Markets

The Japanese yen slid dramatically on Friday as the Asian island was heading towards a long weekend. USD/JPY soared from 155.65 to 158.44 in the wake of another JPY disappointing BoJ meeting. It contrasted with Fed policy needing to be restrictive for longer. The latter was once again obvious from higher than expected March PCE deflators, despite them triggering a minor uptick in core bonds which resulted in net daily changes of 4-5 bps lower at the long end of the curve. Some in the market were bracing for an even higher outcome after the Q1 PCE publication a day earlier. The dollar was generally in a very good place, gaining against almost every one of the G10 peers. EUR/USD retreated from an intraday high of 1.075 to just south of 1.07. DXY tried but failed to recapture 106. The greenback was unhindered by an outright bullish market sentiment that drove stocks up to 2% higher in the US (Nasdaq).

Japanese markets are closed tor Showa Day today but the JPY bears do not take a day off. The sell-off continues with low volume circumstances amplifying a sharp USD/JPY upswing that went beyond 160 for an umpteenth 34y high. That was followed by a violent countermove bringing the pair 5 JPY down to an intraday low of 155. USD/JPY currently trades in the 156.3 region. Japan’s currency chief Kanda didn’t want to comment when asked about these sharp moves in an interview shortly after. But they have “FX intervention” written all over it. Doing it today gives them an advantage because less liquidity works in both ways of course. Currency interventions, as the past has shown as well, usually don’t have a long-lasting market impact. We suspect it won’t be different this time around. For now the JPY strengthening move against the dollar does have knock-on effects in other pairs too. EUR/USD rebounded to 1.0726 and GBP/USD (cable) to 1.254. The Japanese currency will grab most of the market attention today along with the publication of some national inflation readings (Germany, Spain, Belgium) in the run-up to the European figure tomorrow. But that’s only part of a heavy economic calendar this week. EMU Q1 GDP numbers are also scheduled for release while the US readies for the April ISMs, the JOLTS and labour market report, the US Treasury’s quarterly refunding announcement and the FOMC meeting. We believe the combination should draw a firm bottom below core bond yields with the long end of the curve being most vulnerable for some additional losses. The US dollar may regain momentum when the JPY effect wears off eventually. The EUR/USD YtD low of 1.0601 remains the key reference.

News & Views

Rating agency Fitch affirmed the Bulgarian BBB rating with a positive outlook. The potential for a higher credit rating reflects the prospects for euro adoption which would lead to a further improvement in external metrics. Despite the euro adoption process being delayed beyond January 2025 and renewed political uncertainty (snap election in June is sixth parliamentary vote in just over three years), Fitch considers that there is broad political commitment locally and at the EU level to euro adoption. Bulgaria is on track to meet all euro-adoption nominal criteria (public finances, interest rate and exchange rate) apart from price stability criterion. Harmonised inflation (HICP) was 3.1% in March 2024, above the EU27 rate of 2.6%. Fitch expects inflation to continue to ease, albeit more slowly. HICP is set to average 3.3% in 2024 and 2.9% in 2025. GDP growth would accelerate from 1.8% last year to 2.4% this year and 3.1% in 2025. Bulgaria holds a similar BBB rating with positive outlook at S&P and a one-notch better Baa1 rating at Moody’s (stable outlook).

Scottish First Minister Yousaf (SNP) is preparing to quit after he decided that he won’t survive a confidence vote according to The Sunday Times. Yousaf last week decided to end his party’s power-sharing deal with the Greens as it has “served its purpose”. The decision came after the government scrapped a plan to cut carbon emissions by 75% by 2030 after concluding it was unachievable. The SNP want to run a minority government but no longer with Yousaf as PM as the opposition Conservatives tabled a vote of no-confidence in him.

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut and has broad backing. EMU disinflation will continue in April and bring headline CPI (temporarily) at/below the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets come to terms with that, pushing yields up.

US 10y yield

The March dot plot contained several hawkish elements including a symbolically higher neutral rate. In our view they set the stage for a later (September at the earliest, likely December) start of a possibly shallower cutting cycle. Upcoming CPI readings (through base effects) and resilient eco data should confirm this. US yields continue their uptrend across the maturity spectrum, setting fresh YTD highs.

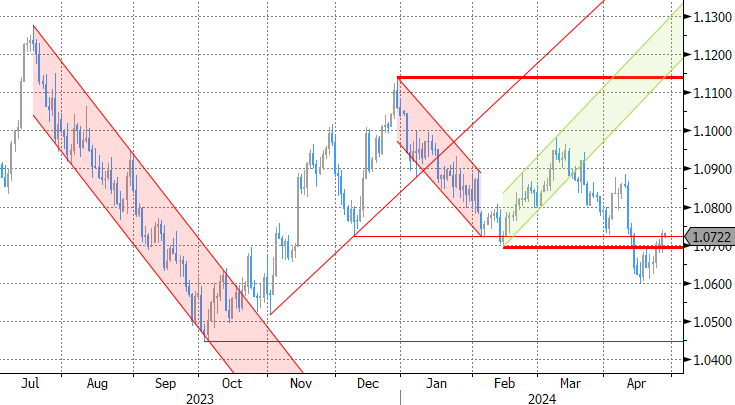

EUR/USD

Economic divergence (US > EMU) and a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead pulled EUR/USD towards the YTD low at 1.0695. Stronger-than-expected US March inflation figures forced a technical break, opening the path to last year’s low at 1.0494.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 – 0.8768 trading range serving as the first real technical reference.

{kind=link}