U.S. Highlights

- Inflation, as measured by the Consumer Price Index, accelerated to 3.5% year-on-year in March – the highest reading in six months.

- Minutes from the Federal Reserve meeting in March showed that officials remained in favor of exercising patience amid persistent inflationary pressures.

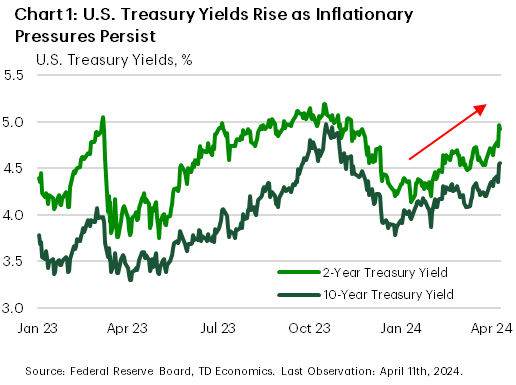

- U.S. Treasury yields spiked roughly 15 basis-points as market expectations for lower interest rates were pushed back into the second half of the year.

Canadian Highlights

- The Bank of Canada held its policy rate at 5%, while comments from Governor Macklem indicated that a rate cut is “within the realm of possibilities” at the June meeting.

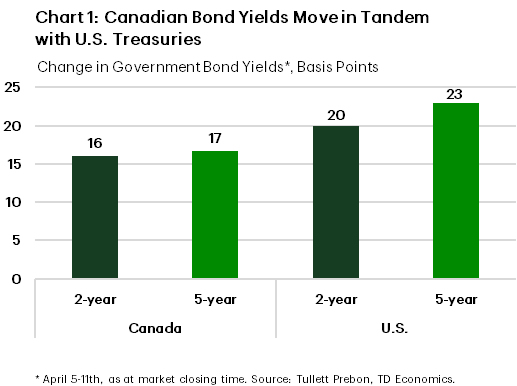

- Canadian Government bond yields moved higher in tandem with U.S. Treasuries. This may slow the Canadian housing market, reducing the extent of relief from expected rate cuts.

- The Federal government’s housing plan will increase the Home Buyers Plan withdrawal limit and extend amortization for some borrowers but will likely have a limited impact on the housing market.

U.S. – One Hundred Days into 2024, Rate Cuts Remain on the Horizon

Financial markets were caught off-guard this week as slightly hotter than expected inflation data prompted a spike in U.S. Treasury yields and a modest retreat in equity prices. As of the time of writing, the ten- and two-year Treasury yields finished the week up roughly 15 basis-points (Chart 1), while the S&P 500 fell 0.9%. While the deviation relative to expectations for the March Consumer Price Index (CPI) inflation was marginal, the underlying details proved to be more concerning.

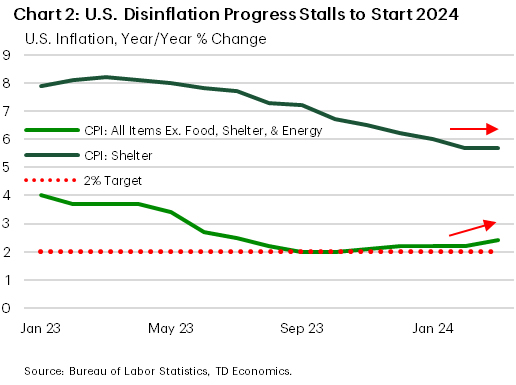

Headline inflation in March jumped to 3.5% year-on-year, with energy prices seeing positive price growth in annual terms for the first time in over a year. Excluding energy and food prices, core inflation remained unchanged relative to February at 3.8%. The reason why the disinflation process stalled in the first quarter is related to two factors. The first is that disinflation in the heavily weighted shelter subcategory moderated relative to the previous quarter. While this offered less support to the Fed’s mission to reattain price stability, the measurement of shelter prices is lagged relative to market trends by several months, and thus the direction of shelter inflation is still expected to be downward moving forward.

The second factor keeping inflation elevated was the acceleration in price growth for categories excluding food, energy, and shelter – aggregately referred to as supercore inflation. Inflation pressures within this subcategory were broad-based in the first quarter (Chart 2) which has not gone unnoticed by the Federal Reserve. In the March meeting minutes released this week, FOMC participants noted they were reluctant to discount the inflation data of the first quarter and emphasized that they would require greater confidence that inflation was on a sustainable trajectory back to the 2% target before considering less restrictive policy options.

This lined up with the even-toned statements made by Federal Reserve officials this week, including Vice Chair and New York Fed President John Williams who stated that he expects “inflation to continue its gradual return to 2 percent, although there will likely be bumps along the way, as we’ve seen in some recent inflation readings”. In a speech this week, Boston Fed President Susan Collins also stated “Overall, the recent data have not materially changed my outlook, but they do highlight uncertainties related to timing, and the need for patience”. Market pricing for the first Federal Reserve cut this year shifted from June to July this week, although market confidence remains weak with the balance of risks skewed towards the potential for a later commencement date.

Looking to next week, we receive an update on retail sales for March on Monday, which are expected to show slower growth relative to the prior month, in part owing to a moderation in auto sales. Next week also marks the start of the Spring IMF meetings, which will include meetings between the Fed and the U.S. Treasury and their international counterparts, in addition to the publication of the IMF’s updated World Economic Outlook.

Canada – A Week of Celestial Events

Two events garnered widespread attention in Canada this week: the solar eclipse and the Bank of Canada’s (BoC) monetary policy meeting. Both have implications for the economy – the former by boosting demand for astro-tourism, the latter by capping demand for almost everything else. As widely anticipated, the Bank held its policy rate at 5%, while comments from Governor Macklem indicated that a rate cut is “within the realm of possibilities” at the June meeting. This had no major impact on the market expectations, where a full rate cut remains priced for the July meeting.

Several takeaways emerged from the Monetary Policy Report – a fresh set of forecasts, accompanying the BoC’s announcement. Namely, the near-term GDP forecast was upgraded reflecting higher population growth and some recovery in consumer spending. Despite the upgrade to the growth outlook, the BoC marked down its inflation forecast by two tenths of a percentage point and now expects its measure of core inflation to reach 2.2% by year-end. In his speech following the announcement, Governor Macklem maintained a cautious tone, stating he would rather err on the side of over-tightening policy to avoid any setbacks in lowering inflation.

Another ‘celestial’ announcement was a 25-basis point (bp) increase in the estimated neutral rate – the policy rate consistent with the economy operating at its full capacity with stable inflation. The Bank justified this increase by citing a higher global neutral rate (using the U.S. as a proxy) and “key Canadian domestic factors” like growth in total hours worked and a younger population of savers. Simply put, the Bank signaled the end point of its upcoming easing cycle will likely be a bit higher than previously thought.

While hard to quantify, an increase in neutral rate likely had only a marginal effect on long-term rates this week. A stronger gravitational pull was exerted by the sharp rise in U.S. Treasury yields following another higher-than-expected inflation reading which resulted in one of the largest weekly moves in yields over the past two years (Chart 1).

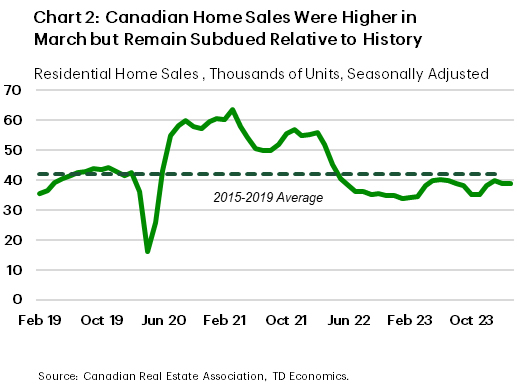

This backup in yields casts a shadow over the Canadian housing market. On the one hand, existing home sales for March were up 0.5% on the month, and, according to CREA, new listings for April are tracking stronger, which could support higher sales activity this month. On the other hand, sales remain below their historical average while higher bond yields will exert additional pressure on affordability, signaling a period of slower activity in the months ahead (Chart 2).

From that perspective, today’s release of the government’s housing plan is timely. Based on Chrystia Freeland’s speech, the government will be increasing the Home Buyers Plan withdrawal limit from $35k to $60k and lifting amortization for insured mortgages from 25 to 30 years for newly built homes and first-time buyers. Our initial assessment suggests that these measures will have a limited impact on the housing market but stay tuned for our comprehensive analysis of the Federal Government Budget next week.