The pound has fallen victim to the market turmoil sparked by the Ukraine conflict, plunging more than 3.5% since late February when tensions with Russia started to rapidly escalate. Investors still expect that the Bank of England will go ahead with most of its planned rate hikes this year, but that’s likely to come at the expense of growth. Can the raft of economic indicators out of the UK on Friday (07:00 GMT) cast some positive light over the outlook?

Going from crisis to crisis

Having only just fully recovered from the pandemic-induced slump, the British economy is facing another crisis. The war in Ukraine has worsened Europe’s energy crunch, fuelling the surge in oil and gas prices. But unfortunately, the ripple effects go beyond the energy sector as raw material prices of everything from food to base metals are soaring as Western sanctions on commodity-rich Russia begin to bite on the rest of the world.

Although Britain is nowhere near as reliant on Russia for its energy needs as several Eurozone nations are, UK fuel prices are expected to skyrocket soon, exacerbating the squeeze on consumers, who will additionally be hit by higher national insurance contributions as of April. So far neither the government nor the Bank of England have indicated they are about to change their policy courses.

Is hawkish BoE adding to pound’s woes?

This could be why sterling has nosedived so much as investors think the BoE is headed for a policy mistake by tightening at a time when the growth outlook is fast deteriorating. Unlike the European Central Bank, which has signalled it is willing to overlook the jump in energy prices that are being driven by factors that are out of its control, the BoE will probably only pause its rate hike cycle once growth starts to significantly slow down.

While it’s true that the UK economy is a little more robust than the Eurozone’s at the moment, it’s unlikely to be as resilient as America’s during this crisis. Nevertheless, the latest economic pointers due on Friday might help ease some of the concerns if they show that 2022 got off to a solid start.

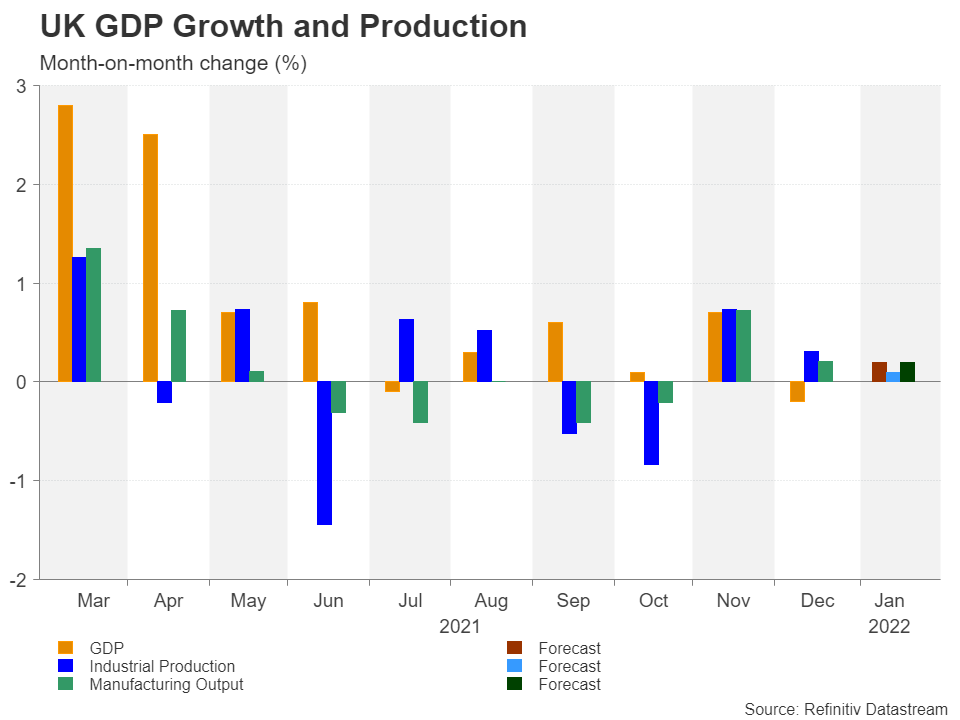

Modest GDP rebound anticipated for January

GDP is projected to have bounced back by 0.2% month-on-month in January after contracting by the same amount in December when Omicron restrictions were introduced. Such a figure would push up annual growth to 9.3% from 6.0%.

Industrial output on the other hand is expected to have grown by a paltry 0.1% m/m in January, driven mainly by the manufacturing sector, which is forecast to have expanded by 0.2%.

Other figures to be released will include the trade balance and construction output for the same period.

Pound’s fate tied to Ukraine war

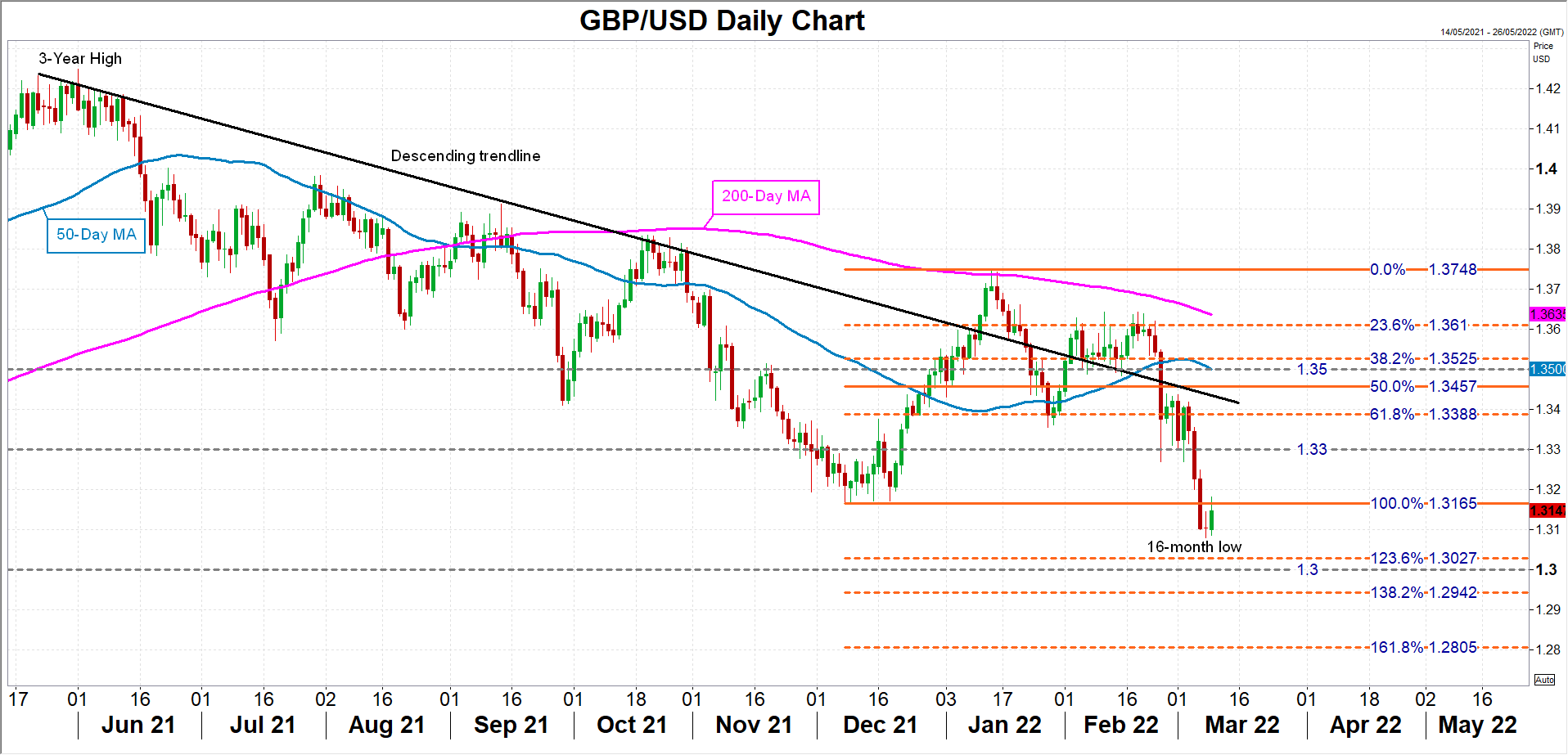

It’s hard to see the data having much of an impact on cable while tensions over Ukraine remain so heightened. At best, stronger-than-expected numbers might provide some much-needed support. In which case, the 123.6% Fibonacci extension of the December-January upleg could act as a crucial defence for halting further declines just above the $1.30 level at $1.3027.

If this support were to fail, the 138.2% and 161.8% Fibonacci extensions at $1.2942 and $1.2805, respectively, would next come into focus.

However, in the event that there is progress in the upcoming talks between the Ukrainian and Russian foreign ministers on Thursday, the pound would be poised for a decent rebound, potentially recovering towards the $1.3165 area initially, before testing the $1.33 handle.

In the bigger picture, though, sterling is likely to remain bearish as long as it’s trading below its long-term descending trendline, with not even BoE rate hikes expected to alter this outlook as long as war is raging in Eastern Europe.

{kind=link}