- Dollar remains under pressure, stocks hover near records in a quiet session

- Markets still driving in risk-on gear as stimulus hopes grow stronger

- But US inflation data and Powell’s remarks could spark volatility today

Risk-taking still the dominant force

It was a quiet session in global markets, without any real news to drive the action. The same old stimulus stories continued to circulate, encouraging investors to take on more risk. The overarching theme lately is that the Democrats will push their supermassive relief bill through Congress without Republican approval, allowing for a higher price tag. Positive vaccine developments and cheap money policies are the other variables in this equation.

Stock markets paused for breath but did not retreat from record high altitudes. The party is likely to resume today as futures suggest the S&P 500 and the Nasdaq will open in new uncharted heights, about 0.5% higher.

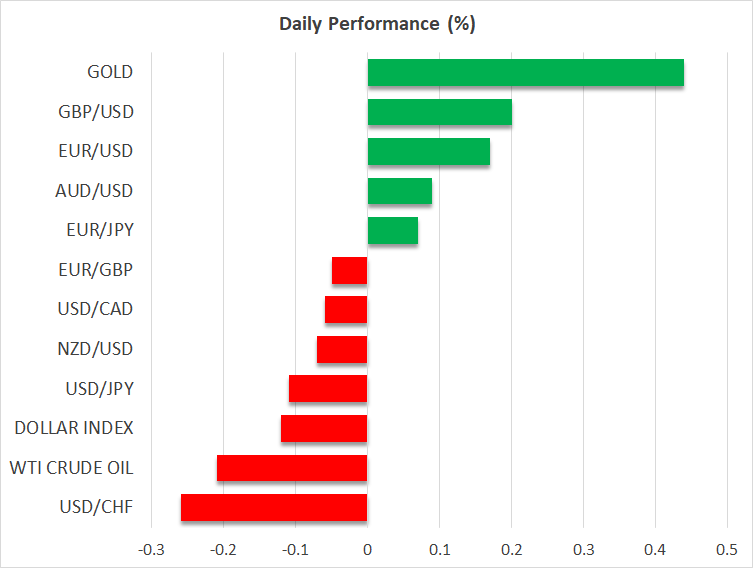

In the FX arena, the sanguine atmosphere has torpedoed the defensive US dollar, giving most other currencies the green light to advance. The question now is whether this is a setback in the greenback’s recent recovery phase, or whether it is a resumption of the broader downtrend.

On the bright side, US fundamentals are solid. Even accounting for the recent patch of weakness in the labor market, the American economy is still far stronger than the Eurozone’s, and all the incoming federal spending could accelerate the recovery further. That said, a powerful recovery might boost riskier plays to the reserve currency’s detriment and the Fed isn’t willing to entertain a normalization discussion yet.

Upside inflation surprise on the cards?

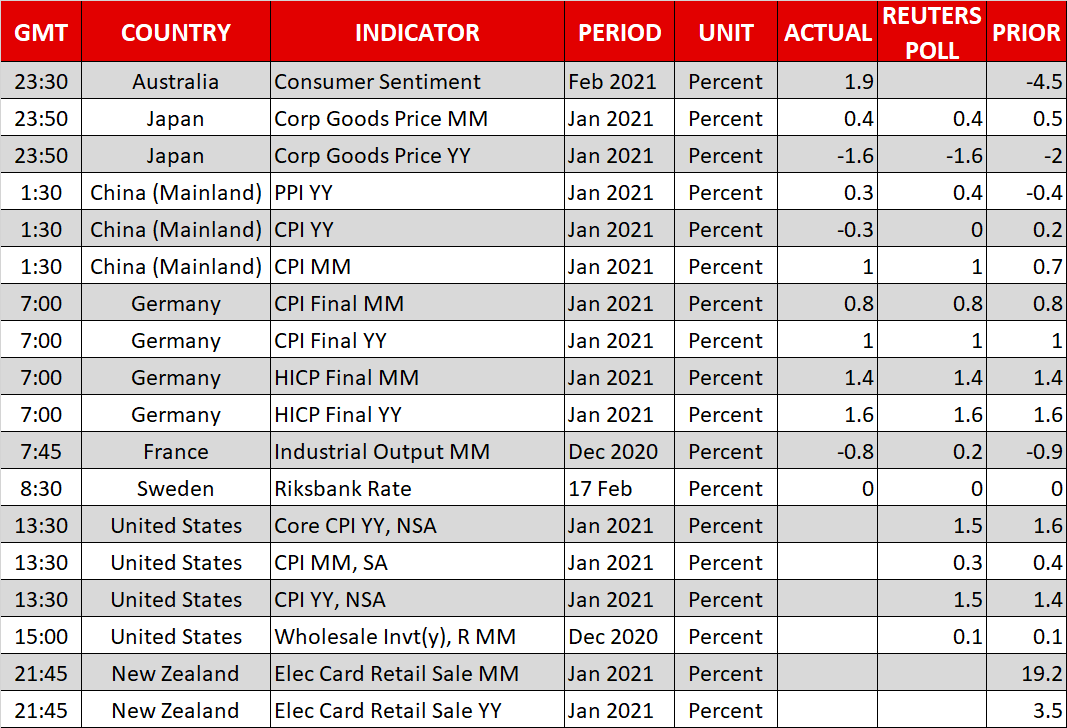

The upcoming US inflation data could make this picture clearer. Forecasts suggest the annual CPI rate ticked up to 1.5% in January from 1.4% in December, while the core rate is expected to dip to 1.5% from 1.6% previously.

If anything, the risks surrounding these forecasts may be tilted to the upside, judging by what the latest PMIs revealed. The ISM manufacturing survey showed a sharp increase in the prices paid by businesses, while the Markit surveys suggested that firms also passed these higher costs onto consumers.

Investors are also bracing for the inflation beast to reawaken soon. Market-based inflation expectations have shot higher lately amid worries that Congress might overplay its hand, spending too much and overheating the economy, with soaring energy prices and supply disruptions adding fuel to the fire.

Turning to the market reaction, if inflation begins to accelerate even before the gargantuan $1.9 trillion aid package is unleashed, that could intensify speculation around how quickly the Fed might begin to reduce its QE dosage. This would argue for a rebound in the dollar and a mild retreat in stock markets.

The catch is that these reactions could fade once Fed Chairman Powell takes the virtual stage at 19:00 GMT. He has been adamant lately that his central bank won’t react to an inflationary episode as it will likely be transitory, so his remarks could act as a tranquilizer for markets.

Cable off to the races, crude flexes muscles

Elsewhere, the British pound continues to capitalize on the dollar’s troubles, with Cable exploring heights not seen since early 2018. The UK economy is still in a deep hole, but the swift pace of vaccinations implies a stronger recovery ahead.

The cheerful market mood is another element underpinning the pound, which has become linked to risk appetite during this crisis thanks to the UK’s chronic twin deficits that require capital flows from abroad. BoE Governor Bailey will speak at 18:00 GMT.

Finally, in the commodity sphere, crude oil prices continued their relentless march higher, buoyed by falling inventories and expectations of vigorous future demand. The latest retreat in the dollar may have played a part as well.

{kind=link}