Sample Category Title

ECB Monetary Policy Decisions

At today’s meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.

Regarding non-standard monetary policy measures, the Governing Council confirms that the net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Dollar Waits for Tariff Ceremony; European Stocks Inch Up ahead of ECB Rate Decision

Here are the latest developments in global markets:

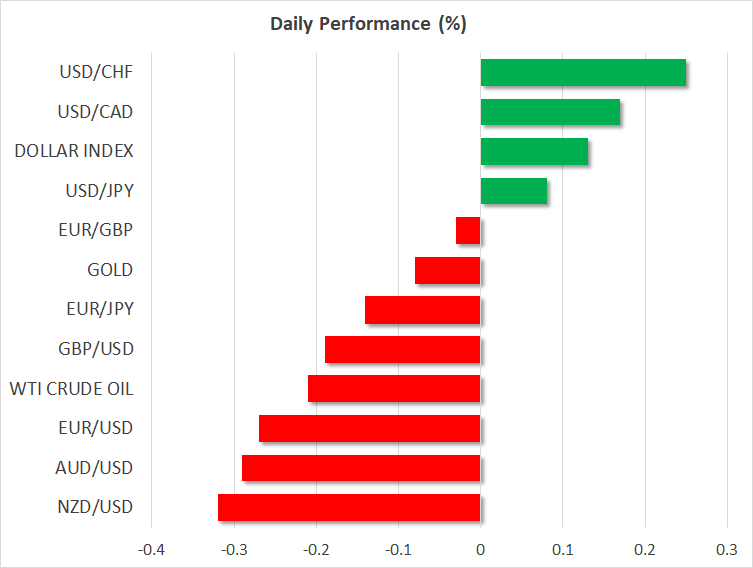

FOREX: The dollar index found the opportunity to crawl up to 89.81 (+0.19%) and dollar/yen climbed to 106.13 (+0.08%) in early European afternoon as investors were waiting for more details on Trump’s import tariffs and were particularly eager to hear if any countries would get exemptions. Euro/dollar traded lower at 1.2370 (-0.34%) ahead of the ECB rate announcement where any clues on the ECB’s plans to change its forward guidance on monetary policy could bring fresh volatility to the currency. A strict language on the trade front could wake euro bears up. Pound/dollar was on a downtrend amid Brexit uncertainties, reaching 1.3856 (-0.32%). The UK trade minister, Liam Fox, said on Thursday that punishing the UK for leaving EU “is language of a gang” and not in the interest of EU members, signaling that a transition deal will not be on the table by the end of this month as Finance Minister, Philip Hammond, claimed on Wednesday. Meanwhile in the monetary front, a Reuters poll showed that 36 out of 63 economists were confident that the Bank of England would raise rates in May and stay pat until the mid of 2019. In antipodean currencies, aussie/dollar and kiwi/dollar retreated to 0.7800 (-0.29%) and 0.7263 (-0.29%) respectively on the back of potential trade risks as Australia and New Zealand are highly exposed to commodity prices which would get into a bearish run if the US tariff measures materialize. Dollar/loonie changed hands at 1.2928 (+0.14%).

STOCKS: European stocks edged up as investors were somewhat relieved after news that Trump could exclude some US allies from his tariff list. However, the gains were not significant and European automakers continued to see their shares falling. The pan-European STOXX 600 and the blue-chip Euro STOXX were up by 0.12% and 0.10% respectively at 1100 GMT led by gains in telecommunication and technology sectors. The German DAX 30, though, tumbled by 0.52% with all sectors being in the red except technology and industrials. The French CAC 40 rose by 0.22% lifted by utilities, the Italian FTSE MIB 100 climbed by 0.17% and the UK’s FTSE 100 was flat. US stock futures were mixed.

COMMODITIES: Oil prices were heading lower as fears of a potential trade war and concerns over a rising US production continued to weigh on the markets. WTI crude and Brent slipped to $61.09 (-0.10%) and $64.17 (-0.26%) per barrel respectively. In precious metals, gold was moving sideways around $1325 (-0.03%) per ounce.

Day ahead: ECB rate decision takes the stage; Trump set to sign import tariffs

Day ahead: ECB rate decision takes the stage; Trump set to sign import tariffs

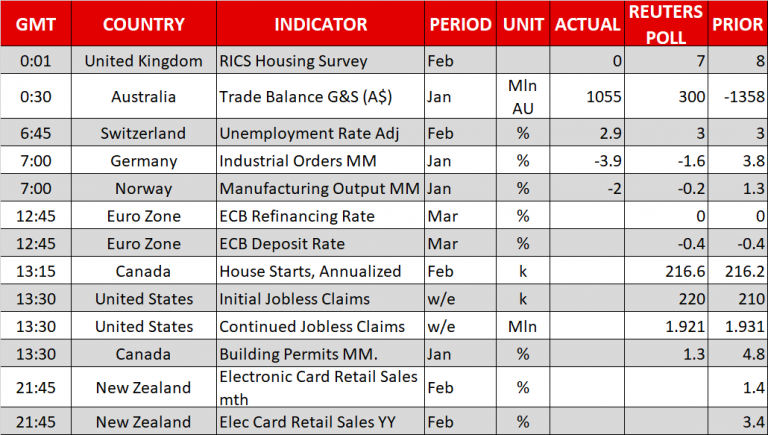

The focus will turn to the European Central Bank (ECB) which concludes its two-day meeting today, with the rate announcement made at 1245 GMT and a press conference by the chief of the central bank Mario Draghi scheduled for 1330 GMT. Following their Canadian and Australian counterparts, ECB policymakers are anticipated to stand pat on interest rates and according to market chatter leave forward guidance on monetary policy unchanged. After a political deadlock in Italy and Trump’s recent tariff proposals on aluminum and steel imports, the ECB will probably hold a cautious tone. Besides, eurozone’s inflation has not shown any significant rise since January’s meeting but instead, it inched lower from 1.3% to 1.2% y/y according to initial CPI estimates for the month of February. The bloc’s economic growth did not gain positive momentum in the fourth quarter of 2017 either as final readings indicated yesterday. Investors will also keep a close eye on the ECB’s growth projections and will be eager to hear any comments on the exchange rate.

In the US, the president is said to formally establish the import tariffs he proposed last week later in the day following the resignation of his chief economic advisor, Gary Cohn on Tuesday, but some officials claimed that this could be postponed to Friday due to legal procedures. According to people with knowledge, the import tariffs which could go into effect in 15 to 30 days after the signing ceremony, are likely to not affect close allies such as Canada and Mexico directly, with Peter Navaro, a top White House trade adviser, saying on Wednesday that “a permanent exclusion will hinge on those countries agreeing to a great trade deal in the ongoing renegotiation of the North American Free Trade Agreement”. Earlier, Trump said that Canada and Mexico could get a 30-day exemption from the planned tariffs and this timeframe could be extended based on progress in NAFTA talks.

In terms of data out of the US, economic releases will be relatively light, with the Department of Labor publishing readings on initial jobless claims at 1330 GMT ahead of the famous nonfarm payrolls due on Friday.

In Canada, the economic calendar will feature figures on February’s housing starts (1315 GMT) and January’s building permits (1330 GMT) with both indicators expected to come in weaker. A speech by the Bank of Canada’s Deputy Governor, Timothy Lane, will also attract attention at 2035 GMT for any comments on the trade front and the central bank’s decision to keep interest rates steady yesterday.

Elsewhere, Japan will report on household spending for the month of January at 2330 GMT. Analysts predict consumer spending to decline sharply by 1.2% on a yearly basis, recording its biggest decline since April. This compares to a fall of 0.1% seen in the previous month.

Meanwhile, the Bank of Japan starts its two-day policy meeting today with the rate announcement scheduled for Friday at 0400 GMT. Predictions are for the BoJ to maintain its loose monetary policy as inflation continues to undershoot its target of 2.0%. It would be interesting though to see whether policymakers are preparing the ground to exit stimulus, something that has been recently echoed.

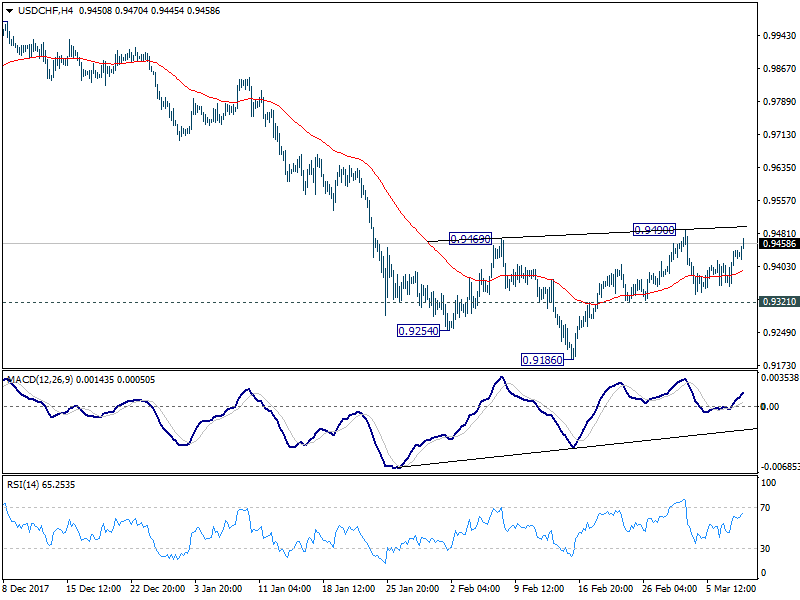

Dollar higher into US session. 0.9490 in USD/CHF watched

Dollar rises broadly entering into a rather busy US session.

ECB will announce rate decision at 12:45 GMT. But focus is on Mario Draghi's press conference at 13:30 GMT.

US will release challenger job cuts, jobless claims.

Canada will release housing starts, building permits, new housing price index.

Also BoC governor Stephen Poloz will speak.

And, Trump will formally sign the order for steel and aluminum tariff. Canada and Mexico are expected to get temporary exemptions.

Based on CHF's broad based weakness, 0.9490 in USD/CHF will be a level to watch.

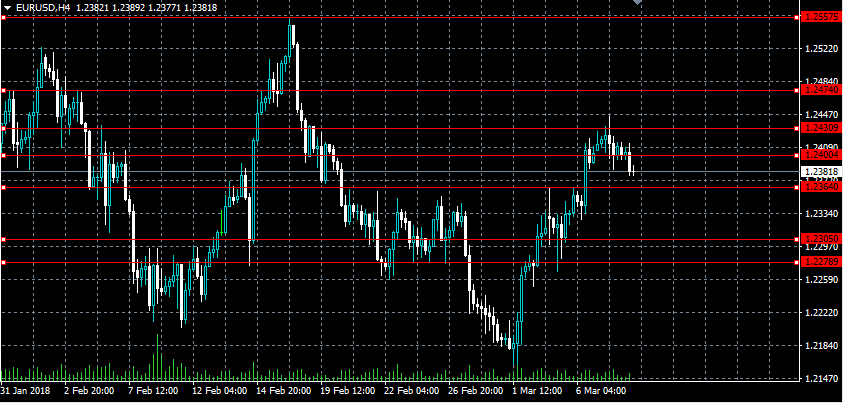

Key EURUSD Levels Ahead Of ECB Decision

The euro continues to consolidate around the 1.2400 handle against the U.S dollar, ahead of today’s ECB interest rate decision and policy statement from European Central Bank President Mario Draghi. The EURUSD pair failed to gain traction above the key 1.2430 level on Wednesday, with traders now taking profits as fears grow ECB President Draghi may discuss the negative impacts of a strong euro currency and U.S trade tariffs. Traders are likely to continue to watch the 1.2430 level for further upside, whilst the 1.2278 now acts as critical weekly support.

The EURUSD is likely to turn bullish above the 1.2430 level, with intraday buyers targeting the 1.2470 and 1.2557 levels.

Should the EURUSD pair fail to move back above the 1.2430 level, price-action may turn bearish toward the 1.2305 and 1.2278 levels.

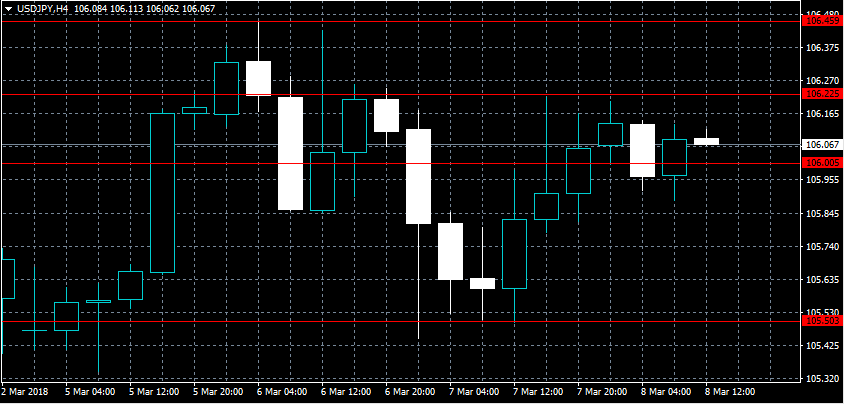

USDJPY Gaining Traction Above 106.00 Level

The U.S dollar has regained upside momentum against the Japanese yen during a quiet European trading session, with intraday buyers reclaiming the 106.00 handle. The USDJPY pair has suffered from depressed trading volumes, with price-action moving in a thirty-point trading-range ahead of a series of market risk-events. USDJPY traders now look towards the upcoming BOJ policy decision and Friday’s Non-farm payrolls job report for February.

The USDJPY pair is likely to edge higher whilst trading above the 106.00 level, further intraday upside towards the 106.22 and 106.45 levels remains possible.

Should USDJPY price-action move convincingly below the 106.00 level, sellers may test towards the 105.50 and 105.24 support regions.

DAX Lower On Soft German Industrial Report, ECB Decision Next

The DAX has lost ground in the Thursday session, after strong gains on Wednesday. Currently, the DAX is trading at 12,205.00, down 0.33% since the Wednesday close. On the release front, German Factory Orders declined 3.9%, weaker than the estimate of -1.9%. This marked the steepest decline since January 2017. Later in the day, the ECB releases its rate decision, followed by a press conference with Mario Draghi.

Global stock markets have been volatile since lat week, when US President Trump stunned investors last week when he proposed stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. Fears of a trade war sent the DAX sharply lower last week, with losses of 5.2%. The DAX has clawed back some of the losses this week, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. This has raised hopes that Trump will back down. However, the unpredictable president could barrel ahead and impose the tariffs, which would likely send global stock markets lower. There was further drama on Wednesday, as Gary Cohn, Trump’s chief economic adviser, resigned. Cohn was a strong advocate of free trade, so his resignation could weaken opposition in the White House to the tariffs. Will Trump make good on his threat or back off? Until the situation is resolved, traders should be prepared for continuing volatility in the markets.

Euro Dips Ahead Of ECB Rate Decision

The euro has edged lower in the Thursday session. Currently, EUR/USD is trading at 1.2376, down 0.28% on the day. On the release front, German Factory Orders declined 3.9%, weaker than the estimate of -1.9%. This marked the steepest decline since January 2017. Later in the day, the ECB releases its rate decision, followed by a press conference with Mario Draghi. In the US, today’s key indicator is unemployment claims.

Investors are keeping a close eye on the ECB, which will set the benchmark rate on Thursday. This will be followed by a press conference with Mario Draghi. Interest rate levels are expected to remain at a flat 0.0%, where they have been pegged for the past two years. What could move the markets, however, is the language used in the press release following the rate decision, as well as Draghi’s press conference. The ECB has continuously included an easing bias, which means that it could increase or extend asset purchases if the economic outlook worsens. If the Bank removes this line, it would represent a less dovish stance, which could push the euro higher. Starting in January, the ECB reduced its monthly asset purchases to EUR 30 billion, and this stimulus program is scheduled to wind up in September. The Bank could extend purchases past this date, although such a move would likely not stir up the markets.

Investors continue to track the latest developments in the tariff crisis, which has shaken up the markets over the past week. President Trump’s threat to impose stiff tariffs on steel imports has infuriated US trading partners, as well as sharp criticism from senior Republican lawmakers. There was further drama on Tuesday, as Gary Cohn, Trump’s chief economic adviser, resigned. Cohnn was a strong advocate of free trade, so his resignation could weaken opposition in the White House to the tariffs. Will Trump make good on his threat or back off? Until the situation is resolved, traders should be prepared for continuing volatility in the markets.

Markets Calm Ahead Of ECB Decision

It's been a relatively calm start to trading on Thursday, as we wait for the latest monetary policy announcement from the ECB and, more importantly, the statement and press conference that accompanies it.

It's not uncommon for markets to be a little quieter in the lead up to major central bank decisions, even those that don't promise to be overly eventful. The ECB extended its bond buying program at the start of the year at a rate of €30 billion per month, with the expiry now pushed back to September this year. It's so far kept its cards close to its chest regarding how it will handle the next taper, but many anticipate it will either end altogether in September or be extended to the end of the year at a reduced rate. Either way, the end of QE is near.

Which of these it opts for, assuming the speculation is accurate, is quite irrelevant, investors are more interested in how long after we can expect the first interest rate hike, with some pencilling one in next year. Anyone hoping to extract this kind of information from the ECB and its President Mario Draghi though will likely be disappointed. Instead, all we're likely to get today is a slight change in the language, with the possible removal of a willingness to increase the asset purchase program in size or duration if the outlook becomes less favourable.

While this may not seem like much, it is the gradual shift in policy stance that policy makers have been alluding to that will signal the end of QE later this year and is indicative of a central bank that is becoming less dovish and more optimistic on the economy. While the recovery remains fragile, the euro area economy is performing well and we are seeing what looks like a sustainable improvement. If that starts to filter through into higher inflation as labour market slack diminishes, it may force the ECB to consider rate hikes earlier than is currently expected.

ECB aside there isn't too much on the radar on Thursday. We'll hear from two Bank of Canada officials, including Governor Stephen Poloz, while US jobless claims are the only notable release on the data side. Traders may have one eye on the US jobs report on Friday, with the Federal Reserve now considering additional rate hikes on the back of tax reform providing additional stimulus in an already strong economy.

Fundamentals: Forex, Gold, Oil & Cryptos

Dollar strength was mitigated by a widening US trade deficit

Resignation of Gary Cohn the Whitehouse is now left without any heavyweight advocate

Forex

Encouraging data on domestic private hiring and labour costs reinforced the view of underlying strength in the US economy pushing it higher against currencies such as the Swiss Franc. However, dollar strength was mitigated by a widening US trade deficit for January, and many investors were favouring the yen as a safe haven asset over the dollar after anxiety of a deterioration of global trade. Despite a strengthening dollar, the euro still managed to make ground against the dollar, now trading above 1.241. Tomorrow, Draghi is likely to err on the side of caution amidst the tightening of global trade tensions. Although Brexit is still causing major headwinds for the Sterling, it too crept higher against the greenback.

Gold

The dollar succeeding to recouping some of yesterday’s losses up 0.2% against a weighted basket of currencies coupled with strengthening US equities saw Gold lose most of yesterday’s gains. However, following the resignation of Gary Cohn, Trump’s top economic adviser, the Whitehouse is now left without any heavyweight advocate of globalisation, reigniting fears of a global trade war which would provide a significant impetus for investors to back the precious metal.

Oil

Forecasts that US Crude Oil inventories increased by 3000k weren’t yet priced into the market as exemplified by the fact that an increase by 2400k was still enough to send US Oil down nearly 2% to $61. With prospects of the likelihood a global trade war increasing after comments that the EU would retaliate to Trump’s tariffs, the oil industry, an industry that thrives off of globalisation, would be negatively impacted.

Cryptocurrency

The cryptocurrency market takes yet another slump after speculation that Binance, one of the world’s largest cryptocurrency trading platforms has been hacked. Bitcoin dips below $10000 but hopefully the continuation of increased adoption in the economy will provide investors with more confidence in this new asset class.

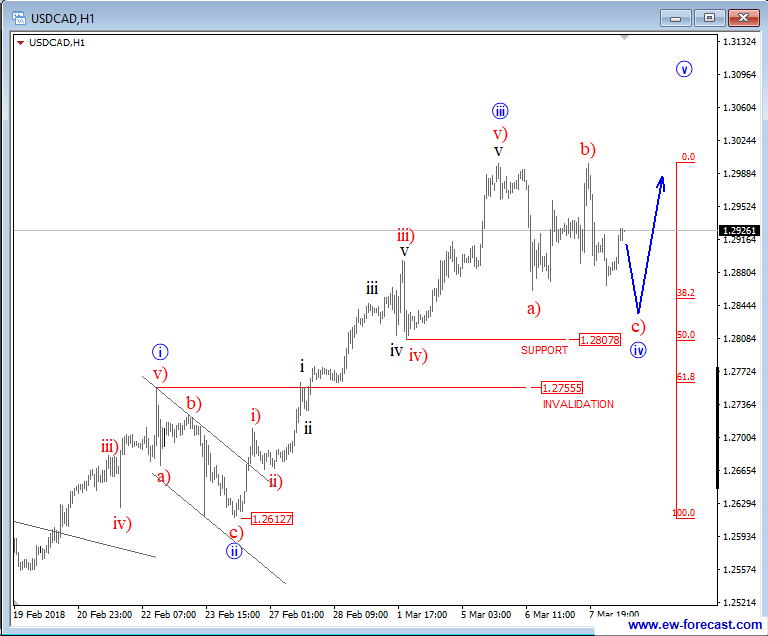

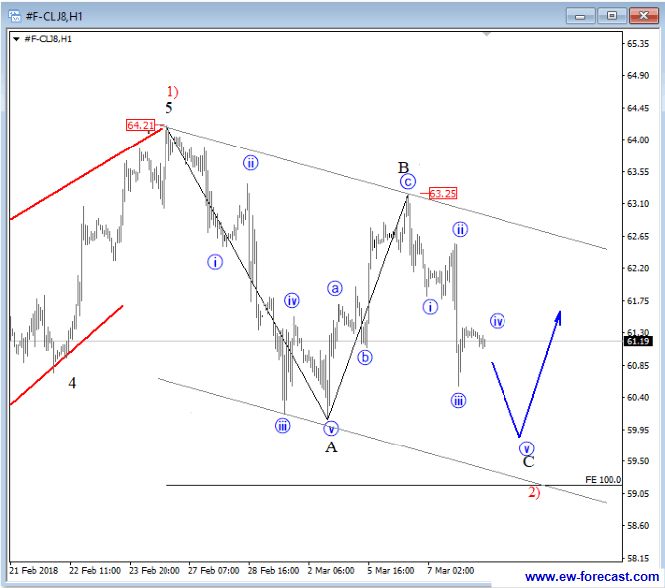

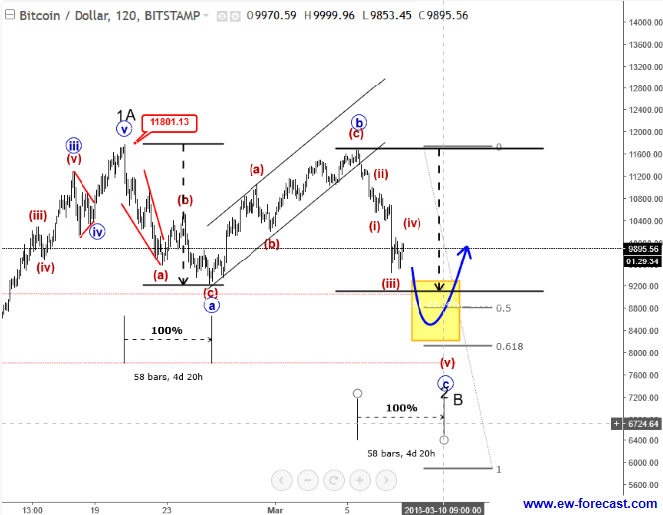

Elliott Wave Analysis: Crude Oil, BTCUSD And USDCAD

Crude oil came lower yesterday but still not into the bear market, as leg down from 63.25 can be wave C of a zigzag down from 64.21 as shown on the updated wave structure. Pay attention to 59.00 area where bounce can occur.

Crude oil, 1H

Crypto market is lower for the last 48 hours and this weakness we can label as wave c. So far there was a nice reaction down, a clear impulse so watch out for a five wave drop before market may see support; ideally, that will be at 8k-9k area, where a new bounce can occur.

BTCUSD, 2H

USDCAD came nicely lower since yesterday; it looks like a wave c) of a three wave structure in wave four which can already be searching for support this morning. Ideally a bounce will come from around 1.2850, while pair trades above 1.2755 invalidation mark.

USDCAD, 1H