- Japanese stocks close in the red on global growth fears in their first trading day of 2019

- US Nonfarm payrolls and Powell’s remarks to affect bearish sentiment

- Euro and pound recover with caution

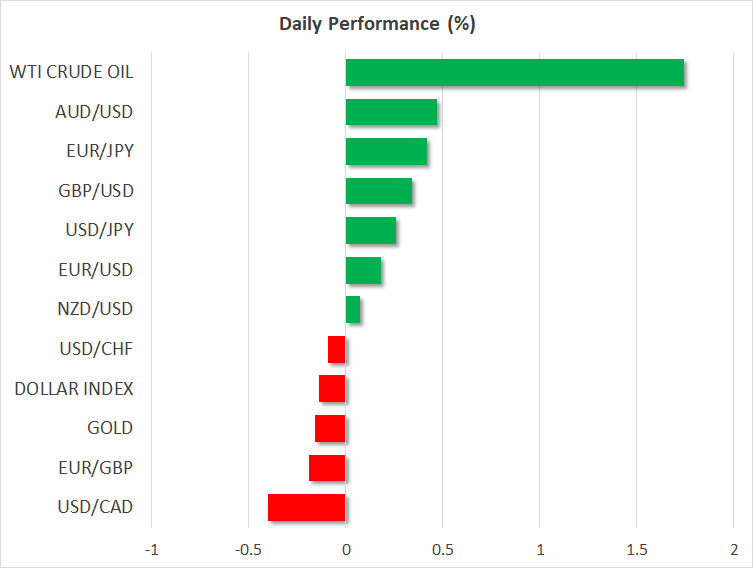

- Loonie hits two-week highs as oil prices surge

Japanese stocks join harsh sell-off, yen down on trade news

Japan’s stock market returned from the New Year’s holiday with a negative appetite as traders had to swallow the bitter global growth warnings which markets tasted in the previous days. With the tech-giant Apple cutting its quarterly forecasts thanks to lower sales in China on Thursday and fundamentals across the globe showing persisting weakness, the likes of Japan’s Nikkei tumbled by more than 2.0%, while the Topix also suffered as investors grew more certain that corporate profits may weaken this year.

The yen which benefitted the most from safe-haven demand, rallying to nine-month highs against the dollar, traded lower early on Friday on hopes that the discouraging data releases could push China and the US to reach a trade agreement sooner than later to avoid further negative consequences. Gold was also weaker, slightly below the 6 ½-month highs it registered yesterday. Details about next week’s trade talks boosted optimism even further after China’s Commerce Ministry announced on Friday that the two sides will hold vice-ministerial level meetings in Beijing on January 7-8. Chinese equities turned green in the wake of the news, while futures tracking US indices such as the S&P 500 and Dow Jones which closed strongly down on Thursday are pointing to some recovery later today.

Dollar awaits December’s jobs report and Powell’s comments

Meanwhile in the US, the new year started on the wrong foot, with Apple’s sales shortfall in China and a sudden pullback in the ISM manufacturing PMI ringing bells that the Fed may not hike interest rates in 2019 and possibly cut them in 2020 if the data continue to disappoint. Concerns elevated even further after the two-year Treasury yield dropped to 2.4%, reaching parity with the Fed’s fund effective rate for the first time since 2008. The funds effective rate moves within the Bank’s key policy range of 2.25-2.5%.

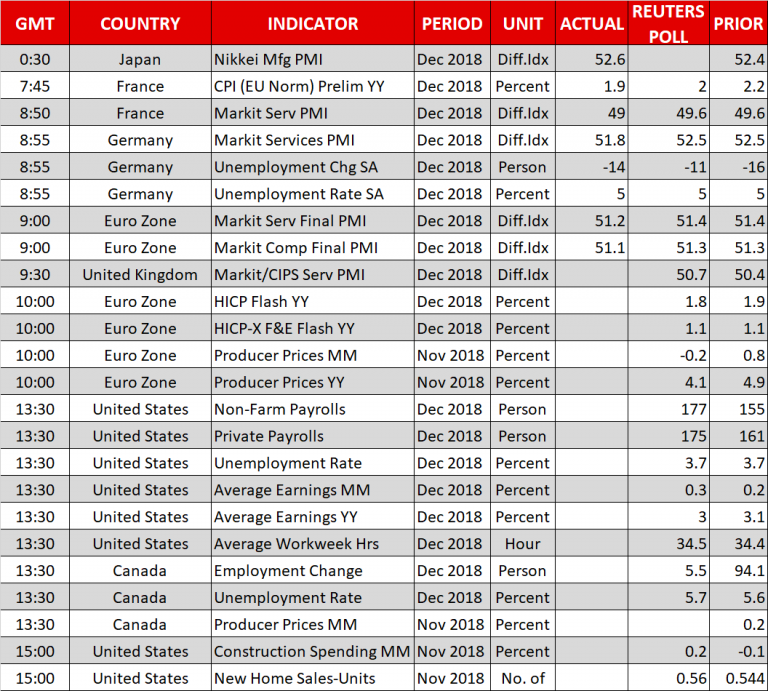

While the fresh trade news, alleviated some of the risk aversion on Friday, helping the dollar to gain some ground today, the sentiment remains bearish overall. Moreover, it would be interesting to see whether the greenback can retain upside in the remainder of the day as the all-important nonfarm payrolls report for the month of December will be closely scrutinized for any signs of slowdown at 1330 GMT, while speeches from several FOMC members including the Fed’s chief Jerome Powell will be in focus for any dovish remarks.

Eurozone flash CPI and UK’s Services PMI in focus

Euro/dollar managed to climb back above 1.14 on Friday, thought it still has some way to go to erase Wednesday’s steep freefall and December’s flash CPI figures could help the pair achieve this. Note that despite the loose monetary policy, the European Central Bank failed to drive core inflation towards its 2.0% price goal in 2018, reporting that a rate spike could only come after the summer of 2019. Therefore, should the preliminary core CPI appear stronger than analysts anticipate,supporting the Bank’s hopes that inflation will head to the target, the euro could extend the rebound and vice versa.

Pound/dollar is also slowly paring losses today, clouded by Brexit uncertainties and particularly concerns about whether the British Parliament will approve May’s deal with the extra assurances the prime minister is working to achieve with the EU in the week starting January 14. With clarity missing around the withdrawal terms and expectations for a BoE rate rise in 2019 standing low, there is no reason for investors to allocate more funds into the pound. Markit/CIPS Services PMI for the month of December could move the currency on Friday.

Employment report and oil prices to drive loonie

The Canadian dollar is among the best performers today and is set to post its first weekly gain after two months. An upbeat employment report later on Friday could add more sparkle to the loonie and lift the price above two-week highs, while additional buying interest for oil, which is currently trading higher by 1.70% could also boost confidence in the market. Yet the latter depends on the outcome of the EIA report on US oil inventories (1600 GMT) and the number of active US oil drillings by Baker Hughes (1800 GMT) due later today.

Interventions?")

{kind=link}