It will be a packed week for the British pound. The Chancellor of the Exchequer Rishi Sunak will present his spring statement before the parliament on Wednesday. UK CPI inflation figures will be published on the same day at 07:00 GMT, while on Thursday and Friday, investors will pay attention to flash Markit/CIPS PMI data (09:30 GMT) and monthly retail sales (07:00 GMT) respectively to get more evidence on the economy. The war in Ukraine is clouding the outlook for the foreseeable future, though if the calendar events manage to restore some optimism, the pound could extend its recovery.

What will Sunak’s spring budget include?

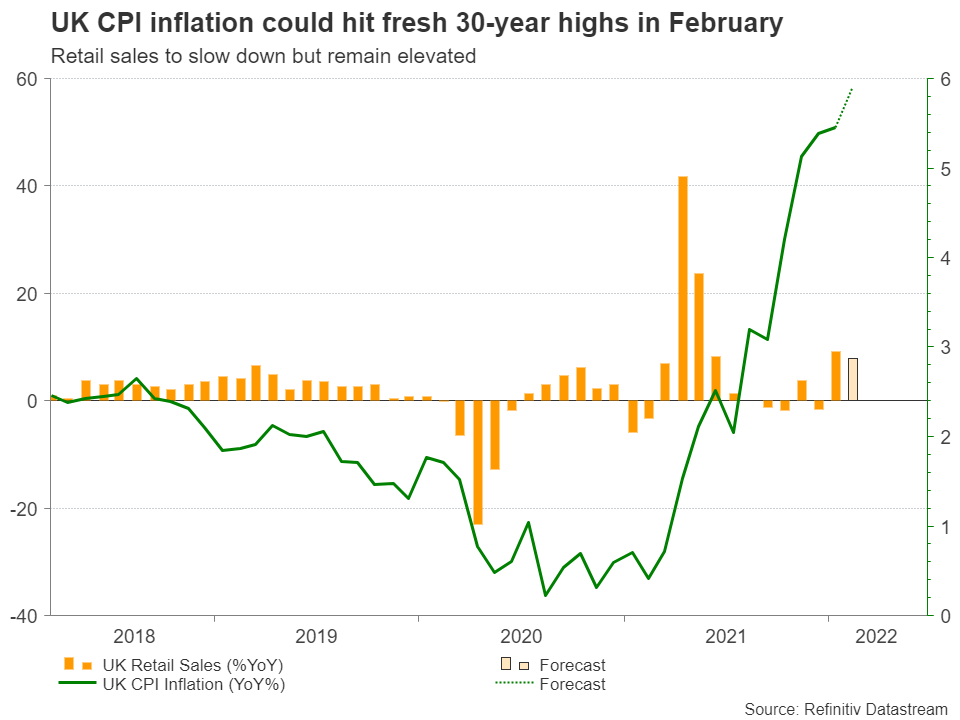

Rishi Sunak is expected to announce a package of supportive measures when he delivers his spring budget before parliament on Wednesday. Before the invasion in Ukraine, the event was intended to be just an economic update, involving new projections from the Office for Budget Responsibility. However, conditions have changed since then. The bombardments in Ukraine alongside the heavy global sanction war against Russia and its oligarchs could force the government to provide another helping hand this week as economists predict higher and more persistent inflation, and therefore a worsening living-cost-crisis in the coming months. The headline CPI inflation figure for February is expected to climb to a new 30-year high of 5.9% y/y and the next releases could be even hotter.

Of course, the government has already released some extra money in February in response to the pandemic-led rising energy and electricity costs, including a £150 tax rebate for some homes and a £200 credit on energy bills to be repaid over the next five years. However, with the Ukrainian nightmare threatening to bolster the already boiling inflation pressures, the Chancellor will probably have no other choice than assisting households and business finances once again.

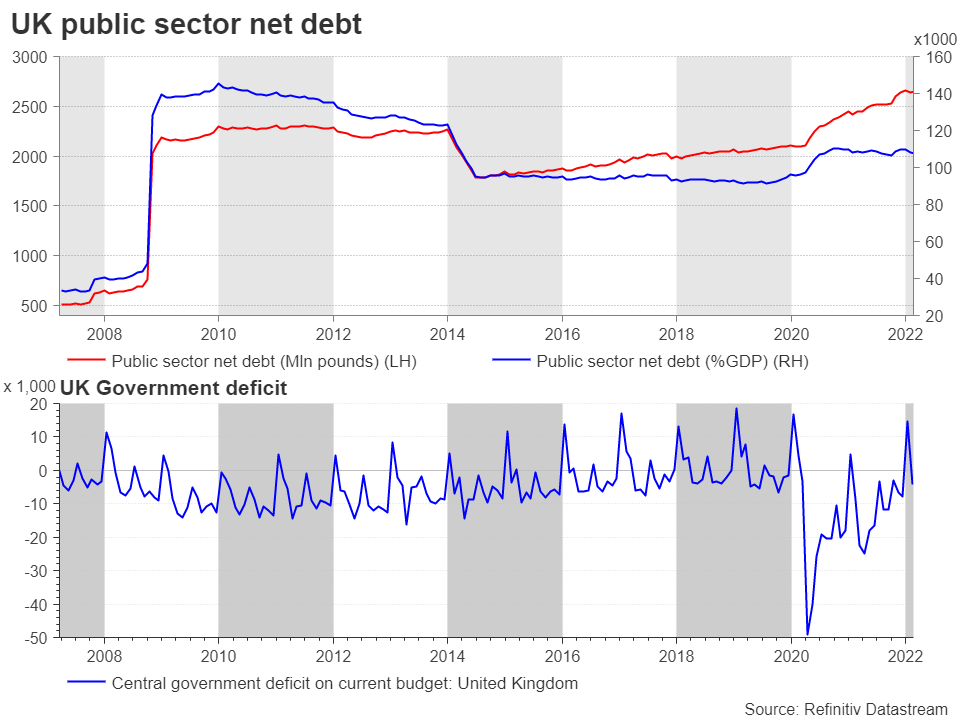

The real question that arises here is if the spring statement will bring any meaningful changes. The UK’s national debt has jumped to around 100% of GDP, the highest since 2014, from around 80% at the end of 2019, while the penalties against Russian oligarchs are not cost-free and could weigh on the British financial system. Hence, besides some additional benefits for childcare, extra giveaways to help households to pay their energy bills and secure petrol tank refills, the government could face strong challenges in re-opening its liquidity taps. Particularly, there is a tough debate whether Sunak will temporarily reverse or delay the £12bln increase in National Insurance, which is set to go up by 1.25% to 13.25% in April, and is a key fund to the NHS.

Moreover, whether the VAT rate will return to 20% at the end of March after falling to 5.0% because of the pandemic, and then rising to 12.5% last October, could be another challenging decision. Overall, some analysts estimate public sector borrowing to rise from £83bn to £100bn in 2022-2023.

Flash business PMIs and retail sales could lose steam, but no worries

As regards the impact on the pound, investors have already priced a slowdown in growth projections and a pickup in inflation estimates. Potentially, they are also largely forecasting additional but careful financial support from the government. Hence, if that turns out to be the case, the spring statement and CPI inflation readings could create little volatility to the pound, with the spotlight shifting next to the flash PMI Markit/CIPS business PMI figures and monthly retail sales.

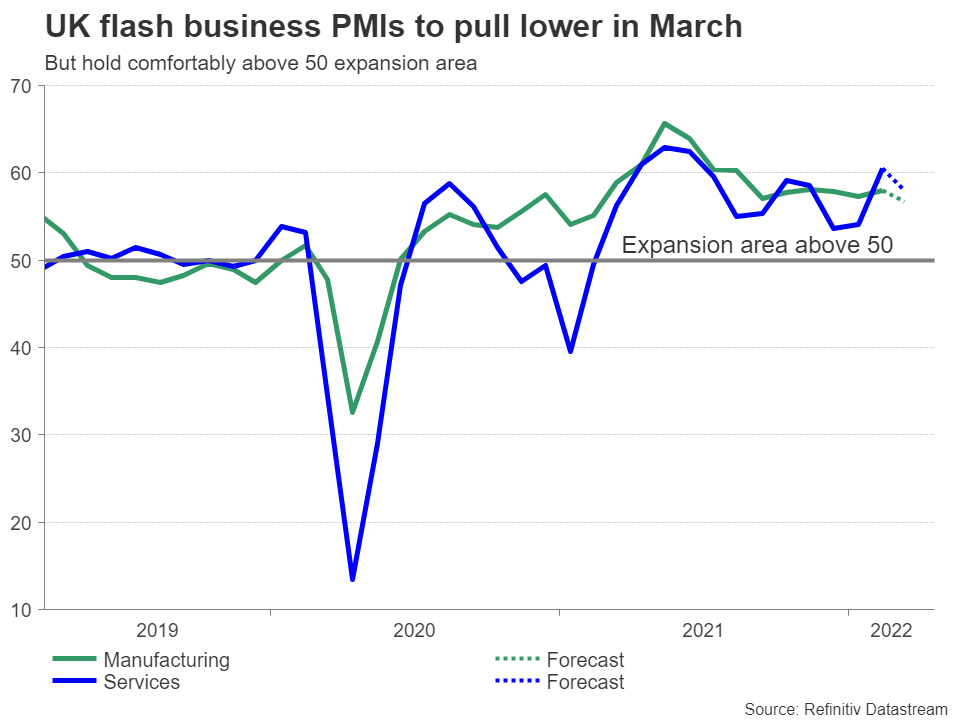

Preliminary PMI data may attract special attention since they regard the month of March and hence may reflect the impact of the geopolitical crisis on business sentiment to some extent. Analysts estimate a weaker print of 56.7 for the manufacturing sector compared to 58 previously. The more important services PMI is also expected to decelerate from 60 to 58, driving the composite PMI to 57.8 from 59.9 in the preceding month. Nevertheless, such an outcome would still keep the business sector comfortably in the expansion area, and unless the readings surprise strongly to the downside, justifying the Bank of England’s cautious approach to faster rate increases, investors may not engage in heavy selling activities.

Monthly retail sales for February could create some discomfort on Friday if the data show a sharper deceleration than analysts predict. The annual growth is expected to weaken to 7.8% from 9.1% previously, while excluding fuel products, the core measure could post a softer increase of 5.6% y/y versus 7.2% in January. Those, however, would still be among the highest readings recorded since mid-2021.

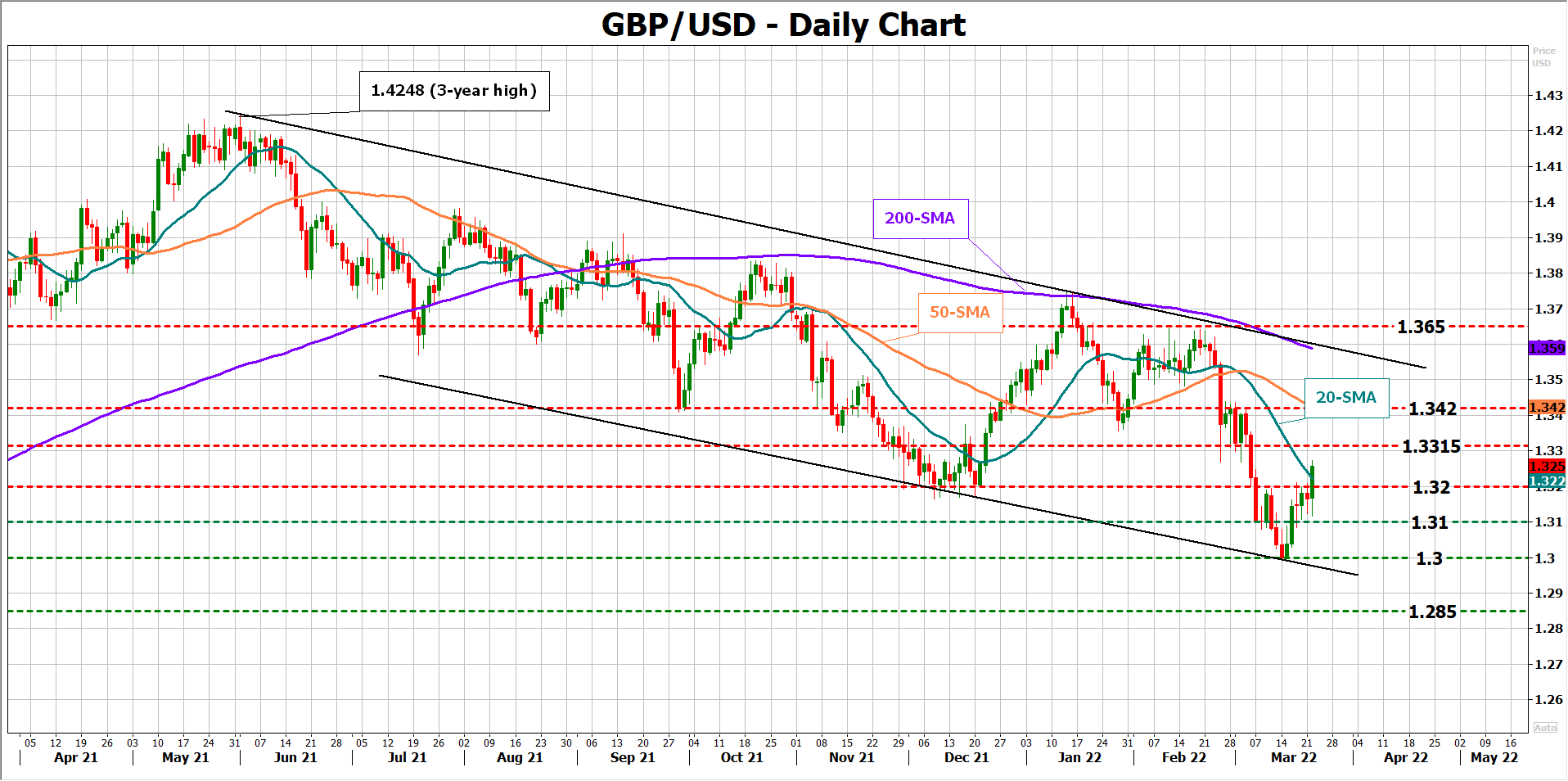

GBP/USD

Turning to pound/dollar, the pair geared above the 1.3200 level on Tuesday after a feeble start to the day. The next resistance could pop up around 1.3315 and then probably near the 50-day simple moving average and the 1.3420 mark. A positive surprise in flash PMI readings, and overall a brighter outlook for the UK economy, could resurface thoughts of faster monetary tightening, helping the pound to reach those levels and even drift higher.

Alternatively, a cautious speech from the Chancellor and disappointing data releases could pressure the pair towards the 1.3200 – 1.3163 region. Yet, only a close below 1.3100 could reduce confidence in the latest bullish price reversal, bringing the lows around 1.3000 on the radar again.

{kind=link}