Sample Category Title

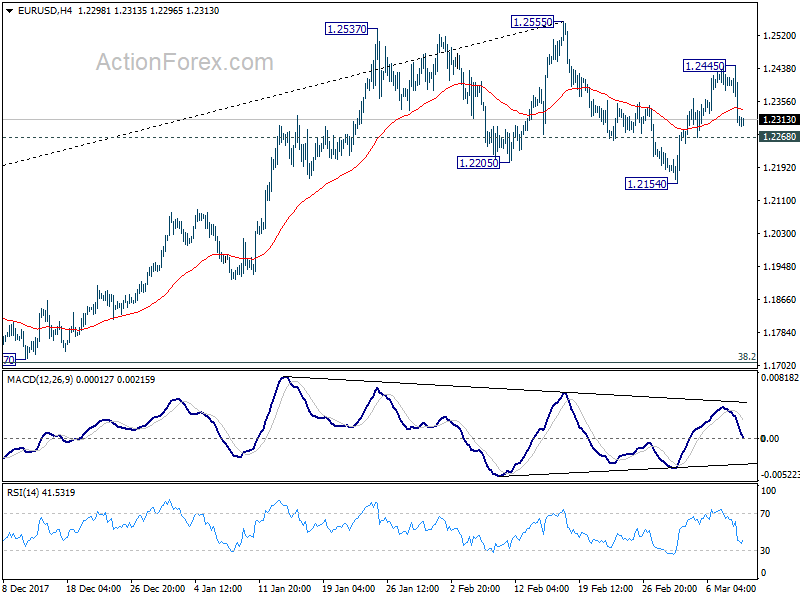

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2257; (P) 1.2351 (R1) 1.2406; More....

EUR/USD dropped sharply from 1.2445 but it's staying above 1.2268 minor support so far. Intraday bias remains neutral first. On the downside, break of 1.2268 will argue that fall from 1.2555 is likely resuming. And intraday bias will be turned back to the downside for 1.2154 support and below. ON the upside, above 1.24455 will turn bias to the upside for retesting 1.2555 key resistance.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

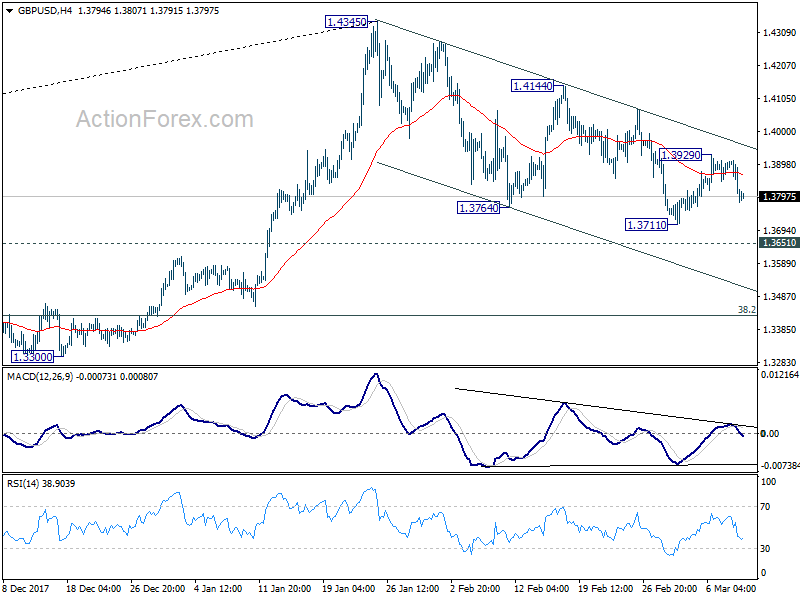

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3757; (P) 1.3833; (R1) 1.3888; More....

GBP/USD drops sharply after recovery from 1.3711 ended at 1.3929. But it's staying above 1.3711 temporary low. Intraday bias remains neutral first. Fall from 1.4345 is in favor to extend and break of 1.3711 will target 1.3651 resistance turned support and below. At this point, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

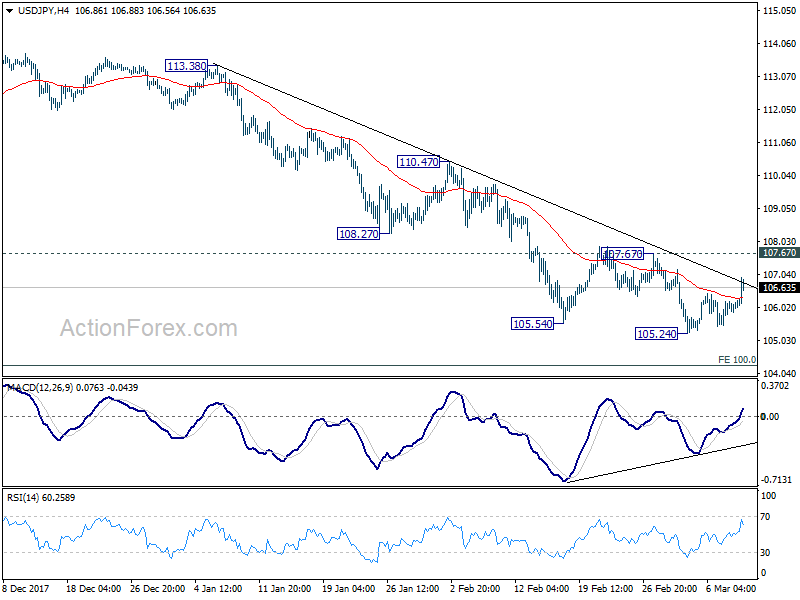

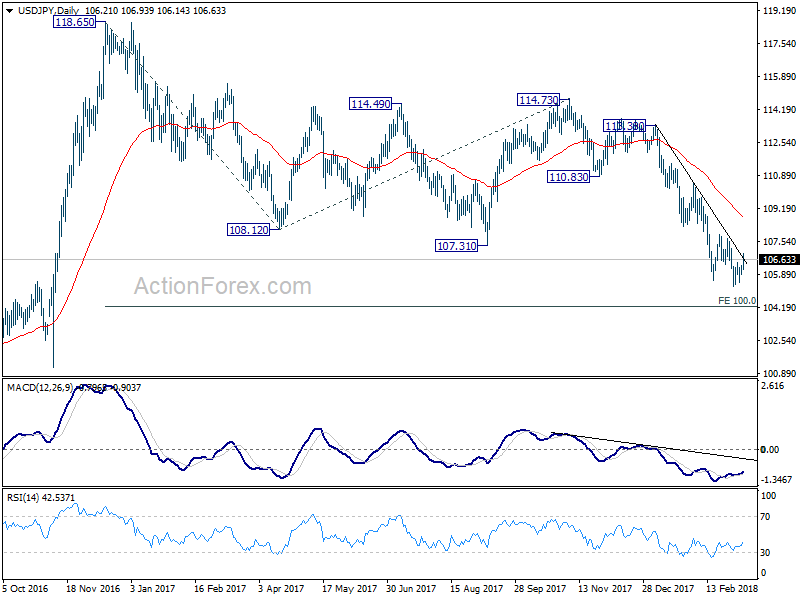

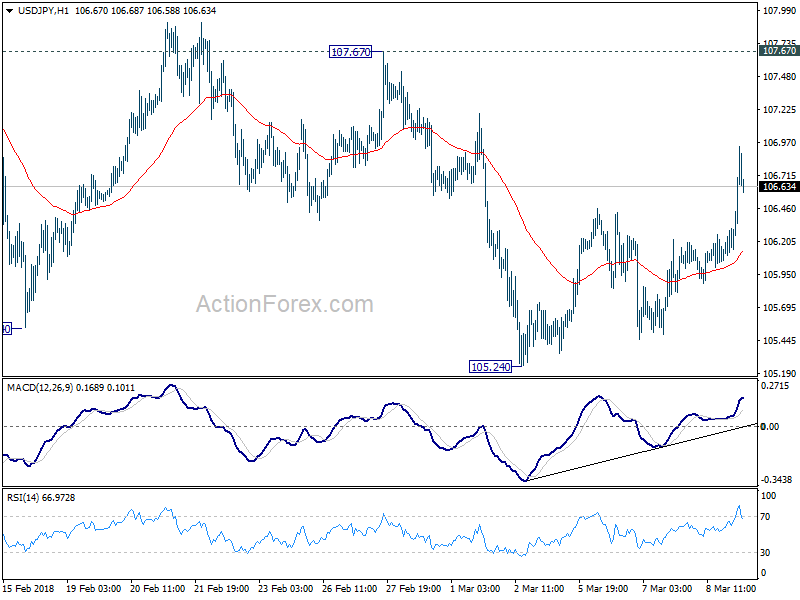

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.95; (P) 106.13; (R1) 106.37; More...

USD/JPY's rebound from 105.24 extends to as high as 106.93 so far. But it's still limited below 107.67 resistance. Intraday bias remains neutral first. Considering bullish convergence condition in 4 hour MACD, decisive break 107/67 will indicate near term reversal. In such case, outlook will be turned bullish for 110.47 resistance next. But before that, another decline is still mildly in favor. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

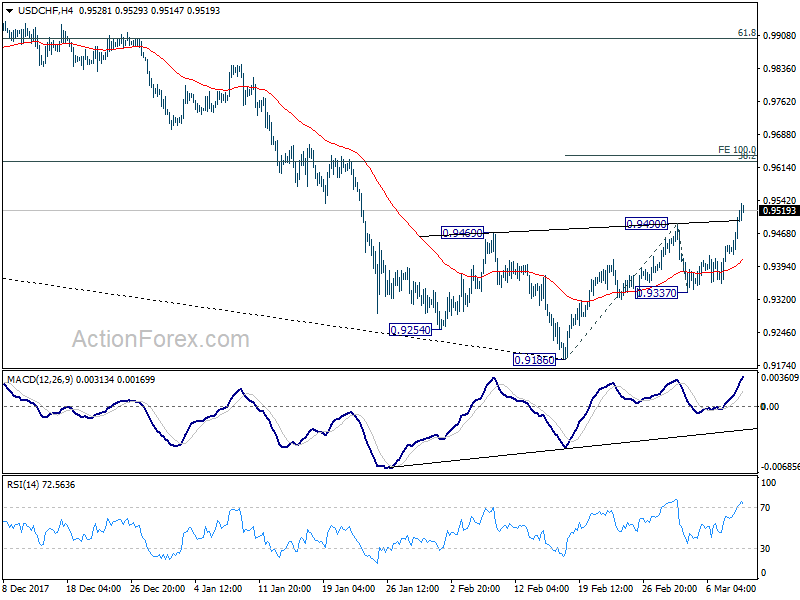

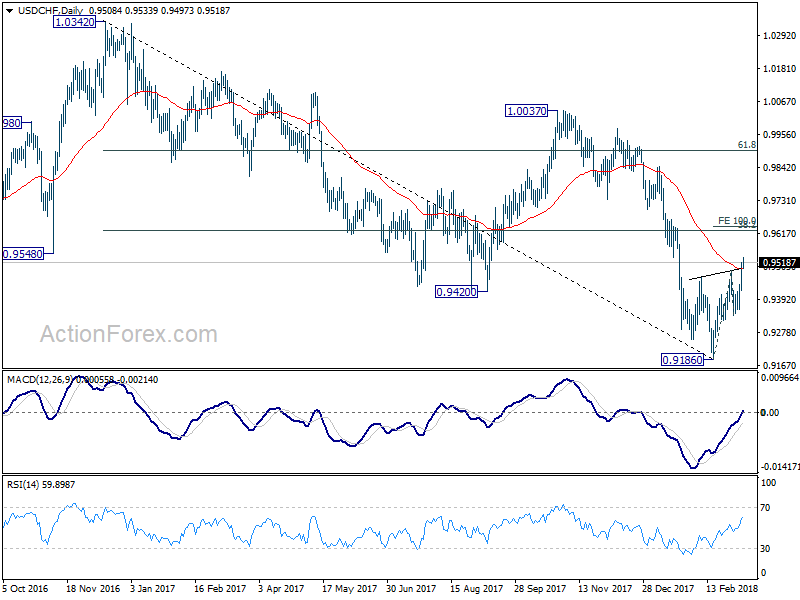

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9448; (P) 0.9484; (R1) 0.9546; More...

USD/CHF's rebound from 0.9186 accelerates to as high as 0.9533 so far today. The strong break of 0.9490 resistance indicates near term reversal. This is supported by bullish convergence condition in 4 hour MACD. Also, there is a head and shoulder bottom pattern (ls: 0.9254, h: 0.9186, rs: 0.9337). Intraday bias is now on the upside for 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9641 first. On the downside, break of 0.9337 minor support is needed to indicate completion of the rebound. Otherwise, near term outlook will be cautiously bullish even in case of retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Dollar Survived Event Risks, Strong as Focus Turns to Non-Farm Payrolls

The greenback emerged as a winner after most of the the event risks this week and is staying firm in Asian session. In particular, Euro's selloff after just slightly less dovish than expected ECB provides much support to the Dollar. And the greenback paid little reaction while US President Donald Trump finally signed the tariff proclamation. US equities ended slightly higher overnight with DOW gaining 0.38%, but still kept below 25000 key handle. Nikkei follows and is trading up 0.8% at the time of writing, unbothered by BoJ rate decisions. The greenback will have look towards the final hurdle of the week, the non-farm payroll report.

Technically, yesterday's rebound in the dollar index carries some significance. It argues that the pull back from last week's high at 90.93 to 89.40 is a corrective move, and has completed. The immediately focus will be back to 91.01 key medium term resistance. As the index is defending long term fibonacci level of 50% retracement of 72.69 to 103.82 at 82.55, firm break of 91.01 will be a strong sign of trend reversal.

Trump signed tariff proclamation, but backed down from no exemption stance

Trump signed tariff proclamation, but backed down from no exemption stance

Trump finally signed the proclamations of 25% steel and 10% aluminum tariff yesterday. The new tariffs will take effect in 15 days. He said in the White House, surrounded by steel and aluminum workers, that "we have to protect and build our steel and aluminum industries, while at the same time showing great flexibility and cooperation toward those that are really friends of ours,"

But he backed down from his original position of no exemption. As Canada and Mexico are exempted, pending NAFTA negotiations outcome. And he opened the door for reduction in tariffs for countries that "treat us fairly".

Trump added "I'll have a right to go up or down, depending on the country, and I'll have a right to drop out countries or add countries." And, "we just want fairness. Because we have not been treated fairly by other countries."

North Korea Kim to meet Trump on denuclearization

Separately, Trump agreed to meet with North Korean leader Kim Jong-un for nuclear talks. The news came after South Korean National Security Council chief Chung Eui-yong said Kim "expressed his eagerness to meet President Trump as soon as possible". White House spokeswoman Sarah Huckabee Sanders said the meeting will be at "a place and time to be determined."

Trump also tweeted "Kim Jong Un talked about denuclearization with the South Korean Representatives, not just a freeze," "also, no missile testing by North Korea during this period of time. Great progress being made but sanctions will remain until an agreement is reached. Meeting being planned!"

Kansas City Fed George: Risks predominately to the upside

Kansas City Fed President Esther George said "risks to the outlook appear to be predominately to the upside." And she urged that Fed should "carefully calibrate its policy to lean against a potential buildup of inflationary pressure or financial market imbalances."The "predominately to the upside" description is in-line with her hawkishness. Other members generally see risks to be "roughly balanced".

Draghi downplayed implication of easing bias removal

Surprising to most market participants, ECB dropped the easing bias in the forward guidance. While this had initially sent the euro slightly higher, it reversed as President Mario Draghi reinforced that the act was 'backward looking' and would not affect future monetary decision making. Policymakers remained confident over the growth outlook but again raised concern over weak inflation. As such, the updated economic projections saw upgrades in the growth but downgrades on inflation outlook. Going forward, the focus is on the tapering process of ECB's asset purchases which stay at a monthly pace of 30B euro. Meanwhile, ECB's forward guidance would gradually focus more on the interest rate path, and its relations with inflation. More in ECB Surprisingly Removed Easing Bias, Draghi Downplayed The Implication On Future Policy.

EC Tusk on Brexit: Ireland first and no financial services in the deal

European Council President Donald Tusk emphasized that the Irish border issue is a top priority in Brexit negotiation. He said that "if in London someone assumes that the negotiations will deal with other issues first, before moving to the Irish issue, my response would be: Ireland first." And he warned that "as long as the UK doesn't present such a solution" regarding a soft border in Ireland, it is very difficult to imagine substantive progress in Brexit negotiations".

In addition, Tusk explained that "services are not about tariffs. Services are about common rules, common supervision and common enforcement to ensure a level playing field, to ensure the integrity of the single market and, ultimately, also to ensure financial stability. This is why we cannot offer the same in services as we can offer in goods. It's also why FTAs don't have detailed rules for financial services." That is, financial services will be bluntly excluded from the Brexit deal.

No surprise from BoJ

BoJ left monetary policy unchanged today as widely expected. Short term policy rate is kept at -0.1%. BoJ will continue to purchase assets at a pace of JPY 80T per annum to keep 10 year JGB yields at around 0%. Goushi Kataoka dissented again, continued his push to lower yields on JGBs with maturities longer than 10 years.

In the statement, BoJ noted that the economy is "expanding moderately, with a virtuous cycle from income to spending operating". And it expects such "moderate expansion" to continue. Core CPI is expected to "continue on an uptrend and increase toward 2percent". Risks to the outlook include US policies, outcome and Brexit negotiation and geopolitical risks. BoJ maintained the pledge on "continuing expanding the monetary base." until core CPI exceeds 2% and stays above in a "stable manner.

Japan household spending rose 2.0% yoy in January versus expectation of -0.8% yoy. M2 rose 3.3% yoy in February. Labor cash earnings rose 0.7% yoy versus expectation of 0.6% yoy.

From China, CPI jumped sharply to 2.9% yoy in February, up from 1.5% yoy and beat expectation of 2.4% yoy. PPI slowed to 3.7% yoy, down from 4.3% yoy and below expectation of 3.8% yoy.

Looking ahead, wage growth the key the watch in NFP

Looking ahead, the economic calendar is rather busy today. Non farm payroll report from the US will be a major focus. Markets expect NFP to show 205k growth in February. Unemployment rate is expected to drop further to 4.0%. Other employment related data showed ADP grew solidly by 235k. ISM manufacturing employment jumped from 54.2 to 59.8. ISM services employment, on the other hand, dropped from 61.6 to 55.0. Overall, there is no sign pointing to downside surprise in the headline NFP number. But again, wage growth is the key to watch. Average hourly earnings are expected to rise 0.2% mom. Wage growth and its impact on inflation will be the key to whether there will be a fourth Fed hike this year.

Elsewhere, Canada will also release employment data. Earlier in European session, UK trade balance, productions will be featured. Germany will release trade balance and industrial production too.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9448; (P) 0.9484; (R1) 0.9546; More...

USD/CHF's rebound from 0.9186 accelerates to as high as 0.9533 so far today. The strong break of 0.9490 resistance indicates near term reversal. This is supported by bullish convergence condition in 4 hour MACD. Also, there is a head and shoulder bottom pattern (ls: 0.9254, h: 0.9186, rs: 0.9337). Intraday bias is now on the upside for 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9641 first. On the downside, break of 0.9337 minor support is needed to indicate completion of the rebound. Otherwise, near term outlook will be cautiously bullish even in case of retreat.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Current development is raising the chance that it is completed. But there is no confirmation yet. Focus will now be back on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add much credence to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BOJ Monetary Policy Statement | |||||

| 23:30 | JPY | Overall Household Spending Y/Y Jan | 2.00% | -0.80% | -0.10% | |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Feb | 3.30% | 3.30% | 3.40% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Jan | 0.70% | 0.60% | 0.70% | |

| 01:30 | CNY | CPI Y/Y Feb | 2.90% | 2.40% | 1.50% | |

| 01:30 | CNY | PPI Y/Y Feb | 3.70% | 3.80% | 4.30% | |

| 07:00 | EUR | German Trade Balance Jan | 21.1B | 21.4B | ||

| 07:00 | EUR | German Industrial Production M/M Jan | 0.60% | -0.60% | ||

| 09:30 | GBP | Visible Trade Balance (GBP) Jan | -12.0B | -13.6B | ||

| 09:30 | GBP | Industrial Production M/M Jan | 1.50% | -1.30% | ||

| 09:30 | GBP | Industrial Production Y/Y Jan | 1.80% | 0.00% | ||

| 09:30 | GBP | Manufacturing Production M/M Jan | 0.20% | 0.30% | ||

| 09:30 | GBP | Manufacturing Production Y/Y Jan | 2.80% | 1.40% | ||

| 09:30 | GBP | Construction Output M/M Jan | -0.50% | 1.60% | ||

| 12:00 | GBP | NIESR GDP Estimate Feb | 0.40% | 0.50% | ||

| 13:30 | CAD | Net Change in Employment Feb | 21.0K | -88.0K | ||

| 13:30 | CAD | Unemployment Rate Feb | 5.90% | 5.90% | ||

| 13:30 | USD | Change in Non-farm Payrolls Feb | 205K | 200K | ||

| 13:30 | USD | Unemployment Rate Feb | 4.00% | 4.10% | ||

| 13:30 | USD | Average Hourly Earnings M/M Feb | 0.20% | 0.30% | ||

| 15:00 | USD | Wholesale Inventories M/M (JAN F) | 0.70% | 0.70% |

Market Morning Briefing: Gold Fell Back Towards 1315

STOCKS

Dow (24895.21, +0.38%) inched up slightly yesterday and is heading upwards towards our near term Target of 25500. While above support near 24500, near term is likely to be bullish.

Dax (12355.57, +0.90%) closed above our mentioned resistance at 12300 and while the index sustains above 12300, the upside momentum could stay intact and the index may head towards 12400-12500 levels.

Nikkei (21553.31, +0.87%) moved up to that resistance near 21800 on the daily candles. If that holds, a rejection towards 21400-21200 is again possible; else a sustained rise could take it higher to levels near 22600 in the medium term. Look at 3 day candles which indicates medium term bullishness for Nikkei. While the channel support holds, the index is likely to move up gradually.

Shanghai (3291.47, +0.09%) is trading at important levels just now as seen on the 3-day candle chart. If the index moves above 3300 and sustains to move up, it could target 3350 or higher in the coming sessions; else a rejection from 3300 could again take it lower towards 3200.

Nifty (10242.65, +0.87%) bounced back from 10140 itself without coming down to test our expected 10080-10020 levels. The current rise is expected to be short lived before another down-leg is seen. Sensex (33351.57, +0.96%) looks as if it may try to test 33750 on the upside before again trying to come off from there. Near term looks bullish.

COMMODITIES

Brent (63.80) is holding below resistance near 66 and is likely to come off towards 62 while WTI (60.26) has support in the 60-59 region from where a bounce is expected.

Gold (1318.80) fell back towards 1315 instead of moving higher towards 1340/50. Note that 1300-1360 is an important region of trade for Gold in the near to medium term and it would be difficult for the price to break on either side just now. A bounce back from 1315-1310 is again possible in the coming sessions taking it higher to another attempt towards 1340/50.

Gold-WTI (21.82) is trading near immediate resistance and if this holds, the ratio may come down again towards 21 and lower.

Copper (3.0740) is down to test 3.07 in line with our expectation and is likely to bounce back from here back to levels near 3.15-3.20 in the medium term. Note that 3.07 is an immediate support on the daily candles and is likely to hold just now.

FOREX

Euro (1.2310) : The impact of the ECB policy decision yesterday was seen in 2 parts. Immediately post the release of the press statement, the dropping of the 'easing bias' (a commitment to increase monetary stimulus if absolutely necessary) was perceived as a step forward in the direction of tighter monetary policy in future. This prompted the Euro to shoot up towards 1.2446. However, later, the visibly dovish stance by Draghi in the press conference and the downward revision of forecasted inflation in 2019, caused the Euro to weaken immediately below 1.24. It is now trading near 1.231. There is support near 1.23 on the weekly candles for Euro which could hold. A break of 1.23 (if it happens) would see Euro testing support on daily candles near 1.22-1.225.

The Dollar Index (90.218) has seen an upmove due to the weakening in the Euro. It has immediate resistance visible on the daily candles near 90.5. If breached, there is higher resistance near 91 on 3 day and weekly line charts. The Bank of Japan policy decision might also impact the Dollar.

Dollar-Yen (106.69) has risen beyond immediate resistance near 106.5 on daily candles and might now confront two important resistances near 107 on the daily line charts provided by 13 days and 21 days moving average lines. The Bank of Japan meeting today might impact the course of Dollar Yen significantly in the days ahead.

The Euro-Yen (131.28) seems to be respecting the channel resistance on daily candles near 131-131.5 and might hence come down towards 129-130 in the coming sessions.

Pound (1.3799) against our expectation has unexpectedly dropped towards 1.38 again but there is strong support near current levels on daily candles which should hold for the time being.

Dollar-Rupee (65.145): Overall uptrend has possibly reasserted itself. A break above 65.20, if seen, takes the market up to 65.40+

INTEREST RATES

The ECB press statement's apparent hawkishness (due to dropping of the easing bias – explained above in Forex) did send German 10 Yr yields (0.628% ) towards 0.69% yesterday but Draghi's dovishness in the press conference that followed pulled yields back down. The ECB as expected kept key interest rates unchanged. The German – US yield spread is again near support on long term charts near -2.24% and might see a rise in the coming sessions (possibly via a downmove in US yields).

US 10 Year Yield (2.87), US 30 year Yield (3.133), US 5 year yield (2.64), US 2 year yield (2.262) : US yields continue their sideways movement in a very narrow range. We had mentioned yesterday that global politics indicates that a rise in US yields beyond long term resistance levels is imminent. However, there might just be some drop in US yields in the coming week, after which the week of the US Fed meeting might then see volatility return, taking yields higher in anticipation of a rate hike.

(Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively – a decisive breach of these levels could happen in March 2nd half.)

The Bank of Japan meeting is underway and the policy decision would be important for global bond markets in the coming weeks.

BoJ stands pat, Kataoka dissents again, little market reaction

No surprise, BoJ left monetary policy unchanged today. Short term policy rate is kept at -0.1%. BoJ will continue to purchase assets at a pace of JPY 80T per annum to keep 10 year JGB yields at around 0%.

Goushi Kataoka dissented again, continued his push to lower yields on JGBs with maturities longer than 10 years.

Quotes from the statement:

- "Japan's economy is expanding moderately, with a virtuous cycle from income to spending operating".

- "Japan's economy is likely to continue its moderate expansion".

- "Year-on-year rate of change in the CPI is likely to continue on an uptrend and increase toward 2percent".

- Risks include: US policies, Brexit and geopolitical risks

- BoJ will "continuing expanding the monetary base:" until core CPI exceeds 2% and stays above in a "stable manner.

Little reaction in USD/JPY as it's on course to extend the rebound from 105.24, following broad based dollar strength.

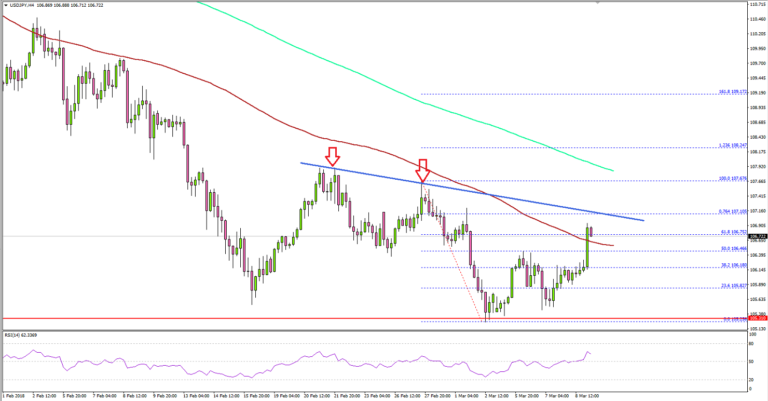

USD/JPY Facing Uphill Task Ahead Of US NFP

Key Highlights

- The US Dollar found support near 105.30 and recovered against the Japanese Yen.

- There is a monster bearish trend line forming with resistance at 107.10 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending March 3, 2018 posted a rise from 210K to 231K.

- Today, the US nonfarm payrolls figure for Feb 2018 will be released, which is forecasted to increase by 200K.

USDJPY Technical Analysis

The US Dollar formed a decent support around 105.30 after a major decline against the Japanese Yen. The USD/JPY pair is correcting higher, but it is facing a crucial resistance near 107.00-10.

Looking at the 4-hours chart of USD/JPY, there was a support formed and the pair recovered above the 38.2% Fib retracement level of the last decline from the 107.67 high to 105.25 low.

However, there is a significant resistance around 107.00 on the upside. There is also a monster bearish trend line forming with resistance at 107.10.

Moreover, the 76.4% Fib retracement level of the last decline from the 107.67 high to 105.25 low is at 107.10. Therefore, it seems like the 107.00-10 region is a crucial hurdle for more gains in USD/JPY.

On the downside, the last swing low of 106.20 is a key support. A break below 106.20 could push the pair towards 105.30. The 100 simple moving average (red, 4-hour) is also a short-term support at 106.50.

Recently, the US Initial Jobless Claims for the week ending March 3, 2018 was released by the US Department of Labor. The market was looking for a rise from the last reading of 210K to 220K.

The result was lower than the forecast, as there was a rise in claims from 210K to 231K. The report added that:

The 4-week moving average was 222,500, an increase of 2,000 from the previous week's unrevised average of 220,500.

Overall, the USD/JPY pair may continue to face a strong selling interest on the upside near 107.10. A close above 107.10 could trigger further gains toward 108.00.

Economic Releases to Watch Today

- Germany's Trade Balance for Jan 2018 – Forecast €21.1B, versus €21.4B previous.

- Germany's Industrial Production for Jan 2018 (MoM) – Forecast +0.5%, versus -0.6% previous.

- UK Industrial Production for Jan 2018 (MoM) – Forecast +1.5%, versus -1.3% previous.

- US nonfarm payrolls Feb 2018 – Forecast 200K, versus 200K previous.

- US Unemployment Rate April 2018 – Forecast 4.0%, versus 4.1% previous.

- Canada's employment Change payrolls Feb 2018 – Forecast 20K, versus -88K previous.

- Canada's Unemployment Rate April 2018 – Forecast 5.9%, versus 5.9% previous.

EC Tusk on Brexit: Ireland first, and no financial services in the deal

European Council President Donald Tusk emphasized that the Irish border issue is a top priority in Brexit negotiation. He said that "if in London someone assumes that the negotiations will deal with other issues first, before moving to the Irish issue, my response would be: Ireland first." And he warned that "as long as the UK doesn't present such a solution" regarding a soft border in Ireland, it is very difficult to imagine substantive progress in Brexit negotiations".

In addition, Tusk explained that "services are not about tariffs. Services are about common rules, common supervision and common enforcement to ensure a level playing field, to ensure the integrity of the single market and, ultimately, also to ensure financial stability. This is why we cannot offer the same in services as we can offer in goods. It's also why FTAs don't have detailed rules for financial services." That is, financial services will be bluntly excluded from the Brexit deal.

Fed George: Risks to growth “predominately to the upside”

Kanasa City Fed President Esther George (a known hawk) said

- "Risks to the outlook appear to be predominately to the upside,"

- Fed should "carefully calibrate its policy to lean against a potential buildup of inflationary pressure or financial market imbalances."

"Predominately to the upside" is in-line with her hawkishness. Other members generally see risks to be "roughly balanced".