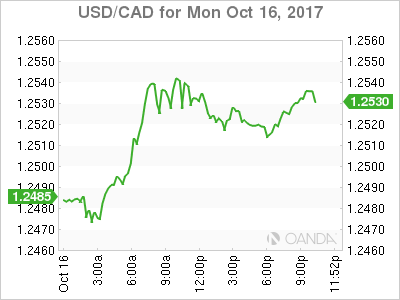

The Canadian dollar depreciated on Monday after the release of the Bank of Canada (BoC) survey of managers. The Business Outlook Survey fell from 2.81 last quarter to 0.86. The anticipated slowdown in economic growth after it expanded at an accelerated growth was reflected in the reduced forecasts. The end result still points to a healthy economy, but not at the same pace that put the central bank into hiking rates twice.

The NAFTA negations have been anything but smooth sailing. The US trade delegation has been pushing for more America First clauses that have not been taken well by the Canada and Mexico delegations. The US tabled an idea a higher regional content for autos to be part of the free tariff access. Current North American content requirement is 62.5 percent and the US wants to increase that to 85 percent (with 50 percent of that being US content).

Negotiations have been tense after the US also proposed a five year term for the updated NAFTA, to which both Canada and Mexico had already objected. US and Mexican governments wanted to wrap up trade negotiations before the end of the year, but with the current pace of progress make this very unlikely.

The USD/CAD rose 0.47 percent since the Asian open. The currency pair is trading at 1.2528 as the US Empire State Manufacturing index posted a higher than expected figure. The survey of NY manufacturers was 30.2 on a 20.3 forecast. The combination of a softer BoC Business Outlook Survey in Canada and a stronger manufacturing indicator in the US further tipped the scales in favour of the US dollar.

NAFTA uncertainty has put the Bank of Canada (BoC) on alert as the loonie could lose up to 10 percent of its value if the Trump administration ends the agreement with no renegotiation. The central bank will meet next week, with 20 percent probability of a rate hike, but since the September rate hike and with a softer pace of growth a third rate hike in 2017 is still a long shot. Inflation and retail sales data later in the week will be more telling on what the BoC could do before the end of the year.

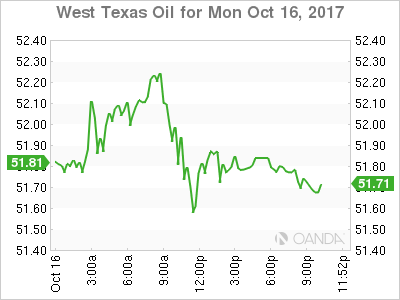

West Texas Intermediate prices have been volatile due to geopolitical events but seem to be attracted to the 51.80 level. The disruption of oil production from Kirkuk in Northen Iraq after the army seized the territory from Kurdish fighters drove prices to the $52.30. The situation is still ongoing, but for now prices remain stable below $52.

The comments from US President Donald Trump threatening to end the Iran nuclear had a positive effect on prices as lower output from oil pushed prices higher. The US congress has a 60 day period to decide if it reinstates the economic sanction to Iran.

Market events to watch this week:

Monday, October 16

5:45pm NZD CPI q/q

8:30pm AUD Monetary Policy Meeting Minutes

Tuesday, October 17

Tentative GBP BOE Gov Carney Speaks

4:30am GBP CPI y/y

Wednesday, October 18

4:30am GBP Average Earnings Index 3m/y

8:30am USD Building Permits

10:30am USD Crude Oil Inventories

8:30pm AUD Employment Change

10:00pm CNY GDP q/y

10:00pm CNY Industrial Production y/y

Thursday, October 19

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, October 20

8:30am CAD CPI m/m

8:30am CAD Core Retail Sales m/m

7:15pm USD Fed Chair Yellen Speaks

Interventions?")

{kind=link}