Sample Category Title

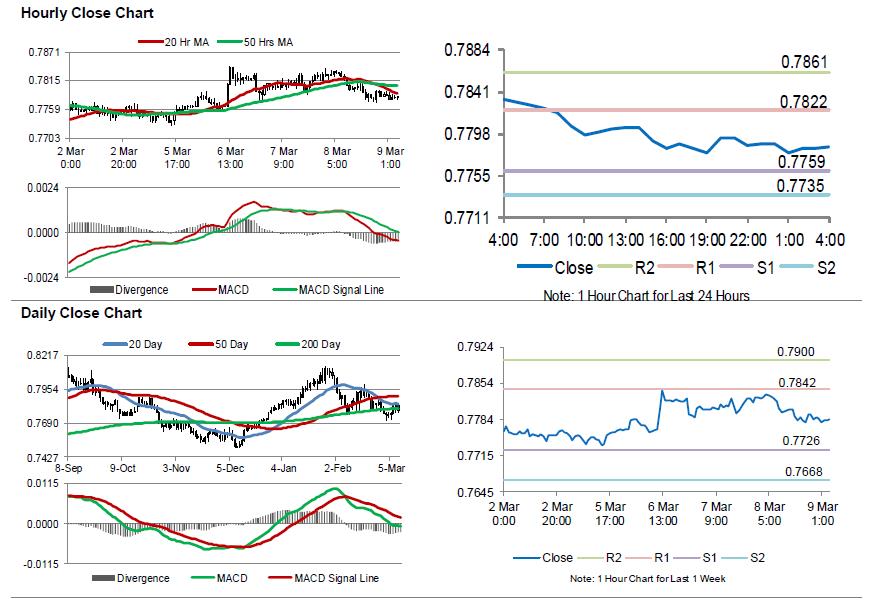

Aussie Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.49% against the USD and closed at 0.7788.

LME Copper prices declined 0.6% or $43.0/MT to $6830.0/MT. Aluminium prices declined 1.4% or $30.0/MT to $2082.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7784, with the AUD trading 0.1% lower against the USD from yesterday's close.

Earlier today, in China, Australia's largest trading partner, the consumer price index (CPI) grew 2.9% on an annual basis in February, beating market expectations for an advance of 2.5% and jumping to its strongest level since November 2013. The CPI had risen 1.5% in the prior month.

On the other hand, the nation's producer price index (PPI) climbed 3.7% on a yearly basis in February, rising at its weakest pace in 15 months and undershooting market consensus for a rise of 3.8%. In the prior month, the PPI had advanced 4.3%.

The pair is expected to find support at 0.7759, and a fall through could take it to the next support level of 0.7735. The pair is expected to find its first resistance at 0.7822, and a rise through could take it to the next resistance level of 0.7861.

Next week, traders would look forward to Australia's NAB business confidence, consumer inflation expectations and the Westpac consumer confidence index.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

ECB Kept Monetary Policy Unchanged, Dropped Its Promise To Extend Stimulus If Needed

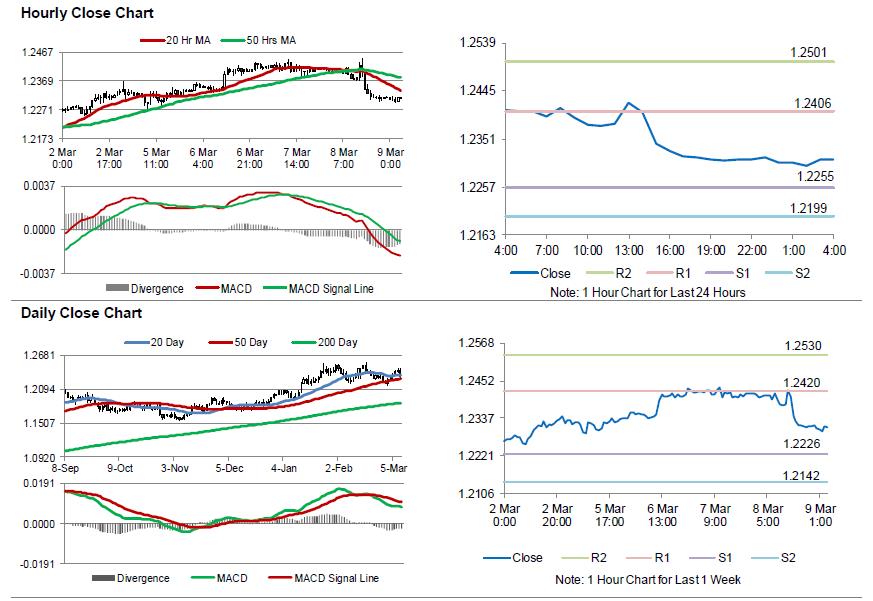

For the 24 hours to 23:00 GMT, the EUR declined 0.71% against the USD and closed at 1.2315, after the European Central Bank (ECB) Chief, Mario Draghi struck a cautious tone on inflation and signalled that monetary policy would remain accommodative until inflation is solidly back on track towards its 2.0% target.

The ECB, in a widely expected move, maintained the benchmark interest rates unchanged at a record low of 0.00% and continued its asset purchase programme at least until September 2018. In a post-meeting statement, the central bank dropped its pledge to boost its asset purchase programme if the Euro-zone's economic outlook worsens, thus highlighting its increasingly confidence over the region's growth outlook. Further, the central bank upgraded its economic growth forecast to 2.4% for this year, from an earlier prediction of 2.3%, while inflation was estimated to remain at 1.4% in 2018.

Separately, Germany's seasonally adjusted factory orders retreated 3.9% on a monthly basis in January, dropping to its lowest level since January 2017. Factory orders had registered a revised rise of 3.0% in the prior month, while market participants had estimated for a fall of 1.8%.

In the US, data revealed that first time claims for the US unemployment benefits rose to a 6-week high level of 231.0K in the week ended 03 March, after recording a 48-year low level of 210.0K in the prior week. Market participants had envisaged the initial jobless claims to rise to a level of 220.0K.

In the Asian session, at GMT0400, the pair is trading at 1.2310, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.2255, and a fall through could take it to the next support level of 1.2199. The pair is expected to find its first resistance at 1.2406, and a rise through could take it to the next resistance level of 1.2501.

Going ahead, investors would keep a close watch on Germany's trade balance and industrial production figures, both for January, slated to release in a few hours. Later today, market participants would focus on the crucial US non-farm payrolls, unemployment rate as well as average hourly earnings data, all for February, to gauge strength in the nation's labour market.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

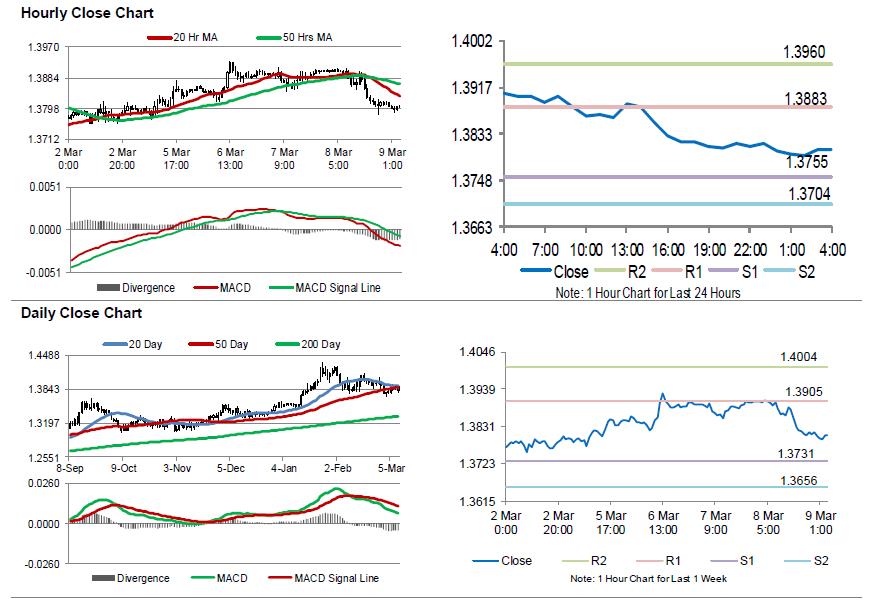

Pound Trading On A Weaker Footing, Ahead Of Key Economic Releases In The UK

For the 24 hours to 23:00 GMT, the GBP declined 0.63% against the USD and closed at 1.3814.

In the Asian session, at GMT0400, the pair is trading at 1.3805, with the GBP trading 0.07% lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3755, and a fall through could take it to the next support level of 1.3704. The pair is expected to find its first resistance at 1.3883, and a rise through could take it to the next resistance level of 1.3960.

Trading trend in the Pound today is expected to be determined by the release of UK’s total trade balance, industrial and manufacturing production data, all for January, slated to release in a few hours. Additionally, the nation’s NIESR GDP estimate for the three months to February, will also be on investors’ radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

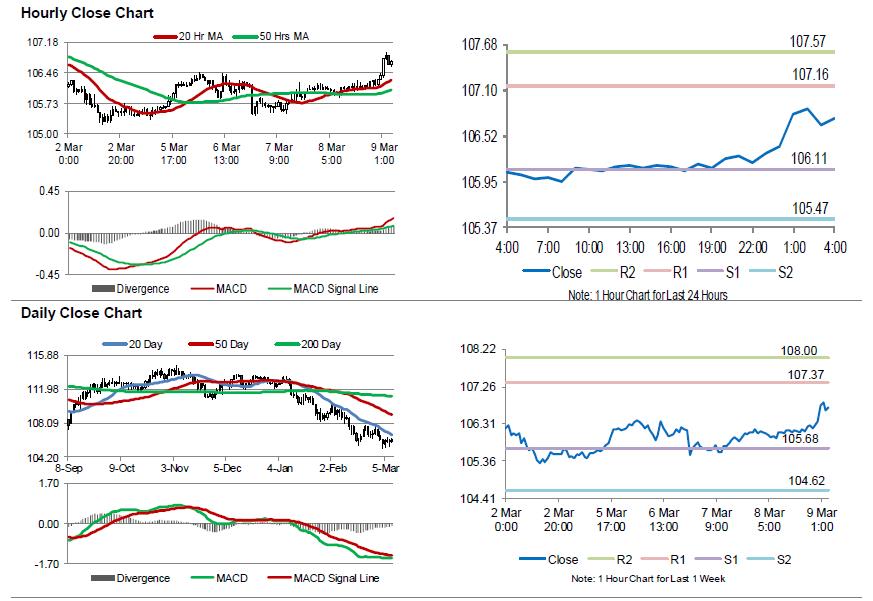

BoJ Held The Benchmark Interest Rate Steady At -0.1%

For the 24 hours to 23:00 GMT, the USD rose 0.2% against the JPY and closed at 106.30.

In the Asian session, at GMT0400, the pair is trading at 106.74, with the USD trading 0.41% higher against the JPY from yesterday’s close.

The Japanese Yen declined against the USD, amid increased risk appetite among investors, on the back of news that the North Korean leader, Kim Jong Un offered to stop nuclear tests and the US President, Donald Trump agreed to meet the North Korean leader by May 2018.

Earlier in the session, the Bank of Japan (BoJ), at its March monetary policy meeting, voted 8-1 to maintain the key interest rate unchanged at -0.1% and its target for 10-year Japanese government bond yields at around zero. Further, the central bank stuck to its upbeat view on the Japanese economy, signalling its conviction that a robust economic recovery will gradually fuel inflation towards its 2.0% target.

The pair is expected to find support at 106.11, and a fall through could take it to the next support level of 105.47. The pair is expected to find its first resistance at 107.16, and a rise through could take it to the next resistance level of 107.57.

Going ahead, investors would closely monitor the BoJ’s meeting minutes along with Japan’s final industrial production and the tertiary industry index, all due to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

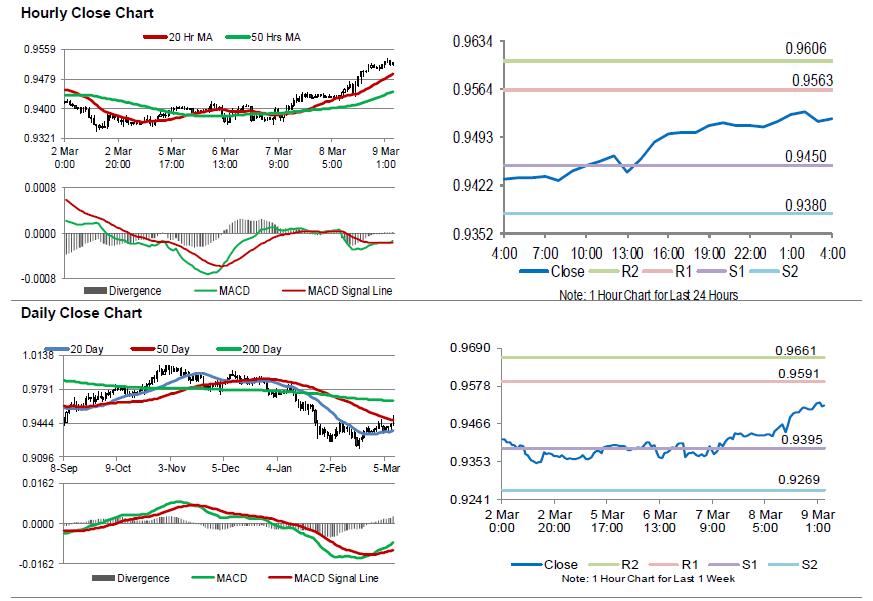

Swiss Unemployment Rate Fell As Expected In February

For the 24 hours to 23:00 GMT, the USD rose 0.8% against the CHF and closed at 0.9508.

In economic news, the seasonally adjusted unemployment rate in Switzerland dropped to 2.9% in February, in line with market expectations. In the prior month, the unemployment rate stood at 3.0%.

In the Asian session, at GMT0400, the pair is trading at 0.9521, with the USD trading 0.14% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9450, and a fall through could take it to the next support level of 0.9380. The pair is expected to find its first resistance at 0.9563, and a rise through could take it to the next resistance level of 0.9606.

Amid no macroeconomic releases in Switzerland today, traders would eye the Swiss National Bank’s interest rate decision, due next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

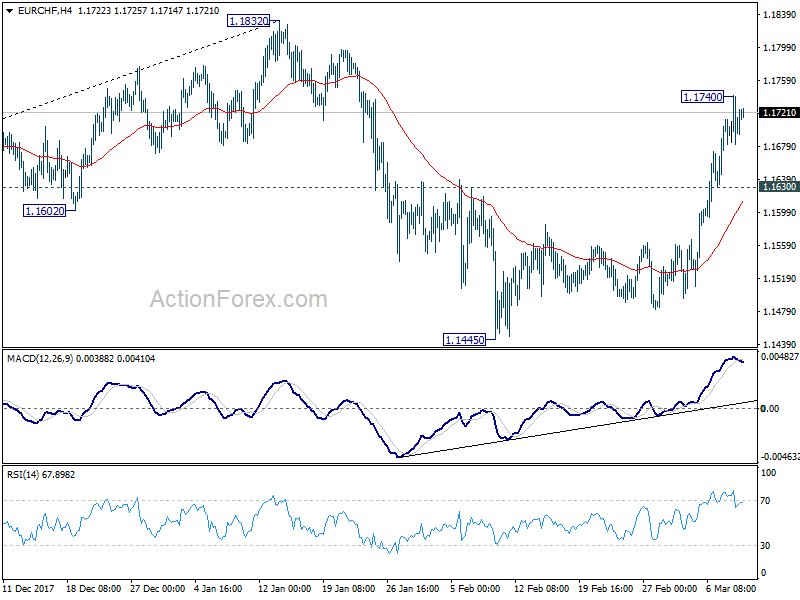

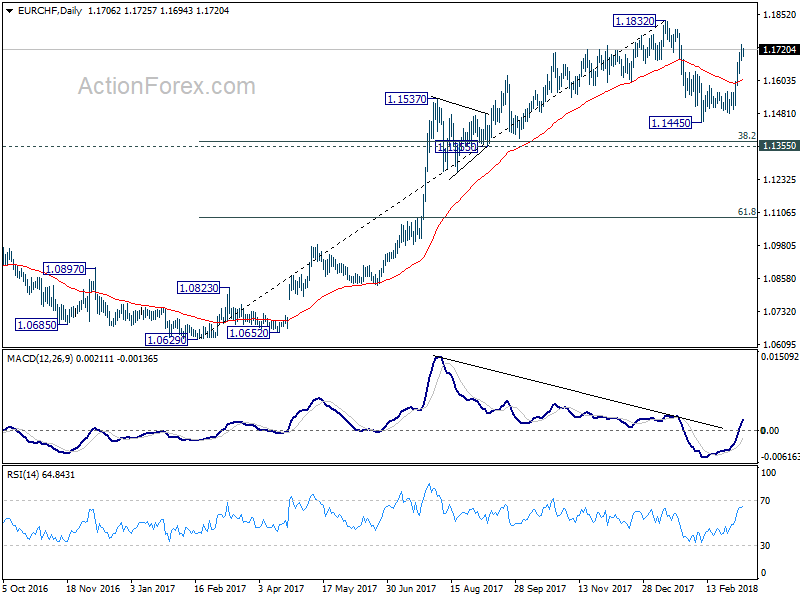

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1681; (P) 1.1710; (R1) 1.1739; More...

EUR/CHF lost some upside momentum after hitting 1.1740. But with 1.1630 minor support intact, further rise is still expected to retest 1.1832 high. At this point, we'll stay cautious strong resistance from there to bring another fall. Corrective pattern from 1.1832 might still have an attempt on 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372) before completion. On the downside, below 1.1630 minor support will target 1.1445 low again.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

Canada’s Housing Starts Surprised To The Upside In February, Building Permits Jumped To An 8-Month High In January

For the 24 hours to 23:00 GMT, the USD slightly rose against the CAD and closed at 1.2892.

Macroeconomic data showed that Canada's seasonally adjusted housing starts surprisingly climbed to a level of 229.7K in February, defying market expectations for a drop to a level of 215.0K, amid a sharp rise in construction of new buildings. In the prior month, housing starts had recorded a revised level of 215.3K. Moreover, the nation's building permits registered an unexpected rise of 5.6% on a monthly basis in January, posting the biggest increase in 8 months and confounding investor consensus for a fall of 1.5%. Building permits had recorded a revised rise of 2.5% in the prior month.

In the Asian session, at GMT0400, the pair is trading at 1.2903, with the USD trading 0.09% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2868, and a fall through could take it to the next support level of 1.2832. The pair is expected to find its first resistance at 1.295, and a rise through could take it to the next resistance level of 1.2996.

Ahead in the day, market participants would draw their attention to Canada's unemployment rate data for February.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Draghi’s Dovish Message Overrides End to ECB Easing Bias

- Draghi calls for 'patience', signalling ECB staying on side-lines

- New ECB projections suggest inflation to remain subdued

- Comments and projections mean markets ignore end to easing bias

- ECB no longer signalling willingness to step up Asset purchases

- ECB signals will calm markets in near term

- We still see stronger Euro area leading to higher policy rates in 2019

There was a small surprise from the ECB yesterday but markets paid more attention to a very clear message from Mario Draghi that any material change in the ECB's policy settings remains some significant distance away. As a result, a brief spike in the exchange rate of the Euro and in term interest rates that followed the ECB's initial policy announcement was more than reversed as Mr Draghi delivered a dovish update of ECB thinking.

The initial surprise came because the ECB opted to remove a commitment to increase the scale or duration of the Asset Purchase Programme in the event of a deterioration in economic or financial conditions. It was small because the improvement in Euro area performance effectively made this commitment redundant some time ago and the minutes of the January ECB policy meeting suggested some officials had mooted to remove it at that point.

It was still something of a surprise because it was felt that the recent step-up in protectionist rhetoric globally would lead the ECB to avoid any change in its signalling that might unsettle somewhat jittery markets. However, risks in this regard were effectively eased by the broadly dovish messaging from the press conference.

In practice, the market absorbed (or ignored) the removal of this 'easing bias' because Mr Draghi's comments and the ECB's new economic projections combined to send a very clear signal that conditions that might warrant tighter ECB policy are unlikely to materialise any time soon.

Mr Draghi again reiterated the need for 'patience' and 'persistence' to allow stronger economic activity and supportive monetary policy settings eventually translate into '..a sustained return of inflation rates towards levels that are below, but close to, 2% over the medium term'. Mr Draghi did acknowledge growing 'confidence' that the 'the strong and broad-based growth momentum in the euro area economy' will deliver such an outcome but the ECB's new projections suggest this will not be a speedy process.

Yesterday's new projections show only a marginal increase in the outlook for economic activity with 2018 GDP growth revised to 2.4% from 2.3%. Importantly, however, the outlook for 2019 and 2020 was not upgraded. So, the exceptional current momentum is seen easing progressively to healthy but not white hot rates of growth.

A somewhat cooler pace of expansion in coming years means that price pressures are projected to increase only slowly, thereby allowing the ECB considerable time to plot and implement a path to more 'normal' policy settings. The ECB's new projections actually entail a slight downward revision to headline inflation for 2019 to 1.4% from 1.5% previously.

While this revision isn't material and reflects a changed trajectory for energy costs rather than any more fundamental change of view (underlying inflation forecasts are unchanged from three months ago), the absence of any marked upward momentum-actual or projected- in Euro area inflation represents both a notable constraint on ECB policy as well as an indicator of current ECB thinking about the future path of policy as diagram 1 below illustrates.

In effect, the new ECB projections represent something approaching a 'goldilocks scenario' in that growth is healthy but not too hot whereas inflation is still cool but not deflationary cold. In these circumstances, the ECB likely feels the balance of risks in terms of a policy error would lie in the direction of a premature tightening either as directly as a result of ECB action (as happened in the historic past) or indirectly through market re-pricing that led to notably tighter financial conditions in the Euro area. As a result, the ECB likely feels a strong need to signal its intention to remain on the side-lines for some time to come.

Mr Draghi was asked a number of times about possible disruptions to the Euro area economy from growing concerns about the threat of trade wars. The ECB president suggested the immediate impact might be 'not too big' but he acknowledged the uncertainty that might follow from risks of tit-for-tat-retaliatory measures, possible effects on exchange rates and broader impacts on confidence.

While an increasing trend towards protectionism is undoubtedly a source of risk to the outlook, we don't think it was central to the dovish tone presented by Mr Draghi yesterday. Significantly, today's new ECB projections see prospects for global trade growth marked up appreciably for each of the three years 2018-2020. A more modest upgrade to Euro area exports may partly reflect the constraining influence of a stronger exchange rate.

We think that the ECB will be very pleased with the market's response to yesterday's pronouncements. The removal of the easing bias in relation to Asset purchases is a very small step but it is one in the direction of a normalisation of policy. Significantly, the ECB has negotiated this first step without the slightest hint of a 'taper tantrum'.

There is little expectation of any further step being taken for some time-most likely not until June or possibly even later as there is little expectation of a sudden stop to the Asset Purchase programme in September.

We think the momentum of growth may continue to surprise on the upside in the near term and some modest uptick in inflation could become evident by summer. Such developments would likely prompt a possibly significant re-evaluation of the current glide path for ECB policy and may turn focus to exactly when and how much policy rates could rise in 2019.

However, in the aftermath of yesterday's ECB meeting, that seems a very distant prospect and the expectation of extended ECB inaction is likely to be seen as a calming influence constraining the sort of moves in the Euro exchange rate and term interest rates that markedly stronger economic conditions in the Euro area would otherwise deliver.

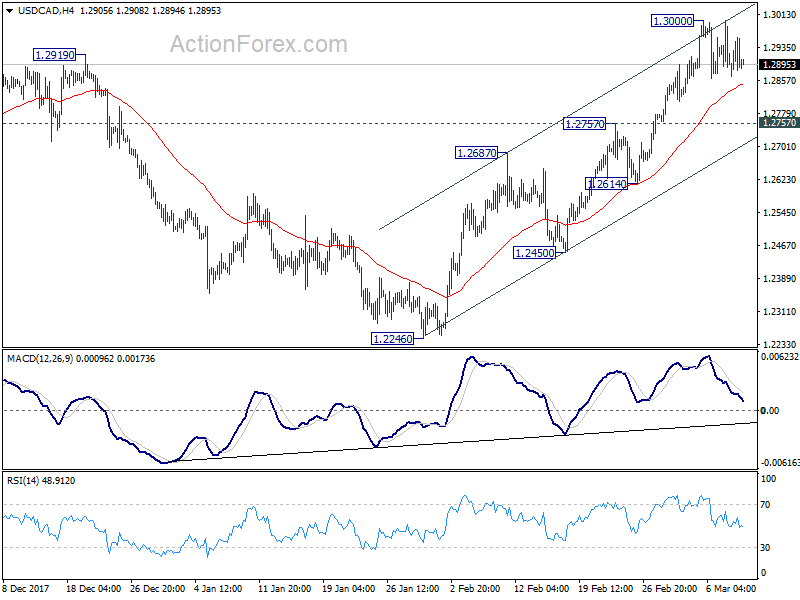

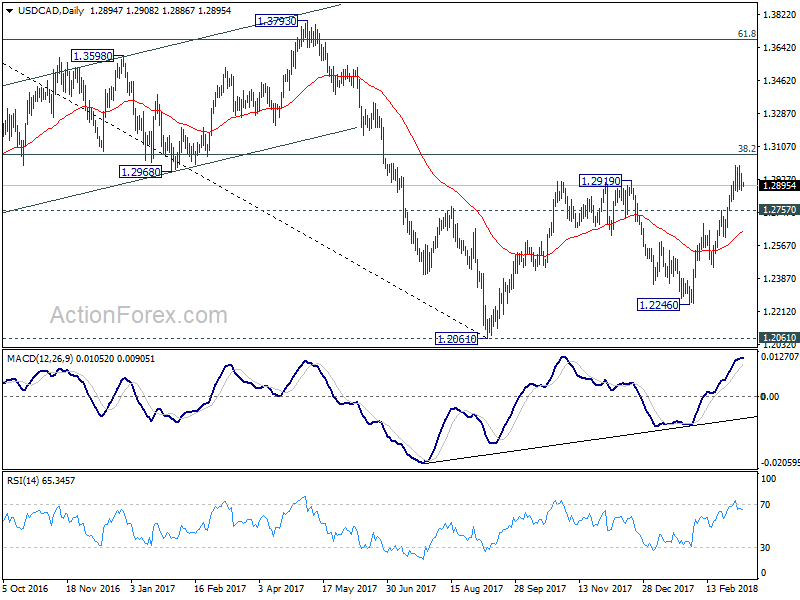

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2854; (P) 1.2908; (R1) 1.2949; More....

Intraday bias in USD/CAD remains neutral for consolidation below 1.3000 temporary top. Near term outlook remains bullish as long as 1.2757 resistance turned support holds. Another rise is still in favor. Above 1.3000 will extend the rise from 1.2246 to t 1.3065 fibonacci level next. However, firm break of 1.2757 will indicate reversal and turn outlook bearish for 1.2450 support.

In the bigger picture, strong break of 1.2919 resistance adds much credence to the bullish case. That is larger down trend from 1.4589 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

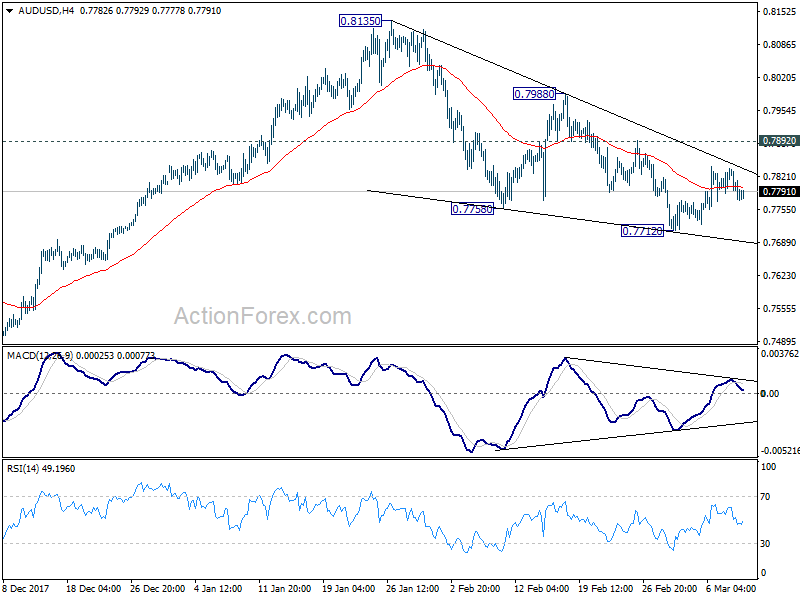

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7760; (P) 0.7799; (R1) 0.7825; More...

AUD/USD is still bounded in range above 0.7712 and intraday bias remains neutral. With 0.7892 minor resistance intact, near term outlook stays mildly bearish. On the downside, break of 0.7712 will extend the fall from 0.8135 towards 0.7500 key support level. However, break of 0.7892 will suggest that the pull back from 0.8135 is already completed. In such case, intraday bias will be turned back to the upside for 0.7988 and then 0.8135 again.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.