Labour market indicators will be published in New Zealand on Wednesday at 10:45 local time (Tuesday, 22:45 GMT), in what will be the last major release before the Reserve Bank of New Zealand’s policy meeting on May 8. With rate cut expectations running high, the New Zealand dollar is vulnerable to positive surprises in the data.

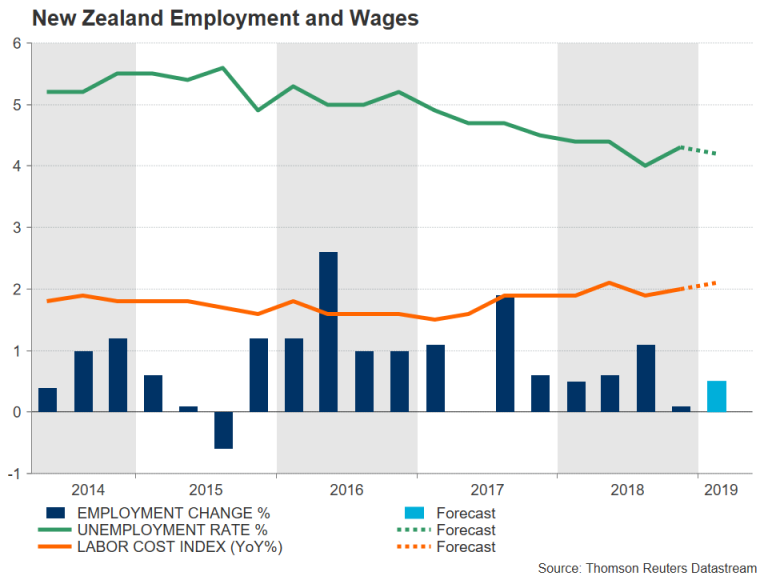

In the prior release, the unemployment rate had unexpectedly shot higher from 4.0% to 4.3% in Q4 2018. Analysts are forecasting the jobless rate to have edged slightly lower in the first three months of 2019 to 4.2%. More importantly, jobs growth is anticipated to have accelerated to 0.5% in Q1 from just 0.1% in the previous quarter. However, the labour cost index, which measures wage growth, likely grew by 0.5% over the quarter, unchanged from the prior figure. On an annual basis, the labour cost index is expected to have risen by 2.1%, which would make it only a marginal improvement from Q4’s 2.0% rate.

A mild improvement in employment growth is unlikely to significantly reduce rate cut bets unless it’s accompanied by substantially faster wage growth. Like most central banks, the RBNZ is combating persistently low inflation and wage growth – the 12-month CPI rate stood at just 1.5% in Q1. The subdued inflation picture prompted policymakers to turn more dovish at the March meeting. The RBNZ surprised markets when it signalled that the “the more likely direction of our next OCR move is down”.

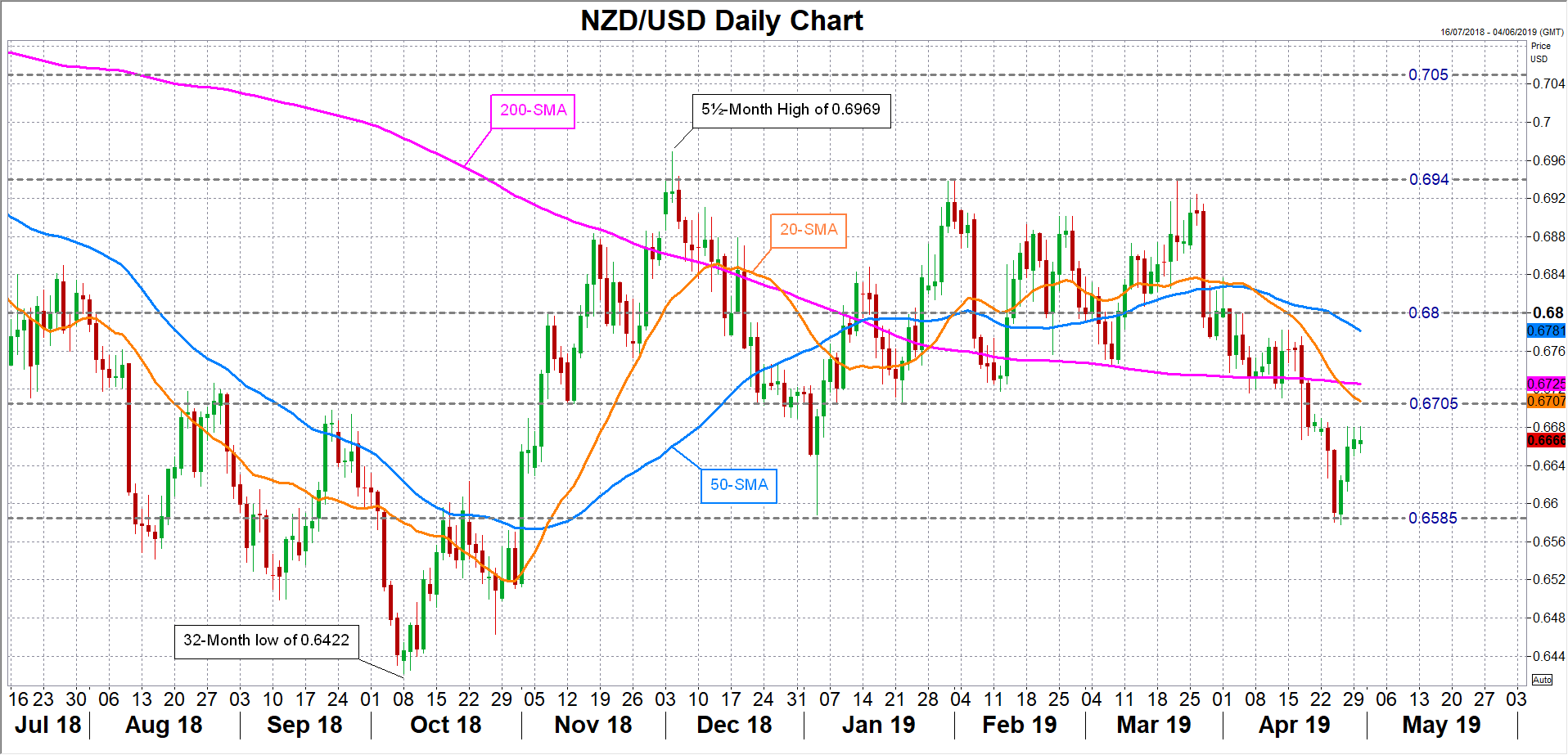

The policy shift set the kiwi on a downtrend, driving it to near 4-month lows against the US dollar last week. A better-than-expected jobs report could provide the kiwi with a modest lift, with immediate resistance at $0.6705, near the 20-day moving average, becoming the key target. However, a weak set of numbers could push the kiwi back towards the April lows in the $0.6585 support region.

A drop below this support to fresh yearly lows is possible from a very bad report, which could see investors bring forward their expectations of a rate cut to as early as the next meeting on May 8. But, on the other hand, any bright spots in the jobs figures would probably do little to convince markets that the RBNZ’s next move won’t be down.

{kind=link}