- Snap elections in France spur panic in euro and French stock market

- Doubts about Germany’s coalition add to euro’s woes

- Is political instability about to become a persistent risk for the euro?

Europe steers to the right

Financial markets don’t usually pay so much attention to elections for the European Parliament, as national governments are often seen as the bigger force in setting EU policy. However, whilst the outcome of far-right parties faring well was widely predicted, it is the fallout in France, and potentially in Germany too, that is having ripple effects in the markets.

President Macron’s Ensemble coalition, made up of liberal-centrist parties, received just 14.6% of the votes, coming second to Marie Le Pen’s National Rally party, which won more than twice that share, gaining 31.4%. When combined with the votes for the smaller Reconquete Party, the share of the far right rises to just under 37%.

Snap elections: brave or foolish?

This must have been enough to ring alarm bells for Emmanuell Macron, who decided on Monday to call a snap election, catching his political opponents as well as his own party completely by surprise. Yet, having lost his parliamentary majority in the previous legislative elections in 2022, a snap election is a huge gamble, as his alliance runs the risk of losing even more seats.

Although it’s unlikely that Le Pen’s party will win as many votes in national elections, it is currently ahead in the polls, with Macron’s Ensemble third behind the left-wing alliance. If Macron’s gamble doesn’t pay off and his alliance comes out weaker, the likely outcome is a “cohabitation” whereby parties not affiliated to the president would form the government. The pick of prime minister would still be up to the president in such a scenario, but Macron would have no choice but to appoint someone from rival parties, making him a lame duck president less than halfway through his term.

Running out of allies

Complicating matters for Macron is the chaos within the centre-right Les Republicains party – the most obvious choice to partner with to keep the far-right out of power. Its leader has called for an alliance with the far-right National Rally to the horror of other senior figures within Les Republicains. While in another setback, left-wing parties made up of socialists, communists and the Greens have just announced a new pact, further diminishing Macron’s options for possible coalition partners.

With France in danger of plunging into political turmoil, the elections couldn’t have come at a worse time for Europe. Germany – the other half of the Franco-German political engine that drives EU integration – is also on the brink of a political crisis. Chancellor Olaf Scholz’s Social Democrats came third in the European elections, with the coalition hanging by a thread.

Change might not be a bad thing

Germany’s coalition government, which also includes the Greens and the Free Democrats, has been under strain for some time, while relations between Macron and Scholz have been uneasy at best. Thus, political change in either Paris or Berlin, or both, might not necessarily turn out to be so disastrous.

Yes, the threat of far-right parties gaining more influence in both France and Germany doesn’t bode well for further European integration. But it’s worth remembering that Italy is currently being run by a far-right government and that hasn’t led to radical policies that would spook the markets. If anything, Georgia Meloni’s government has brought some rare stability in Rome. Moreover, despite the upsets, centrists held their ground in the European Parliament.

Euro skids, but not much

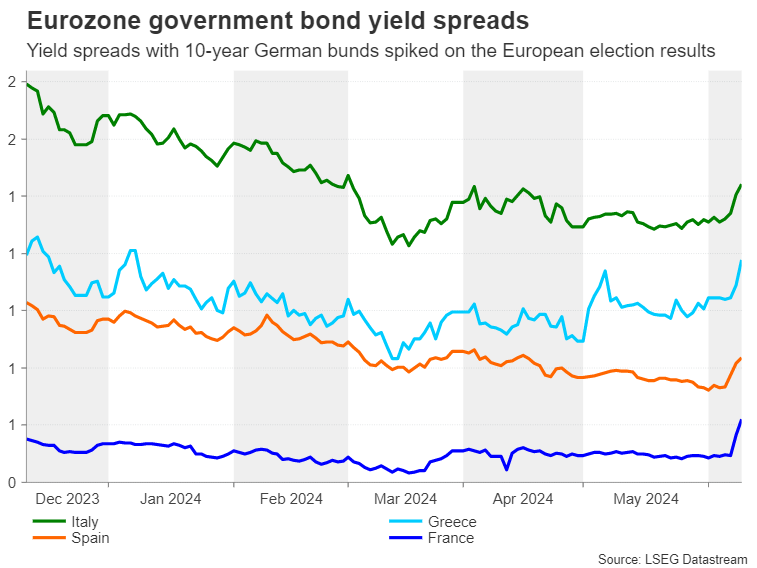

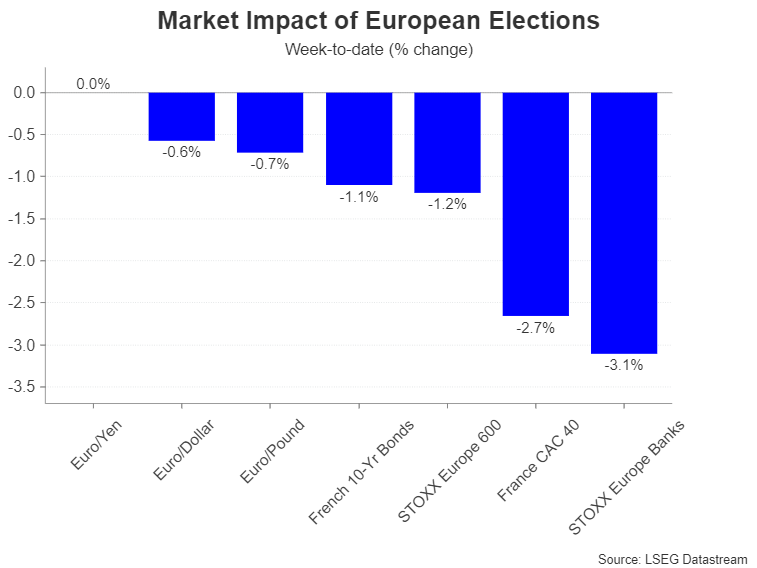

However, traders aren’t so convinced, and French government bond yields have surged in the aftermath of the election fallout. Italian yields also spiked, though the moves in safe-haven German bunds were more muted. The euro, meanwhile, has come under significant pressure, but its weekly losses are less than 1% and look exaggerated as it came after Friday’s slump on the back of the strong US jobs report.

A bumpy road ahead amid uncertainties

The answer is probably no. But markets may have woken up to the possibility of a permanent shift in Europe’s political landscape and that brings with it a number of uncertainties over the longer term. In France, the prospect of a Le Pen government is already causing angst for local traders, with the CAC 40 index taking the brunt of the selloff. Investors are worried about the risk to the economy from interventionist policies should far-right parties win power.

Nevertheless, with the debate to start soon on whether to reappoint Ursula von der Leyen as President of the EU Commission and the ongoing uncertainty about the monetary policy paths in both the US and the Eurozone, the summer period may be a bumpy one for the euro.

{kind=link}