Things are looking up in the euro area with business activity ticking higher in the first two months of 2023, easing concerns about an imminent recession. Falling energy prices, improving supply chains and a relatively mild winter have all contributed to staving off a major economic downturn. However, the euro has been unable to break new ground in its uptrend and has been drifting lower since the beginning of February. Have the upside risks been already fully priced into the euro or is this just a waiting game until the March policy decisions when both the Federal Reserve and European Central Bank will update their policy outlooks.

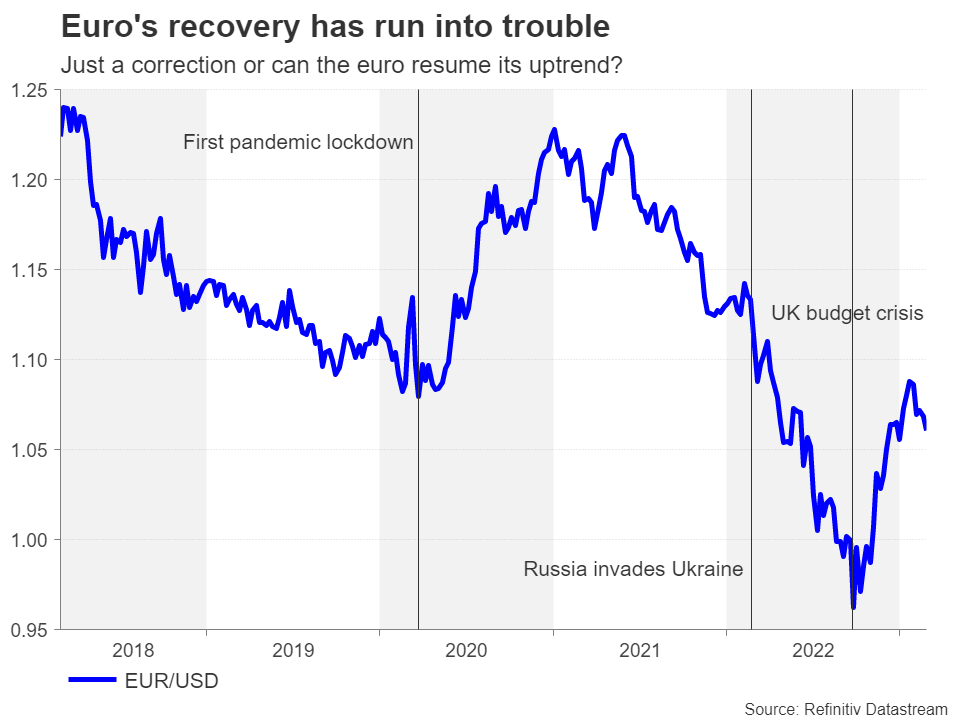

Euro loses its shine

The euro rallied about 15% from its low point in September 2022 to its peak in February this year. The gains were driven mainly by the ECB taking an increasingly hawkish stance as well as speculation that the Fed is nearing the end of its tightening cycle. These expectations were supported by the comparative data on the two economies, as European indicators kept beating the forecasts, while the American economy displayed signs of a sharp slowdown towards the end of 2022.

However, the tide seems to be shifting again as the US economy has not only regained some growth momentum, but also the rate of decline in inflation is moderating. Investors have had to price in at least two additional rate increases for this year since December as the Fed’s ‘higher for longer’ policy stance finally started to sink in. But expectations for the ECB’s terminal rate have risen too as the euro area outlook has brightened. Yet, even after the latest repricing, the euro has been unable to make much headway.

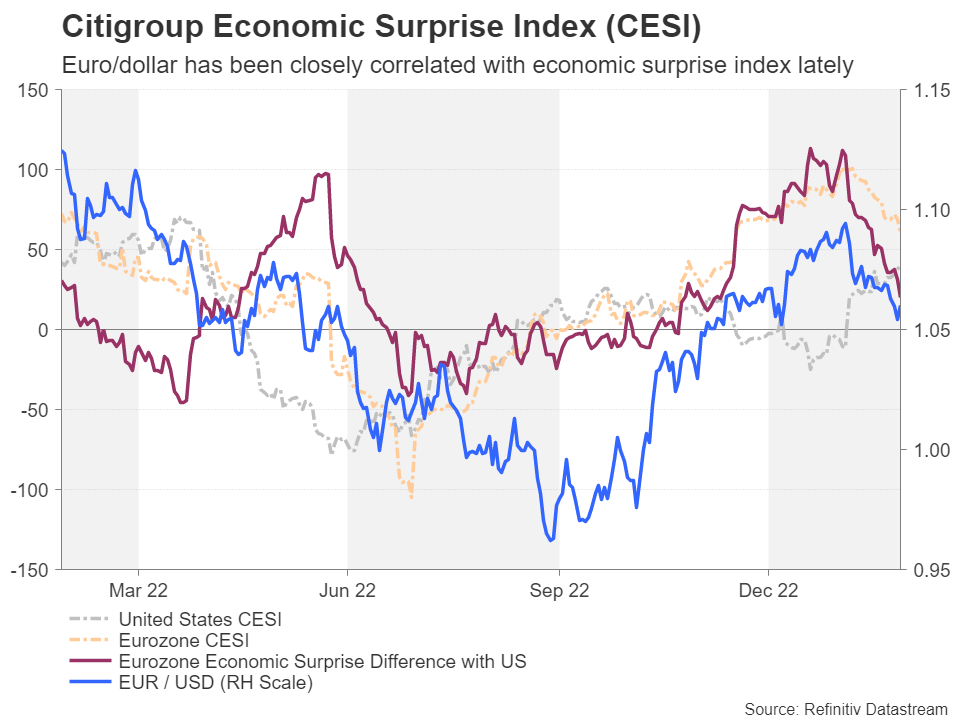

One way of looking at it is that the gap between the positive surprises in European data versus the US has narrowed and so the boost to the currency from this particular source has started to fade. At the same time, the spread between US and Eurozone yields has started to widen again, increasing the attractiveness of the US dollar over the euro.

Battling it out in the economic league table

But what happens from hereon is not clear. Both economies have proved to be more resilient than anticipated against the backdrop of higher prices and rising borrowing costs and both the Fed and ECB have sent strong signals to investors that getting inflation down is their top priority. It could be argued therefore that euro/dollar’s performance will come down to which central bank pauses first and which economy emerges out of the tightening cycle in better shape.

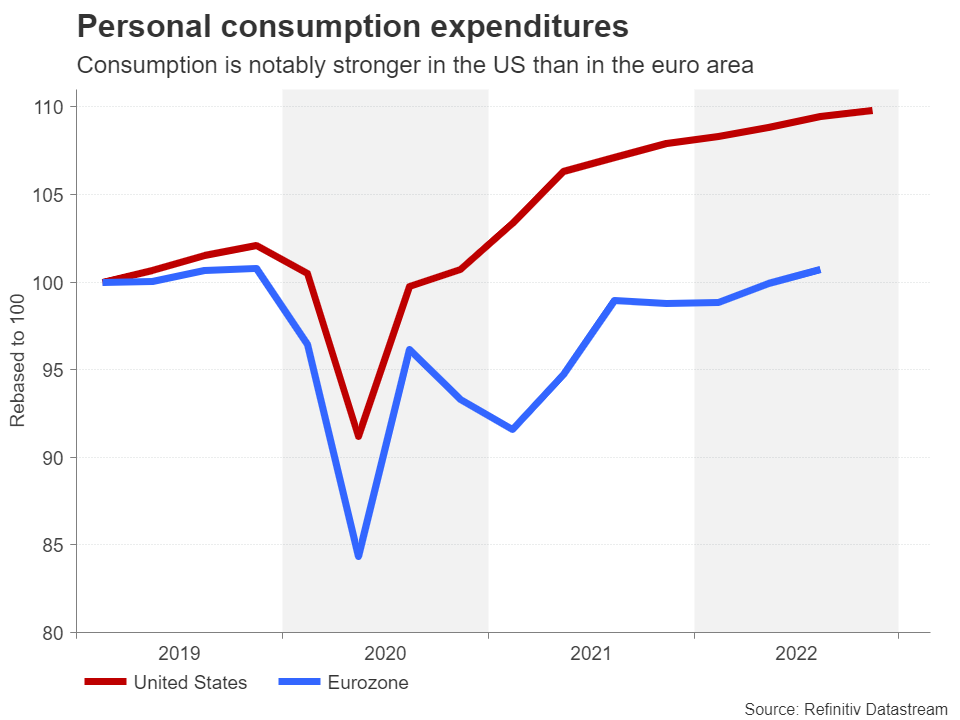

So just how robust are the American and Eurozone economies? There can be no doubt that the US economy went into the energy crisis and broader inflation storm in a much stronger position as it made a swifter recovery from the pandemic. The labour market remains hot despite a cumulative 450 basis points of rate increases. Consumers have started spending again after tightening their purse strings towards the end of last year. Even the manufacturing sector is showing some signs of a rebound.

In comparison, consumption in the euro area has been notably weaker ever since higher energy bills began to bite. Businesses also took a more direct hit from the fallout of the war in Ukraine than their US counterparts. But confidence among both consumers and businesses is returning now that fuel costs have come down from sky-high levels. Moreover, European manufacturers are likely to benefit more from China’s reopening than US exporters.

One less obvious positive about the Eurozone has been the labour market. Although it’s not anywhere near as tight as it is in America, the European jobs market has been booming since the post-pandemic recovery began, and combined with generally higher savings rate than across the Atlantic, this bodes well for future consumption.

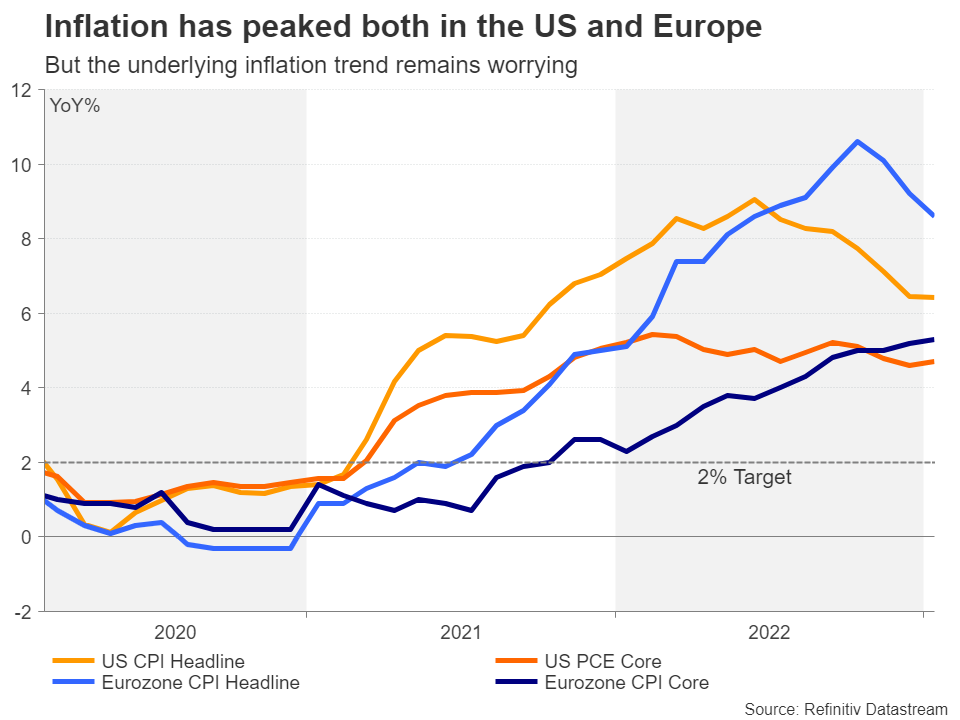

The inflation fight is far from over

But what about inflation? In America, the consumer price index peaked lower and was falling faster until January when it appeared to stall. More worryingly, underlying inflation as measured by the core PCE price index crept up to 4.7%. This is still lower than the core metric in the euro area that strips out food, energy, alcohol and tobacco prices, which climbed to 5.3% in January.

Based on the inflation data alone, the ECB has more work to do than the Fed. It’s hard to tell how much of the difference in inflation rates is to do with the Fed having been a lot more aggressive in 2022 and how much of it is because of the Eurozone’s greater exposure to the energy crisis, but the ECB’s more cautious approach to rate increases has left it further behind the curve than the Fed.

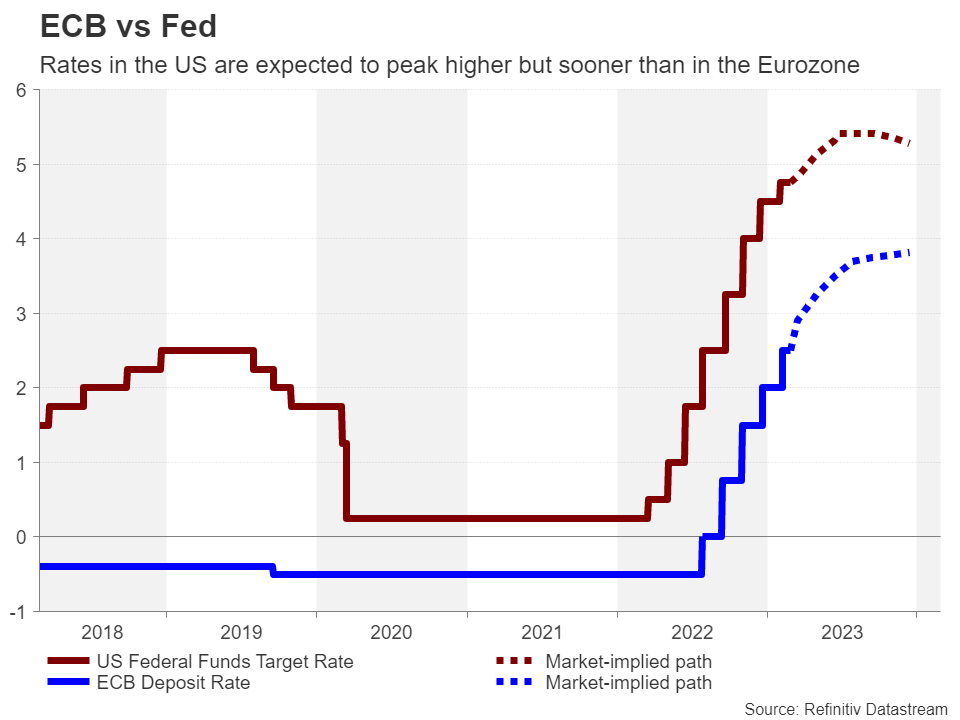

Markets are currently pricing in at least another 150-bps worth of rate hikes in the euro area versus another 75 bps in the US. For euro/dollar, however, this may not be much of a game changer. Even though it is very likely that rates in the US will peak higher than in the Eurozone and the latter’s lower tolerance threshold for elevated rates puts the euro at a major disadvantage, what may matter more in 2023 is not so much the end point but who makes the first dovish pivot.

Will the Fed pause before the ECB?

And on that, expectations that the Fed will call time on rate hikes before the ECB does haven’t changed. This provides the euro decent with odds to resume its uptrend at some stage over the coming weeks, potentially as early as the March policy meetings. The ECB meets on March 16 and the Fed on March 22.

As long as the Fed doesn’t sound the alarm bells over inflation taking longer than anticipated to drop back to 2% and the median projection of the terminal rate in the dot plot is revised higher by only 25 bps, this could work in the euro’s favour, especially if the ECB on its part keeps the door open to another 50-bps hike after March.

There is some risk that FOMC members might pencil in a much-higher-than-expected terminal rate to save face from having downshifted to 25 bps too soon. But perhaps the bigger danger is that the March decisions fail to offer significant clarity on how much further tightening is left to go, potentially leaving euro/dollar paralyzed at least until the summer.

The clouds have yet to fully clear over the outlook

By that point, policymakers will probably have a better idea on the amount of additional work needed to tame inflation and whether the major economies have indeed managed to dodge a recession or not. In the scenario that inflation turns out to be a lot stickier than is currently predicted, the dollar is likely to be the winner as the Fed would respond more forcefully than the ECB to persistent price pressures. In addition, the greenback’s safe haven attributes would attract increased flows from heightened uncertainty about an impending downturn.

However, if this setback with inflation’s climbdown slowing down proves to be temporary, there isn’t another wave of rate hike bets being pushed up by investors and policymakers are confident about a soft landing, the euro would be well placed to revisit the $1.10 handle, if not the $1.12 level. The dollar tends to depreciate at times of global risk appetite so even if both the US and Eurozone economies avoid a hard landing, the euro could still notch up fresh gains.

{kind=link}