Here are the latest developments in global markets:

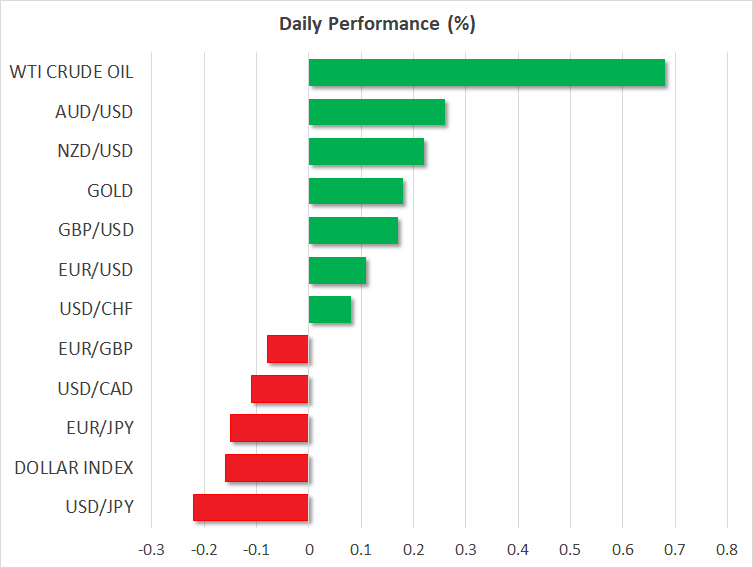

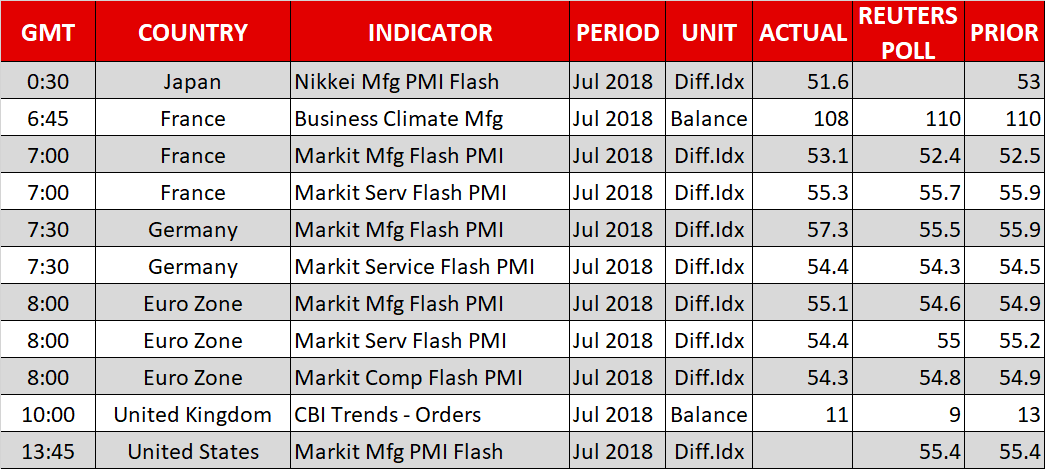

FOREX: The US dollar is showing modest losses versus most currencies. The greenback continued to weaken against the Japanese yen on Tuesday, as dollar/yen fell by 0.15%, approaching the 111.00 psychological level. The US dollar index fell marginally by 0.04%, giving back the gains that it had posted earlier in the day. Preliminary PMI survey data indicated that the eurozone economy lost momentum in July. The IHS Markit composite PMI fell to 54.3 from 54.9 in June, missing the forecast for 54.8. Also, the flash services PMI inched down to 54.4 versus 55.2 before. However, the preliminary manufacturing PMI ticked higher to 55.1 from 54.9 previously, beating expectations for a modest decline. Euro/dollar climbed by 0.07%, holding near 1.1700, while euro/yen retreated by 0.13%. Pound/dollar is trying to pare some of yesterday’s losses, jumping by 0.18% to 1.3124. The antipodean currencies were moving higher with aussie/dollar and kiwi/dollar rising by 0.24% and 0.21% respectively. Meanwhile, dollar/loonie lost some momentum (-0.12%), capped by its 20-day SMA.

STOCKS: European equities were a sea of green on Tuesday, while carmakers and miners were among the biggest winners in the European STOXX 600. The index surged by 0.94%, while the blue-chip Euro STOXX 50 was up by 0.96%. The German DAX 30 jumped by 1.46%, looking set to post a strong bullish day. The French CAC 40 and the Spanish IBEX 35 rose by 0.97% and 0.92% respectively, while the British FTSE 100 advanced by 0.86%. Turning to the US, futures tracking the Dow Jones, S&P 500, and Nasdaq 100 were all in positive territory, pointing to a higher open today.

COMMODITIES: The tensions between the US and Iran remained a market theme, likely helping to drive oil prices higher today. Iran’s foreign ministry replied that the nation will respond with equal countermeasures if the US attempts to block its oil exports. The West Texas Intermediate (WTI) crude oil added 0.71% to its performance, hitting the $68.28 level. Moreover, London-based Brent rose by 0.19% and stood above the $73 handle. In precious metals, gold prices remained slightly above their opening level for the day to $1,225.71, climbing by 0.07%.

Day ahead: US Markit PMIs on the docket; Australian inflation prints to follow

The most noteworthy releases left on the economic calendar for Tuesday will be the US preliminary Markit manufacturing and services PMIs for July, due out at 1345 GMT. Although the market typically pays more attention to the ISM surveys, these could still attract some interest with soiluch a light calendar, particularly since they will provide the first snapshot of how the US economy entered the third quarter.

Both the manufacturing and the services indices are forecast to remain unchanged at 55.4 and 56.5 respectively, levels consistent with solid expansion in both sectors. Investors are currently anticipating a very strong US GDP print for Q2, so any deviation from these forecasts will be closely watched for signs of whether the US economy is gaining, or losing momentum entering Q3. The dollar is likely to move accordingly – higher in case of a data beat, and lower in case of a disappointment.

In energy markets, the private API weekly crude inventory data will attract attention at 2030 GMT.

On the equities front, 3M, Verizon, Harley-Davidson, and AT&T, are among companies releasing quarterly results today. The first three will release their figures before Wall Street’s opening bell, while AT&T will be reporting them after the market close.

A few hours later, during the Asian session Wednesday, aussie-traders will turn their gaze to Australia’s CPI data for Q2, at 0130 GMT. Forecasts are mixed, with the headline inflation rate expected to have risen in yearly terms, the trimmed mean rate projected to remain unchanged, and the weighted median CPI rate anticipated to tick down. In other words, a rise in energy prices may have lifted the overall print, but core measures are likely to show that underlying inflationary pressures remain subdued. To the extent that such prints solidify expectations the RBA will stay on hold over the foreseeable future, they could bring the aussie under renewed selling interest.

{kind=link}