Sample Category Title

Euro Struggles to Gain as ECB Draghi Talks Down Even Tiny Step of Exit

Euro is initially short up as ECB turned a bit less dovish in the statement after keeping monetary policy unchanged. However, the common currency cannot extend gains as there is no follow through buying. More importantly, ECB President Mario Draghi tries to tone down the significance of the change in the post meeting pressing conference. For now, EUR/USD is still trading below 1.2443 minor resistance, EUR/GBP below 0.8967, EUR/JPY below 132.01. The only exception is EUR/CHF, which is marching on 1.17 today and is on course for 1.1821 key resistance.

Elsewhere, Canadian Dollar is trading as the strongest major currency today on relief that Canada will be exempted from US President Donald Trump's steel and aluminum tariff. Dollar trading seems to be relieved too as the greenback is following the Loonie as the second strongest for today. DOW opens the day higher and is up around 100 pts at the time of writing. It could be having a taken of the difficult 25000 handle again.

ECB takes tiny step in exit, but Draghi still talks it down

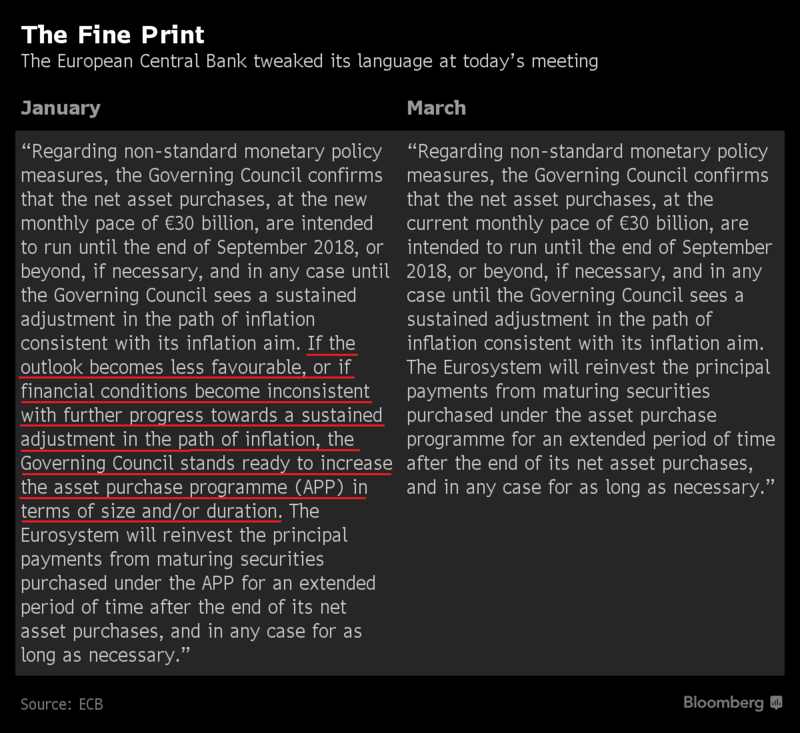

ECB left the main refinancing rate unchanged at 0.00% today as widely expected. The marginal lending facility rate and deposit facility rate are held at 0.25% and -0.40% respectively. The program to buy EUR 30b assets per month till September is also held unchanged. The most important part of the policy statement is that the option to "expand" the asset program is taken out. That is, the following texts are omitted from today's statement:

"If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration."

But later in the post meeting press conference, Draghi tried to tone down the change. . While the decision was unanimous, Draghi emphasized that it's just removing "explicit reference" to the chance of increasing the size of the APP again. However, firstly, ECB will keep interest rate at the current level for an extended period after the APP ends. And secondly ECB is still keeping the option to "extend" the APP beyond September.

ECB also released updated economic projections. There are little changes except that growth in 2018 is expected to be slightly faster at 2.4%. 2019 inflation projection is lowered by 0.1% to 1.4%.

GDP

- 2018 at 2.4% vs 2.3% prior

- 2019 at 1.9% vs 1.9% prior

- 2020 at 1.7% vs 1.7% prior

Inflation

- 2018 at 1.4% vs 1.4%

- 2019 at 1.4% vs 1.5%

- 2020 at 1.7% vs 1.7%

Released earlier in European session, German factory orders dropped -3.8% mom in January. Swiss unemployment rate was unchanged at 2.9% in February.

Trump's tweet in-line with expectation of exemptions of Canada and Mexico in tariff

Trump will be formally signing the order on 25% steel and 10% aluminum tariff today. Trump tweeted this morning that "looking forward to 3:30 P.M. meeting today at the White House. We have to protect & build our Steel and Aluminum Industries while at the same time showing great flexibility and cooperation toward those that are real friends and treat us fairly on both trade and the military."

The message is so far in line with market expectations that Canada and Mexico will be given temporary exemption on the tariffs while NAFTA negotiation is carrying on.

Released from US, initial jobless claims rose 21k to 231k in the weekended Mar 3. Prior week's 210k was the lowest since 1969. Four week moving average rose 2k to 222.5k. Continuing claims dropped 65k to 1.87m in the week ended February 24.

From Canada, housing starts rose to 229.7k in February, above expectation of 220k. New Housing price index rose 0.0% mom in January versus expectation of 0.1% mom. Building permits rose 5.6% mom in January versus expectation of 1.3% mom.

Australia recorded massive AUD 1.06b trade surplus in January

Australia recorded massive trade surplus of AUD 1.06b in January, a turnaround from December's AUD -1.15b trade deficit. Exports jumped 4% mom to AUD 33.9b, with 4% rise in non-rural goods, 54% rise in non-monetary gold. Much more than offsetting -8% fall in rural goods. Imports, on the other hand, dropped -2% to AUD 32.9b. Consumption goods dropped -7%, non-monetary gold dropped -19%, capital goods dropped 1%.

China pledges "justified and necessary response" to trade wars"

China Foreign Minister Wang Yi pledged to have "justified and necessary response" to trade wars. He said that "A trade war has never been the right way to solve the problem, especially under globalization." And, these conflicts "will only harm everyone and China will surely make a justified and necessary response."

At the same time China's trade surplus widened to USD 33.7b in January, or CNY 225b. Both were way better than expectation of USD -8.5b or CNY -71b deficit. Exports rose 44.5% yoy. Imports rose 6.3% yoy.

From Japan, Q4 GDP was finalized at 0.4% qoq, revised up from 0.1% qoq. GDP deflator was revised up to 0.1% yoy.

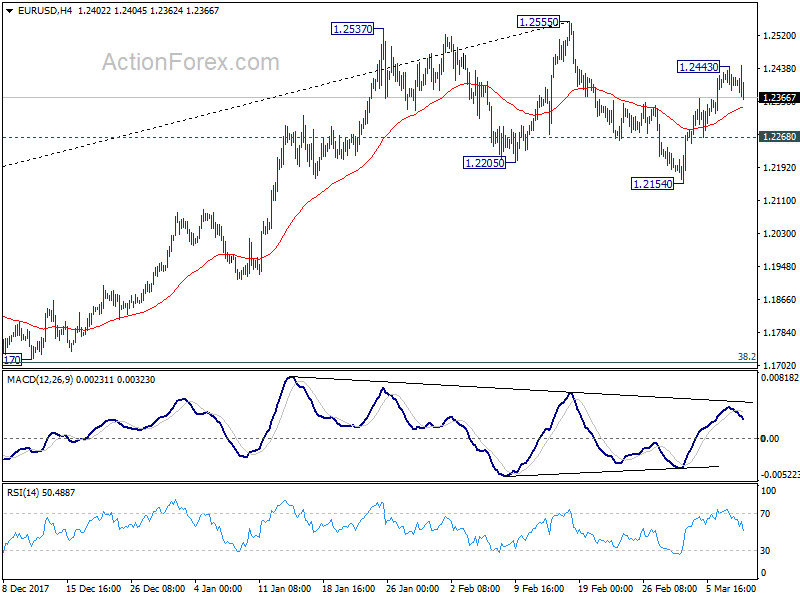

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2413 (R1) 1.2441; More....

EUR/USD edges higher to 1.2445 but fails to sustain gain above 1.2443 temporary top. Intraday bias remains neutral first and some more consolidative could be seen. For now, further rise will remain mildly in favor as long as 1.2268 minor support holds. Firm break of of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

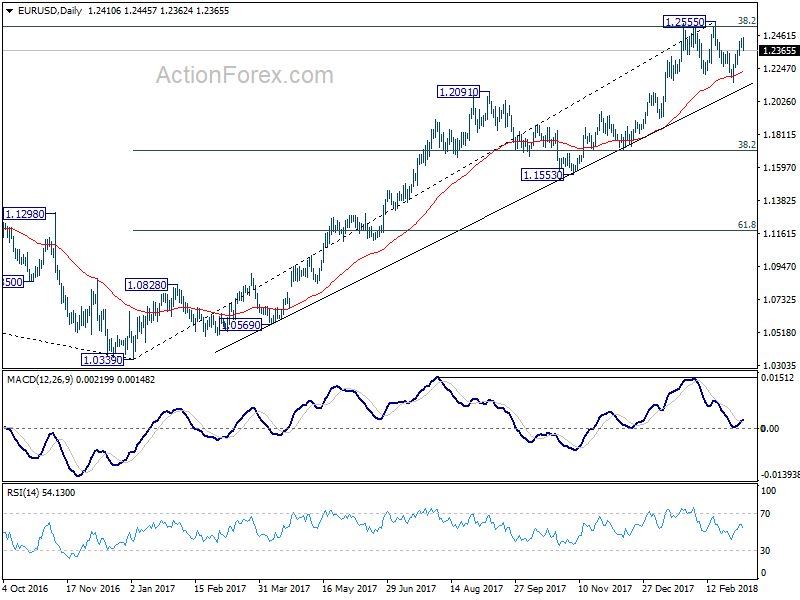

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q4 | 2.80% | 0.50% | ||

| 23:50 | JPY | Current Account (JPY) Jan | 2.02T | 1.76T | 1.48T | 1.68T |

| 23:50 | JPY | GDP Q/Q Q4 F | 0.40% | 0.20% | 0.10% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 F | 0.10% | 0.00% | 0.00% | |

| 00:01 | GBP | RICS House Price Balance Feb | 0% | 7% | 8% | |

| 00:30 | AUD | Trade Balance Jan | 1.06B | 0.22B | -1.36B | -1.15B |

| 02:00 | CNY | Trade Balance (USD) Feb | 33.7B | -8.5B | 20.3B | |

| 02:00 | CNY | Trade Balance (CNY) Feb | 225B | -71B | 136B | |

| 06:45 | CHF | Unemployment Rate Feb | 2.90% | 2.90% | 3.00% | |

| 07:00 | EUR | German Factory Orders M/M Jan | -3.90% | -1.60% | 3.80% | 3.00% |

| 12:30 | USD | Challenger Job Cuts Y/Y Feb | -4.30% | -2.80% | ||

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | 0.00% | |

| 13:15 | CAD | Housing Starts Feb | 229.7K | 220K | 216K | 215.3K |

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.00% | 0.10% | 0.00% | |

| 13:30 | CAD | Building Permits M/M Jan | 5.60% | 1.30% | 4.80% | 2.50% |

| 13:30 | USD | Initial Jobless Claims (MAR 3) | 231K | 216K | 210K | |

| 15:30 | USD | Natural Gas Storage | -58B | -78B |

Euro staying in range as Draghi tones down language change

Euro fails to extend gain as Draghi tried to tone down the change in language. While the decision was unanimous, Draghi emphasized that it's just removing "explicit reference" to the chance of increasing the size of the APP again. However, firstly, ECB will keep interest rate at the current level for an extended period after the APP ends. And ECB is still keeping the option to "extend" the APP beyond September.

Here are the updated economic projections:

GDP

- 2018 at 2.4% vs 2.3% prior

- 2019 at 1.9% vs 1.9% prior

- 2020 at 1.7% vs 1.7% prior

Inflation

- 2018 at 1.4% vs 1.4%

- 2019 at 1.4% vs 1.5%

- 2020 at 1.7% vs 1.7%

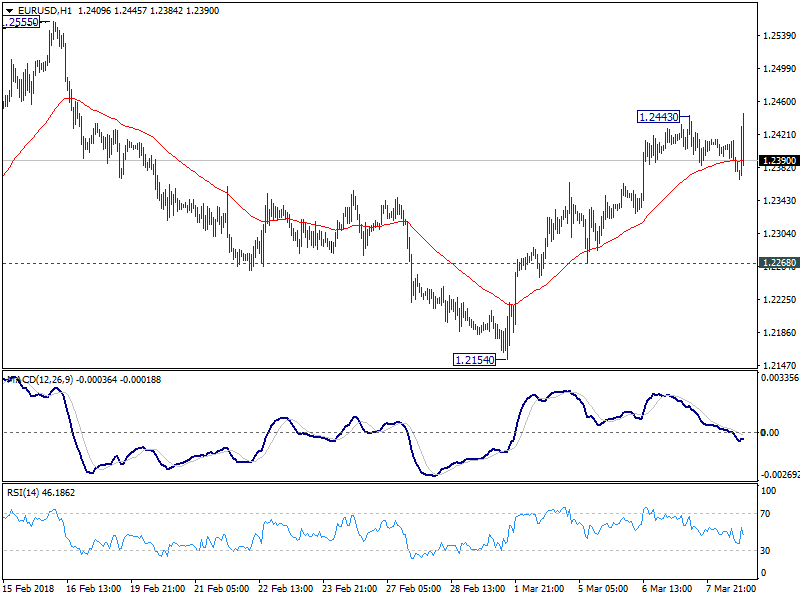

EUR/USD fails 1.2443 so far. Draghi’s press conference script.

EUR/USD tries to break 1.2443 as ECB turned less dovish in the statement. But no follow through buying seen yet.

(ECB) Introductory Statement to the Press Conference

Mario Draghi, President of the ECB,

Vítor Constâncio, Vice-President of the ECB,

Frankfurt am Main, 8 March 2018

INTRODUCTORY STATEMENT

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today's meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.

Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will continue to reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

Incoming information, including our new staff projections, confirms the strong and broad-based growth momentum in the euro area economy, which is projected to expand in the near term at a somewhat faster pace than previously expected. This outlook for growth confirms our confidence that inflation will converge towards our inflation aim of below, but close to, 2% over the medium term. At the same time, measures of underlying inflation remain subdued and have yet to show convincing signs of a sustained upward trend. In this context, the Governing Council will continue to monitor developments in the exchange rate and financial conditions with regard to their possible implications for the inflation outlook. Overall, an ample degree of monetary stimulus remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term. This continued monetary support is provided by the net asset purchases, by the sizeable stock of acquired assets and the forthcoming reinvestments, and by our forward guidance on interest rates.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP increased by 0.6%, quarter on quarter, in the fourth quarter of 2017, after increasing by 0.7% in the third quarter. The latest economic data and survey results indicate continued strong and broad-based growth momentum. Our monetary policy measures, which have facilitated the deleveraging process, continue to underpin domestic demand. Private consumption is supported by rising employment, which is also benefiting from past labour market reforms, and by growing household wealth. Business investment continues to strengthen on the back of very favourable financing conditions, rising corporate profitability and solid demand. Housing investment has improved further over recent quarters. In addition, the broad-based global expansion is providing impetus to euro area exports.

This assessment is broadly reflected in the March 2018 ECB staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.4% in 2018, 1.9% in 2019 and 1.7% in 2020. Compared with the December 2017 Eurosystem staff macroeconomic projections, the outlook for real GDP growth has been revised up for 2018 and remains unchanged for 2019 and 2020.

The risks surrounding the euro area growth outlook are assessed as broadly balanced. On the one hand, the prevailing positive cyclical momentum could lead to stronger growth in the near term. On the other hand, downside risks continue to relate primarily to global factors, including rising protectionism and developments in foreign exchange and other financial markets.

According to Eurostat's flash estimate, euro area annual HICP inflation decreased to 1.2% in February 2018, from 1.3% in January. This reflected mainly negative base effects in unprocessed food price inflation. Looking ahead, on the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around 1.5% for the remainder of the year. Measures of underlying inflation remain subdued overall. Looking forward, they are expected to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

This assessment is also broadly reflected in the March 2018 ECB staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.4% in 2018, 1.4% in 2019 and 1.7% in 2020. Compared with the December 2017 Eurosystem staff macroeconomic projections, the outlook for headline HICP inflation has been revised down slightly for 2019 and remains unchanged for 2018 and 2020.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual rate of growth of 4.6% in January 2018, unchanged from the previous month, reflecting the impact of the ECB's monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 remained the main contributor to broad money growth, continuing to expand at a solid annual rate.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is progressing. The annual growth rate of loans to non-financial corporations strengthened to 3.4% in January 2018, after 3.1% in December 2017, while the annual growth rate of loans to households remained unchanged at 2.9%. The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for an ample degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Against the background of overall limited implementation of the 2017 country-specific recommendations, as communicated by the European Commission yesterday, greater reform effort is necessary in the euro area countries. Regarding fiscal policies, the increasingly solid and broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Deepening Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.

ECB Drops Easing Bias, EUR Climbs

As expected by many, the European Central Bank (ECB) have held rates steady, but tweaked some of the language at its monetary policy decision.

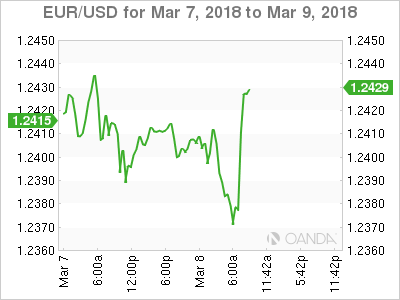

The EUR (€1.2423) has rallied after the ECB dropped its easing bias – referring to the option to increase asset purchases under its quantitative easing (QE) program if the eurozone economy deteriorates.

Still, the ECB reiterated that bond purchases “are intended to run until the end of September 2018, or beyond, if necessary.”

Germany’s 10-year Bund yield briefly backed up to +0.70% after the ECB announcement. It had traded at +0.67% before the decision.

Germany’s 10-year Bund yield briefly backed up to +0.70% after the ECB announcement. It had traded at +0.67% before the decision.

ECB President Mario Draghi is due to hold a press conference at 08:30 am EST.

US initial jobless claims rose 21k to 231k

US initial jobless claims rose 21k to 231k in the weekended Mar 3. Prior week's 210k was the lowest since 1969. Four week moving average rose 2k to 222.5k. Continuing claims dropped 65k to 1.87m in the week ended February 24.

From Canada, housing starts rose to 229.7k in February, above expectation of 220k. New Housing price index rose 0.0% mom in January versus expectation of 0.1% mom. Building permits rose 5.6% mom in January versus expectation of 1.3% mom.

Markets are now listening to ECB Draghi's press conference, and await Trump's order of steel and aluminum tariffs

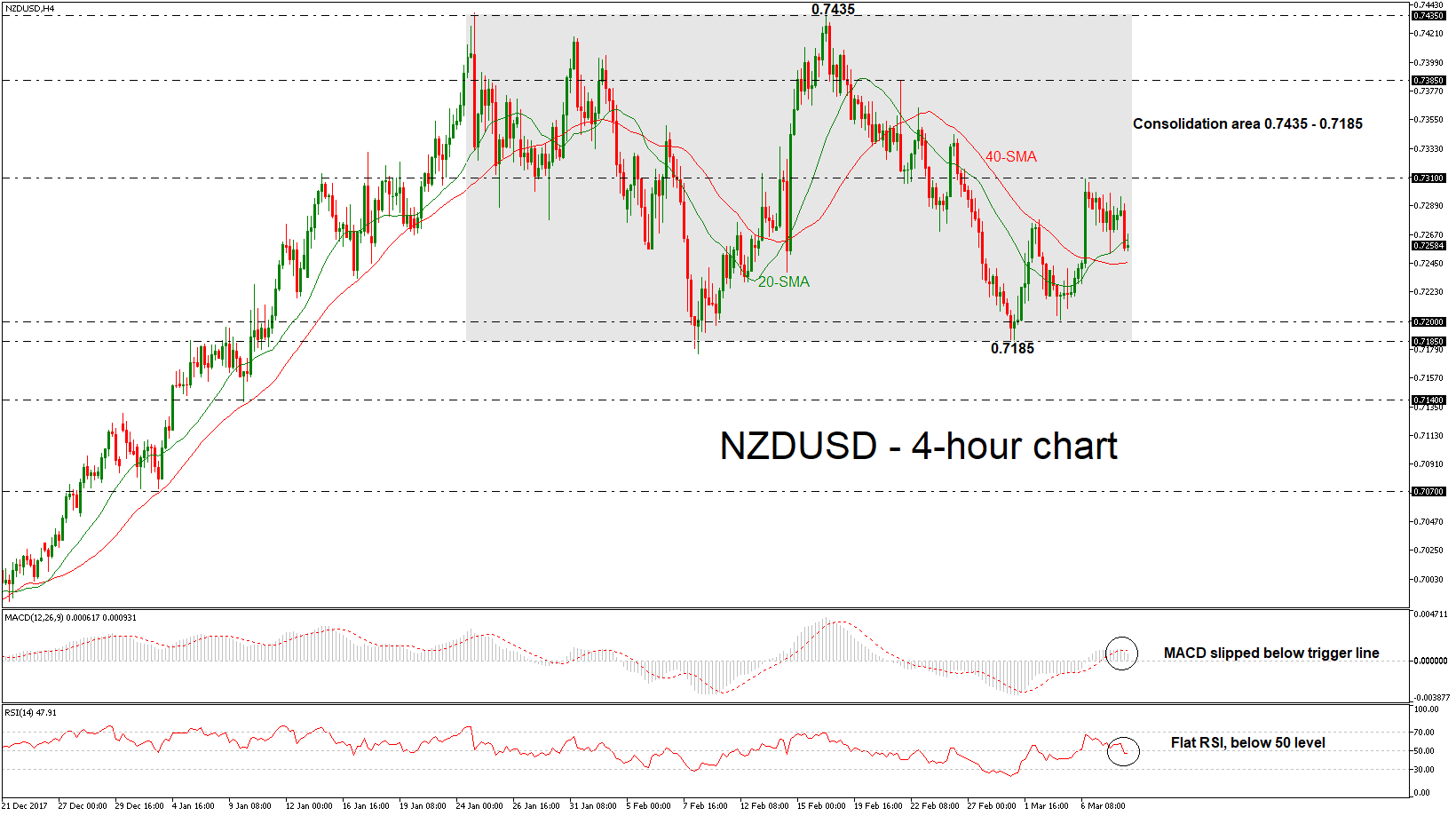

NZDUSD Stands in Sideways Channel; Negative Movement is Forecasted

NZDUSD edged sharply lower in the previous session while is paring some losses the last hours. The price has been consolidating within a trading range with upper boundary the 0.7435 resistance level and lower boundary the 0.7185 support barrier since January 24. When looking at the bigger picture the pair lacks a clear trend after its rally from 0.6780 stalled at 0.7435.

In the 4-hour chart, momentum indicators are also pointing to a continuation of the sideways channel but with a downside risk. The MACD oscillator is standing below the trigger line and slightly above the zero line with weak momentum. Also, the RSI indicator dropped below the 50 level and is flattening.

If the price extends its losses below the 40-simple moving average of 0.7245, it could open the door for the 0.7185 – 0.7200 support area. A penetration of the aforementioned range could drive the pair towards the next support at 0.7140.

On the flip side, in the event of an upside reversal, the next level to watch is the 0.7310 resistance barrier. Further gains could push the price until the 0.7385 level.

Into ECB & NAFT

Markets stabilise on reports that Trump will expempt NAFTA countries from tariffs. As we move to the ECB press conference, all currencies are down against the USD while US indices bounce off their 100-DMA and attempt breaching their 55 DMAs. Draghi's press conference will focus on the ECB's latest revisions for growth and inflation and any takes with regards to trade wars and the FX implications. EURUSD pushed higher after the ECB rates announcement removed the reference to the possibility of increasing the QE program if necessary.

The focus was squarely on the Canadian dollar on Wednesday and it delivered a tumultuous day. The loonie slumped after the Bank of Canada highlighted trade worries and household debt. A s a result USD/CAD climbed to 1.3000 from 1.2910.

But some of those worries may be quickly calmed if reports that Trump will exempt NAFTA countries from the tariffs prove to be true. The market reacted by erasing the move in USD/CAD and sending it back to 1.2900. The possibility of a waiver was something we warned about yesterday. The that shift also helped stock markets recover into a flat close.

In the bigger picture, the landscape remains deeply unsettled. Relief for Canada and Mexico might be coming but that leaves the rest of the world still subject to a harsh tariff and a high likelihood of retaliation. Cohn's exit may also highlight that tariffs and are part of a broader White House agenda that he wasn't comfortable with.

Another troubling development was an increase in the US trade deficit in January to $56.6B compared to $55.0B expected, including a record in the deficit excluding petroleum. The sharp deterioration in the past four months suggests the tax cut funds are adding to imports at the margin and that could accelerate. In turn, that will make Trump more likely to take dramatic actions on trade.

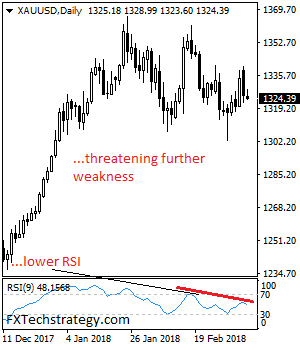

Gold: Takes Back Gain, Sets Up To Weaken Further

GOLD: The commodity closed lower after backing off higher prices on Wednesday. On the downside, support comes in at the 1,330.00 level where a break will turn attention to the 1,320.00 level. Further down, a cut through here will open the door for a move lower towards the 1,310.00 level. Below here if seen could trigger further downside pressure targeting the 1,300.00 level. Conversely, resistance resides at the 1,340.00 level where a break will aim at the 1,350.00 level. A turn above there will expose the 1,360.00 level. Further out, resistance stands at the 1,370.00 level. All in all, GOLD looks to weaken further.

Euro mildly higher as ECB drops pledge to increase QE if necessary

Euro jumps slightly after ECB kept interest rates unchanged at 0.00%. More importantly, ECB dropped the pledge to "increase" the size of QE if necessary. That is "If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration." is omitted from from today's statement.

Below are the March 8 and January 25 statement for reference. But for now, EUR/USD is staying below 1.2443 temporary top as we await Draghi's press conference.

March 8 Statement (Today)

At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

January 25 statement

At today's meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the net asset purchases, at the new monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. If the outlook becomes less favourable, or if financial conditions become inconsistent with further progress towards a sustained adjustment in the path of inflation, the Governing Council stands ready to increase the asset purchase programme (APP) in terms of size and/or duration. The Eurosystem will reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.