Here are the latest developments in global markets:

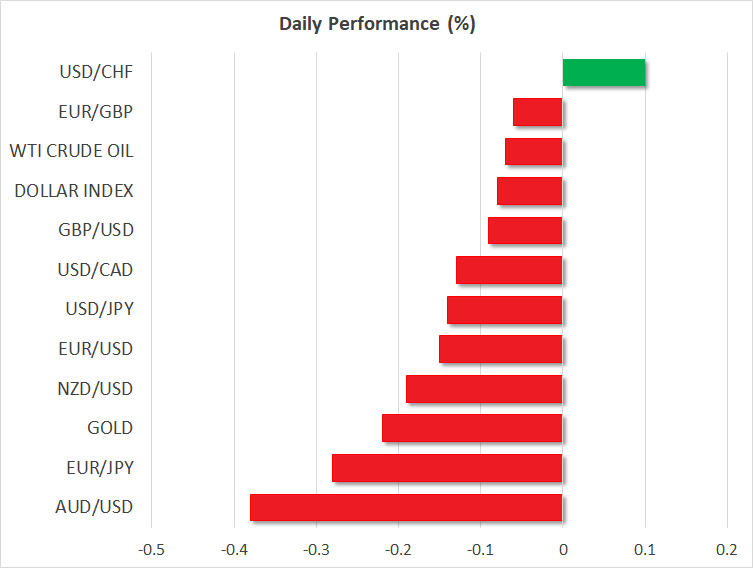

FOREX: The dollar index was down by 0.08% on Thursday, extending the losses it posted in the previous session following the meeting between European Commission President Jean-Claude Juncker and US President Donald Trump. The two agreed to lower industrial tariffs and increase US natural gas and soybean exports to Europe. Also, they decided to harmonize regulatory standards to allow for medical devices to have better access in Europe. Dollar/yen is one of the weakest pairs for the week so far. It fell by 0.14% today and is set to post the seventh red day in a row, as speculation that the BoJ may appear hawkish next week continues to dominate. Euro traders will now turn their focus to Mario Draghi’s press conference today as no change to policy is expected later in the day. Euro/dollar moved lower by 0.16%, hovering slightly above the 1.1700 handle. Moreover, pound/dollar edged slightly lower (-0.08%) amid uncertainties over Brexit, while investors are waiting for the BoE interest rate decision next week. In the antipodean sphere, aussie/dollar and kiwi/dollar are paring some of yesterday’s gains, losing 0.38% and 0.18% respectively. Finally, the Canadian dollar was set to extend the gains it posted in the previous days amid hopes for a NAFTA deal. Dollar/loonie was lower by 0.13% towards 1.3032, creating a 6-week low.

STOCKS: European equities edged mostly higher on Thursday after Trump agreed with Juncker to suspend new tariffs and continue to negotiate over trade. The benchmark European STOXX 600 was up by 0.52% at 1000 GMT, led by industrials. It reached its highest level in six weeks. Meanwhile, the blue-chip Euro STOXX 50 increased by 0.75%. The Italian FTSE MIB jumped by 0.10%, the French CAC 40 rose by 0.74% and the German DAX 30 moved considerably higher by 1.31%. However, the British FTSE 100 traded lower by 0.03%. The Dow Jones and S&P 500 are poised to open higher, while the Nasdaq 100 is expected to open lower today according to US stock futures.

COMMODITIES: Oil prices were mixed today as West Texas Intermediate (WTI) crude dropped by 0.07% to $69.25 per barrel. However, Brent prices rose by 0.65% to $74.41 per barrel, hitting a 10-day high after Saudi Arabia postponed its oil shipment through a Red Sea strait. As for gold, the yellow metal moved sideways in the previous days and on Thursday, it slipped by 0.23% to $1,228 per ounce.

Day ahead: ECB takes center stage, all eyes on Draghi’s Q&A

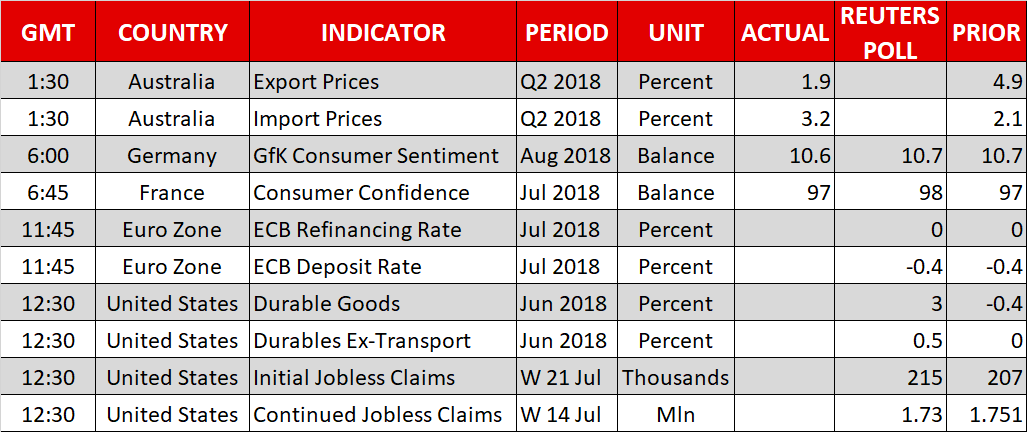

The main event will undoubtedly be the ECB policy decision at 1145 GMT, and the subsequent press conference by President Draghi at 1230 GMT. With the Bank having outlined its plans for ending QE at the June meeting, markets have started to focus on the timing of a potential rate increase. Back then, policymakers said rates would stay at present levels “through the summer of 2019”, which is a rather vague guidance that keeps open both the prospect of a hike as early as July next year, or as late as October. Market pricing is currently leaning towards the latter, with a 10bps hike being fully factored in for October 2019, according to EONIA swaps.

Hence, any optimistic remarks from Draghi that suggest a hike may come before October are likely to benefit the euro. Conversely, anything that pushes the anticipated timing of the first hike further into the future, could weigh on the currency. To be fair, one should not expect any clear comments from Draghi on this – after all, the phrasing was probably kept vague on purpose to allow the Bank some flexibility. Still, his overall tone, as well as any other comments – on trade for instance – could give investors a sense of direction on the matter. On balance, the prospect for a positive euro reaction appears slightly more likely, considering that the market is already quite pessimistic on the timing of a rate increase, and also that trade risks may have subsided a little following the constructive meeting between Juncker and Trump.

On the data front, the only noteworthy release still to come are US durable goods orders for June, slated for 1230 GMT. Forecasts are pointing to a strong rebound in the headline print, which is expected to rise by 3.0% in monthly terms, following a 0.4% decline in May. Most of the improvement appears to have come from volatile items though, as the core print that excludes transportation equipment is only expected to rise by 0.5%, after posting no growth previously. Weekly data on initial and continued jobless claims are also due out of the US at the same time.

In equities, the earnings season continues with some of the biggest firms reporting their results today being Amazon, Comcast, Intel, McDonald’s, Starbucks, Under Armour and Xerox.

As for the speakers, Mexican Economy Minister Guajardo is due to visit Washington to meet with US Trade Representative Lighthizer to discuss NAFTA. There are some hopes that a deal can be reached in the next months ahead of the US midterm elections, so any optimistic comments on the matter could benefit the loonie. The opposite holds true as well.

{kind=link}