The Bank of Japan will round up this week’s central bank decisions on Friday but is unlikely to follow in the footsteps of the Federal Reserve and Bank of England by raising interest rates. Although consumer prices in Japan are soon set to surge on the back of the jump in global energy prices, BoJ Governor Haruhiko Kuroda has signalled this does not change anything on the policy front in Japan. It’s no wonder therefore that the yen is tumbling, particularly against the US dollar, in spite of heightened geopolitical risks, as it’s becoming increasingly difficult for investors to ignore the widening policy divergence.

Inflation only just firing up

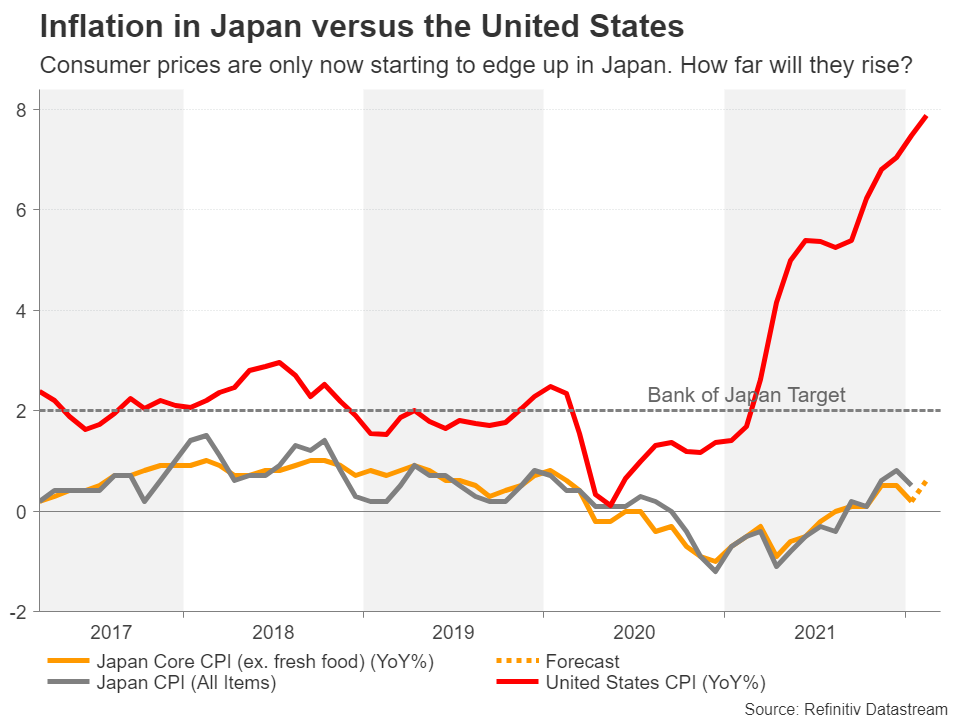

The latest inflation data due on Friday is expected to show Japan’s core consumer price index rose by an annual rate of 0.6% in February – a figure that is a far cry from the 5% plus readings in most other advanced economies. However, the subdued picture isn’t anticipated to last much longer as it’s almost certain that the rally in energy and other commodity prices will push up inflation to above the 2% target over the coming months.

Japan is not only a big net importer of oil and petroleum products, but the country’s manufacturers also rely heavily on imports for most of their raw materials. Hence, the pain on businesses as well as on households is expected to be quite acute and is why the Bank of Japan is more worried about the economic impact of the war in Ukraine than the inflationary effects, especially as GDP has yet to completely recover from the pandemic.

The ‘wrong type’ of inflation

Specifically, Japan is about to be hit by the wrong type of inflation and Kuroda has already ruled out tightening monetary policy solely on the back of cost-push factors. Like his Australian counterpart, Kuroda thinks it’s vital that wage growth rises to 3% so that inflation can meet the Bank’s 2% objective sustainably.

Although there has been some pickup in wage deals lately, employers have mostly been compensating their workers through bonuses rather than increasing regular salary levels. Even in countries such as Britain and the United States where there has been a substantial acceleration in wage growth, real salaries are being depressed by the surge in living costs. Thus, achieving this goal remains quite far off for the Bank.

Will the BoJ have to do a U-turn?

But as the BoJ sticks to the script and keeps policy unchanged on Friday, there are some risks to this stance and policymakers may yet have to perform an embarrassing U-turn like the ECB did recently. For one, with the effect of soaring energy prices yet to fully transpire in fuel bills, it’s hard to predict accurately how high CPI will rise and for how long it will remain elevated thereafter.

The other danger is that the Japanese yen is coming under pressure from both the diverging monetary policy paths of the BoJ with the other major central banks as well as the deterioration in Japan’s trade deficit due to the increasing cost of energy and commodity imports. A weaker yen would only worsen the impact of the energy crisis by making imports even more expensive.

Yield curve control might be tweaked

It’s plausible therefore that the BoJ won’t have to wait as long as it’s implying it will before it takes initial steps towards normalizing policy. Those steps could even come at the next meeting in April when the Bank will have updated quarterly projections and there will be more data on how much damage the conflict between Russia and Ukraine is inflicting on the Japanese economy.

The easy option for policymakers to combat a depreciating currency and spiralling inflation is to widen the yield band for 10-year government bonds. As part of its yield curve control policy, the BoJ targets a band of plus or minus 25 basis points around zero. Setting a wider cap would allow the 10-year yield to rise much higher, effectively boosting the yen by narrowing the yield spread with other sovereign bonds.

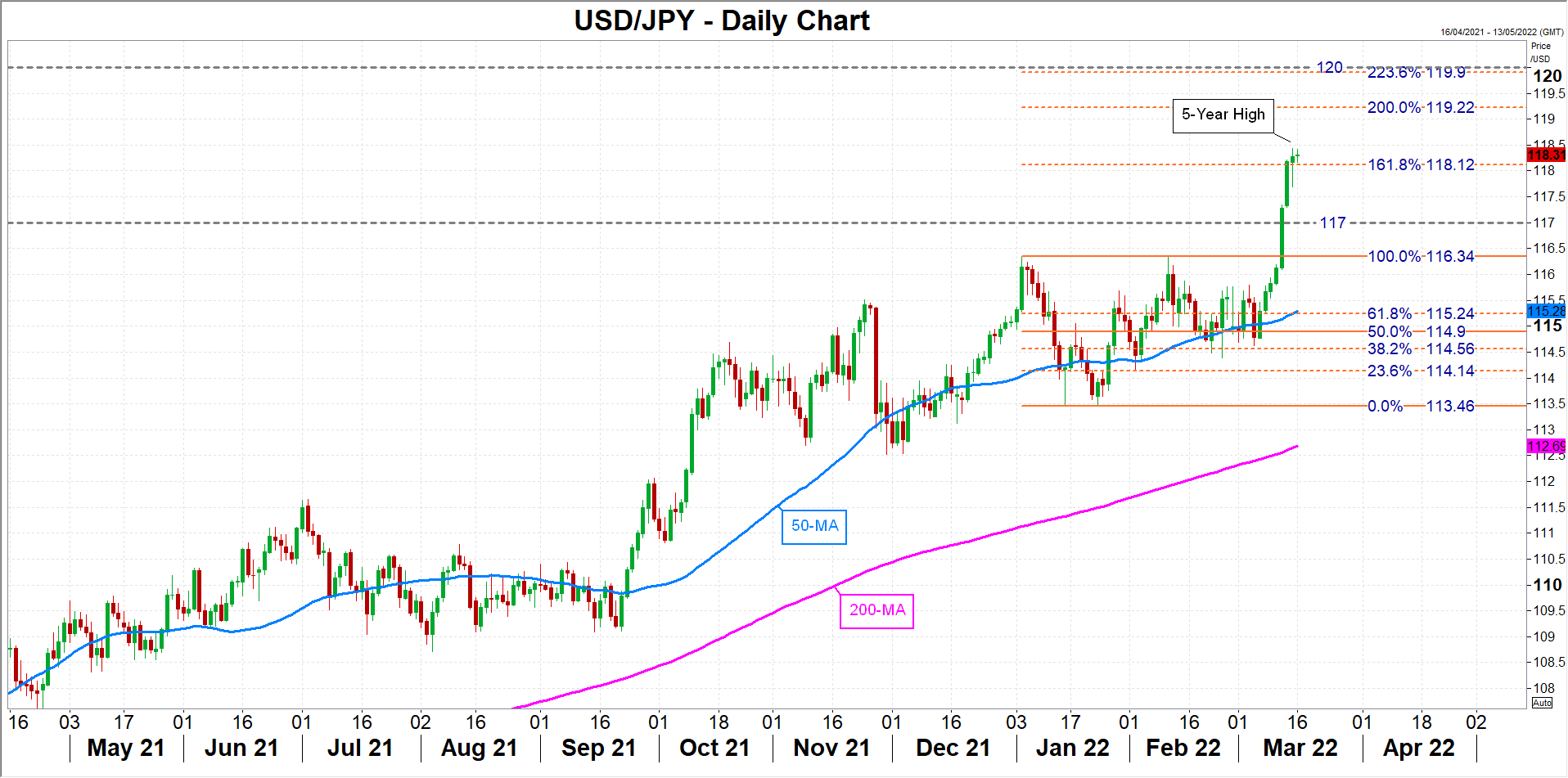

Dollar eyeing 120 yen

Should Kuroda acknowledge the upside risks to inflation and hint that adjusting the yield target is on the cards, dollar/yen could fall back towards the 117 level. Breaching this support could see the pair revisiting the 116.35 region.

However, if the BoJ reinforces the view that it has not intention of changing policy anytime soon, dollar/yen could extend its recent gains that have lifted it to five-year highs, climbing towards the 200% Fibonacci extension of the January downtrend at 119.22 before aiming for the 120 handle, which lies slightly above the 223.6% Fibonacci.

{kind=link}