Sunrise Market Commentary

- Rates: Payrolls unable to give US Treasuries firm direction?

The outcome of the payrolls is highly uncertain. We see risks for a strong report. However, a Treasury sell-off won’t trigger a relevant break of key support. Similarly, key resistance looks to tough to break in case of a weak report. We envisage a sell-on-upticks in the latter case. - Currencies: Will payrolls be strong enough to inspire further USD gains?

Yesterday, the formal nomination of Jerome Powell as Fed Chairman and a proposal on US tax reforms were not able to give the dollar clear directional guidance. Today, the focus is on the US payrolls. We expect a strong report. A positive surprise in average hourly earnings is probably needed to support further USD gains

The Sunrise Headlines

- US equities ended the session nearly unchanged with the Dow outperforming after recouping early losses (on tax plan). Asian shares trade mixed with Japanese markets closed for a holiday. China underperforms.

- House Republican leaders rolled out their sweeping tax plan. The proposal cuts the corporate rate to 20%, reduces the number of individual brackets and eliminates the estate tax. It also halves the cap on the popular mortgage-interest deduction on new home sales and imposes a levy of up to 12% on offshore earnings. Trump said the bill will be law by Christmas.

- Brent headed for a fourth weekly gain, with the Saudi and Russian energy ministers possibly meeting in Uzbekistan to discuss oil-output cuts. Brent trades currently at $60.86/barrel.

- Venezuela is restructuring its global debt. President Maduro said PDVSA will make one last $1.1 billion payment before negotiating with banks and investors. Risk of contagion seems limited. Mexican peso was little changed in Asia.

- Apple forecasts record sales tied to robust demand for the iPhone X. It will help generate as much as $87 bn. in the Dec. quarter. Tim Cook said production which has had problems was "going well" and initial demand is strong."

- Mr.Powell pledged to pursue the Fed’s goals of stable prices and maximum unemployment while keeping an eye on financial market risks. Trump officially named him to succeed Janet Yellen as Fed chairman.

- Chinese Caixin-Markit services PMI rose to 51.2 in October, up from 50.6 previously. New business growth was modest while business expectations picked up slightly.

- The market calendar will be dominated by the US payrolls. Minor items are the UK services PMI and speeches of ECB Nowotny & Coeuré and Fed Kashkari

Currencies: Will Payrolls Be Strong Enough To Inspire Further USD Gains?

Will payrolls trigger a new USD up-leg?

The dollar showed no clear trend yesterday. Markets awaited the nomination of the new Fed chairman and the tax proposal of the GOP. Equities and the dollar dropped temporary as the first details of the tax plan hit the screens, but the decline was soon reversed. US president Trump as expected appointed Jerome Powell as Fed Chairman. In the end, both factors had only limited impact on markets. The nomination of Powell was largely discounted. The tax proposals are still subject to amendments. EUR/USD finished the session at 1.1658 (from 1.1619). USD/JPY closed the session in well-known territory just north of 114.

Overnight, Asian equities show modest gains. Tech stocks are supported by strong earnings from Apple published after the WS close. Chinese equities underperformed even as the Caixin services PMI rose from 50.6 to 51.2. Chinese authorities consider tighter rules on foreign investments. USD/JPY is little changed in the 114 area in light trading conditions (Japanese markets are closed). EUR/USD holds a tight range in the 1.1650/70 area. Yesterday’s rebound of the Aussie dollar is aborted by poor Q3 retail sales. AUD/USD returned below the 0.77 handle.

Today, the October US payrolls will dominate trading. After a hurricane-distorted September report, a strong bounce is expected. Consensus expects net payrolls’ growth of 323K. We side with the consensus and expected a strong figure. The unemployment rate is expected stable at 4.2%. Average Hourly Earnings are probably the most important element of the report. A moderate 0.2% M/M gain is expected. That would slow the Y/Y advance to 2.7% from 2.9%. We see the risks on the upside. Other US eco data (trade deficit, ISM, factory orders) will be only of second tier importance.

The dollar was in better shape at the end of last week, but the rebound slowed this week. The publication of a tax proposal and the nomination of Powell as Fed Chairman were not able to break the stalemate. If the payrolls (especially AHE) are strong, the dollar might try a new up-leg. However, recent price action showed that there is little room for disappointment.

LT we maintain a EUR/USD sell-on-upticks bias. Of late, the dollar failed to gain against the euro despite widening interest rate differentials since early September. This trading dynamic was broken after the ECB decision last week. Policy divergence between the ECB and the Fed is again on the radar. However, any additional rate support for the dollar will probably be modest near term. So, further EUR/USD decline might develop gradually

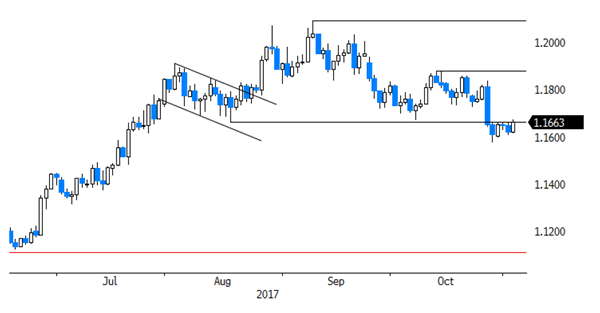

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but there are no convincing follow-through gains yet. If the break is confirmed, it would signal that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY’s momentum was positive in September. The pair regained 110.67/95 resistance, a positive. The 114.49 correction top is the next resistance. Sentiment improved last week, but the first test on Friday failed. We don’t preposition for a sustained break higher.

EUR/USD broke below 1.1662 support, but breaks still needs to be confirmed

EUR/GBP

Sterling tumbles on soft BoE assessment

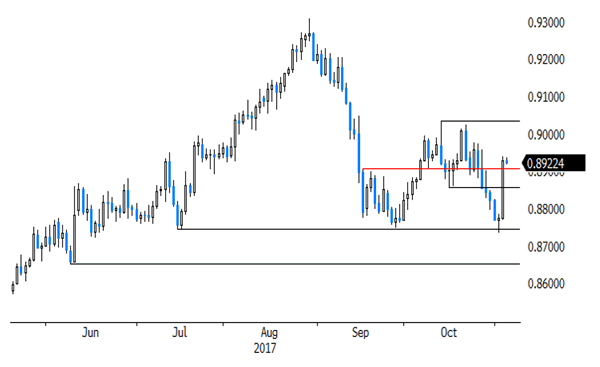

Yesterday, the BoE voted 7-2 to raise the base rate by 0.25 bp. However, the policy assessment was very dovish. The BOE assumes that inflation will return close to 2% by the end of the 3-year forecasting horizon. In order to meet the target, only two additional rate hikes are pencilled in. So, this scenario only sees very limited interest rate support for sterling medium term. EUR/GBP jumped from the low 0.88 area to 0.89 area and closed the session at 0.8927. Cable also fell off a cliff and finished the session at 1.3059 (from 1.3245).

Today, the UK services PMI will be published. A small decline from 53.6 to 53.2 is expected. This would confirm the picture that the UK economy has entered an era of lower growth. Markets will also monitor the consequences of the reshuffles within the UK government. More political instability will undermine confidence in the UK government and in sterling. In a day-to-day perspective, the decline of sterling might slow after yesterday’s sell-off. However, sterling remains vulnerable to negative eco and political news which is still highly likely to reoccur.

EUR/GBP staged a strong uptrend from April till late August with a top at 0.9307. Rising UK inflation and the BoE preparing markets for a rate hike caused a sterling rebound. This rebound did run into resistance. EUR/GBP tried to regain the 0.89/90 area, but there were no follow-through gains. EUR/GBP retested the 0.8743 support earlier this week, but rebound sharply yesterday. We maintain the view that the 0.8733 -0.8652 support area will be though to break in a sustainable way. A EUR/GBBOP buy-on-dips approach is favoured. 0.9023/33 is the first important resistance for the EUR/GBP cross rate

EUR/GBP: rebounds off 0.8733/43 support on soft BoE policy assessment

{kind=link}