japan's economy is expanding moderately, with a virtuous cycle from income to spending operating," the BOJ said in its policy statement.

Consumer inflation in China accelerated to 2.9% Y/Y in February, the highest since November 2013. Only a rise to 2.5% (from 1,5%) was expected. However, the sharp upswing was largely due to higher food prices related to the China Lunar New Year holidays. PPI inflation decelerated to 3.7% Y/Y from 4.3% Y/Y, the slowest pace in 15 months.

Markets Cheer As Donald Trump And Kim Jong Unextend Olive Branch

President Trump agreeing to meet the North Korean leader Kim Jong Unpleasantly surprised the markets on Thursday.Just a couple of months ago,the two leaders were in in a rather childish spat over whose nuclear button was bigger and hurled insults at each other, at every opportunity. Now, they are about to make history, not only with a possible reconciliation, but also because this would be the first ever meeting between a U.S. president and a North Korean leader. Investors are hopeful that there will finally be a diplomatic breakthrough.

Although relations between the U.S. and North Korea were not a major market concern, an improvementwill still boost appetite, particularly in South Korean stocks. The KOSPI is the best performing Asian stock index today rising as much as 2%, before easing to 1% higher.

The safe haven Yen declined early Friday, falling to its lowest level in a week against the U.S. dollar. As expected,Bank of Japan kept monetary policy unchanged, holding overnight interest rates at -0.1% and capping 10-year bond yields at about 0%.

Trump signs tariffs on steel and aluminum

Trump's tariffs are no longer just a threat, they'renow official. The President followed through on his promises yesterday,and signed two orders that implement tariffs on imported steel and aluminum. The good news was that Canada and Mexico were exempted.

Commodity prices fell in Asia with iron ore leading the losers and declining more than 5%. This has limited Asian stock appreciation as miners were dragged lower. But overall, most major indices are higher for the day.

If market participants feared a trade war, reactions would have been verydifferent to what we saw today. Commodity prices should have been sharply lower, investors would have sold their high yielding assets and run for the safety of treasuries, gold and the Yen. Given the limited market reaction to Trump's tariffs, investors seem to believe that Trump's actions won't drive a full-blown trade war. However, nothing should be taken for granted, and we will have to wait for the official response from the E.U. and China.

Draghi comments weigh on the Euro

Mario Draghi's wordshad a stronger impact than the ECB's statement, which finally dropped the line that talked about the possibility of increasing the asset purchase program, if the economic outlook deteriorated. The slightly hawkish ECB statement sent EURUSD to 1.2446, but the currency pair took a U-turn after Draghi started speaking.

Mr. Draghi said interest rates will remain at their present levels for an extended period of time and well past the horizon of net asset purchases, suggesting that interest rate differentials between the ECB and the Fed will remain high for a prolonged period of time. The ECB also lowered their 2019 inflation forecast and warned that underlying inflation remains subdued, which is another factor affecting the single currency.

It's NFP day

Traders will closely watch the U.S. non-farm payrolls reports. Although hiring is expected to have picked up slightly in February and employment to have declined to 4% from 4.1%, both of these figures will be ignored. Investors are mainly concerned about the average hourly earnings figure. After increasing at the fastest pace in almost a decade, wage growth is expected to fall 0.4% YoY. If this materializes, then previous inflation fears which caused the steep drop in equities beginning of February, arelikely to ease.

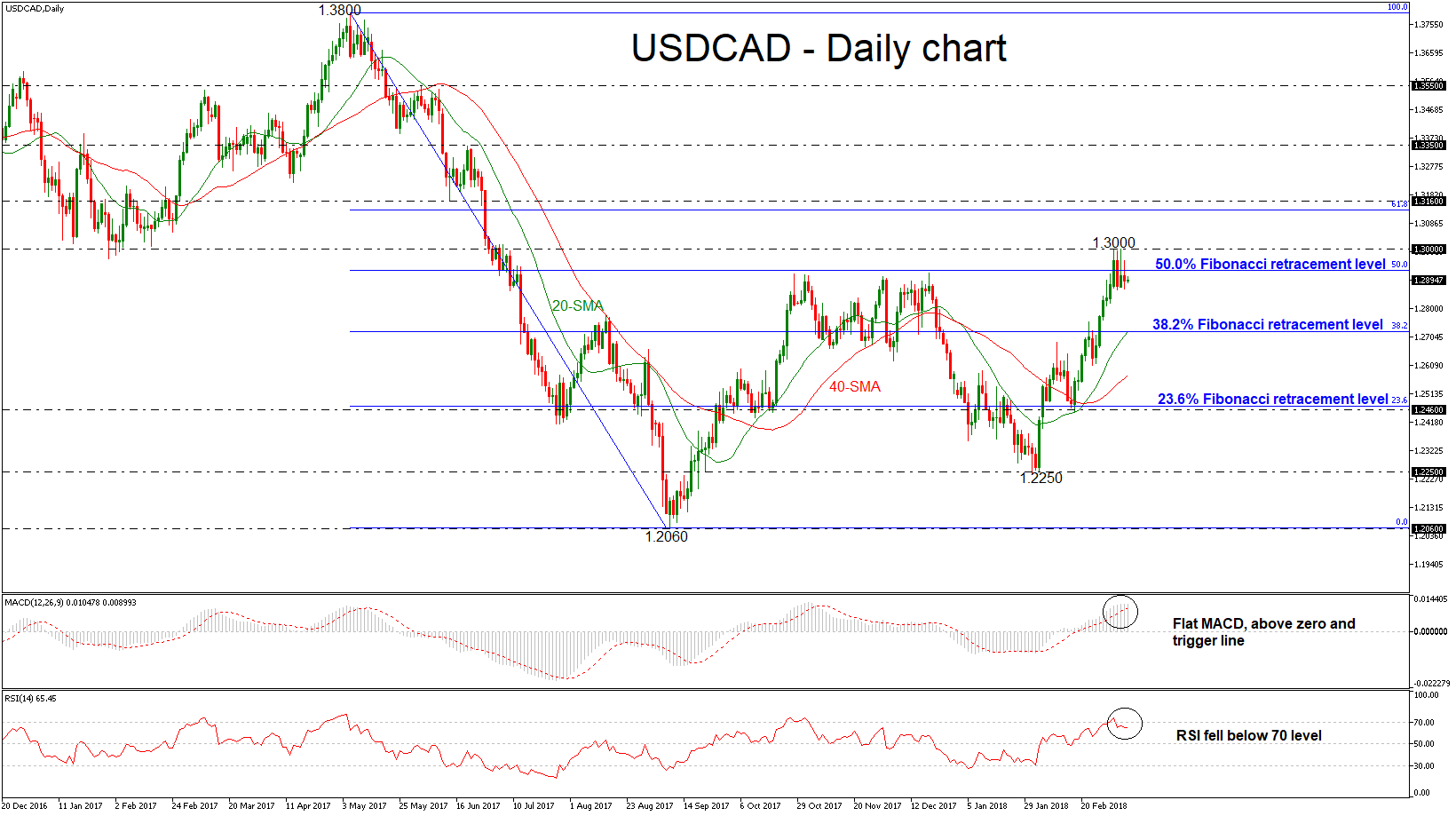

USDCAD Posts Eight-Month High Of 1.3000, Sideways Movement In Short Term

USDCAD is trading sideways after the aggressive buying interest that was created following the rebound on the 1.2250 support level. The pair hit an eight-month high near the 1.3000 critical psychological level and successfully surpassed the 50.0% Fibonacci retracement level at 1.2930 of the downleg from 1.3800 to 1.2060.

However, currently, the price action has slipped below the aforementioned obstacle and is holding near its opening level at 1.2890. The short-term technical indicators are endorsing the possible retracement on the price as the momentum is too weak to provide a sustained move higher.

In the daily timeframe, the MACD oscillator is holding in the positive territory but is moving sideways, while the RSI indicator dropped below the overbought area and is sloping to the downside. The indicators are suggesting that the latest upswing may be running out of steam and that the risk of a near-term correction is high. On the other hand, the 20 and 40 simple moving averages are continuing the upward movement.

If the price continues to extend its uptrend, this would mirror further improvements above the 1.3000 handle. The price could hit the 61.8% Fibonacci mark slightly below the 1.3160 resistance barrier. A jump above this area could open the door for the 1.3350 level.

On the flip side, if figures disappoint could create a bearish correction and hit the 38.2% Fibonacci mark, which overlaps with the 20-SMA near 1.2720. Moreover, a deeper move could shift the focus to the downside until the 1.2460 support barrier.

US Non-Farm Payrolls & Unemployment, UK Industrial Production And Canadian Unemployment

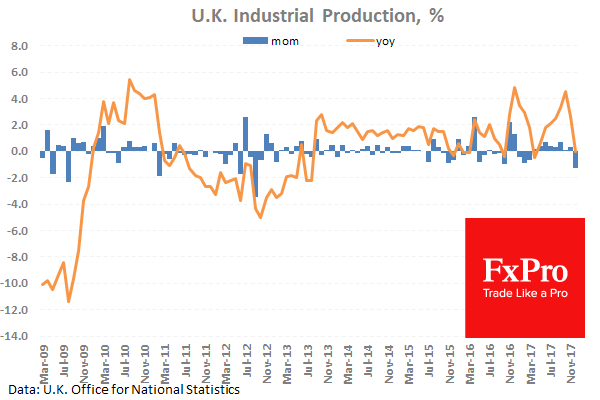

At 09:30 GMT, UK Industrial Production (YoY) (Jan) is expected to be 1.8% against a previous 0.0%. Manufacturing Production (MoM) (Jan) is expected to be 0.2% against 0.3% previously. This figure had been less volatile during much of 2017, with readings staying positive but close to zero. Industrial Production (MoM) (Jan) is expected to be 1.5% against -1.3% previously. Seasonally, there is generally a downturn in this figure with a drop into negative territory early in the New Year. Manufacturing Production (YoY) (Jan) is expected to be 2.8% against 1.4% previously. GBP pairs could move because of this data release.

At 13:00 GMT, UK NIESR GDP Estimate (3M) (Feb) is expected to be 0.3% against 0.5% prior. The data point has been moving closer to 0.0% since hitting a high of 1.0% in May 2014. However, it has managed to remain positive in that time, with an average of 0.4%. GBP pairs may experience price volatility from this data release.

At 13:00 GMT, UK NIESR GDP Estimate (3M) (Feb) is expected to be 0.3% against 0.5% prior. The data point has been moving closer to 0.0% since hitting a high of 1.0% in May 2014. However, it has managed to remain positive in that time, with an average of 0.4%. GBP pairs may experience price volatility from this data release.

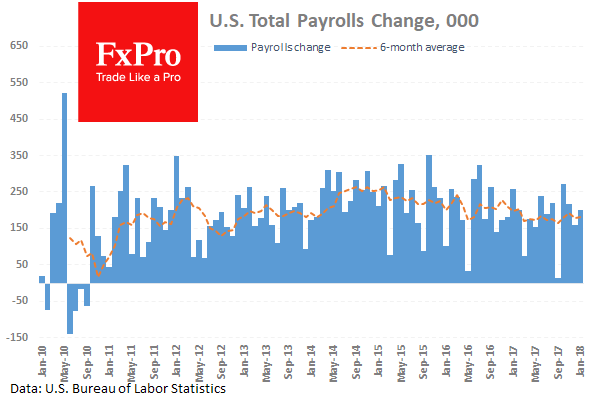

At 13:30 GMT, US Non-Farm Payrolls (Feb) is expected at 200K v a prior 200K. This measures the change in the number of employed people in February. The Unemployment Rate (Feb) is expected at 4.0% with a prior of 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during February. Average Hourly Earnings (YoY) (Feb) is expected to be 2.8% against 2.9% previously. Average Weekly Hours (Feb) is expected to be 34.4 against a previous 34.3. Labour Force Participation Rate (Feb) is expected to be 62.5% against a prior reading of 62.7%. It was this data release on the 2nd of February that resulted in the pullback in equity markets last month. At the time, the higher than expected wage data created concern about increased inflation and a responding rise in interest rates, resulting in a perfect storm with the market going risk-off. Any hint of rising wage inflation could see a repeat of events last month, especially given trade tariff tensions. USD crosses could experience volatility around these data releases.

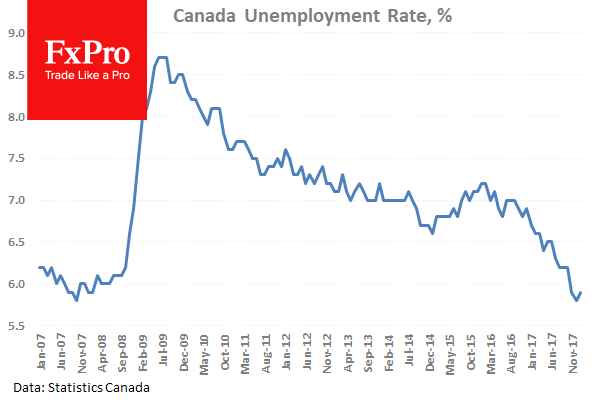

At 13:30 GMT, Canadian Unemployment Rate (Feb) is expected to be 5.9% against a previous 5.9%. Participation Rate (Jan) is expected to be 65.6% against 65.5% prior. Net Change in Employment (Dec) is expected to be 20.0K against a prior -88K. Unemployment had fallen to the lowest levels in ten years in November but ticked up slightly in December, with the large drop in the Net Change in Employment data, the largest fall since 2009. CAD pairs could see an increase in price movement from this data.

At 18.00 GMT, Baker Hughes US Oil Rig Counts will be released, with a headline number from last week of 800. WTI Oil could become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

In Europe, Industrial Production Is Due In Both Germany And The UK

Market movers today

The key event today will be the US employment report, where all focus will be on the wage growth component . The increase in hourly earnings jumped to 2.9% y/y in January from 2.7% y/y in December, stirring inflation fears and causing a jump in US yields. Today, we look for a small decline in hourly earnings to 2.8% y/y (consensus 2.9%), which would likely give a relief in markets and dampen the US inflation fears. The unemployment rate and payrolls will also be in focus. We look for an unchanged unemployment rate at 4.1% (consensus 4.0%) but broadly agree with consensus on payrolls to be around 200k.

The Fed's Evans (non-voter, dovish) is due to speak in a CNBC interview shortly after the employment report . This is one of the last chances ahead of the Fed's blackout period starting on Saturday.

In Europe , industrial production is due in both Germany and the UK.

In the Scandies, Norwegian CPI will be in focus. Sweden is due to release average house prices and household consumption data.

Selected market news

As expected, the ECB changed its forward guidance at ye sterday's meeting so it no longer entails the QE flexibility. President Mario Draghi struck a softish tone in the press conference, in particular as victory on inflation cannot be declared yet . Overall, our ECB view has not changed, as the meeting included little new guidance. Importantly, the decision yesterday was taken unanimously. In the updated staff projections, the near-term growth out look was strengthened but we still think the ECB's core inflation forecast remains too optimistic. For full details please see ECB Review: "Hawkish" action – softish language, 8 March.

In a surprising move, US President Trump has agreed to meet with North Korea's leader Kim Jong-un (first ever US president to meet with a North Korean l eader). While markets consider this mainly to be good news, as it may increase the likelihood of a diplomatic solution, we think this move is " high risk, high reward" in the sense that it also increases the risk that the situation could escalate if the summit collapses. The meeting should take place in May.

As expected, Trump made his decision to impose tariffs on steel and aluminium imports official yesterday, exempting Mexico and Canada for now due to the ongoing NAFTA renegotiations (other countries may be exempt as well). The EU and China have already said they will retaliate to any measures taken by the Trump administration. Trump's next move is likely to target China specifically. The Republican establishment also seems to support this, at least based on House Speaker Paul Ryan's statement yesterday . It remains our base case that future measures will also be limited in scope, but we believe trade policy will remain a market theme for some time. For more details on US trade policy, Research US: Symbolic protectionism with limited impact on growth and inflation but risks remain, 7 March 2018.

The Bank of Japan made no changes to monetary policy at its meeting overnight. While consensus among board members is still that inflation is moving towards 2%, Kataoka still thinks more easing is needed.