- BoJ to keep interest rates and yield curve control unchanged

- Friday’s CPI data may show abating inflationary pressures

- Wage negotiations could decide exit from ultra-loose policy

- Yen suffers as markets dial back rate hikes

BoJ makes baby steps towards policy normalisation

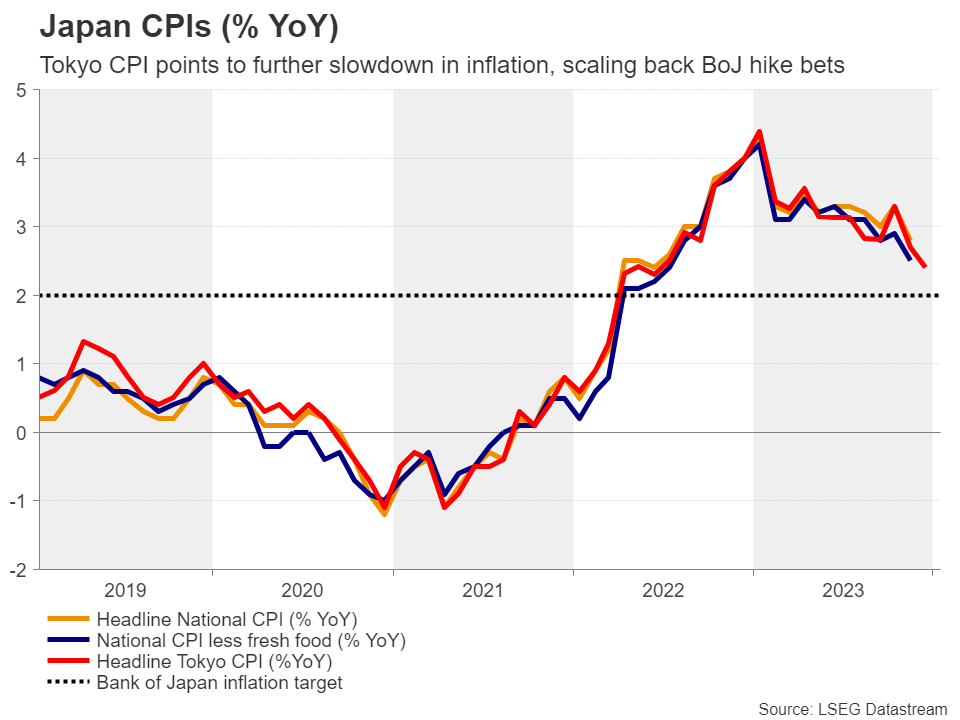

Although inflation in Japan has been above the 2% target for more than a year and a half, the Bank of Japan stood pat at its December meeting, remaining the last major central bank in the world with negative interest rates. In the accompanying statement, the Bank pushed back against a quick exit from loose monetary conditions until wage growth and inflation stabilise at target levels.

In a sense, the latest data have been favouring the Bank’s stance as inflationary pressures seem to be subsiding in the absence of any external shocks, such as the energy crisis in 2022. The Tokyo CPI print, which oftens acts as a proxy for the National CPI measures, revealed notable slowdowns in both headline and core consumer prices for December.

Hence, all eyes will fall on the upcoming CPI report on Friday, with forecasts suggesting that core inflation decelerated from 2.5% to 2.3% year-on-year in December. Such an outcome might endorse the BoJ’s cautious approach towards policy normalisation and inflict more damage on the yen.

Wage negotiations; the key for exiting negative rates

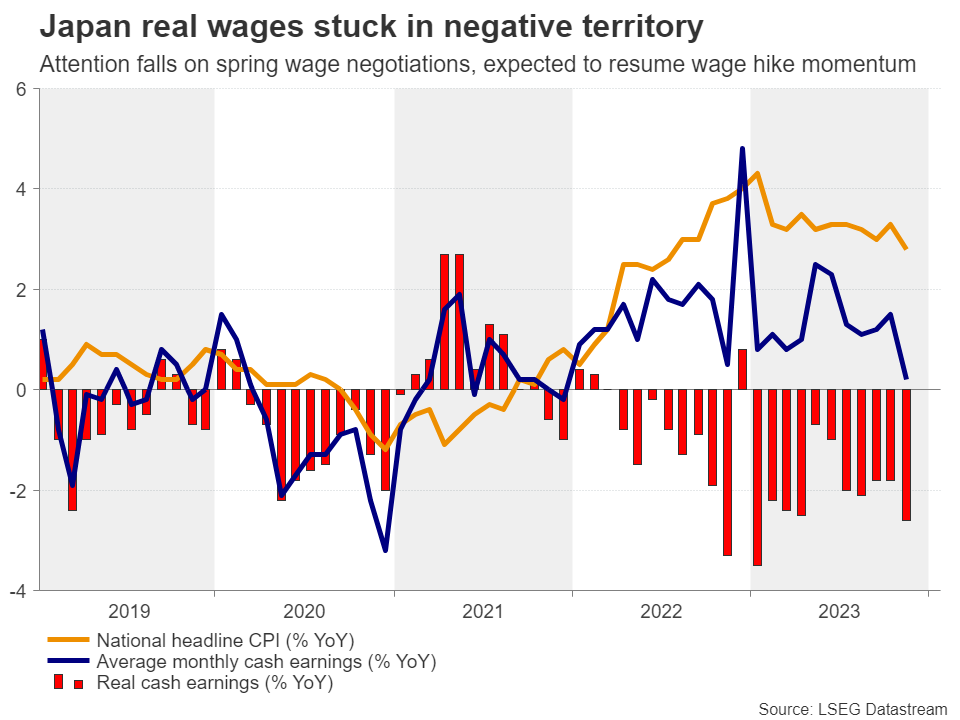

Governor Ueda has repeatedly stated in recent months that even though the BoJ is open to tightening, this won’t happen before a sizable growth in wages is confirmed. Therefore, the spring wage negotiations are deemed as the next tipping point, which could prompt the BoJ to exit negative rates.

Right now, markets are forecasting that wages will rise at a faster pace than last year’s 3.58%, driven by strong corporate profits and tight labour conditions. Given that the BoJ wants to see real wages turning positive before hiking, there is speculation that a positive outcome in annual wage talks could allow the Bank to do so in its April meeting.

However, the market pricing is currently implying that the initial rate increase will occur at the June meeting.

No change expected in yield curve control policy

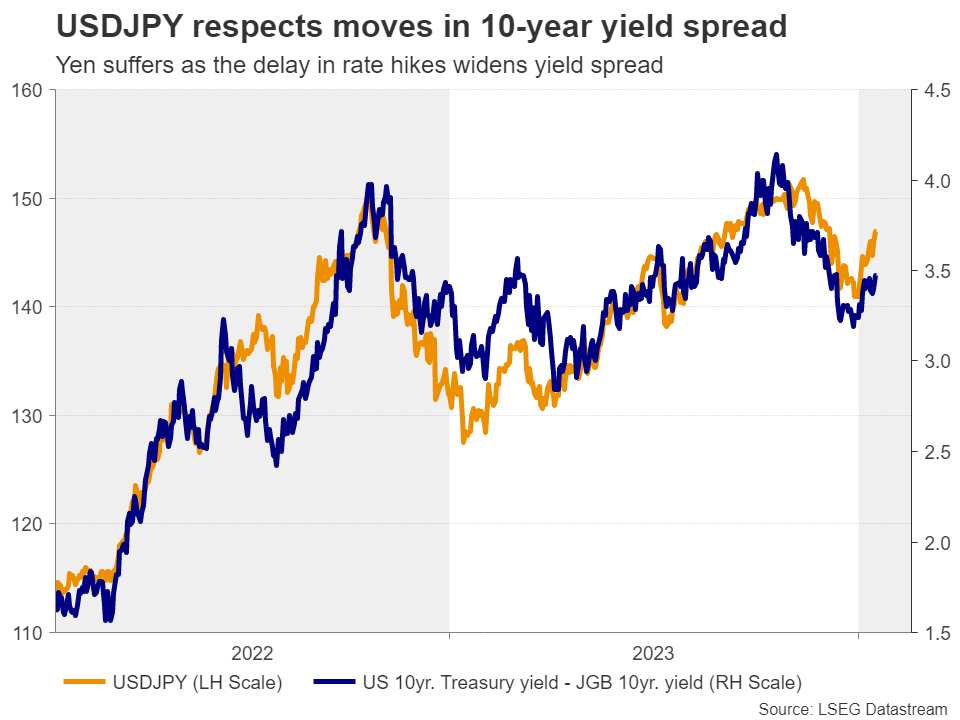

After a period of strengthening on the back of rate hike bets, the yen has been on the retreat again as the BoJ’s dovish commentary in December dialed back those expectations. Considering that rate increases are out of the picture for now, further easing in the yield curve control policy could offer some relief to the Japanese currency.

Nevertheless, such a move is not anticipated in the upcoming meeting next Tuesday, leaving the yen vulnerable to more selling pressure in the short term. Moving forward, the idea of dollar/yen reaching intervention levels does not seem far-fetched, with faster-than-anticipated cuts by the Fed being the main downside risk on the horizon.

Levels to watch

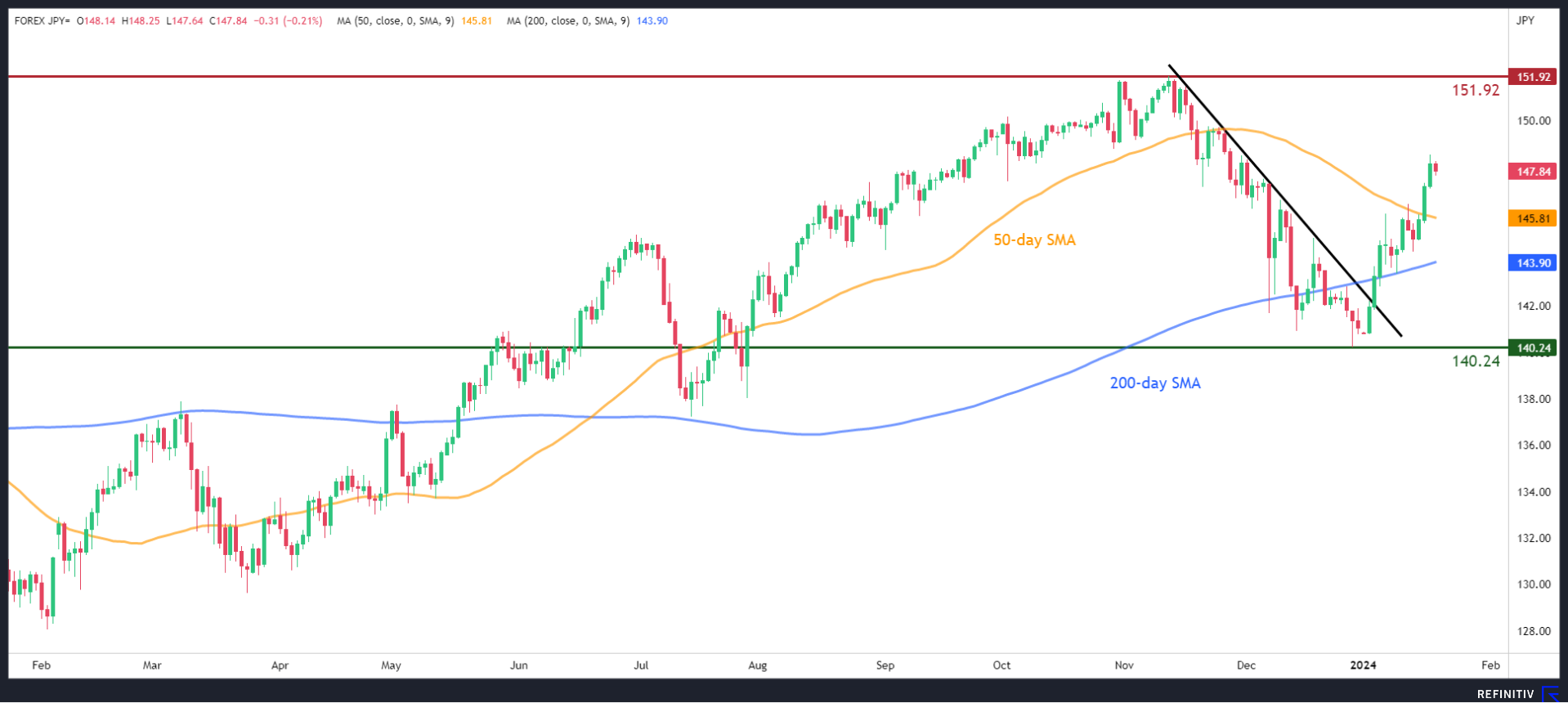

Taking a technical look, dollar/yen appears ready to erase its recent pullback in the absence of any aid from macroeconomic developments. Hence, it remains to be seen whether any hawkish remarks in the upcoming BoJ meeting could prevent the pair from revisiting intervention threshold levels.

To the upside, if the recent rebound persists, the pair might challenge the 32-year high of 151.92. Meanwhile, a hawkish meeting could bring the December low of 140.24 under examination.

{kind=link}