The core PCE index due for release on Friday at 12:30 GMT will be the last piece of economic information ahead of the Jackson hole symposium. Hence, although investors have already gotten some taste of inflation in July and may not get surprised in the wake of a potential slowdown, personal consumption and income figures accompanying the survey might still be important to watch. If the figures mirror a fragile demand picture, the latest bearish correction in the dollar may gain another leg.

Investors vs Fed

Two contradictory scenarios are currently playing in investors’ minds. On the one hand, the latest pullback in the US CPI inflation immediately signaled a less hawkish Fed in the year ahead. On the other hand, the latest commentary from Fed policymakers surprisingly played down that case and backed additional aggressive rate hikes instead.

Well, markets have been in this confusing situation more or less a year ago when investors were increasingly foreseeing an inflationary period and higher interest rates ahead, whereas the Fed was seeing only a transitory growth in prices and a steady policy only to find later that it was wrong. The horizon is now dangerously cloudier than during the optimistic post-lockdown period as recession risks are more real than ever. Besides the ongoing pandemic negative spillovers, the climate and war-related constraints have further worsened the supply outlook for energy and other raw materials and the question that arises here is: will investors be correct for a slower monetary tightening this time?

Core PCE to inch down as US economy loses steam

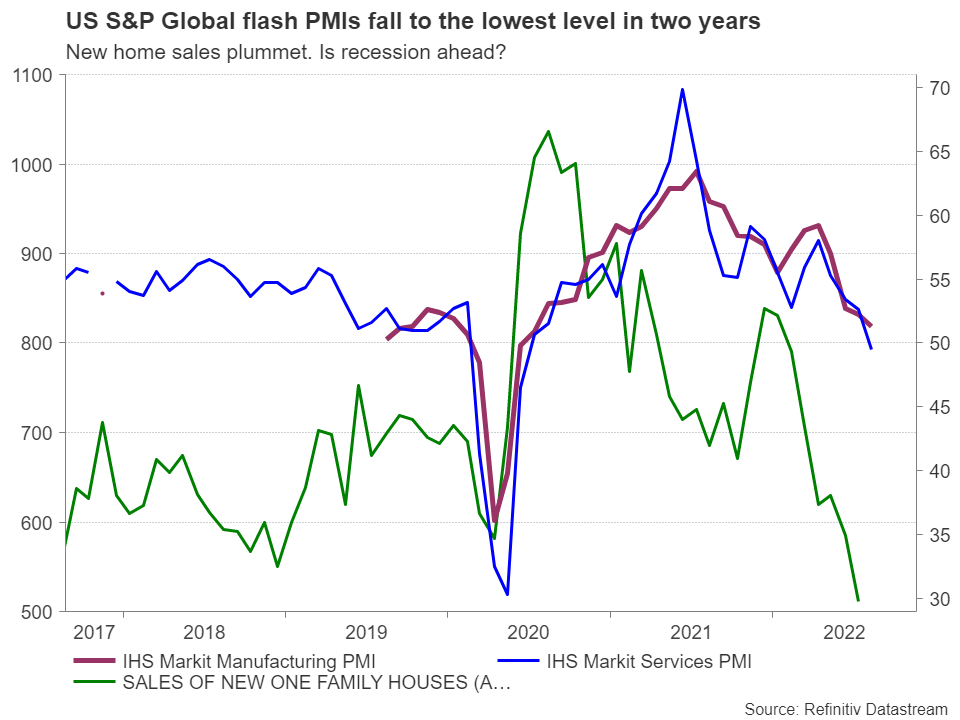

The truth is that evidence from recent data is leaning towards a less hawkish side. After a miss in CPI inflation, July’s flash business PMI figures also diminished faster than analysts anticipated, with the services sector moving deeper in the contraction area. Softer hiring, subdued domestic and foreign demand conditions, and easing but still expensive input costs were a common drag in both the services and manufacturing indices, signaling that the cocktail of rising interest rates and above-target inflation has started to rein in consumers’ appetite to spend.

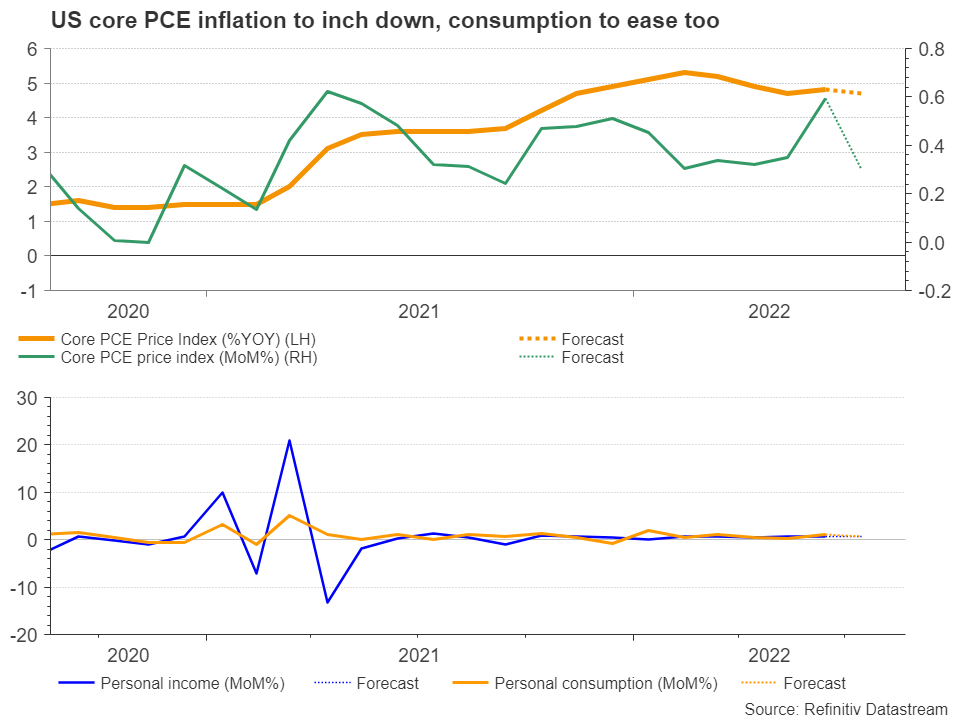

The Fed’s favorite inflation measure, the core PCE index, will shed more light on the above argument on Friday. Following the slight pickup in June, the measure is expected to flip slightly back to May’s level of 4.7% from 4.8% previously, remaining below the March peak of 5.3%. The monthly reading is also projected to ease from 0.6% to 0.3%.

Demand conditions closely monitored

Such a scenario would not be very surprising given July’s lower-than-expected CPI inflation data. Hence, investors may pay more attention to the monthly personal consumption and income stats as they are eager to learn whether demand has indeed switched to a downhill slope. Discouragingly, the former is expected to trim June’s rebound to return to 0.6% m/m from 1.1% previously, while the latter is forecast to stay steady at 0.6% m/m, reflecting little distress among consumers.

A worse-than-expected outcome could strengthen the case for a less hawkish Fed in September, making the US dollar lose some of its shine.

Inflation remains top priority

Currently, future markets are indecisive between a 75 bps and 50 bps rate hike in September, with the former priced at a probability of 58%. Perhaps any data surprises could easily shift the odds accordingly, but traders will likely seek stronger signs of commitment when the Fed chief Jerome Powell delivers his Jackson Hole speech on Friday. Probably that will not be his last word before the September FOMC policy meeting as the central bank will wisely wait for the next nonfarm payrolls and inflation reports to get a clearer picture on the economy before announcing any critical twists in guidance.

Still, given the Fed’s priority to cool the still monstrously high inflation as fast as it can, and the hot labor market, policymakers may not hesitate to repeat July’s 75 bps rate increase in September and Powell will likely avoid any big changes in guidance this week until further notice.

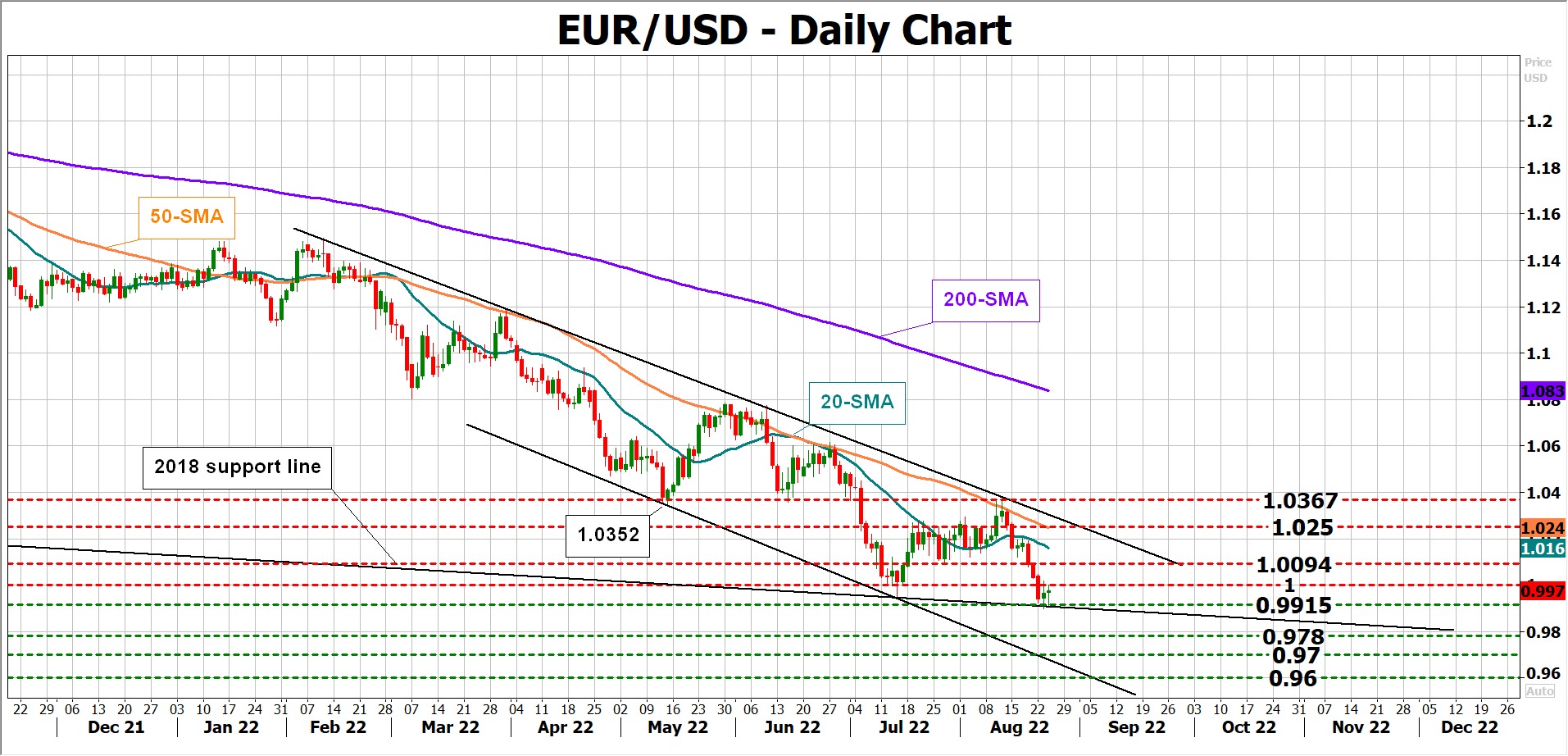

EUR/USD

Looking at EUR/USD, the pair is trading bearish within a downward-sloping channel just below parity at 0.9913, holding its feet above the long-term support line that joins the lows from 2018. If the upcoming data increases the stakes for a slower Fed tightening, the pair could pivot northwards to test parity and then the 1.0094 barrier. Higher, the 20-day simple moving average (SMA) at 1.0157 could add some pressure ahead of the channel’s upper boundary and the 50-day SMA around 1.0250.

Alternatively, should the stats promote a continuation of the current rate hike pace, the pair could plummet towards the 0.9780 – 0.9700 support region taken from 2002, where the channel’s lower boundary is also positioned.

{kind=link}