- It has been a rollercoaster period for Fed rate cut expectations

- Sticky US inflation is keeping the market on its toes

- Numerous Fed speakers this week; market sensitive to hawkish comments

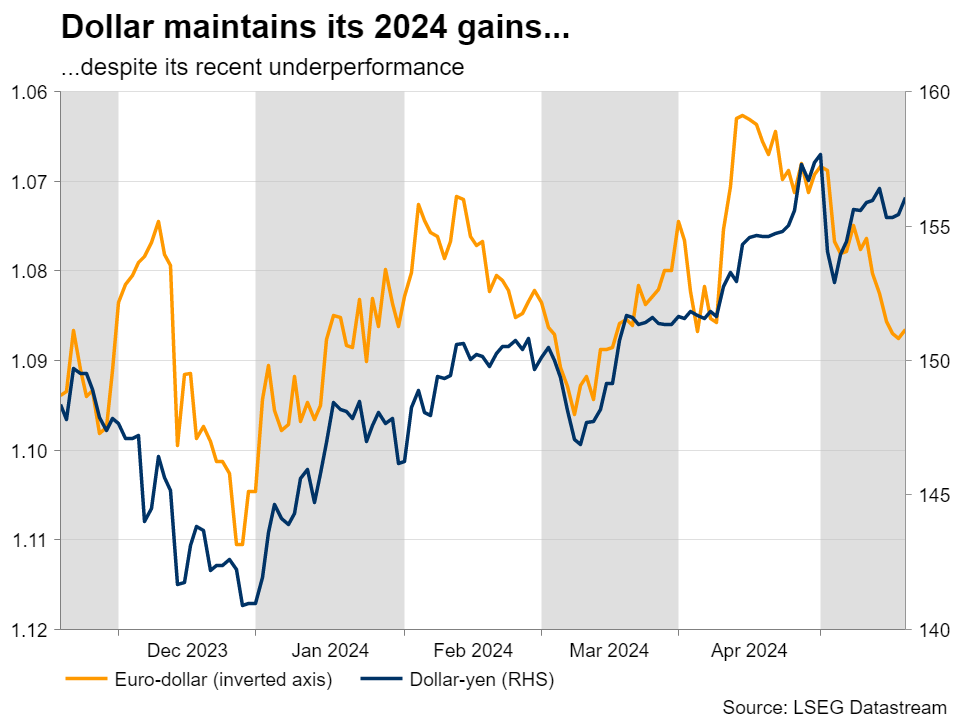

- Dollar’s 2024 gains dented despite divergent monetary policy outlooks

The year started with the market firmly believing that the Fed would deliver six rate cuts during 2024 on the back of an aggressive slowdown in inflation, which has not materialized up to now. Developments elsewhere, in particular the numerous geopolitical events, have greatly affected market sentiment during 2024, but US inflation remains a dominant force of market movements, causing a rethinking of the Fed’s outlook every time there is a surprise in store.

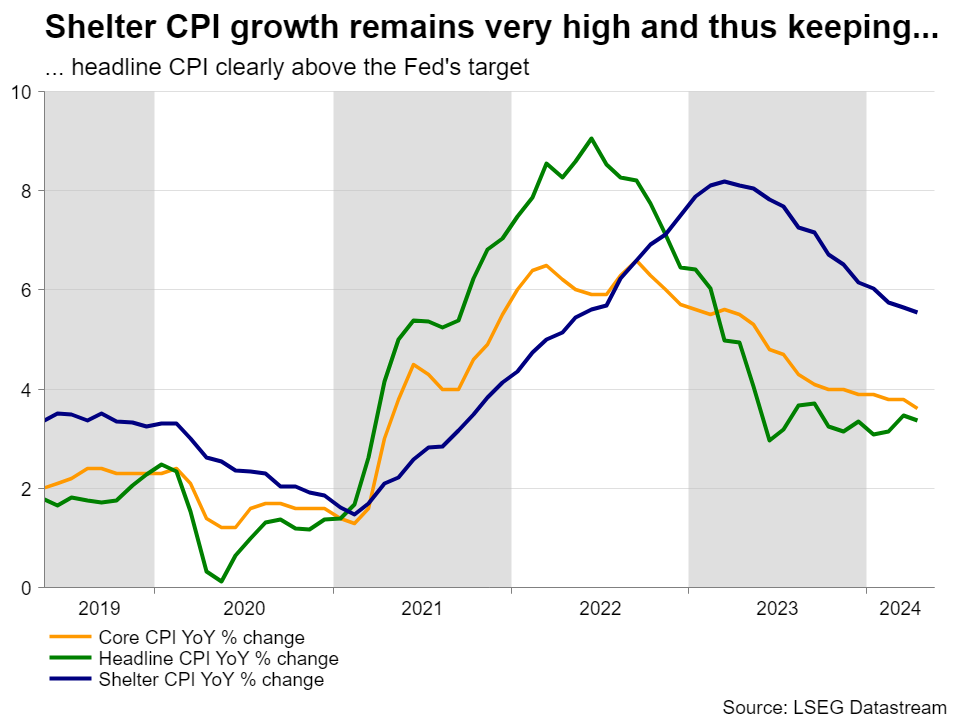

The last CPI report showed a small easing in price pressures

US headline inflation for April printed at 3.4% yoy, slightly below the March figure, but remains in the middle of its recent 3.0-3.7% range. The stickiness in CPI prints during 2024 has thrown a spanner in the works for the Fed doves, despite the continued easing seen in the core index that excludes food and energy prices, albeit at a very gradual pace. Potent consumer spending appears to be one of the key reasons for these elevated inflation prints, despite the relatively high Fed rates.

The most recent inflation reports indicate that both food and energy prices have eased considerably over the past few months. However, services, and in particular shelter, continue to generate strong price increases. The April report showed an annual growth of 5.5% in shelter costs, below the 2022 high of an 8.2% increase, but still far above the Fed’s inflation target.

Market looks for almost two rate cuts

The market is acknowledging the stickier inflation as it is currently pricing in only 42bps of easing for 2024 – one full 25bps rate cut and a 68% probability for a second rate move of equal size. Interestingly, the key investment houses are split between September and December for the timing of the first Fed cut.

Until the next set of key US data releases, rate cut expectations could be affected by Fed members’ rhetoric. A minimum of 15 Fed members are scheduled to speak this week, including most of the 2024 voters.

An analysis of almost 30 public appearances by Fed speakers since May 1 reveals an overwhelming support for patience as both the hawks and the doves accept the lack of progress on the inflation front. The recent economic growth moderation has been welcomed but the main message is that more time is needed to measure the domestic demand’s strength, via the retail sales data, and hence evaluate the firms’ ability to keep raising their prices.

Hawks more aggressive; minutes could confirm their stance

Importantly, the hawks have become more concerned lately about the restrictiveness of the current Fed rates forcing Chairman Powell to denounce any thoughts of rate hikes at this juncture. Repeated hawkish commentary this week could prompt a market reaction, although chances for a rate hike are currently perceived as extremely low.

Interestingly, on Wednesday the minutes from the May 1 Fed meeting will be published. This release is slightly out-of-date considering the newsflow since then, but it will be an interesting read to further understand the Fed’s reaction function and how high the bar was set for a rate hike.

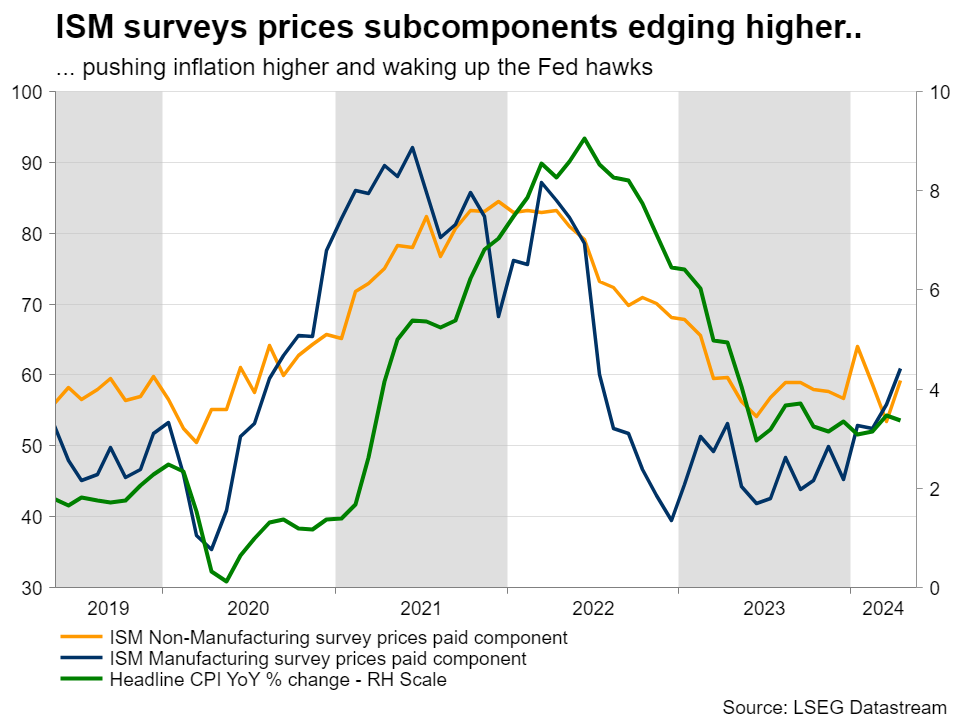

A true test of both the market’s understanding and the hawks’ determination could come on Thursday with the preliminary PMI manufacturing and services surveys for the month of May. With both the ISM surveys dropping below 50 in April, but their prices paid sub-indicators recording decent jumps, it would be extremely interesting to judge if the current US soft patch has legs or if the hawks could be justified to maintain their recent rhetoric.

Dollar remains dominant despite the recent pullback

The US dollar has been outperforming its main counterparts in 2024. It is currently 1.5% higher against the euro and a massive 10% versus the ailing yen. Despite the aggressive scaling back of Fed rate cut expectations, the US economy remains the strongest one among the developed nations, which along with certain geopolitically-induced risk-off episodes, is keeping the demand strong for the greenback.

Until the June 12 meeting, the numerous Fed speakers, the US labour market data and the June CPI report are bound to keep the market on its toes. Barring a considerable worsening in US data, the dollar could remain supported especially as the ECB is ready to commence its easing spree and the Bank of England could enjoy a rare drop in inflation.

{kind=link}