Sample Category Title

Trump to meet North Korea Kim on denuclearization

Trump agreed to meet with North Korean leader Kim Jong-un for nuclear talks.

The news came after South Korean National Security Council chief Chung Eui-yong said Kim "expressed his eagerness to meet President Trump as soon as possible".

White House spokeswoman Sarah Huckabee Sanders said the meeting will be at "a place and time to be determined."

Trump also tweeted "Kim Jong Un talked about denuclearization with the South Korean Representatives, not just a freeze," "also, no missile testing by North Korea during this period of time. Great progress being made but sanctions will remain until an agreement is reached. Meeting being planned!"

Trump signed tariff proclamation but backed down from no exemption position

Trump finally signed the proclamations of 25% steel and 10% aluminum tariff yesterday. The new tariffs will take effect in 15 days. He said in the White House, surrounded by steel and aluminum workers, that "we have to protect and build our steel and aluminum industries, while at the same time showing great flexibility and cooperation toward those that are really friends of ours,"

But he backed down from his original position of no exemption. As Canada and Mexico are exempted, pending NAFTA negotiations outcome. And he opened the door for reduction in tariffs for countries that "treat us fairly".

Trump added "I'll have a right to go up or down, depending on the country, and I'll have a right to drop out countries or add countries." And, "we just want fairness. Because we have not been treated fairly by other countries."

ECB Surprisingly Removed Easing Bias, Draghi Downplayed The Implication On Future Policy

Surprising to most market participants, ECB dropped the easing bias in the forward guidance. While this had initially sent the euro slightly higher, it reversed as President Mario Draghi reinforced that the act was 'backward looking' and would not affect future monetary decision making. Policymakers remained confident over the growth outlook but again raised concern over weak inflation. As such, the updated economic projections saw upgrades in the growth but downgrades on inflation outlook. Going forward, the focus is on the tapering process of ECB's asset purchases which stay at a monthly pace of 30B euro. Meanwhile, ECB's forward guidance would gradually focus more on the interest rate path, and its relations with inflation.

The eyebrow-raising decision was removal of the language that, 'if the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, we stand ready to increase the asset purchase programme (APP) in terms of size and/or duration'. Removal of the easing bias signaled less stimulus going forward. However, at the press conference, Draghi stressed that the unanimous decision was 'substantially a backward-looking decision without signals or implications for either our expectations or our reaction function'. He emphasized that 'key ECB interest rates to remain at their present levels for an extended period of time and well past the horizon of our net asset purchases'. Meanwhile, he reaffirmed that the asset purchase program remained in effect.

On economic developments, the members were confident that 'Incoming information, including our new staff projections, confirms the strong and broad-based growth momentum in the euro area economy, which is projected to expand in the near term at a somewhat faster pace than previously expected'. Inflation remained subdued. Yet, the members were confident that the robust growth outlook suggested that inflation would 'converge towards our inflation aim of below, but close to, 2% over the medium term'. Some more time might be needed for core inflation 'show convincing signs of a sustained upward trend'. While the risks remained broadly balanced, ECB explicitly indicated the negative impacts of protectionism noting that 'downside risks continue to relate primarily to global factors, including rising protectionism and developments in foreign exchange and other financial markets'.

The latest staff economic projection revealed upward revision for growth this year. Annual real GDP is estimated to expand by +2.4% in 2018, up from +2.3% projected in December. Growth forecasts for 2019 and 2020 stayed at +1.9% and +1.7%, respectively. Downward revision on inflation forecasts for 2019 was probably another reason for the dove to dump euro. The staff estimated headline CPI to be at 1.4%, +1.4% and +1.7% for 2018, 2019 and 2020, respectively. While the estimates for 2018 and 2020 stayed unchanged from December's projections, that for 2019 was -0.1 percentage lower.

On the policy outlook, the focus is on the tapering process of ECB's asset purchases which stay at a monthly pace of 30B euro. Note that the central bank maintained the language that the net asset purchases 'are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim'. However, the current economic development signal QE extension beyond September is unnecessary. Meanwhile, ECB's forward guidance would gradually focus more on the interest rate path, and its relations with inflation. On the policy rate, the first thing to deal with is the negative deposit rate. We believe ECB would stress, when the time comes for bringing the deposit rate back to positive territory, that this does not indicate the beginning of a rate hike cycle.

Gusto Dollar + Breaking News

Breaking News

Donald Trump to meet Kim Jong-un in May after an invitation from North Korea

Both the Nikkei and USDJPY are rocketing higher on encouraging North Korea Headlines and improving risk sentiment

We should expect this news to boost regional market sentiment as well

However, USDJPY should run into some headwinds as we approach 107 as Fiscal Year end selling along with an uptick in equity inflow flows should cap the USDJPY move

Longer term BoJ policy implications should overshadow this bounce in USDJPY, despite the fact we've taken out key resistance at 106.45-55 level

Gusto Dollar

Broad-based dollar strength dominated overnight markets as a combination of a dovish Draghi, tariff and position adjustments ahead of Friday AHE print were the primary drivers

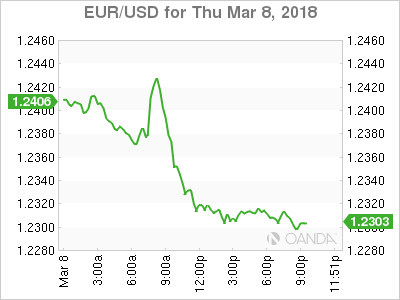

The EURUSD initially spiked higher on ECB assurance not to increase the size of their monthly bond purchases. But then plummeted when the central bank revised their inflation forecast for 2019 to 1.4 percent from 1.5 percent.

To the delight of the ECB doves, Draghi struck a dovish chord by subtly tweaking forward guidance and even suggested that the negative fall out from an escalation of a global trade war will keep the ECB sidelined for some time to come. Traders caught long, and wrong ran for the exits as the markets pushed back a more definitive shift in ECB policy expectation to mid-2019

Ignoring advice from crucial trading allies and ranking members of his party, President Trump inked the steel tariff but included a provision for Canada and Mexico – the duties won't apply to these countries if a Nafta deal is signed. Therefore, they won't go into effect while negotiations are still going.

It's abundantly clear the Trump is setting sights on China noting that while he has 'great respect' for President Xi, he doesn't know 'if anything is going to come' of the US's current negotiations with them around these measures. He also called these measures 'a first stop.' suggesting further escalation is around the corner

Currency Markets

The Euro

The downgrade in ECB's inflation forecasts overwhelmed the hawkish shift from the removal of the easing bias in the statement. And with hawkish Fedspeak from Brainard and Powell angling to adjust language on top side risks at the March FOMC meeting, the short-term outlook for the EURUSD looks extremely murky

The Japanese Yen

JPY focus turns to the BoJ today, but the BoJ is really up against it as JPY continues to trade firm on the backdrop of policy normalisation chatter. Unless the BoJ offers up an unlikely aggressive easing signal, Yen strength should remain in play over the short to medium term.

The Malaysian Ringgit

The prospects of a full-out trade war are weighing on regional sentiment as is the more hawkish Fed narrative is denting the Ringgit sentiment. We may see an extended pickup in regional outflows as Trump continues to beat the Trade war drums where he's expected to take direct aim at Asia with his next tariff salvo.

Oil Markets

The stronger dollar and reality check that US production continues to ramp up is causing traders to pare back bullish bets. As well, they escalation of tariff wars continue to weigh on the forward demand side of the curve all but suggesting the path of least resistance is lower

Gold Markets

The stronger dollar is weighing on Gold prices but uncertainty over the fall out of an impending trade war with China could result in acute drops in global equity gold should remain bid on dips in this probable scenario

Dollar Divided On Trade Anxiety And Jobs Data Anticipation

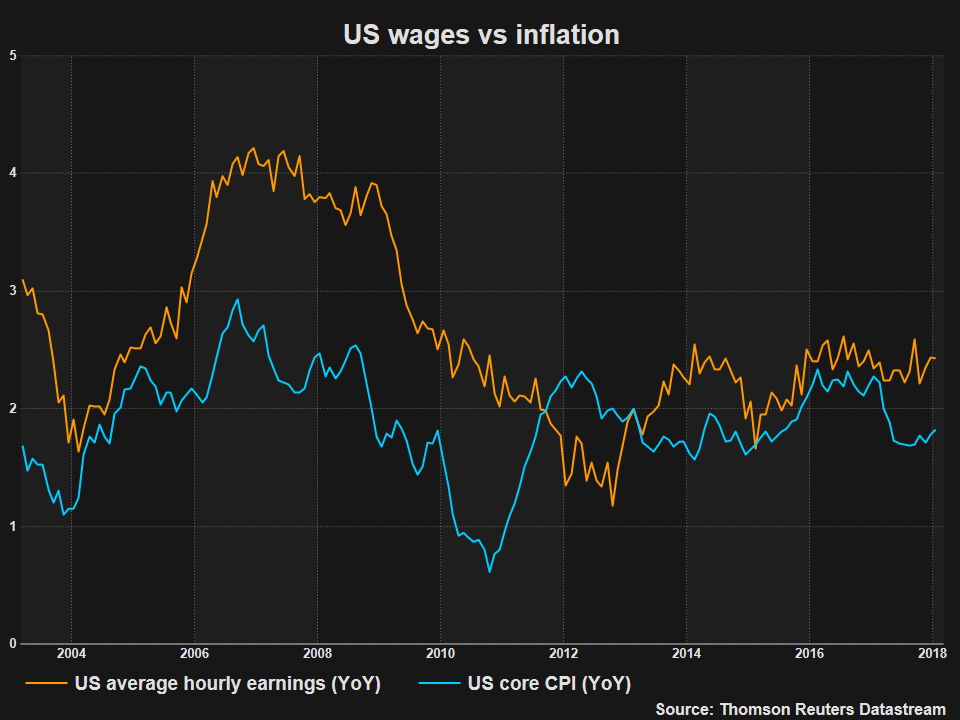

The USD was higher on Thursday after the European Central Bank (ECB) published a hawkish statement but was neutralized by the central bank’s President Mario Draghi who remains concerned about low inflation and the rise of protectionism. The steel and aluminium tariffs announced last week have threatened to start a trade war and despite the US President’s unfazed demeanour it could end up costing the US thousands of jobs. Employment data will be the focus of the market on Friday as the U.S. non farm payrolls (NFP) report will be released at 8:30 am EST with US worker wages garnering the most attention as inflationary signals..

- US expected to add 200,000 jobs in February

- Canadian jobs to bounce from January drop

- US wage growth forecasted at 0.2 percent

Dollar Higher After ECB Awaiting US Jobs Report

The EUR/USD lost 0.81 percent on Thursday. The single currency is trading at 1.2310 as investors sold some positions after the European Central Bank (ECB) published its rate statement. The central bank kept rates unchanged but did remove mention of adding more stimulus if the economy needed it. ECB President Mario Draghi was neutral with his comments as he praised rising European growth but also mentioned slow inflation and trade challenges ahead. The EUR gained on the statement but Draghi made sure to bring the currency back to reality as inflation and trade are in focus. The promised tariffs by the Trump Administration are yet to materialize but it is not hard to expect this is the last time they will be used to protect American manufacturers.

The world appears to be moving without the US as evidenced by the signing of the Trans Pacific Pact (TPP) on Thursday by the 11 remaining nations. The US steel and aluminium tariffs have already cost Trump the backing of economic advisor Gary Cohn who resigned this week after failing to convict the White House from sounding the tariff horn. Draghi during his press conference used the tariffs as an example of the dangers in unilateral decisions, specially when aimed at your allies.

The market is pricing in a rate hike in two weeks by the U.S. Federal Reserve. The CME FedWatch tool shows a probability of 86 percent that central bank will lift interest rates by 25 basis points, those odds are up from 76.1 percent a month ago. The dollar has not been able to capitalize of strong growth expectations and a tightening policy by the American central bank as concerns have risen on the twin deficits, but also on what will happen after rates hit the 3 percent target.

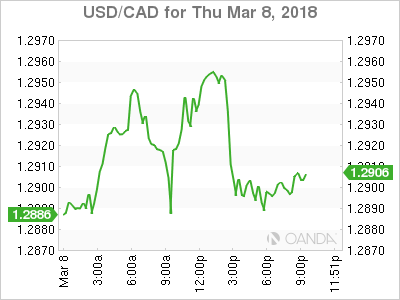

The USD/CAD lost 0.10 percent in the last 24 hours. The currency pair is trading at 1.2897 in a volatile day of trading for the loonie. The Canadian currency depreciated during the Asian session and traded near 1.2950 only to appreciated below 1.29 only to once again rise ahead of US data. The final trend in the session came courtesy of a report outlining that the steel and aluminium tariffs will begin in 15 days, but that Canada and Mexico are exempt. The exemption is a CAD positive as it could also mean NAFTA will remain as the White House is taking into consideration the benefits of the trade deal. Canadian NAFTA negotiators were floored by the proposed US tariffs but it appears the US has backed down as both Mexico and Canada commented they were prepared to retaliate if they were not excluded.

The CAD has had a horrible start to 2018 and is down 2.51 percent against the USD as the uncertainty of the fate of NAFTA lingers with the 8th and final round to take place at the end of the month. The Canadian economy is slowing down, which in turn will make it less likely the Bank of Canada (BoC) keeps pace with the Fed’s rate hike path

The Federal Reserve is widely expected to raise rate four times in 2018, but the Bank of Canada will likely be unable to compete with that kind of pace. The BoC is concerned with economic growth, which slowed in the fourth quarter, as well as uncertainty over NAFTA, which could fall apart if the Trump administration makes good on its threat to withdraw if its demands for more favorable treatment for US goods is not met. The Bank is not expected to raise rates before May, and if the Fed outpaces the BoC on the rate front, the Canadian dollar could lose ground to a more attractive US currency.

Canadian jobs will look to bounce back form the worst drop in nine years. Statistics Canada will release the employment change data on Friday, March 9 at 8:30 am EST. The Canadian economy is expected to add close to 22,000 jobs after January’s debacle where it lost 88,000. The jobs data in Canada will share release time with the NFP that will be more heavily scrutinized by the market with an eye for higher inflation signals in the US.

Market events to watch this week:

Thursday, March 8

Midnight JPY BOJ Policy Rate

Midnight JPY Monetary Policy Statement

Friday, March 9

JPY BOJ Press Conference

4:30am GBP

Manufacturing Production m/m

8:30am CAD Employment Change

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

Gold Dips, Markets Await Key Employment Data

Gold has posted losses in the Thursday session. In North American trade, the spot price for an ounce of gold is $1320.79, down 0.36% on the day. In economic news, unemployment claims disappointed and climbed to 231 thousand, well above the estimate of 220 thousand. On Friday, the US releases wage growth and nonfarm payrolls, so traders should be prepared from some movement from gold.

The US dollar has been under pressure since US President Trump proposed stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. There is also strong domestic opposition to the proposal, as Republican lawmakers, including House Speaker Paul Ryan, have come out against the move. This has raised hopes that Trump will back down. There was further drama on Wednesday, as Gary Cohn, Trump’s chief economic adviser, resigned. Cohn was a strong advocate of free trade, so his resignation could weaken opposition in the White House to the tariffs. Will Trump make good on his threat or back off? Until the situation is resolved, traders should be prepared for continuing volatility in the markets.

Employment numbers continue to be in focus in the latter part of the week. On Wednesday, ADP nonfarm payrolls ticked upwards to 235 thousand, up from 234 thousand a month earlier. This easily beat expectations, boosting investor risk appetite and sending gold prices lower. The nonfarm payrolls report is also expected to remain steady, and if the indicator can again beat expectations, gold could continue to head south.

After Soft Q4 GDP in Australia, Wage Growth Is Key for RBA

We are not terribly concerned by the miss in this week's GDP report, as the drags from trade and business spending will likely prove temporary. Still, the RBA is apt to keep rates on hold until wage inflation shows up.

Drags from Trade and Business Spending to Blame

The Australian economy expanded just 0.4 percent (not annualized) in the fourth quarter, slightly below market expectations of 0.5 percent. It bears noting that growth in the prior quarter was revised marginally higher, so the growth in the fourth quarter was coming off a slightly higher base. Temporary trade dynamics and weakness in business investment are much to blame for the softness of fourth quarter growth. Domestic demand was actually quite strong over the period, reflecting gradual growth in the labor market and perhaps suggesting stability from consumer spending ahead.

The unemployment rate has trended lower, even as labor force participation approaches a record high. Despite these improvements in the labor market, wage growth remains modest…at least for now. There is a growing perception that improvement in the labor market will inevitably translate into higher wages. In the official statement explaining its decision to keep the cash rate unchanged earlier this week, the Reserve Bank of Australia (RBA) observed, "the rate of wage growth appears to have troughed."

The RBA went on to describe the lack of skilled workers available to employers. Increased competition for skilled labor in particular could eventually translate into the long-anticipated wage growth, which would foster increases in inflation this year.

Even without the wage growth, the improved labor market dynamics appear to be supportive of GDP growth. Household spending increased 1.0 percent over the quarter, as retail sales showed some upward momentum after signs of weakness in the third quarter. The fourth quarter was the fastest quarterly rate of personal consumption growth for the whole of 2017. To the extent that the anticipated improvements in wage growth materialize, we should expect to see continued support from consumer spending in the quarters ahead.

Similarly, the slight pick-up in imports further signals continued domestic demand. However, export growth significantly slowed over the quarter, causing net exports to shave off 1.9 percentage points from the headline quarterly figure. With the global growth backdrop improving, we do not expect exports to continue to weigh on growth.

"Holding the stance of monetary policy unchanged"

As was widely expected, the RBA held its key lending rate unchanged at 1.50 percent. We expect the RBA to stay on hold, as it remains clear that policymakers are content with current economic conditions. The language in the policy statement continues to emphasize improving global dynamics, without implying a particularly hawkish stance. Our baseline expectation is that the RBA will continue to remain on hold, before eventually joining other global central banks in normalizing policy later this year with an eventual rate hike. The key is whether or not the elusive wage growth materializes.

Dollar gains momentum with help from Euro selloff

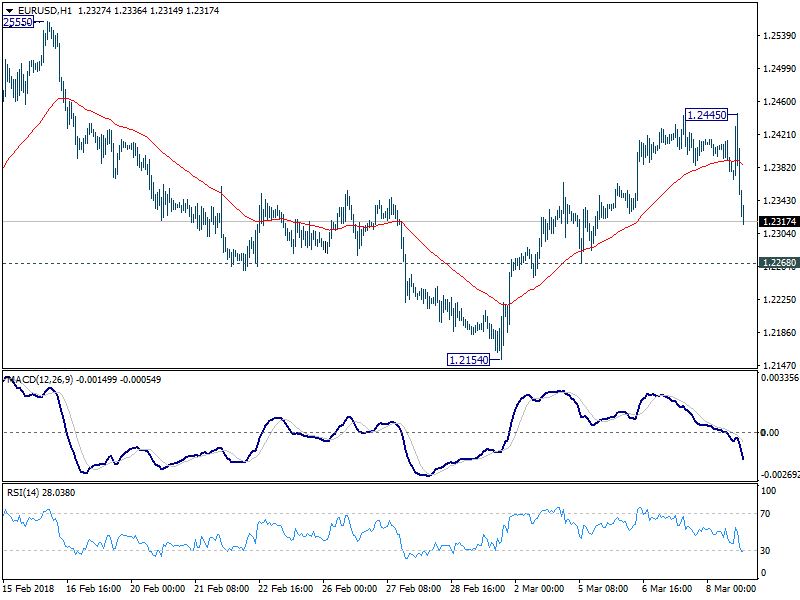

Dollar is gaining momentum as the US session goes on . That's partly helped by ECB disappoint as we see EUR is now the weakest one for the day. DOW pared initial gains and it's trading nearly flat. Markets are now awaiting Trump's signing of the order for tariffs. USD/CHF has taken out 0.9490 resistance mentioned earlier. Quickly, focus now turns to 1.2268 in EUR/USD.

US Jobs Report: All Eyes on Wages

The US will release its all-important monthly employment report for February, on Friday at 1330 GMT. While forecasts point to yet another healthy month in terms of jobs added, investors are likely to focus primarily on the wage numbers, to gauge whether higher inflation is indeed just around the corner. How wages evolve will likely be critical for market expectations regarding how many hikes the Fed may deliver this year and thus, for the dollar’s forthcoming direction.

The US economy is projected to have added 200k jobs outside of the farming industry in February, exactly as many as in January. The unemployment rate is anticipated to have ticked down to 4.0% from 4.1% previously, which would mark a fresh low last seen in 2000. Last but not least, average hourly earnings are projected to have slowed slightly to 2.8% in yearly terms, from 2.9% in the previous month.

Overall, this looks like yet another strong report, which is not surprising; the US labor market has been on a tear for years now. The US economy has added jobs at a robust pace while the unemployment rate has steadily declined, stoking speculation that Americans may be set to enjoy a pay rise as companies start having difficulties finding skilled personnel and need to raise salaries to attract talent.

Wage growth is extremely important for central bankers and investors around the globe, as it is considered a precursor to inflation. In an environment where wages are rising, firms faced with rising labor costs will have to raise their own prices to compensate, or see their profits fall. Therefore, once wages begin to accelerate, inflation is expected to follow suit.

This theory fits in nicely with recent market moves. Back in early February, an upside surprise in US wages raised speculation that inflation may be set to pick up, and that the Fed may have to respond by raising interest rates more aggressively, in order to “reign in” price pressures. The result was a surge in US bond yields, as well as a modest recovery in the dollar – which up until that point was plunging. This narrative puts even more emphasis on the upcoming set of data. Investors will be watching closely to see whether last month’s acceleration in wages was just a fluke, or a sign of things to come.

This theory fits in nicely with recent market moves. Back in early February, an upside surprise in US wages raised speculation that inflation may be set to pick up, and that the Fed may have to respond by raising interest rates more aggressively, in order to “reign in” price pressures. The result was a surge in US bond yields, as well as a modest recovery in the dollar – which up until that point was plunging. This narrative puts even more emphasis on the upcoming set of data. Investors will be watching closely to see whether last month’s acceleration in wages was just a fluke, or a sign of things to come.

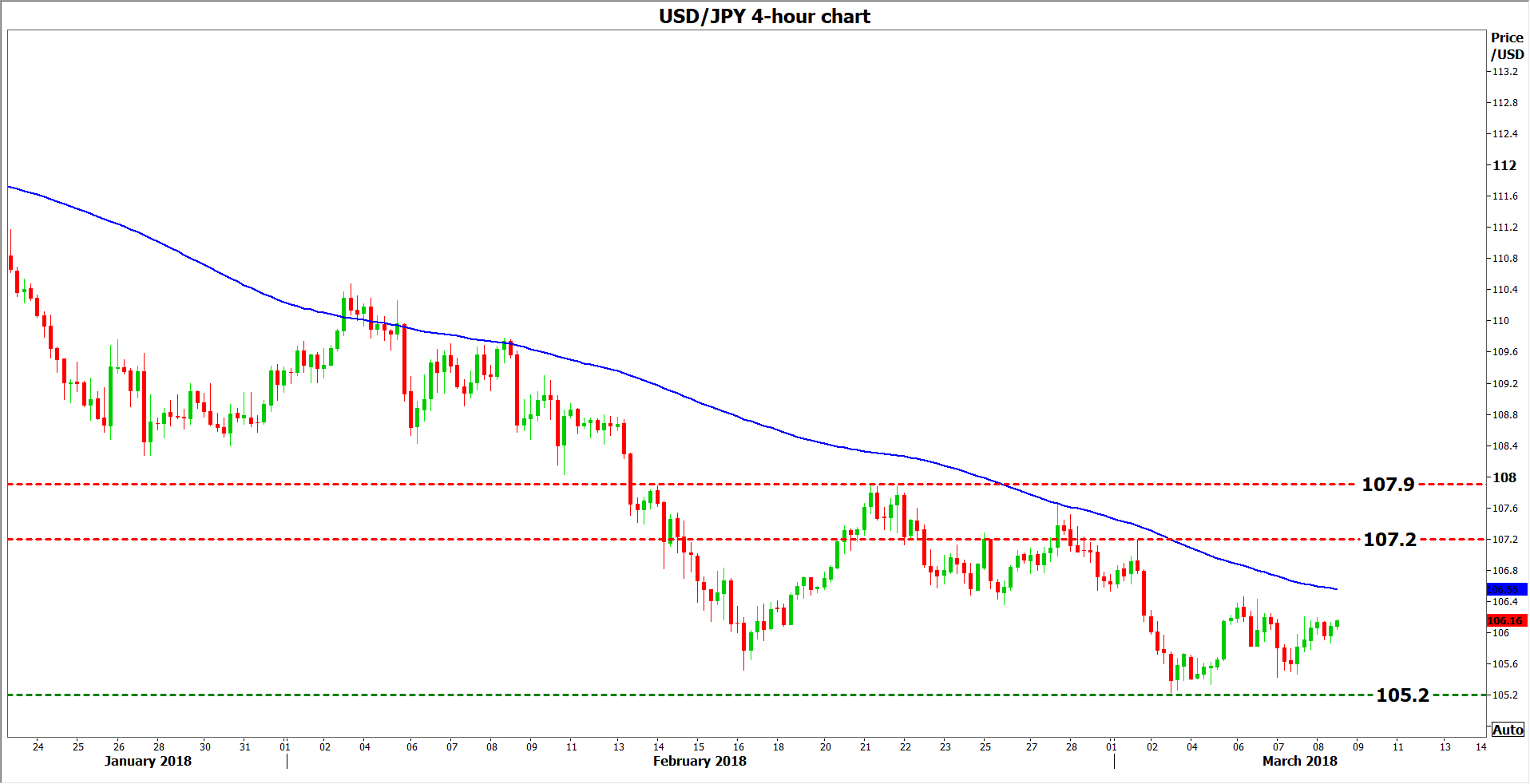

At the time of writing, market pricing and the Fed’s own rate projections for this year are almost exactly in line. In December, the FOMC signaled it is likely to deliver three quarter-point rate hikes in 2018, and markets have so far priced in two hikes fully, while they also see a 92% probability for a third one, according to the Fed funds futures. In case these data come out stronger than anticipated – particularly on the wages front – that would likely seal the deal for three hikes this year, and may even raise speculation for a fourth. The dollar would likely benefit in such circumstances, with dollar/yen possibly aiming for a test of the 107.20 resistance area, marked by the peaks of March 1. If the bulls are strong enough to overcome that hurdle, then sell orders may be found near the 107.90 level, which is the high of February 21.

On the flipside though, if the data disappoint, for instance with wages slowing by more than expected, then the dollar would probably soften as markets become more skeptical about a third hike. Dollar/yen is likely to tumble and initially test the 105.20 zone, which is the March 2 low. Further declines below that barrier would mark a forthcoming lower low on the daily chart, and could be a signal for steeper declines. In this case, support may be found near 104.30, which is the high of September 2016.

Finally, it should be noted that the Bank of Japan’s policy gathering early on Friday could also impact price action in dollar/yen, ahead of the US jobs data.

Finally, it should be noted that the Bank of Japan’s policy gathering early on Friday could also impact price action in dollar/yen, ahead of the US jobs data.