U.S. Highlights

- Headline inflation rose 0.1% m/m in March, while core rose by a strong 0.4% m/m. The 12-month change on headline slipped to a near two-year low of 5%, while core ticked higher to a still uncomfortable 5.6%.

- Retail sales (-1.0% m/m) slipped again in March, falling for a second consecutive month after an unusually strong start to the year. Declines were seen across most categories, leaving a weak handoff heading into Q2.

- Though there are tentative signs the economy is cooling, the Federal Reserve likely has one more 25 basis-point rate hike to follow through on in May, before pausing to better assess the full impact of rate hikes.

Canadian Highlights

- The Bank of Canada held the policy rate at 4.50% for a second straight decision. Markets believe interest rate cuts are on the docket in 2023, but Governor Macklem has pushed back against that notion.

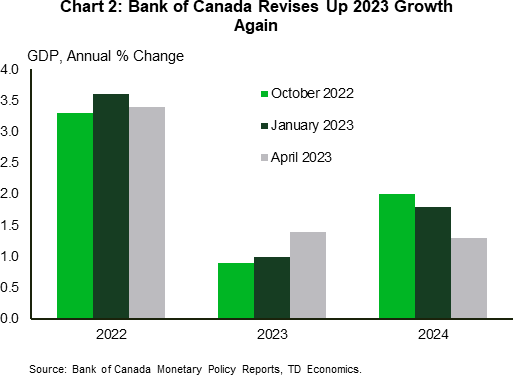

- The Bank of Canada revised up 2023 GDP growth yet again in its latest Monetary Policy Report (MPR). The Canadian economy continues to power forward and expectations for 2023 growth are now at 1.4%, revised upward by 0.4 ppts from the January MPR.

- Canadian CPI inflation data is on watch for next week, where we expect a cooling in both headline and core measures.

U.S. – Calm Prevails As Economy Shows Tentative Signs of Cooling

Rounding the corner into earnings season, a sense of calm seemed to descend across financial markets this week. But with earnings season not officially in full swing until Friday morning, investor focus fell squarely on the economic data. The two headliners this week were the March readings of CPI inflation and retail sales, though the release of the FOMC meeting minutes also garnered some attention.

The latest move by the Federal Reserve occurred during the recent regional banking crisis, which ultimately forced the FOMC to rethink its trajectory for the federal funds rate. The uncertainty was on full display in the minutes, where several participants thought it was appropriate to hold the target range steady last month in light of recent events. This was an abrupt U-turn from what policymakers had communicated just a few weeks prior to the interest rate announcement, where the thought was rates needed to move both higher and faster relative to what had been assumed in the December’s Summary of Economic Projections. But perhaps the most noteworthy takeaway from the minutes was an explicit mention that considering the recent banking crisis “… the staff’s projection included a mild recession starting later this year, with a recovery over the subsequent two years”. Indeed, participants agreed that the actions taken by the Federal Reserve and other government agencies helped calm conditions in the banking sector but deemed that it was still too early to assess the confidence and magnitude of the effect of credit tightening on the real economy.

This morning’s retail sales gave a first glimpse into the impact that tighter credit conditions may already be having on households. Both nominal and real spending fell 1.0% m/m in March, marking the second consecutive month of declines. But even after accounting for the pullback, consumer spending is still tracking a robust 4.2% for Q1. However, the weak handoff from March suggests last quarter may have been the “last hurrah” as the cumulative effect of higher interest rates alongside the recent tightening in lending standards appear to be bearing down on the consumer.

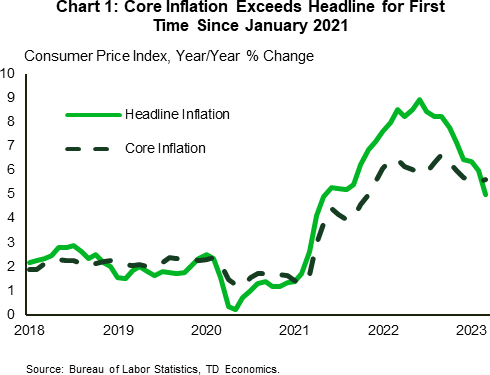

From an inflation standpoint, the softening in demand has yet to manifest in any significant easing in core consumer price pressures. Indeed, headline inflation slipped to 5% y/y – a near two-year low – thanks to lower food and energy prices (Chart 1). However, core CPI rose 0.4% m/m, leaving the 3-month (annualized) and 12-month rates of change at 5.1% and 5.6%, respectively. Underpinning the gains was an acceleration in goods prices alongside continued strength in shelter (0.6% m/m) and non-housing services (0.3% m/m).

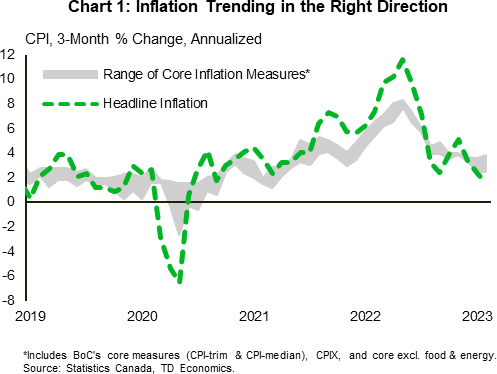

For a central bank who has become increasingly data dependent, the continued persistence in core inflation alongside the recent uptick in inflation expectations is unlikely to sit well (Chart 2). Provided there are no further flare-ups in financial markets, it is likely that the FOMC will need to raise the benchmark rate by another 25-bps in May, before pausing to better assess the full impact of the 500-bps of rate hikes.

Canada – Bank of Canada Versus Markets

The spotlight was on the Bank of Canada’s (BoC) interest rate decision this week. As was widely expected, the Bank left the policy rate unchanged at 4.50% for a second straight decision. However, where markets and the Bank differ is how long this policy pause will last.

Markets are still maintaining their conviction that the policy rate will be cut later this year. But, when asked about the potential for near-term rate cuts, Governor Macklem’s answer was explicit, “that doesn’t look today like the most likely scenario to us”. Markets caved a touch, shifting out the timing of a 25-basis point cut from September to December. As the dust settles, we too would lean against markets, and expect the 4.50% policy rate is here to stay for the remainder of the 2023.

At this meeting, the BoC struck out the reference to its ‘conditional hold’ and skewed its language toward a bias for potential further tightening. The BoC acknowledged that the return to the 2% inflation target could prove to be more difficult than expected. Inflation is cooling, and our forecast calls for Canadian inflation reaching 3% year-on-year (y/y) by the summer. This is progress, but it’s not the 2% level the BoC is striving to achieve. The message was cemented by Macklem at an IMF meeting the following day where he stated, “that band, it’s not a zone of indifference. You need to aim for the middle if you want to be in the band most of the time”.

As inflation continues to rein itself in, the BoC will take a narrower lens in assessing if easing price pressures are sustainable. Core inflation has been trending downward (Chart 1), but they will also continue to watch inflation expectations and wage growth, which are proving to be a bit stickier.

The Canadian economy is still showing signs of resiliency, forcing the BoC to revisit growth estimates yet again. The April MPR shows GDP growth for 2023 revised upward to 1.4%, 0.3 percentage points (ppts) higher than in the January MPR (Chart 2). A consumption led slowdown through the remainder of 2023 provides a weak hand off to 2024, leading to a downward revision to the growth forecast to a modest 1.3% (1.8% in the January MPR).

A smattering of Canadian data this week added further support to a strong first quarter. Manufacturing sales gave back some of January’s 4.5% gain in February (-3.6% m/m), but sales are still tracking positive for the quarter. Existing home sales and prices were up in March, 1.4% and 2.0% m/m, respectively. This reinforces that housing markets are finding their bottom.

Next week’s highlight is the March inflation (CPI) release, where we expect a further cooling in headline and core inflation measures. We see headline inflation pulling back for a fifth straight month to 4.6% year-on-year (y/y) and core to moderate to 4.5%. Also on tap, retail sales for February are tracking another gain, following strong consumer spending in the last two months.

Minutes of the Federal Open Market Committee")

%20interest%20rate%20decision%20this%20week.%20As%20was%20widely%20expected,%20the%20Bank%20left%20the%20policy%20rate%20unchanged%20at%204.50%%20for%20a%20second%20straight%20decision.%20However,%20where%20markets%20and%20the%20Bank%20differ%20is%20how%20long%20this%20policy%20pause%20will%20last.){kind=link}