Summary

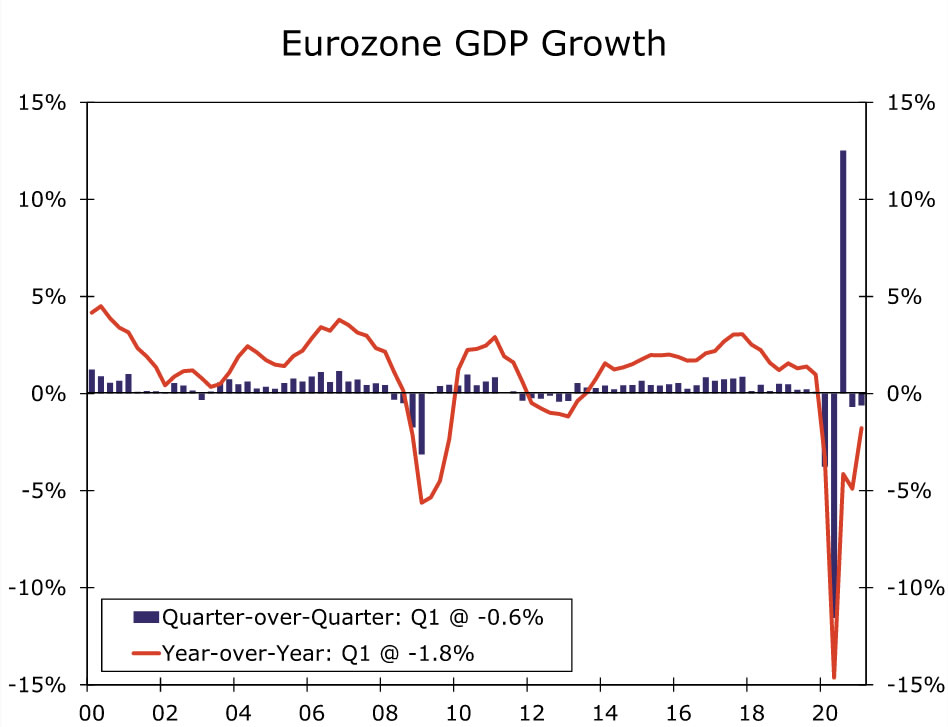

The Eurozone economy shrank for a second straight quarter in Q1, with GDP declining 0.6% quarter-over-quarter. The German economy was particularly weak, although declines in GDP were also reported in Italy and Spain. More recent confidence surveys point to a recovery, although we expect the pace of the rebound in Eurozone GDP to be gradual. With inflation pressures also muted, we expect the European Central Bank to maintain its accommodative monetary policy stance for an extended period.

Eurozone GDP Shrinks for a Second Straight Quarter

The Eurozone economy started the year on a soft note, as GDP declined for the second quarter in a row. Eurozone Q1 GDP fell 0.6% quarter-over-quarter, a bit less than expected, and was down 1.8% compared to the same quarter last year. The weakness in the region’s economic activity stemmed largely from a renewed rise in COVID cases and the implementation of associated restrictions, which appeared to restrain service sector activity in particular. While full details are not available with this initial release, there are enough details to offer some interesting insights. For the region’s major economies Germany was by far the weakest, reporting a Q1 GDP decline of 1.7% quarter-over-quarter. Italy’s Q1 GDP fell 0.4% and Spain’s Q1 GDP fell 0.5%, but France managed to eke out a 0.4% increase in GDP in the first quarter.

There was also some information released for the economy by type of expenditure which, not surprisingly, indicated that much of the weakness was concentrated in consumer spending. For Germany that information was only qualitative in nature—however, the German statistical office noted that weakness was concentrated in household consumption in particular. In terms of more precise estimates Spain’s Q1 consumer spending fell 1.0% quarter-over-quarter, although France did manage a small 0.3% increase in consumer spending during the quarter.

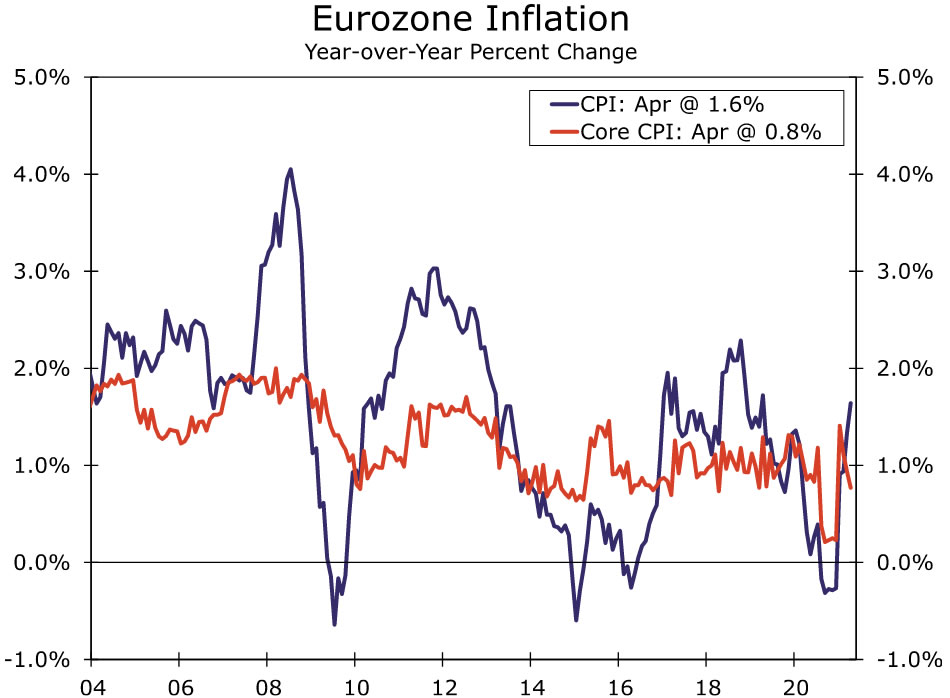

Slow Road to Recovery AheadConfidence surveys do point to at least a gradual recovery in activity as 2021 progresses. The Eurozone April service PMI rose to 50.3, the first time that index has returned to growth territory since August of last year. Eurozone April economic confidence also jumped to 110.3, from 100.9 in March, although the magnitude of that increase is perhaps somewhat surprising given that restriction were still in place in many countries across the region during the month. We still forecast only a moderate recovery for the Eurozone economy for full-year 2021, anticipating a 3.2% rise in GDP for this year. Moreover, inflationary pressures remain muted. While the headline CPI quickened to 1.6% year-over-year in April, the core CPI eased to 0.8%. Against this backdrop of modest growth and muted inflation, we expect the European Central Bank (ECB) to maintain its accommodative monetary policy stance for an extended period. Specifically, as the ECB has signaled, we expect the central bank to fully utilize its €1.85 trillion purchase envelope for the Pandemic Emergency Purchase Program, with purchases set to continue through until at least Q1-2022. Indeed, if the Eurozone recovery struggles to gain traction and the rebound is slower than anticipated, the risks are tilted towards the ECB’s asset purchases lasting longer or being larger in size than we currently expect.

{kind=link}