The latest US employment report will be released at 13:30 GMT Friday. Nonfarm payrolls likely cooled because of the Omicron wave and a negative print cannot be ruled out. That said, the most important metric for the Fed is wage growth, as that will decide how many rate increases are needed to hammer inflation. As for the dollar, the playbook may be to fade the initial negative reaction if payrolls disappoint.

Tight jobs market

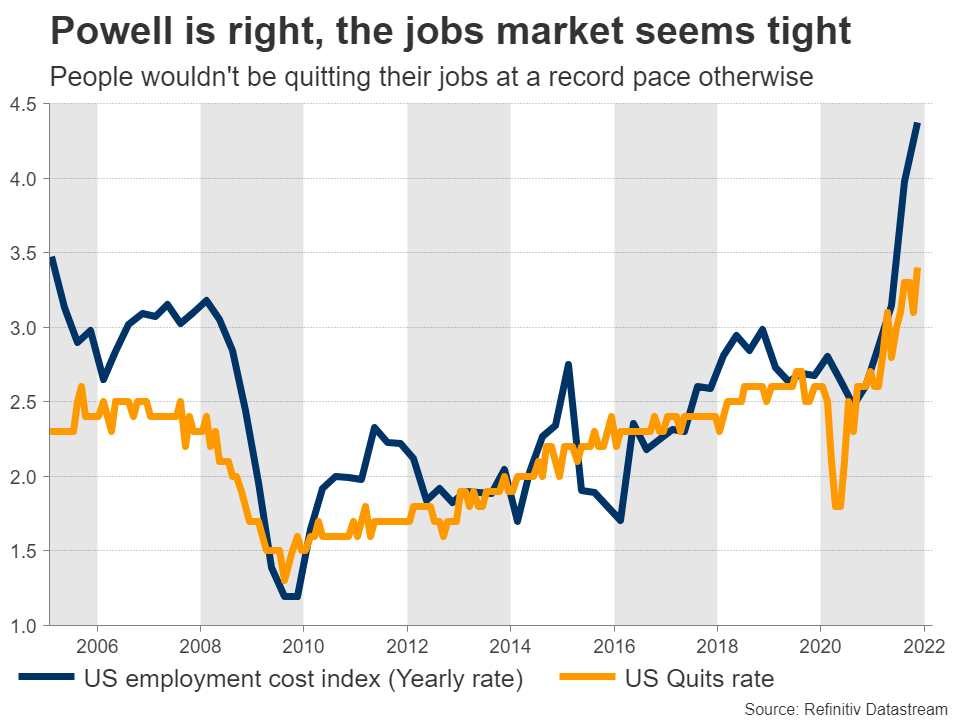

The US labor market has recovered at a stunning pace. Even the Fed chief admitted last week that the jobs market is tight, highlighting the record number of job openings in the economy and the record number of people quitting their jobs in search of higher salaries and other benefits.

Labor force participation is the only dark spot, as it remains lower than before the pandemic. There’s a big debate about whether that will change – if the people that retired in 2020 are ever coming back. Of course, this is a longer-term question that doesn’t matter much for markets in the short-term as the Fed generally focuses on the unemployment rate.

Another even more crucial variable for the Fed is wage growth. With inflation so hot already, Fed officials worry that it could spill over into wage negotiations, fueling a wage-price spiral that keeps feeding inflationary pressures even after the supply chain normalizes.

This means wage growth is seen as the canary in the coal mine, telling the Fed where inflation will be in the future and hence guiding policy changes. In other words, wage growth is the single most important factor at this stage of the economic cycle.

Weak payrolls, strong wages?

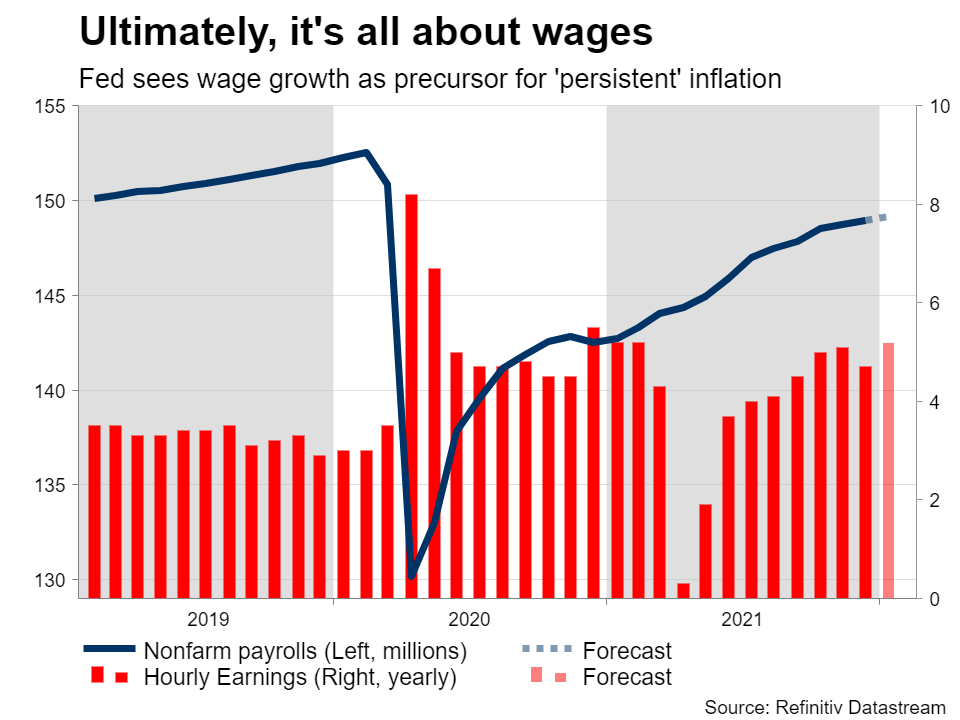

This is going to be a weird report. Nonfarm payrolls are forecast to have risen by 150k in January, which would keep the unemployment rate unchanged at 3.9%. However, there might be some room for disappointment.

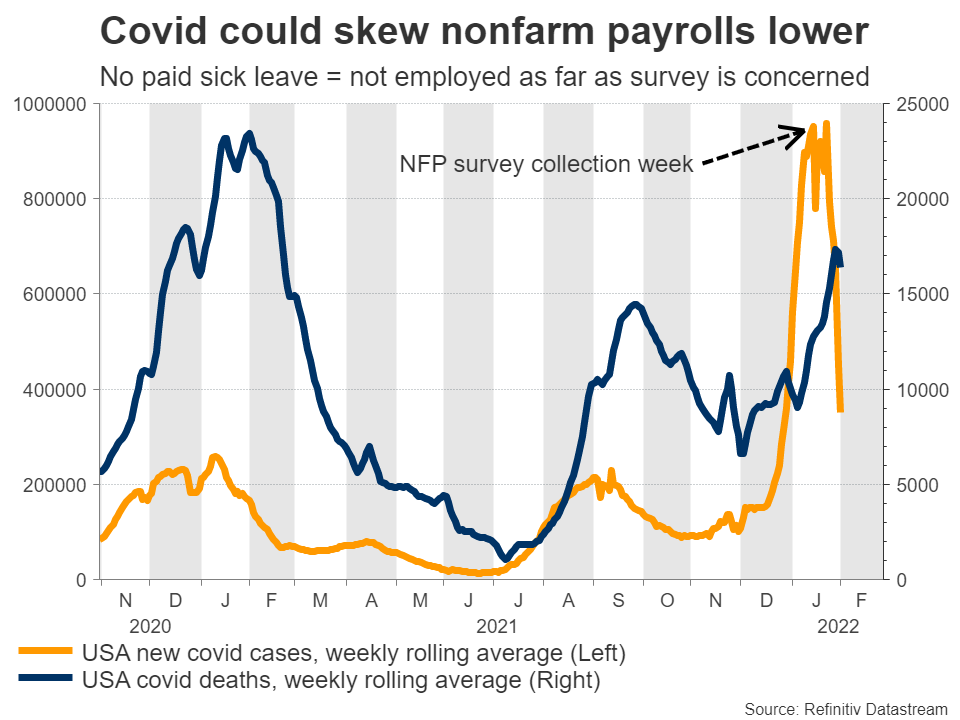

The Bureau of Labor Statistics collects the data for these surveys during the second week of each month. In January, this was the week when covid cases peaked amid the Omicron outbreak. If someone was out sick during this week and was not getting paid sick leave, they would be counted as unemployed in the jobs survey.

Hence, this could artificially skew the nonfarm payrolls number lower this month. Also arguing for a weak NFP print are jobless claims, which rose dramatically during the survey week from a month ago. This implies we could even see a negative payrolls number.

On the bright side, wage growth might be strong. Forecasts suggest average hourly earnings accelerated to 5.2% in yearly terms from 4.7% previously, something supported by business surveys like the Markit PMIs that pointed to “soaring wage bills” as companies competed to attract workers.

Fade the downside?

In the markets, the initial reaction in the dollar might be negative in case the nonfarm payrolls print is indeed disappointing. Yet any dollar weakness may not last long, as a soft print wouldn’t represent the true state of the labor market – only a statistical quirk.

Indeed, Fed officials like Thomas Barkin have already said they would view any disappointment in this report as a temporary setback given the covid numbers during the month. That would be especially true if wages are solid. As such, this could be a case of the dollar dipping on the news, before recovering in the following hours.

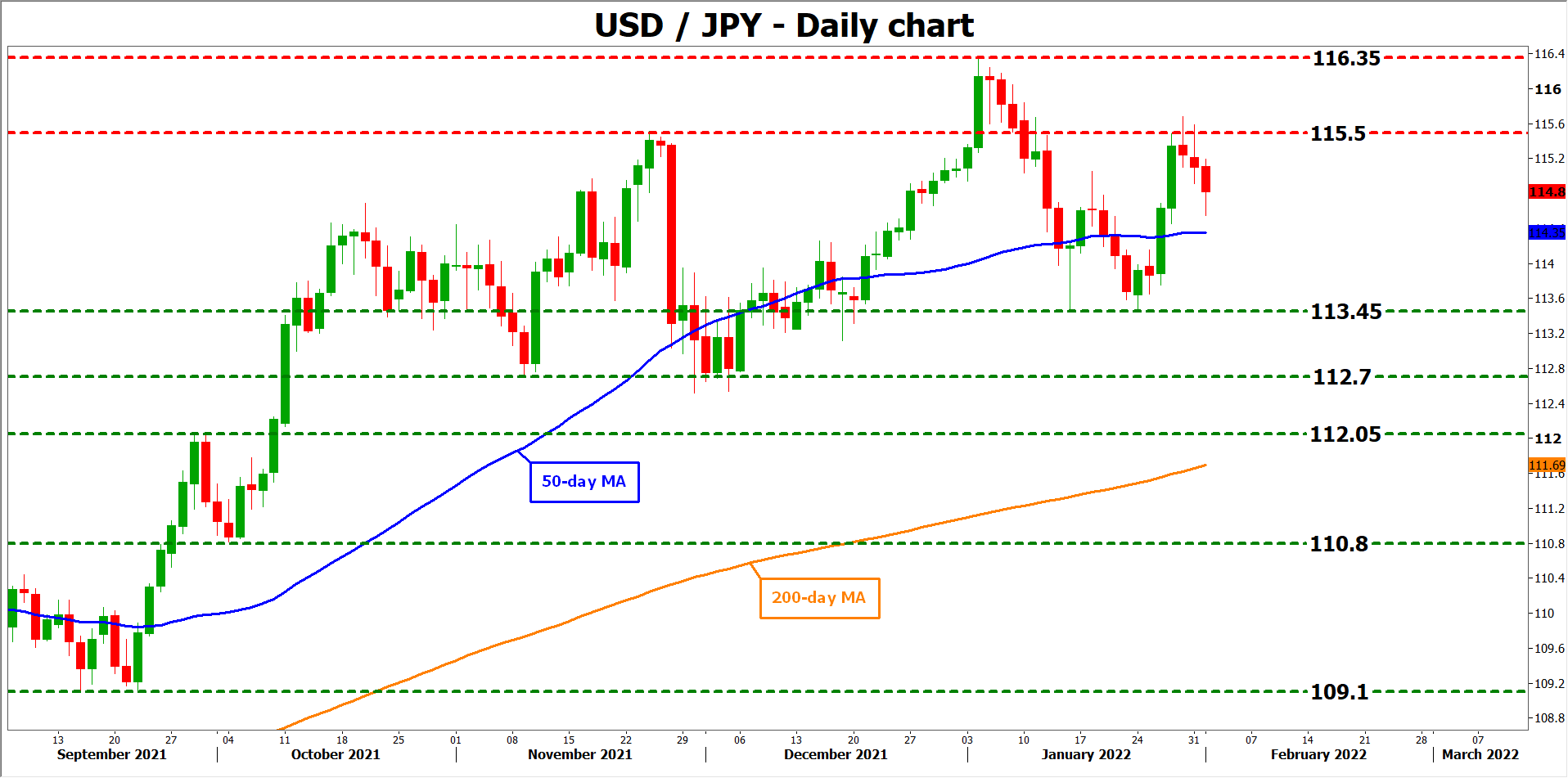

Taking a technical look at dollar/yen, a pullback could encounter immediate support near the 50-day moving average currently at 114.35. A violation would turn the focus towards the 113.45 zone.

On the upside, the first target for the bulls may be the 115.50 region, a break of which could open the door towards the five-year high of 116.35.

{kind=link}