Stronger clothing prices, and a surprise inclusion of health insurance premium increases, offset the suppression of power bills by Tasmanian electricity rebates.

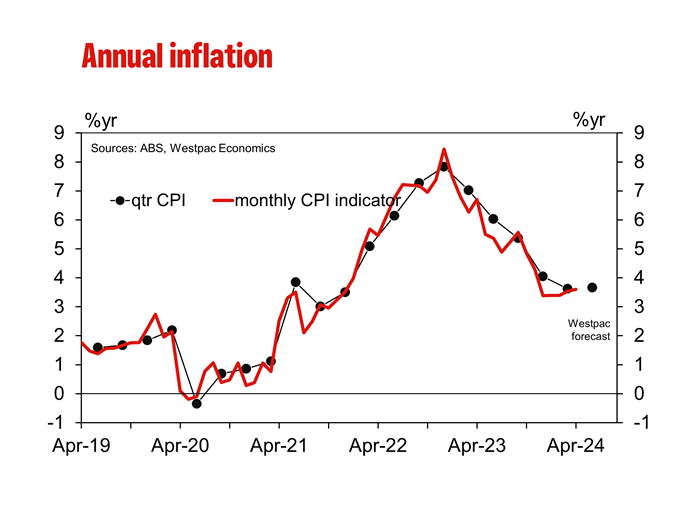

The Monthly CPI Indicator gained 3.6% in the year to April compared to 3.5%yr in March and 3.4%yr in both February and January.

The April print was slightly stronger than Westpac’s forecast of 3.5%, the market median was 3.4%yr, but this variation appears to be due to rounding and revisions as the reported increase in the month was 0.7%, in line with Westpac’s preview in our Weekly. However, it is worth noting a tension in the forecast which suggest an upside surprise in the underlying fundamentals for inflation.

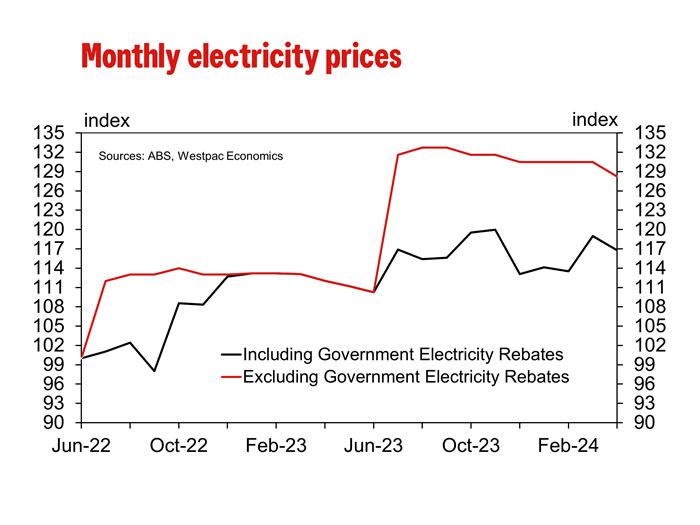

Holding inflation back in the month was a 1.9% fall in electricity prices as there was the second instalment of the Energy Bill Relief Fund for concession and newly eligible households in TAS. We had expected prices to rise again following the 4.8% increase in March. The ABS is now reporting a 9% gap between the electricity bills being paid and the actual price of electricity before the rebate.

In the recent budget the Federal Government introduced universal power bill rebates for the 2024/2025 year of $75 per quarter, on top of which the Queensland government announced a $1,000 lump sum rebate. However, neither will start until July so there is still room for a snap higher in electricity prices over the next few months as the gap between bills paid and the underlying price of electricity closes. It is also worth noting the electricity prices excluding rebates have fallen 3.4% since peaking in September 2023.

Offsetting the fall in electricity prices and holding up inflation in April was stronger than expected durable goods prices. Clothing & footwear rose 4.0% in the month (we had pencilled in -0.2%) and outside of garments for men & women, this group is surveyed in the first month of the quarter and so it will go straight into our quarterly estimate.

There was also an unexpected 2% increase in medical & hospital services in April. We were aware of the announced increase in health insurance premium but as this series has historically been surveyed in the last month of the quarter, we had not expected it to appear until the June survey. As the increase in premium applied from April 1, the ABS decided to incorporate in the April survey. The ABS still notes that this series is a quarterly survey in the release.

Taken at face value, as the April Monthly CPI Indicator came as broadly as expected you could assume that it would not have an impact on our June quarter CPI forecast. However, the quarterly CPI is not a simple average of the Monthly CPI Indicator and history has taught us that a simple ‘face value’ estimate can be misleading. As noted earlier, the quarterly surveyed clothing & footwear prices were stronger than expected which will see an upwards revision to these components in our June quarter CPI forecast. Assuming all else is held constant, this would suggest an upward revision to our forecast. This risk can also be illustrated with the annual pace on the Monthly Indicator Tradables measure lifting from 0.5%yr to 1.1%yr, the fastest pace since November 2023.

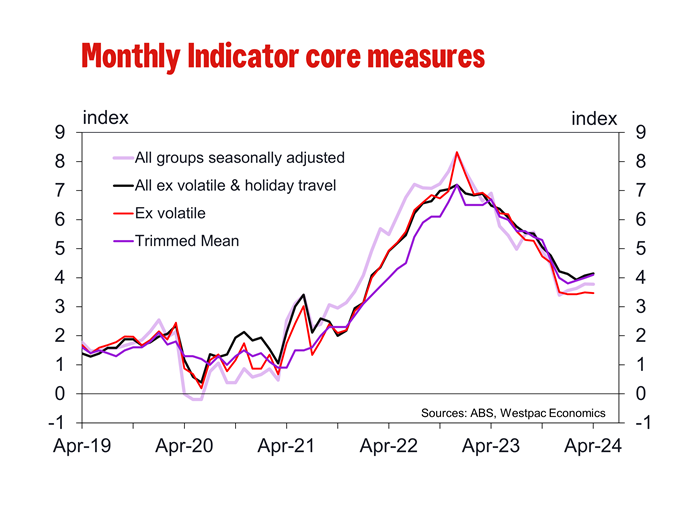

For the various core measures, seasonally adjusted excluding volatile items & holiday travel lifted from 4.1%yr to 4.2%yr while the Trimmed Mean measure lifted from 4.0%yr to 4.1%yr, the fastest pace since the 4.6%yr reported in November 2023.

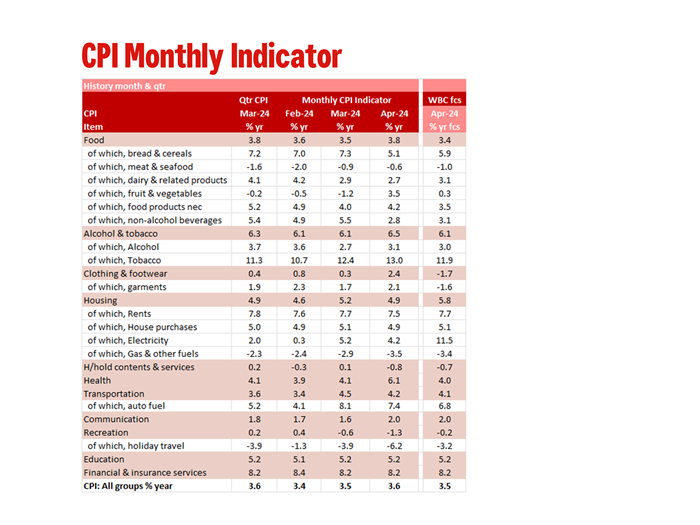

In more detail the difference to our monthly forecast was:

- Food was a touch softer at 0.5% compared to 0.1% forecast.

- Alcohol & tobacco was on the stronger side, 0.6% vs. 0.2% forecast, due to a stronger-than-expected tobacco price increase.

- Clothing & footwear was stronger at 4.0% vs. 0.2% forecast due to strong price gains for both male and female garments as well as the quarterly clothing & footwear surveys.

- Housing was softer than expected at 0.1% vs. 0.9% forecast, due to Tasmanian rebates suppressing electricity prices. Rents were close to expectations (0.5% vs. 0.7% forecast) while dwellings came in softer lifting just 0.3% vs. 0.4% forecast. It is somewhat surprising we are still yet to see a meaningful lift in dwelling price inflation.

- Household contents & services were close to expectations at 0.6% vs. 0.7% forecast.

- Health was surprising lifting 2.0% vs. 0.0% forecast as we had not expected the increase in health insurance premiums till the June survey. Recreation was also on the softer side 2.0% vs. 3.1% forecast) with a smaller 4.6% rise in holiday travel (we had expected an 8% lift).

{kind=link}