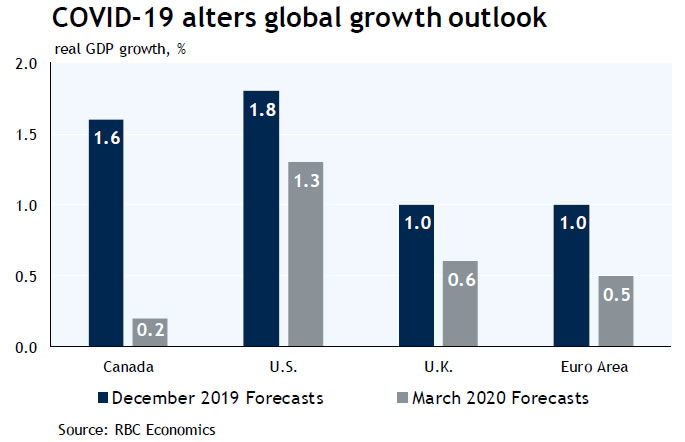

The coronavirus upends the global growth picture

Since our last update in December, the outlook for the global economy has been severely impacted by the spread of COVID-19 amplified by the sharp decline in oil prices that will magnify the pain of virus-related shocks in oil-producing regions. Central banks have responded by lowering interest rates. Governments are also stepping in with stimulus measures to help blunt the impact. Will these actions be enough? Financial markets remain skeptical, with equity markets plunging and investors running to the safety of government bonds. Even with aggressive intervention, it is increasingly likely that countries around the world will fall into recession this year. This is particularly true in Canada where the combination of falling oil prices and virus-related stoppages are likely to overwhelm any lift that lower interest rates and government spending provide. We expect that the economy will contract in the sec-ond and third quarters driving annual growth in Canada down to just 0.2%.

Financial markets brace for a global recession

Worries about the impact of COVID-19 on the global economic outlook ramped up in February as financial markets extrapolated what looked like a modest hit to the world economy into a full-fledged economic downturn. As the virus spread outside China, governments and busi-nesses reacted aggressively – closing schools and can-celing events and flights, and in the case of Italy, impos-ing a country-wide lockdown. The direct hit to activity from the interruption of global supply chains along with falling travel and tourism activity resulted in downward adjustments to 2020 growth forecasts. The OECD cut its baseline projection for its member countries by 0.5 per-centage points and said there is a risk that the hit might be as big as 1.5 ppts. China, the economy initially affect-ed, is now forecast to expand at the slowest pace since 1990. This projection assumes that a sharp decline in the first quarter will prove temporary. The anticipated slowing in the UK and Euro area economies is now expected to be more severe, with the US economy headed for slowest year since the Great Reces-sion and Canada likely headed into recession. These downgrades align more closely with what financial markets anticipate. The rout in global stock markets continues with the world index down almost 20% from its February 12 high. Yields on government bonds repriced and now imply central bankers could see policy move beyond the extraordinary stimulative levels that followed the Great Recession.

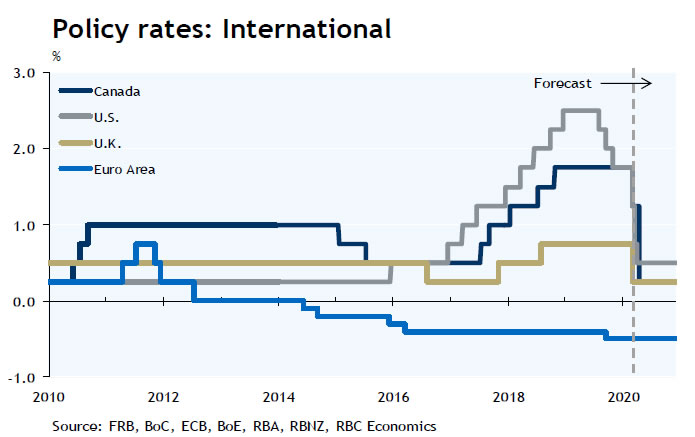

Central banks act aggressively

Investors’ demand for a coordinated global policy response saw central banks first off the mark with the US Federal Reserve mak-ing its first inter-meeting cut to the policy rate since October 2008. The Bank of Canada matched the Fed’s 50bps cut at its regularly scheduled meeting the next day. Taking a page from the Fed, the BOE moved ahead of a scheduled meeting and lowered rates by 50bps and implemented a scheme to support lending to small businesses. The ECB also acted with targeted measures including quantitative easing and cheap financing for the corporate sector. We expect central banks with room to move rates lower will do so in the months ahead to ease financial pressures for households and businesses.

Governments have and will continue to unveil policies aimed at supporting industries and individuals impacted by the virus. Over the past week, stimulus packages have been announced in the UK and to a lesser extent in Canada. Governments in the US and Europe are also preparing their stimulus packages. Data vacuum on virus effect So far, few economic releases outside of China have captured the virus effect. China’s business sentiment index fell to a record low in February and factory and retail activity likely slumped, underpinning the cuts to the growth forecast. Chinese exports plunged in February. We anticipate similar reports will emerge in Europe as school closures and event cancellations show up in the economic data. Our current view is that the hit outside of China will be most evident in Q2 and look for a negative print in most countries we follow.

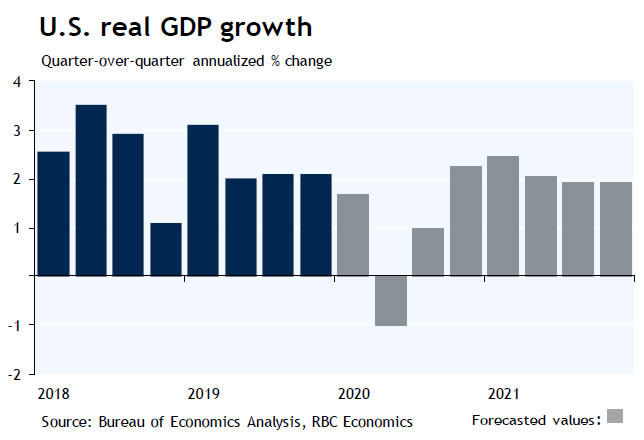

US policymakers lean in

US data have yet to show any impact from the virus outside of anecdotal reports and panic in the financial markets. Consumers are in good shape with jobs and healthy balance sheets, and to-date confidence readings remain high. Businesses are facing challenges with supply chains interrupted and residual tariffs on Chinese imports causing strains and lower oil prices weighing on energy producers. But the wildcard in the near term will be the persistence and pervasiveness of the virus and the ensuing directives issued by public health officials. Upcoming data on consumer and business confidence, travel and tourism activity and the ability of businesses to get production inputs will scale the hit to growth in the second quarter. Our baseline forecast calls for the economy to contract at a 1% annualized rate in the second quarter with a growing probability that a recovery will be delayed until late in the year.

The Fed’s aggressive response to the growing downside risks was aimed at keeping financial conditions accommodative and confidence high. We expect a 50bps rate cut at the meeting later this month with another 25bps to follow. Monetary policy itself won’t be able to counter the near-term impact of the virus on some industries, meaning governments and other agencies will need to provide targeted funding and may turn to programs typically used to address disruptions associated with natural disasters. Markets are monitoring the Trump Administration’s response with talk of a payroll tax cut, support for hourly wage earners impacted by the virus and tax payment deferrals.

Whether the virus can still be contained is an open question, but at this stage, we are assuming that the greatest economic impact will have passed heading into the second half of the year. At that time, the combination of low interest rates and other policy measures should work to restore confidence. We do not expect a sharp bounce-back but see a gradual return to positive growth over the second half of the year. On net, we look for the US economy to grow 1.3% in 2020, half a percentage point lower than our December report. By 2021, with the 2020 election cycle also in the rear-view mirror, we expect the economy to return to a trend pace of 1.8% opening the door to the Fed reversing at least some of the “emergency” rate cuts.

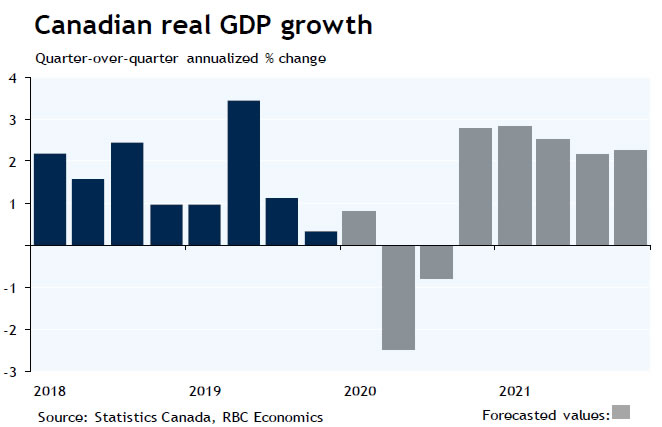

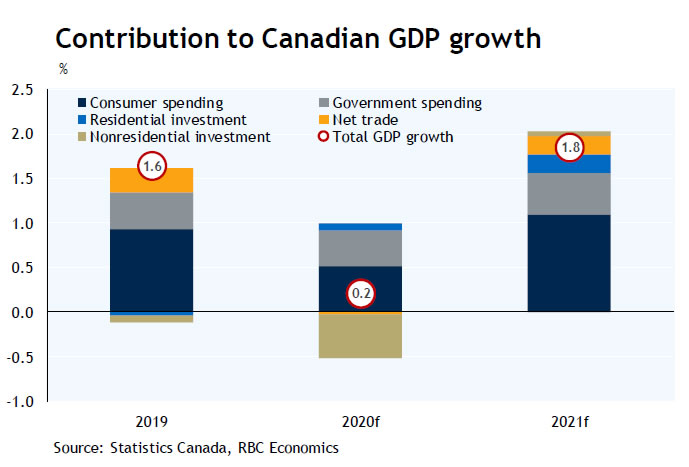

Recession in Canada expected

The handoff to 2020 was weak in Canada with real GDP rising at a paltry 0.3% annualized pace in the fourth quarter. The transitory factors that weighed on growth at the end of last year didn’t completely disappear. If anything, newfound temporary factors were amplified by concerns associated with COVID 19 and plunging oil prices. The Bank of Canada stepped up with a 50bps rate cut on March 4 and a commitment to make additional adjustments as needed to limit the tightening in financial conditions associated with wider credit spreads and falling equity prices. We expect they will cut the policy rate by another 100bps.

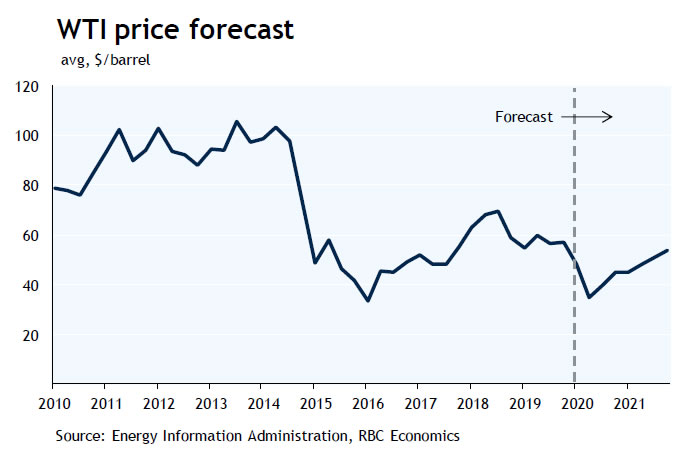

Oil price drop adds more downside to outlook

Another powerful force for the near-term economic outlook is the plunge in oil prices that occurred following a dispute between Saudi Arabia and Russia over oil production. The disagreement resulted in Saudi Arabia announcing it would ramp up production and cut prices effective April 1. Oil prices were already under pressure as the coronavirus weighed on demand for fuel. The global benchmark price, West Texas Intermediate, is more than 50% below its recent peak on January 6, 2020. Sharply lower oil prices spell another period of strain for the oil producing provinces and a hit to the country’s income.

We’ve made significant downward revisions to our forecast and now look for real GDP to increase at a modest 0.8% pace in Q1 followed by two quarterly declines of 2.5% and 0.8% in Q2 and Q3 respectively. Our baseline assumption is that the impact of the virus will run its course by the end of the first half of the year however the persistence of low oil prices will prevent the economy from recovering. Key to the near term outlook and the pace of the recovery will be the policy response by governments. The federal government’s plan to provide support measures to mitigate the impact of the virus included upping health care transfers, and increasing unemployment insurance, though both program increases were relatively limited. Our forecast assumes the federal budget on March 30 will include additional support.

The weakness in commodity prices, including oil, will weigh on some key sectors of the economy in the near term. The degree of pressure on the services sector is forecast to rise over the next several months. We expect that the biggest negative impact from the coronavirus to show up in Q2 with the weight from lower oil prices weighing on the economy in the third quarter. Falling travel and entertainment activity will spill over into other parts of the economy. Disruptions to supply chains and falling external demand will have negative repercussions for the Canadian industrial sector.

In the final quarter of the year, we expect the economy will pick up more substantially, teeing up for a better 2021. Still, we are not expecting the economy will make up for losses in 2020 quickly, given the blow to household confidence and impact of yet another round of retrenchment in the oil & gas sector.

Bank rate cuts to continue

While lower interest rates opened the door to the rally in Canada’s housing market continuing, the hit to financial assets and the prospect that the recession will lead to job cuts will limit activity. We expect layoffs and job losses in some highly exposed industries but anticipate many of these to prove temporary, although there is a greater risk of permanent layoffs in the energy sector. Given the cur-rent tightness of the labour market, employers are unlikely to be quick to cut workers given the challenges associated with rehiring once the economy bounces back.

The Bank of Canada had to weigh the risks between the economy stalling and lower interest rates stoking debt accumulation when it made its decision on policy. The 50 bps cut clearly shows it views the bigger risk to the econo-my coming from households and businesses retrenching and exacerbating what was already a weakening trend in the growth outlook. Given the elevated level of uncertainty about the domestic outlook and global disruptions, we expect the bank will increase policy support at upcoming meetings and forecast the overnight rate will fall to match the record low of 0.25%.

The Canadian dollar suffered as oil prices fell and risk aversion saw investors pivot into US dollars. The outlook for the currency will be dominated by these two factors going forward as monetary policy in both countries is likely to ease further. We see further downside for Canada’s dollar in the current anxiety-ridden environment and the persistence of low oil prices and are forecasting the currency will continue to weaken into mid-year before recovering modestly.

{kind=link}