Sample Category Title

ECB Review: ‘Hawkish’ Action – Softish Language

- As expected, the ECB's changed its forward guidance so it no longer entails the QE flexibility. President Mario Draghi struck a softish tone in the press conference, in particular as victory on inflation cannot be declared yet.

- Overall, our ECB view is not changed based on today's events, as it included little new guidance. Importantly, the decision today was taken unanimously.

- Staff projections. The near-term growth outlook has strengthened but the ECB's core inflation forecast remains too optimistic.

- Market reaction. The overall implication was a knee-jerk reaction, with the softish language driving yields and the EUR slightly lower, particularly the comment on inflation on declaring victory.

In line with our expectation, the ECB removed their pledge to stand ready to increase the volume if the outlook becomes less favourable. Draghi emphasised the improved economy and the change in language is a natural step to the forward guidance. Recall that this wording has been used since December 2016, when they adjusted the purchase rate from EUR80bn to EUR60bn, at a time when the economic outlook was worse than now (core inflation around 0.8-0.9% and quarterly growth rates around 0.4-0.5% back then).

On inflation we take note of Draghi saying that victory can't be declared yet on inflation. That's amongst the most dovish we got today. He also noted uncertainty on output growth and slack in the economy, but we do not view him to be overly concerned on this, for now. The removal of the QE easing bias reflected the stronger growth outlook and thereby also a narrowing of the convergence path in inflation. Further, the lack of bonds available for the QE programme should also be noted. ECB's Benoît Coeuré presented the free float of eligible German bonds to be less than 10% in a speech on 23 February.

We have previously argued that with deflation risk gone and strong growth fundamentals, ECB could remove the QE bias, but the first rate hike is still not a pressuring theme. We assign the key driver for the first rate hike to be the inflation – and in particular core inflation. We re-emphasise that markets should not be too focused on spot headline inflation but on core (and super-core) inflation. Further, we highlight that the decision today was taken unanimously, which is a very strong signal on the path of communication. Finally, Draghi stepped up its rhetoric on call for other institutions/governments do their job with structural reforms.

ECB core inflation projection remains too optimistic

The ECB also released new economic forecasts at the meeting, which, as expected, were little changed from the December 2017 forecasts.

- Near-term growth outlook has strengthened: The GDP growth forecast for 2018 was lifted marginally to 2.4% from 2.3%, reflecting stronger recent growth momentum and upward revisions in foreign demand, and remains above our forecast of 2.1%. The projection for 2019 and 2020 were left unchanged at 1.9% and 1.7%, respectively. Risks to the growth outlook were judged to be broadly balanced.

- The inflation outlook was slightly revised down, mainly reflecting the dampening effect of the stronger euro. The ECB expects headline inflation to hover around 1.5% for the rest of the year and Draghi stressed that underlying inflation pressures remain subdued and are expected to rise only gradually over the medium-term driven by an expected pick-up in wage growth and continuing economic expansion. The ECB kept its 2018 and 2020 headline inflation forecasts unchanged, but lowered the 2019 forecast by 0.1pp to 1.4%. Surprisingly, core inflation projections remained unchanged despite the expected negative effect of the higher euro exchange rate. The ECB still projects core inflation to accelerate significantly to 1.8% in 2020, supported by an expected strong pick-up in wage growth to 2.7% in 2020, which we still see as optimistic (see also Part 2: Eurozone Inflation - Upside risks from oil prices and rising wage pressures), 27 February.

Fixed income

The overall implications on the fixed income markets from the ECB meeting and the press conference is modestly upward pressure on the core EU rates combined with a bearish flattener between 5Y and 30Y on the German government curve and the EU swap curve.

The periphery continue to perform despite the rise in rates. The ECB is able to signal a gradual approach to "scaling down" QE without hurting the peripheral markets. Hence, we have hit our profit target on being long 10Y Portugal relative to swaps. Our long position in 10Y Spain has also performed well.

FX

EUR/USD moved towards 1.2450 on the announcement of QE flexibility being removed, and also initially pressed higher still as Draghi did not come out as soft as expected at first. However, with Draghi framing the change in language as a natural step given the 'strong' outlook - and thus the move not representing that the ECB is in a hurry to 'exit' as such – the EUR/USD rally faded somewhat. Thus the year-to-date high of 1.2555 was not at risk today.

Despite some brief comments on the challenges arising from a stronger currency, we think that today's shift in forward guidance, while not in itself a trigger for a new EUR uptrend, will keep alive FX markets' belief in the ECB keeping up the pace in its the gradual move towards the 'exit'. The potential for this to support the single currency, not only from a relative rates point of view, but also from a capital-flow point of view still holds EUR upside.

Further, with omnipresent arguments for USD weakness, see Part 5: FX and inflation - US inflation outperformance + comfy Fed = weaker USD, 2 March, it leaves EUR/USD fundamentally supported. In our view, this leaves the 1.21-1.26 range for the pair intact for now, but the cross is set to continue to grind higher further out. A possible trigger for this could be the ECB looking to adjust its rates communication which we do not expect to happen before the September 2018, at the earliest.

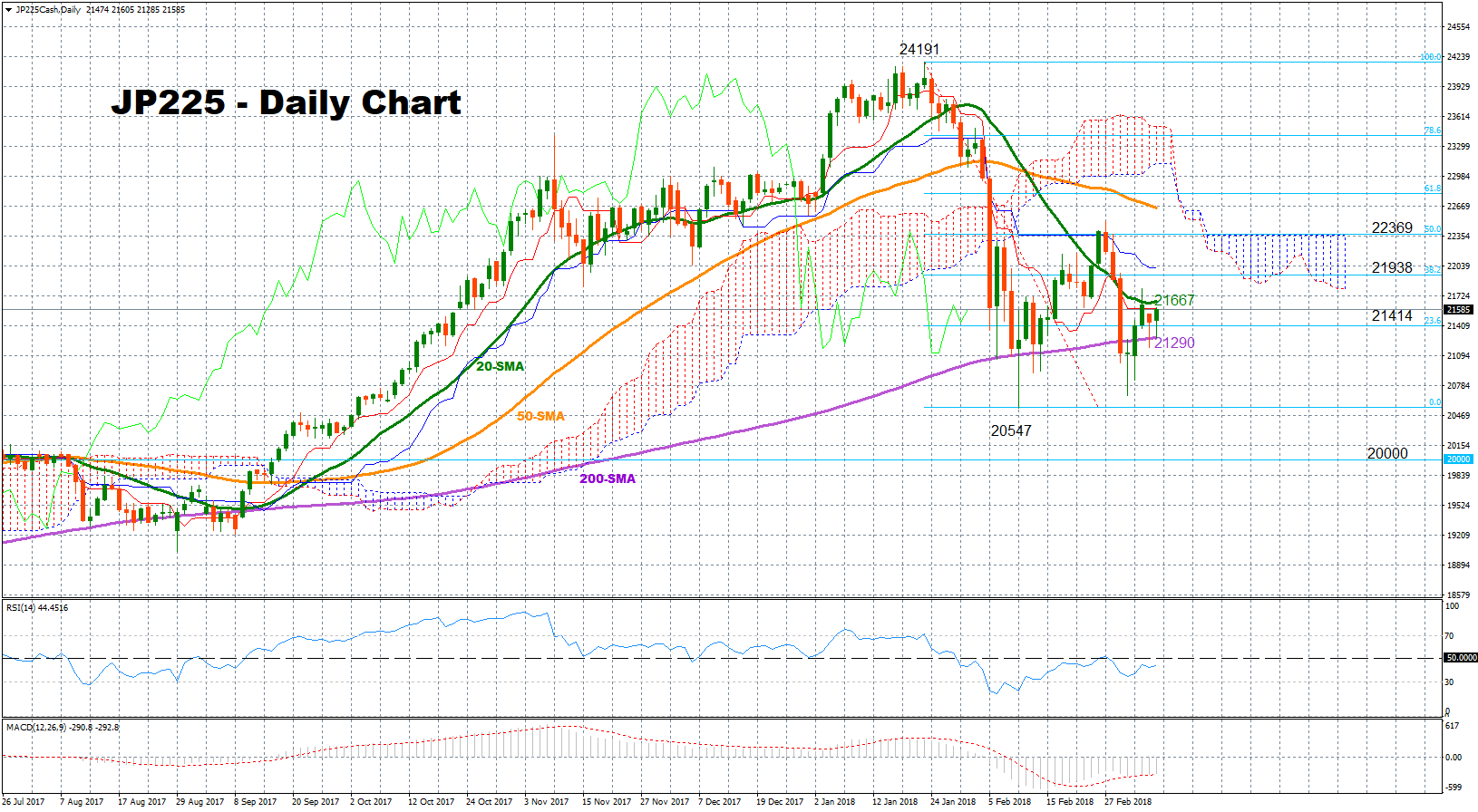

Japan 225 Stock Index Builds Base around 200-SMA; Neutral in Short-Term

Since its deep fall towards four-month lows in early February, the Japan 225 stock has been going back and forth below the 50% Fibonacci retracement of its long way down from 24191 to 20547, creating a base around the 200-day simple moving average line (SMA). The technical picture supports that the range bound is likely to continue in the short-term.

Looking at momentum indicators, the RSI is lacking direction slightly below it neutral threshold of 50, suggesting that the market could keep consolidating in the near term. MACD is in the negative territory but is currently embraced by its red signal line supporting this view as well.

In the wake of negative pressures, the market could meet support at the 23.6% Fibonacci of 21414 before it heads lower to the 200-day SMA, currently at 21290. A successful close below this level could see a retest of the previous low of 20547, while in case of steeper declines, the index could breach this trough, diving to the 20000 psychological mark which used to provide resistance during last summer.

On the flip side, a move to the upside could see immediate resistance at the 20-day SMA at 21667 but should the market increase positive momentum above this area, the 38.2% Fibonacci of 21938 could be the next level in focus. A stronger barrier, though, could be found at the 50% Fibonacci of 22369 since any strong violation of this point could increase chances for further gains probably towards the 50-day SMA.

Turning to the medium-term picture, the market seems to be in bearish mode given that the index trades below the 50-day SMA. But as long as the bullish cross between the 50- and the 200-day SMA remains intact, there is hope that the market could return to bullish phase.

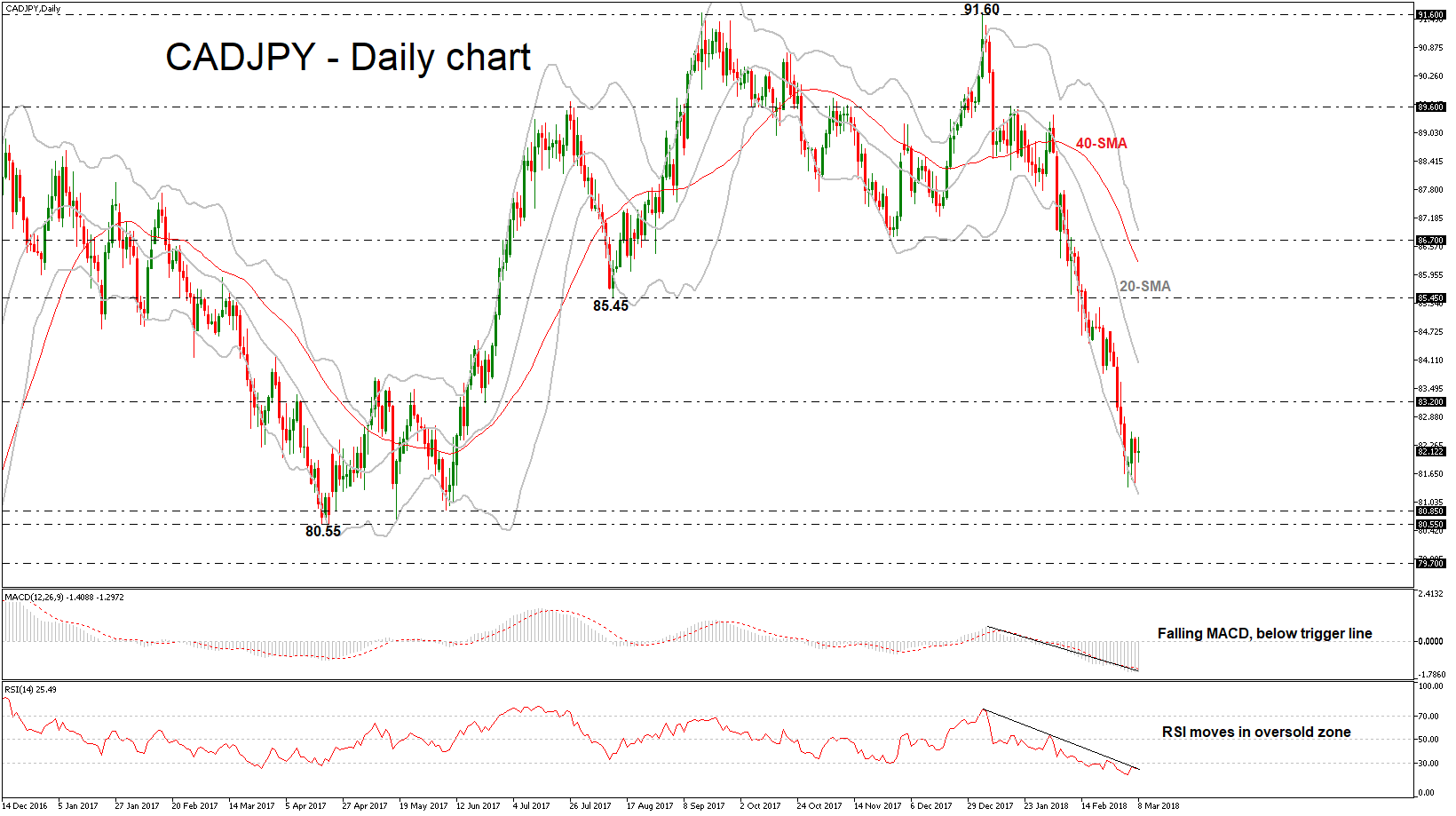

CADJPY Posts Aggressive Bearish Move; Holds Near 9-Month Low

CADJPY has been plunging since the pullback on the 91.60 resistance level. The pair posted three consecutive weekly bearish sessions and recorded a fresh 9-month low of 81.36 level, while it touched the lower Bollinger band. The short-term technical indicators are endorsing the aggressive sell-off in the price action.

Technically, in the daily chart, the MACD oscillator continues to strengthen the downwards move below the zero and trigger lines, while the RSI indicator is holding within the oversold zone, suggesting that the negative movement continues.

Further losses should see the June low of 80.85 acting as a major support. A drop below the 80.55 – 0.8085 support zone could reinforce the bearish structure in the short-term and open the way towards the next key level of 0.7970 taken from the high in October 2016.

Conversely, in case of an upside retracement, the price could touch the immediate resistance at 83.20. A jump above this area could open the door for the mid-level of the Bollinger band near 84.00.

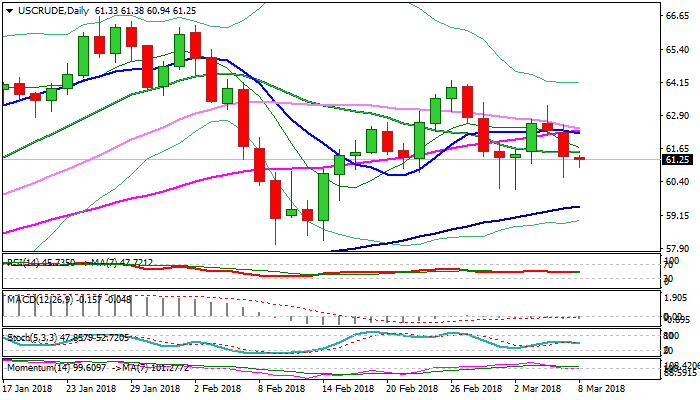

WTI Oil – Daily Cloud Base Holds for Now But Risk for Further Weakness Persists

WTI oil remains in red on Thursday as negative sentiment increased after downbeat supply data on Wednesday, which added to existing pressure on concerns over possible trade war. Fresh downside attempts on Thursday were so far contained by the base of thick daily cloud ($60.91) after previous day's dip to below cloud base was short-lived. Techs continue to work in favor of bears as daily MA's returned to bearish setup and 14-d momentum is probing into negative territory. Bears look for eventual close below cracked support at $61.32 (Fibo 61.8% of $60.12/$63.26 upleg) to generate fresh bearish signal which would be reinforced by close below cloud base, for final push towards key support at $60.12 (02 Mar trough). Immediate downside risk would remain on hold while cloud base hold, but close above broken 20SMA ($61.55) is needed generate initial bullish signal.

Res: 61.55; 61.91; 62.25; 62.63

Sup: 60.91; 60.57; 60.12; 59.48

Sunset Market Commentary

Markets

German Bunds opened in positive territory, but gradually returned the initial gains as global sentiment on risk improved. Investors were also looking forward to the ECB policy announcement. In the policy statement, the ECB omitted its easing bias as it didn't repeat its intention to increase bond buying if necessary. European yields jumped up to 4 bp higher upon the publication of the statement. During the ECB press conference, the 2018 growth forecast was revised slightly higher but the bank decreased the inflation forecast for 2019. The ECB president admitted that the change in the language on QE was unanimous, but at the same time said that no victory can't be declared on inflation yet. The initial rise in EMU interest rates was reversed during the press conference. At the time of writing, German yields are little changed across the curve. On the intra-EMU bond markets, yield spread chances versus Germany mostly narrowed further with Greece (-10bp), Spain and Portugal (-6/-5bp) outperforming and Italy (+4bp) underperforming. The changes in US Treasury yields are much more contained. Markets' angst on an outright trade war eased, but the issue of the US putting import tariffs in place isn't out of the way yet. US yields decline between 0.6 bp (2-y) and 3.0 bp (30-y) in rather volatile trading.

The dollar gained modest ground against the euro and yen as risk sentiment on improved. Investor fears on an outright trade war eased as the White House indicated that import tariffs could be applied in a selective way. The euro jumped temporary higher as the ECB dropped its indication that it could still raise the amount of asset purchases if needed. However, the euro strength was short-lived as other elements in the ECB assessment were little changed. Draghi indicated that the removal of this easing bias should be considered as mostly backward looking. The ECB president also said that the EBC is monitoring FX volatility as a factor in its policy assessment. In line with EMU yields, the euro reversed initial gains during the press conference. EUR/USD trades currently in the 1.2350 area, slightly lower on a daily basis. USD/JPY is little changed hovering near the 106 level.

Sterling trading was mostly driven by global factors today as there were no important UK eco data. EUR/GBP mostly followed the intraday swings of the single currency due the ECB policy statement and during the ECB press conference. The pair trades marginally lower on a daily basis. (currently 0.8915 area). The post-Drahgi reversal of EUR/USD is also slightly weighing on cable. The pair trades currently in the 1.3850 area.

News Headlines

German factory orders declined a bigger than expected 3.9% M/M in January. The consensus estimate only expected a decline of 1.8% M/M. Orders for German factories were still 8.2% higher compared to the same month last year. A sharp fall in orders from other EMU countries was the culprit behind the decline. Statistical issues with respect to year-end factory closures might have distorted the data.

Ratings agency Moody's cut Turkey's sovereign rating one notch further into junk territory. The rating was put at Ba2 with a stable outlook. Moody's said the government appears to be focused on short-term measures. It also mentioned erosion of the strength of the country's institutions and the increased risks from its current account deficit.

The Italian League Party is rumoured to hold informal talks with dissidents of the center-left Democratic Party to seek support for a governing alliance. Both parties didn't answer questions on the issue.

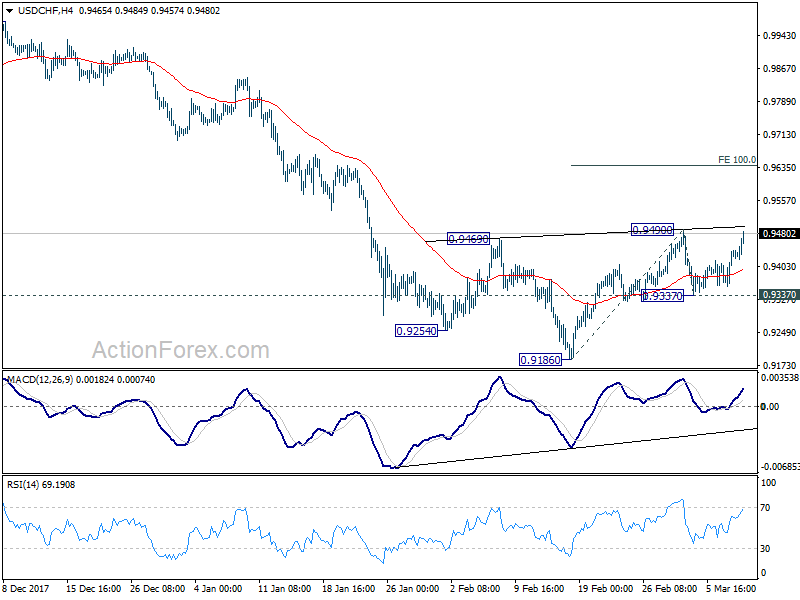

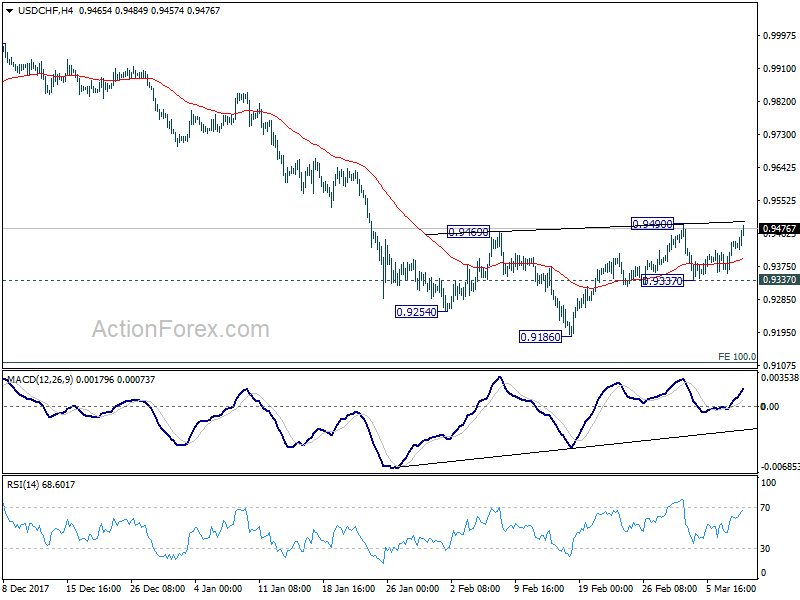

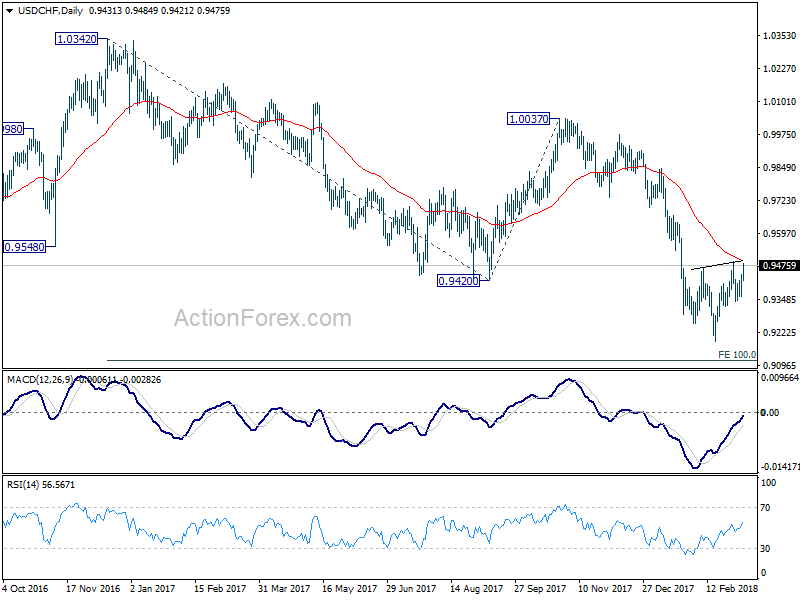

USD/CHF forming head and shoulder bottom

USD/CHF is a pair to watch for the rest of US session as it's pressing 0.9490 resitsance. Break there will complete a head and shoulder bottom pattern. LS: 0.9254, H: 0.9186, RS: 0.9337. In that case, further rise would be seen to 100% projection of 0.9186 to 0.9490 from 0.9337 at 0.9464. And as USD/CHF could have reversed its down trend, there would be prospect of a test on 0.9977 further down the road. But agian, that's subject to a solid break of 0.9490 first.

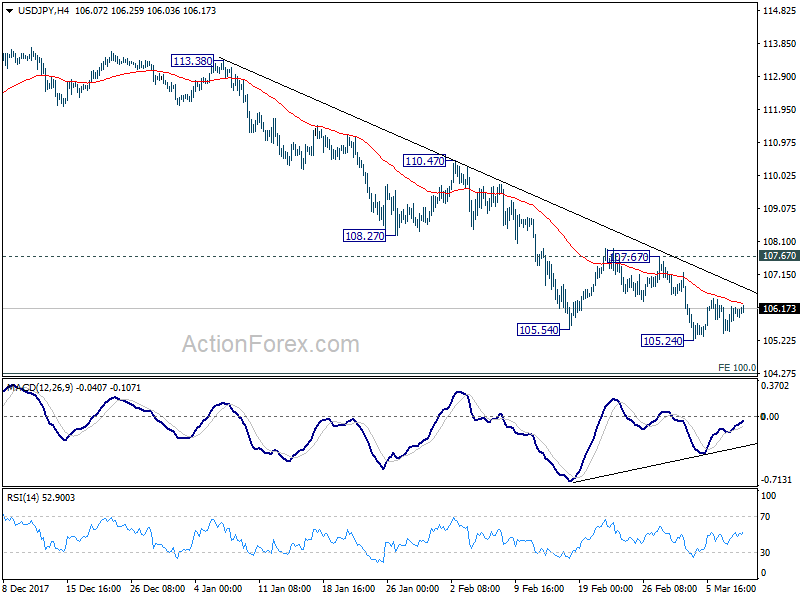

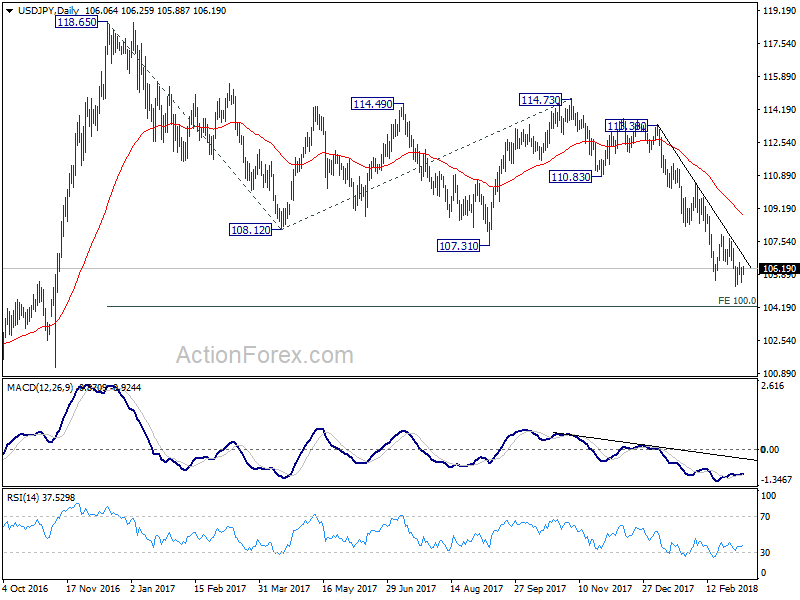

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.60; (P) 105.91; (R1) 106.37; More...

USD/JPY continues to be bounded in consolidation above 105.24 and intraday bias remains neutral. With 107.67 resistance intact, near term outlook stays bearish and further fall is expected. On the downside, break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will pave the way to 98.97 key support level and below. However, break of 107.67 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 55 day EMA (now at 108.93) first.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9380; (P) 0.9411; (R1) 0.9465; More...

USD/CHF rises to as high as 0.9484 and focus in now on 0.9490 resistance. Break till revive the case of near term reversal. And that is supported by head and shoulder bottom pattern (ls: 0.9254, h: 0.9186, rs: 0.9337). In that case, near term outlook will be turned bullish for a test on 1.0037 resistance. Nonetheless, break of 0.9337 should send USD/CHF through 0.9186 to resume larger down trend to 0.9115 projection level.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

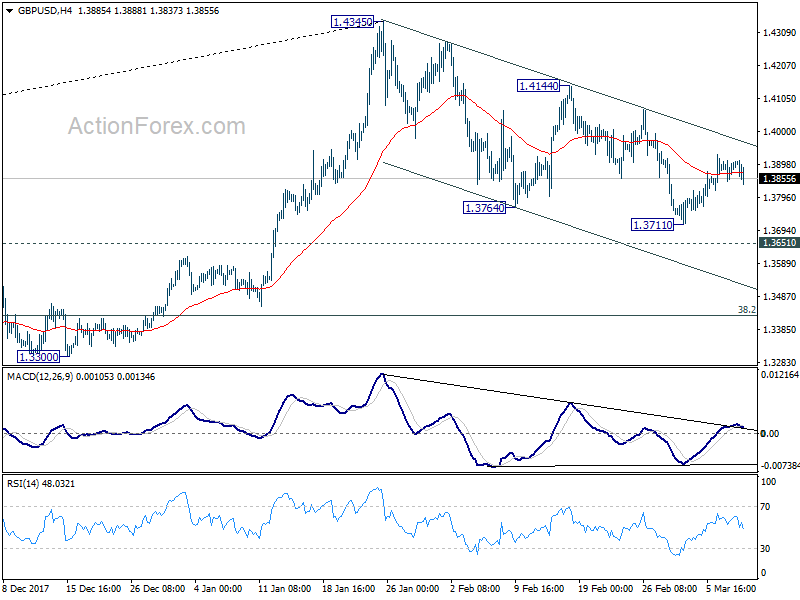

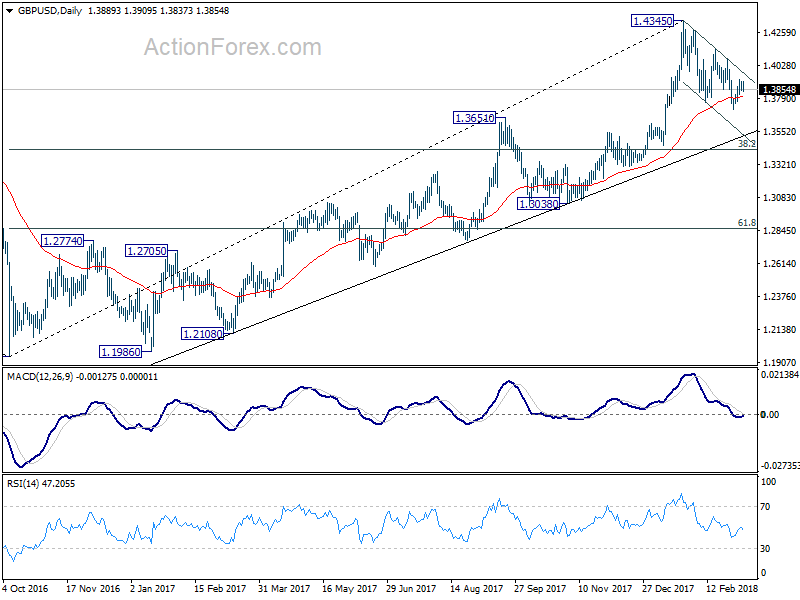

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3862; (P) 1.3887; (R1) 1.3928; More....

GBP/USD is struggling to stay above 4 hour 55 EMA but for the moment it's kept well above 1.3177 temporary low. Intraday bias remains neutral first. As noted before, decline from 1.4345 is in favor to extend with 1.4144 resistance intact. Below 1.3711 will resume the fall from 1.4345 through 1.3651 resistance turned support. We'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

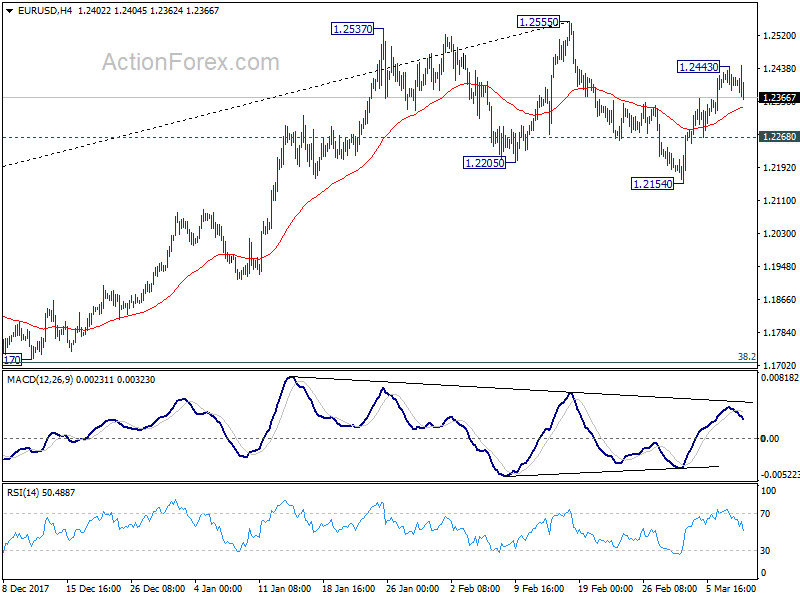

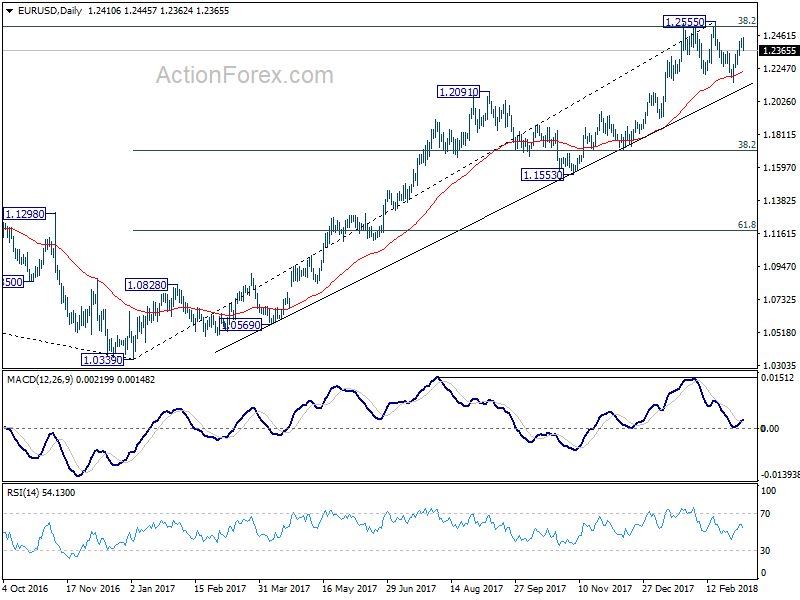

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2413 (R1) 1.2441; More....

EUR/USD edges higher to 1.2445 but fails to sustain gain above 1.2443 temporary top. Intraday bias remains neutral first and some more consolidative could be seen. For now, further rise will remain mildly in favor as long as 1.2268 minor support holds. Firm break of of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corr

ective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

ective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.