Sample Category Title

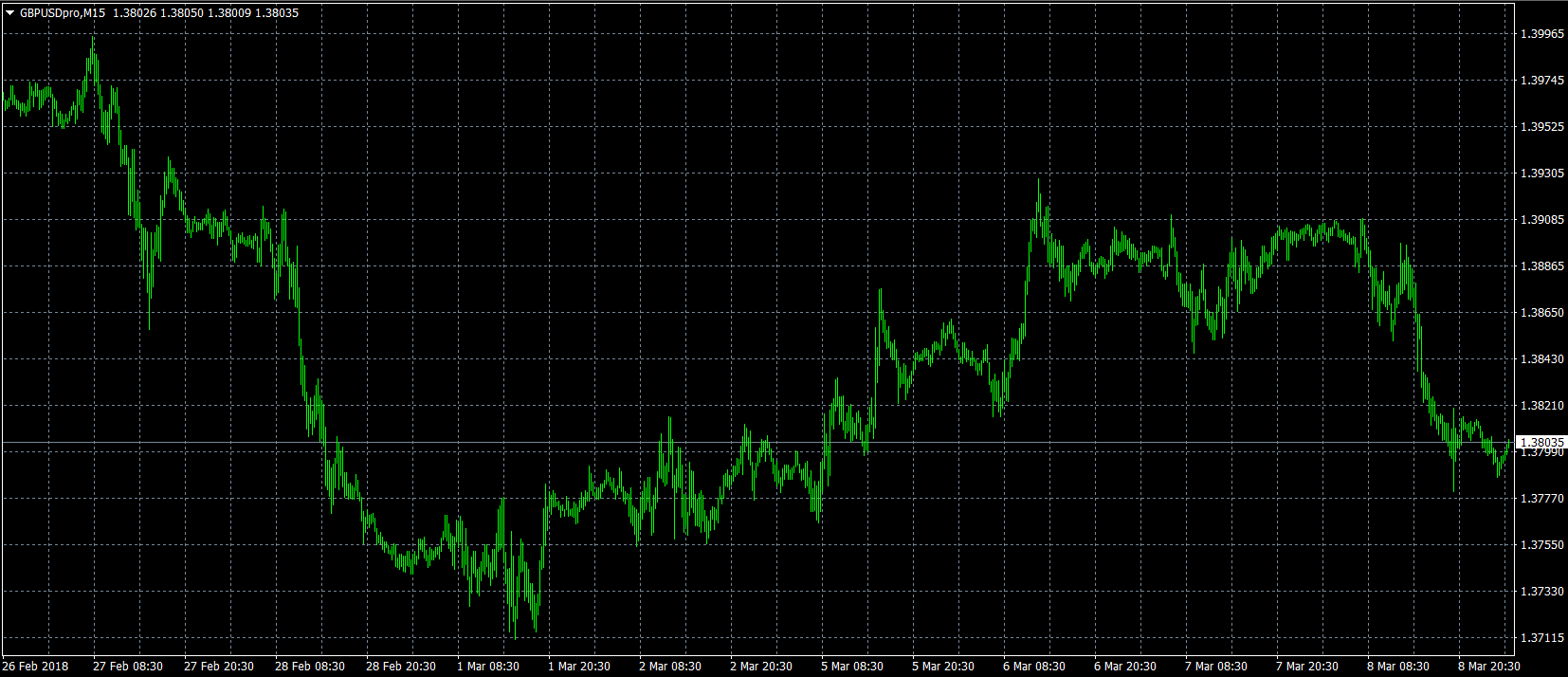

Pound Sellers Eye Key 1.3765 Support Level

The British pound has turned sharply lower against the U.S dollar, as Brexit frustrations and a dovish Mario Draghi sent sterling lower alongside the euro. The GBPUSD pair has quickly slumped back towards the 1.3800 region, after repeated price failures around the 1.3900 technical level. Moving into today’s European trading session, we see the release of key UK Manufacturing data, whilst sellers are increasingly looking to towards the key 1.3765 support level.

The GBPUSD pair is likely to decline further below the 1.3800 level, sellers will likely target the 1.3765 level with further support at 1.3714 and 1.3660.

If the GBPUSD pair can hold the 1.3800 support area, a technical test of the key 1.3837 and 1.3868 resistance levels seems likely.

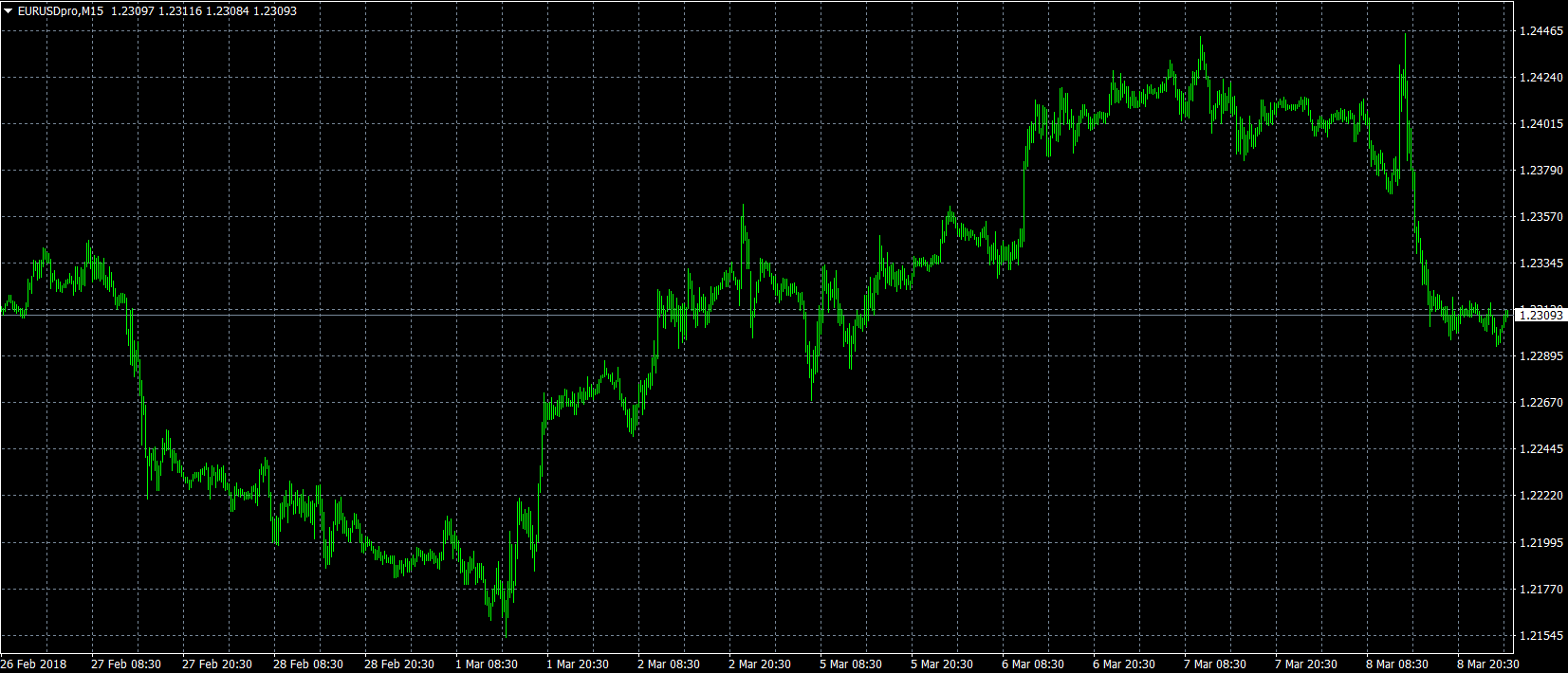

EURUSD Intraday Bearish Below 1.2358

The euro has moved lower against the U.S dollar, after European Central Bank President Mario Draghi issued a stark warning about potential Trade Tariffs from the U.S during yesterday’s ECB policy meeting. The EURUSD tumbled back towards the 1.2300 level, with the pair was strongly rejected from the 1.2400 handle again, following Draghi’s dovish comments. Price-action currently holds just above the 1.2300 level headed into the European trading session, with the 1.2278 level the next major downside support level to watch.

The EURUSD pair is intraday bearish whilst trading below the 1.2358 technical level, key intraday support is found at the 1.2178 and 1.2060 levels.

Should the EURUSD pair gain traction back above the 1.2358 level, price-action may correct towards the 1.2400 and 1.2430 levels.

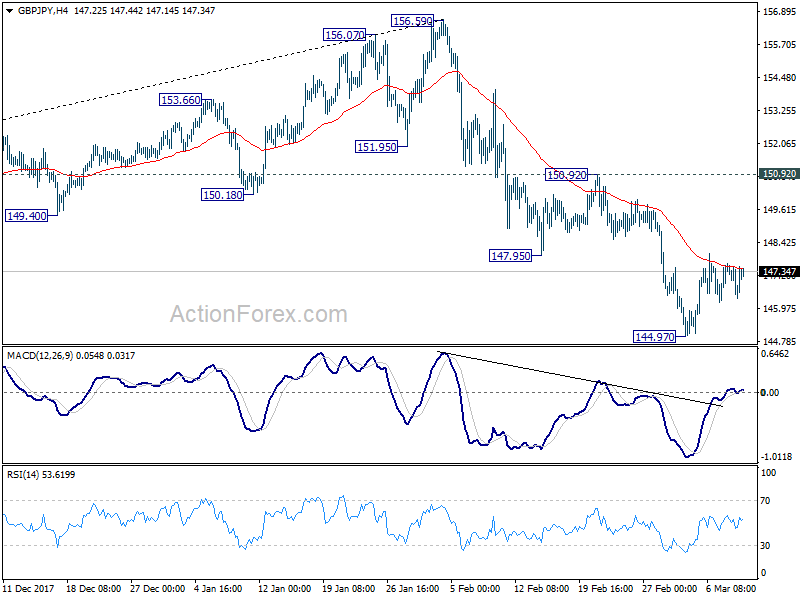

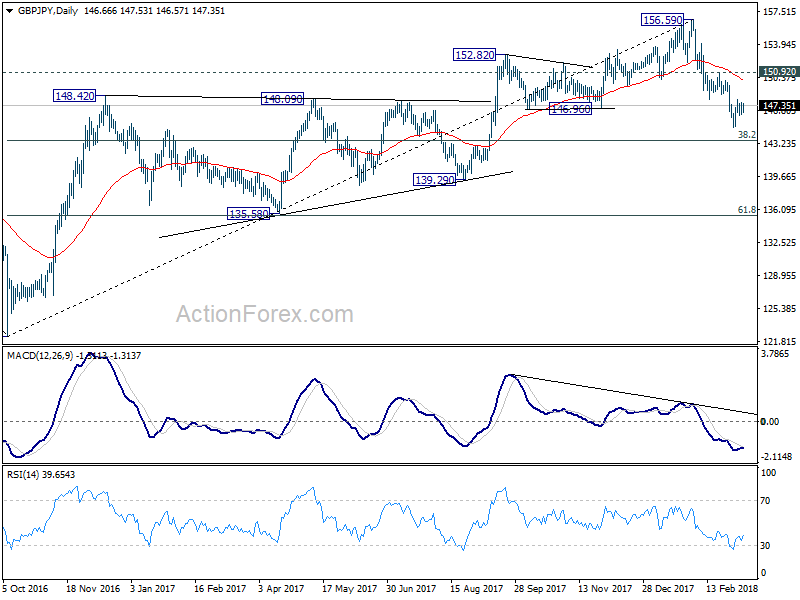

GBP/JPY Daily Outlook

Daily Pivots: (S1) 146.08; (P) 146.86; (R1) 147.47; More...

GBP/JPY is staying in consolidation from 144.97. Intraday bias remains neutral first. In case of stronger recovery, upside should be limited below 150.92 resistance and bring fall resumption. On the downside, break of 144.97 will extend the fall from 156.69 to 143.51 medium term fibonacci level next. We'll look for bottoming signal there. But firm break will target 139.29 support.

In the bigger picture, the case for medium term reversal continues to build up. There is bearish divergence condition in daily MACD. 146.96 support was taken out. And GBP/JPY was rejected by 55 month EMA. Break of 38.2% retracement of 122.36 to 156.59 at 143.51 will pave the way to 61.8% retracement at 135.43 and below. This will now be the preferred case as long as 150.92 resistance holds.

Nonfarm Payrolls Takes Centre Stage

US nonfarm payrolls will captivate the financial markets on Friday, giving investors what is arguably the most closely-watched calendar event of the month. The February report will provide the latest clues about the health of the world's largest economy and could impact everything form currencies to the bond markets.

Friday also features a deluge of economic reports from Europe, beginning at 07:00 GMT with a report on German industrial production and trade. Output in Europe's largest economy is forecast to rise 0.5% in January. Meanwhile, Berlin's trade surplus is projected to narrow slightly to €21.1 billion from €21.4 billion.

The United Kingdom will also release a spate of economic figures at 09:30 GMT, including industrial production, manufacturing production, trade and consumer inflation expectations. The report on trade is forecast to show a narrowing of the trade deficit to £12 billion from £13.57 billion.

The European Commission's statistical agency will report on euro-wide employment at 13:30 GMT.

Shifting gears to North America, the Department of Labor will release its monthly jobs report at 13:30 GMT. Nonfarm payrolls are projected to rise by 200,000 for February, following an identical increase the previous month. The jobless rate is also forecast to dip slightly to 4% from 4.1%.

Average hourly earnings, a proxy for wage inflation, are expected to climb 2.8% annually after shooting up 2.9% the month before.

Earlier this week, the ADP payrolls processor said US private-sector jobs rose by 235,000 last month, smashing estimates calling for 195,000.

North of the border, the Canadian government will also unveil its latest employment figures for February. Economists expect the report to show a net gain of 20,000 jobs last month.

In terms of monetary policy, the Federal Reserve's Eric Rosengren and Charles Evans are scheduled to deliver speeches at 17:45 GMT.

EUR/USD

Europe's common currency fell hard on Thursday after the European Central Bank (ECB) kept monetary policy unchanged. The EUR/USD exchange rate fell 100 pips to settle in the low 1.2300 region. The pair was last seen hovering around 1.2310, where it had broken two key support levels.

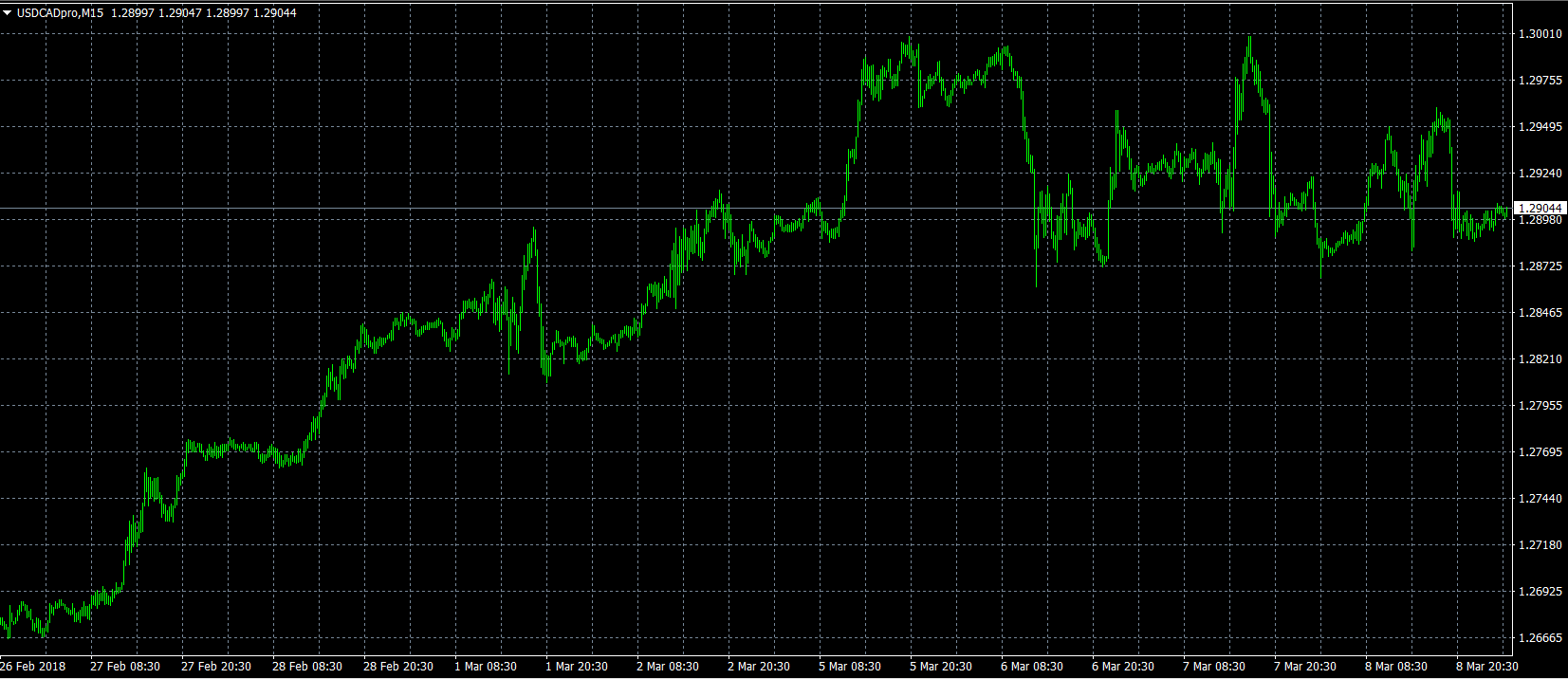

USD/CAD

USD/CAD

The USD/CAD made a strong push for 1.3000 this week before hitting a major psychological hurdle that sent prices back down to 1.2900. The pair was last seen trading at 1.2905. Jobs data from both sides of the border will have a strong influence on the direction of USD/CAD on Friday.

GBP/USD

Cable was under pressure on Thursday, as prices hit a double-bottom before recovering just north of 1.3800. The GBP/USD exchange rate was last seen trading at 1.3805, where it was down 0.1% from the previous close. Immediate support is located at 1.3712, which is the bottom from last week.

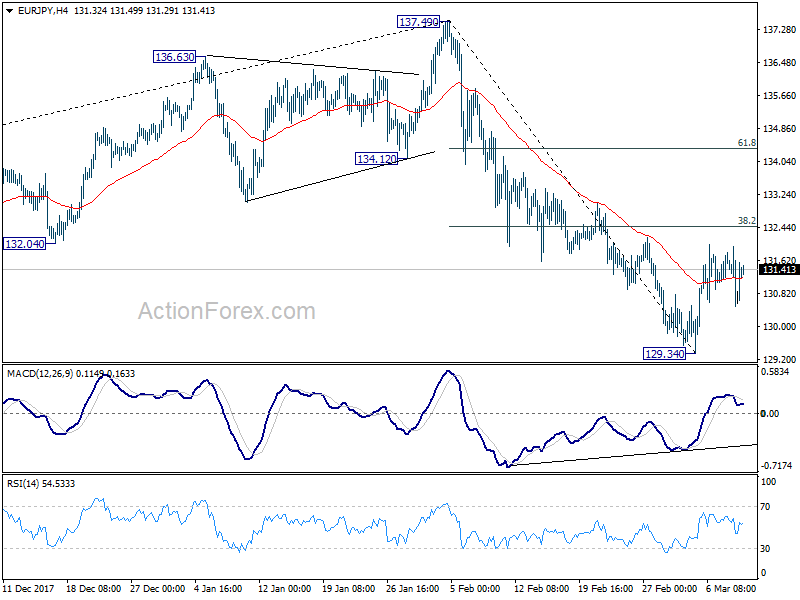

EUR/JPY Daily Outlook

Daily Pivots: (S1) 130.18; (P) 131.07; (R1) 131.64; More....

At this point, EUR/JPY's rebound from 129.34 short term bottom should still extend higher to 38.2% retracement of 137.49 to 129.34 at 132.45. We'd be cautious on strong resistance from there to limit upside. Break of 129.34 will resume the whole decline from 137.49 to 126.61 medium term fibonacci level. Nonetheless, sustained break of 132.45 will target 61.8% retracement at 134.37 first, before resuming the fall from 137.49.

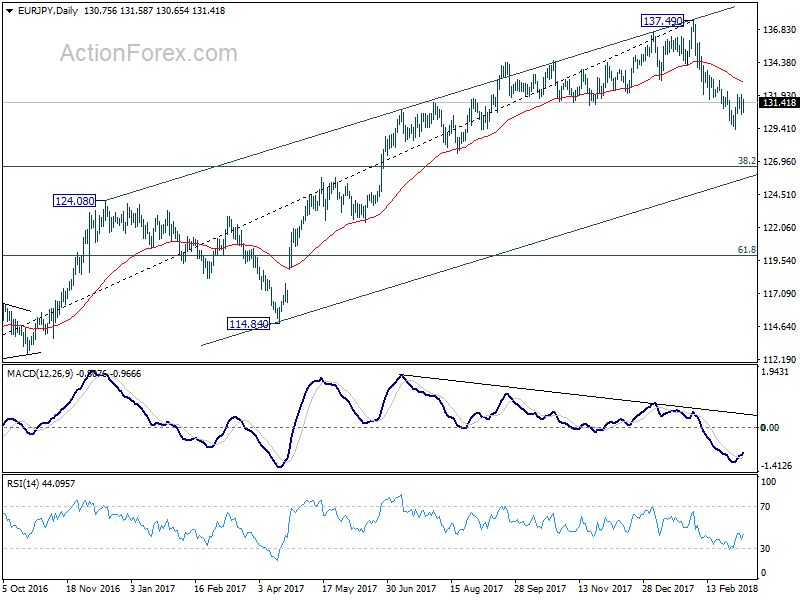

In the bigger picture, current development argues that rise from 109.03 has completed at 137.49, on bearish divergence condition in weekly MACD. Deeper fall should be seen to 38.2% retracement of 109.03 to 137.49 at 126.61 first. On the upside, break of 137.49 is needed to confirm medium term rise resumption. Otherwise, risk will now stay on the downside even in case of strong rebound.

Forex Analysis: Trump Signs Trade Tariffs As North Korea Suspends Missile Tests

Yesterday, US president Trump signed to formalise Steel and Aluminium Tariffs with notable exemptions for Canada and Mexico, subject to NAFTA progress. There were also hints that exemptions would be extended to key allies.

Tensions on the Korean Peninsula have eased of late, with North and South Korea sending a joint team to the recent Winter Olympics, which has led to bilateral talks this week. Significant progress has been made, with the North Korean Leader agreeing to suspend nuclear weapon and missile tests. South Korean NSA Chung has met with President Trump in the White House and there is talk that a meeting between the President and North Korean Leader Kim may take place before May 2018. USDJPY has reacted to the Korean developments and moved higher from 106.165 to a high of 106.939. For markets, the key data release today is the US Nonfarm Payrolls and Average Hourly Earnings at 13:30 GMT.

The Eurozone ECB Deposit Rate Decision was left on hold at -0.4%, unchanged from the previous reading. The ECB Interest Rate Decision was also released and left unchanged at 0%. EURUSD moved higher from 1.23758 to a high of 1.24457.

Canadian Housing Starts s.a. (YoY) (Feb) was 229.7K v an expected 216.6K, from 216.6K previously, which was revised down to 215.3K. This data shows an increase in the number of residential construction projects breaking ground and is the strongest reading for January and February since 2008. USDCAD fell to a low of 1.29032 before reaching a high of 1.29232 after the data release.

US Initial Jobless Claims (Mar 2) was 231K v an expected 220K, from 210K previously. Continuing Jobless Claims (Feb 23) was 1.870M v an expected 1.921M, from 1.931M previously, which was revised up to 1.934M. This data point had been holding steady around the 200 mark for much of 2017, with extremes at 300 above and 130 below over the course of the year. The data has remained above 100 since November of 2011, showing that the US jobs market is robust and performing steadily. On this occasion, the Jobless claims were higher than expected but the previous reading was the lowest in 48 years, suggesting an extremely tight labour market.

The ECB Press Conference and Monetary Policy Statement took place, with President Draghi making the following comments: Economic growth is set to expand by a faster pace than was earlier expected, underlying inflation is subdued and expected to hover around 1.5% for 2018. He said that the text that was removed from the Monetary Policy Statement must be taken into account and that the decision to remove it was unanimous. When asked about the US trade policy, he said he would not call recent exchanges on trade a war just yet. He said that policy continues to remain reactive rather than proactive and that global risks include deregulation. EURUSD sold off from a high of 1.24457 to a low of 1.23213 during and after his statements.

The Bank of Japan left Interest Rates on hold at -0.1% and maintained its 10-year JGB yield at 0.0%. The BOJ said that the Japanese economy is expanding moderately and it is keeping its assessment unchanged but is cutting its view on housing, with housing investment weaker.

EURUSD is up 0.06% overnight, trading around 1.23189.

USDJPY is up 0.50% in early session trading at around 106.724.

GBPUSD is unchanged this morning, trading around 1.38045.

Gold is down -0.22% in early morning trading at around $1,318.80.

WTI is down -0.22% this morning, trading around $60.18.

Elliott Wave Analysis: Copper At Risk Of Further Weaknesses

Copper (HG_F) broke below $3.5 low ($3.095) earlier today. As a result, it shows a bearish sequence from 2/16 peak ($3.272), risking for further downside. Current short term Elliott Wave view in Copper suggests that the rally to $3.272 on 2/16 ended Primary wave ((X)). The decline from there is unfolding as a double three Elliott Wave structure where Intermediate wave (W) ended at $3.0955 on 3/5 and Intermediate wave (X) ended at $3.178 on 3/6. Intermediate wave (Y) remains in progress, and while near term bounces stay below $3.178, Copper should see further downside.

Internal of Intermediate wave (W) unfolded as a zigzag Elliott Wave structure where Minor wave A of (W) ended at $3.164 on 2/21, Minor wave B of (W) ended at $3.243 on 2/23, and Minor wave C of (W) ended at $3.0955 on 3/5. A zigzag structure has a 5-3-5 subdivision and the chart is showing a nice 5 waves impulse Elliott Wave structure subdivision within Minor wave A and Minor wave C.

Intermediate wave (X) correction from $3.0955 low has a subdivision of a zigzag Elliott Wave structure. Minor wave A of (X) ended at $3.142, Minor wave B of (X) ended at $3.129, and Minor wave C of (X) ended at $3.179. Decline from $3.179 appears to be unfolding as a zigzag with first leg Minor wave A subdivided as 5 waves. Minute wave ((i)) of A ended at $3.1175, Minute wave ((ii)) of A ended at $3.1445, Minute wave ((iii)) of A ended at $3.0705, Minute wave ((iv)) of A ended at $3.087, and Minute wave ((v)) of A appears complete at 3.055. Minor wave B bounce is in progress to correct cycle from 3/6 high in 3, 7, or 11 swing. While Minor wave B bounce stays below $3.179, expect Copper to extend lower.

Copper 1 Hour Elliott Wave Chart

Market Update – Asian Session: US Payrolls And BoJ Gov Kuroda Press Conference In Focus

Headlines/Economic Data

Asian equities trade generally higher but pare gains

China Feb CPI rises at fastest pace since 2013; Government cites Lunar New Year impact

China Feb banking lending slows more than expected

PBoC officials discuss the merits of M2 in terms of monetary policy

PBoC Gov Zhou said the central bank is developing digital currency

Few surprises seen in BoJ policy statement

Markets now await upcoming BoJ Gov Kuroda press conference (prior was held at 6:30 GMT)

Upcoming release of US monthly payrolls and wage data also in focus

Australia/New Zealand

ASX 200 opened +0.1% closed +0.3%

ASX 200 Telecom Index +1.6%, Consumer Discretionary +1%, Financials +0.7%; Resources -1.8%, Energy -1.2%

(AU) Australia sells A$M v A$500M indicated in 3.25% April 2029 Bonds, avg yield 2.8212% v 2.6438% prior, bid to cover 4.36x v 3.8x prior

(NZ) RBNZ paper: natural rate of unemployment is estimated at about 5%

China/Hong Kong

Hang Seng opened +0.7%, Shanghai +0.1%

Shanghai Property index declines less than 1%

(CN) CHINA FEB CPI Y/Y: 2.9% V 2.5%E (highest reading since Dec 2013)

(CN) China: March CPI growth to be lower as holiday (Lunar New Year) factor fades.

(CN) China National Development and Reform Commission: sees 2018 China PPI growth at ~4% - Chinese press

(CN) CHINA FEB NEW YUAN LOANS (CNY): 839.3B V 900BE

(CN) CHINA FEB AGGREGATE FINANCING z(CNY): 1.17T V 1.07TE

(CN) CHINA FEB M2 MONEY SUPPLY Y/Y: 8.8% V 8.7%E; M1 MONEY SUPPLY M1 Y/Y: 8.5% V 11.0%E

(CN) PBoC comments on Feb lending data: Jan-Feb loan data should be read together due to the Lunar New Year holiday

(CN) PBoC Gov Zhou: Global economy shows recovery signs; to rely less on quantitative stimulus, may reduce reliance on money supply to boost growth

(CN) PBoC Dep Gov Yi: There is no quantitative target for China M2 in 2018

(CN) China PBoC Vice Gov Pan Gongsheng: FX reserves to be basically steady in future; mortgages have risen rapidly; reiterates monetary policy is neutral and appropriate

(CN) China Commerce Ministry (MOFCOM): Firmly opposes US trade measures, urges US to withdraw measures on steel and aluminum; to take 'strong' measures to safeguard own interest

(US) US Commerce Dept: Affirms preliminary determination on some China steel fittings; to impose 13.79% duties

(CN) China PBoC Open Market Operation (OMO): To skip OMO (5th straight session) v: Net drain CNY40B v CNY100B drain prior; For the week, PBoC drained net of CNY240B v net CNY120B injection w/w

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3451 v 6.3239 PRIOR

(CN) Shanghai Rebar Steel declines over 4.5%

(CN) China said to place curbs on OTC options trading by asset managers

Japan

Nikkei 225 opened +1.1%; closed +0.5%

(JP) Nikkei 225 March Futures and Options said to settle at ~21,575

(JP) BANK OF JAPAN (BOJ) LEAVES INTEREST RATE ON EXCESS RESERVES (IOER) UNCHANGED AT -0.10%; AS EXPECTED; Official Kataoka dissents for 5th straight meeting.

(JP) Japan Jan Labor Cash Earnings Y/Y: 0.7% v 0.7%e; Real Cash Earnings Y/Y: -0.9% v -0.7%e

(JP) Japan Feb Money Stock M2 Y/Y: 3.3% v 3.3%e; M3 Y/Y: 2.8% v 2.8%e

(JP) Japan Jan Overall Household Spending Y/Y: +2.0% v -1.0%e

(JP) Japan Finance Min Aso: US tariffs will disturb global steel and aluminum markets; to have 'big' effect on global economy; To work to get Japanese companies excluded from the tariffs; Will take necessary action in the WTO on the tariffs.

Mazda and Toyota Establish Joint-Venture Company "Mazda Toyota Manufacturing, U.S.A., Inc."; involves investment of $1.6B and expected to create up to 4K jobs by 2021, annual capacity seen at 300K units

Korea

Kospi opened +0.4%

(KR) South Korea Envoy Chung-Eui-Yong: North Korea to 'refrain further missile tests'; US President Trump and North Korea leader Kim Jong Un to meet by May

(KR) US White House: Confirms President Trump to accept invitation to meet with North Korea leader Kim; the time and place of meeting yet to be determined

Other Asia

Taiwan Semi [2330.TW]: Reports Feb Sales NT$64.6B -9.5% y/y

North America

US equity markets closed mostly higher: Dow +0.4%, S&P500 +0.5%, Nasdaq +0.4%, Russell 2000 -0.2%

S&P500 Consumer Staples +0.9%, Real Estate +0.8%

(US) Pres Trump: we need to show flexibility on tariffs to global friends; Confirms 25% tariff on foreign steel and 10% tariff on foreign aluminum; Canada and Mexico to be exempt while NAFTA talks go on; Open to modifying or removing tariffs for individual countries as long as we find way to ensure products no longer threaten security; US Trade Rep Lighthizer will be in charge of accepting offers from countries seeking exemptions - comments from White House

(US) Fed George (hawk): Reiterates important to continue gradual normalization of rates; Risks appear to be 'predominately' to upside

GoPro [GPRO]: Said to not receive 'serious' bid interest - NY Post

Europe

(UK) UK govt officials reportedly don't see reaching a Brexit deal until next year – press

(UK) Foreign Min Johnson: UK govt is prepared for a "no deal" Brexit scenario; No deal Brexit should not hold any terrors for UK because we'd 'do very well' under WTO rules

(EU) Internal ECB staff calculations assume final €30B of QE purchases in Q4; Sources say there is broad agreement among members of the Governing Council that QE should probably come stop by the end of 2018 – press

(EU) EU trade chief: to ask for clarity on tariff issue in days ahead; still believe EU should be exempt from US steel & aluminum tariffs

Levels as of 01:00ET

Hang Seng +1%; Shanghai Composite +0.3%; Kospi +0.9%

Equity Futures: S&P500 flat; Nasdaq100 flat, Dax flat; FTSE100 flat

EUR 1.2295-1.2320 ; JPY 106.16-106.96; AUD 0.7776-0.7796 ;NZD 0.7249-0.7275

Feb Gold -0.3% at $1.318/oz; Feb Crude Oil +0.3% at $60.24/brl; Mar Copper -0.1% at $3.074/lb

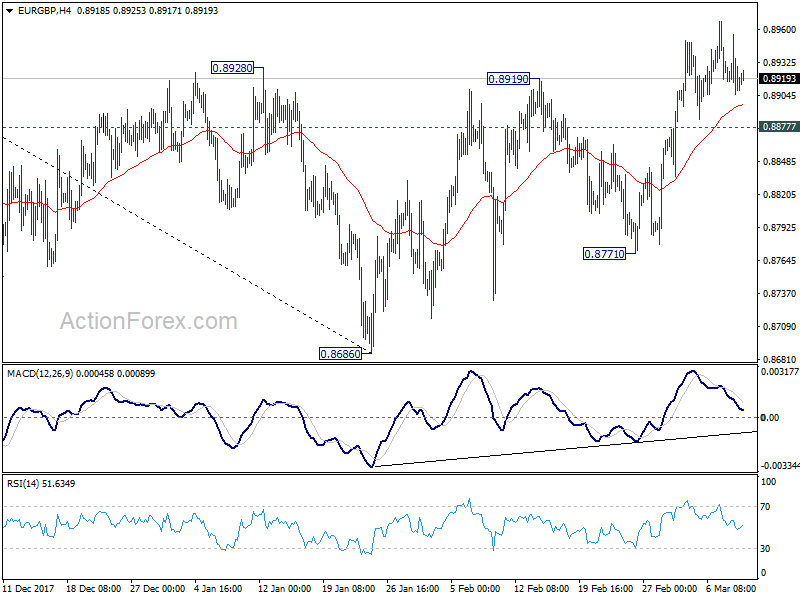

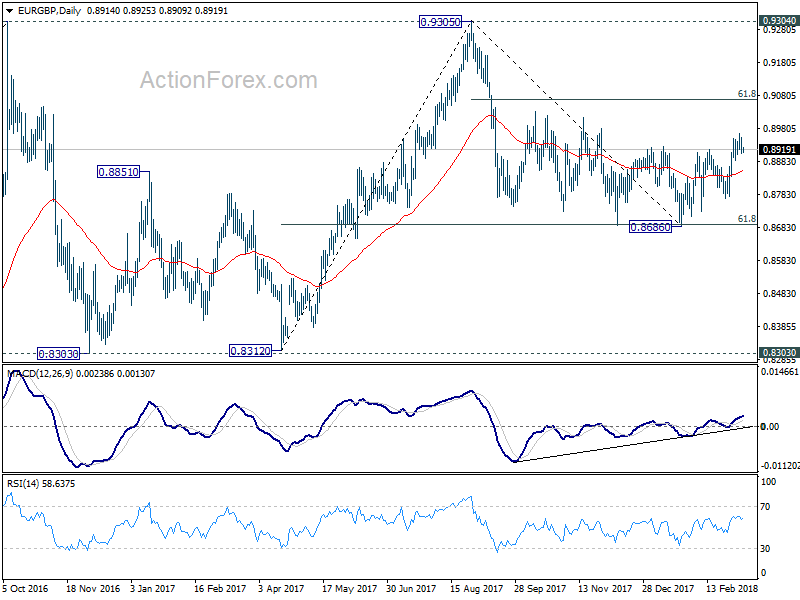

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8893; (P) 0.8925; (R1) 0.8943; More...

EUR/GBP continues to lose upside momentum, as seen in 4 hour MACD. Still, with 0.8877 minor support intact, further rise is expected. Prior break of 0.8928 resistance indicates near term trend reversal. Decline from 0.9305 has completed at 0.8686 after hitting 61.8% retracement of 0.8312 to 0.9305. Further rise should be seen back to 61.8% retracement of 0.9305 to 0.8686 at 0.9069. Firm break there will target retest of 0.9305 high. On the downside, below 0.8877 minor support will dampen this bullish view and target 0.8771 support instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

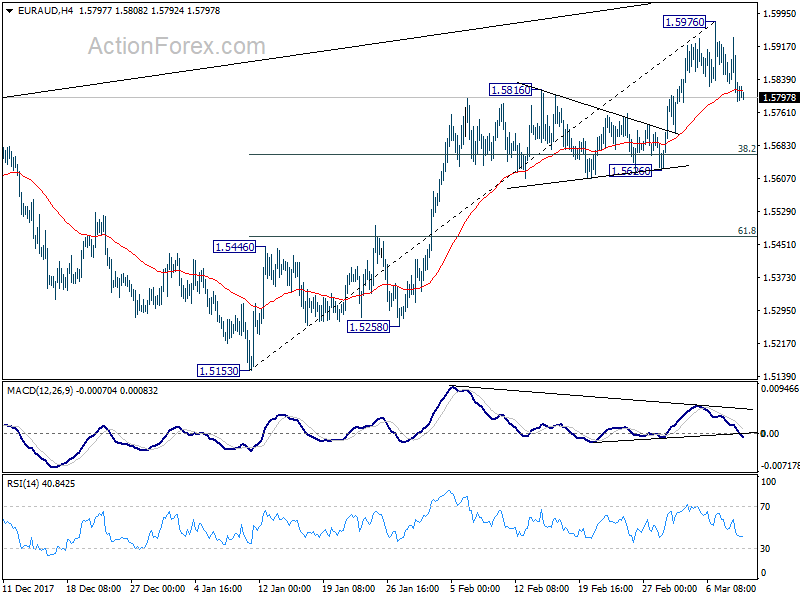

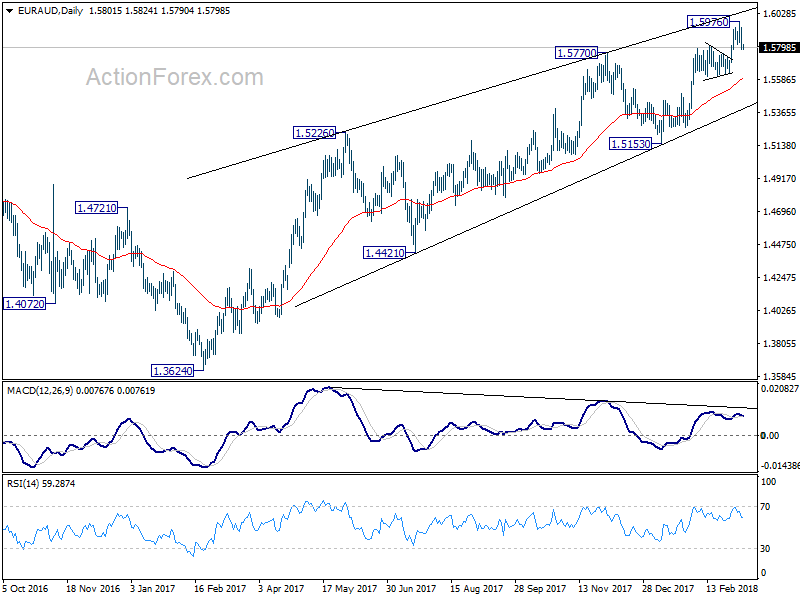

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5753; (P) 1.5846; (R1) 1.5904; More....

Break of 1.5823 minor support indicates short term topping at 1.5816, on bearish divergence condition in 4 hour MACD. Intraday bias is turned to the downside for pull back. At this point, we'd expects strong support from 1.5626 to contained downside to bring rebound. But break of 1.5976 is needed to confirm up trend resumption. Otherwise, more consolidation would be seen first.

In the bigger picture, medium term rise from 1.3624 is still in progress for 1.6587 key resistance. At this point, we'd be cautious on strong resistance from there to limit upside. But decisive break will confirm resumption of long term rise from 1.1602. On the downside, break of 1.5153 support is needed to indicate completion of the medium term rise. Otherwise, outlook will remain bullish in case of pull back.