Here are the latest developments in global markets:

FOREX: The dollar edged slightly higher versus a basket of currencies but was still trading not far above a two-week low hit yesterday. The US currency continued gaining versus the yen, being supported by rising Treasury yields.

STOCKS: The Nikkei 225 closed down by 0.1% and the Topix added 0.1% to renew its 26-year high. The Hang Seng was up by 0.5%. Euro Stoxx 50 futures were marginally lower at 0726 GMT, while Dow, S&P 500 and Nasdaq 100 equivalents were all up, though close to being flat.

COMMODITIES: WTI and Brent crude were both little changed, trading at $58.12 and $64.55 per barrel. Gold was also not much changed, trading around two-week high levels at $1,265.67 an ounce.

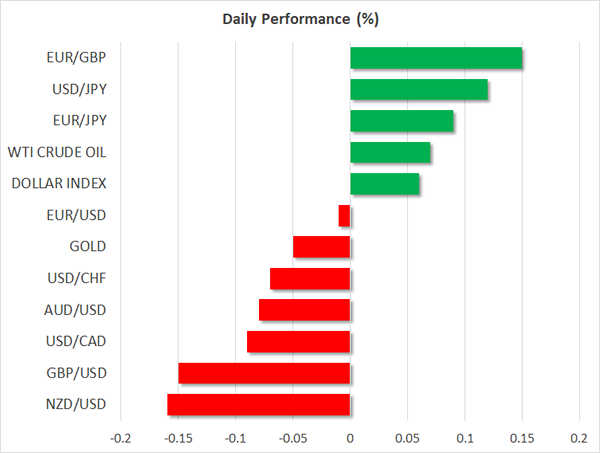

Major movers: Dollar on the rise versus yen, helped by yields and dovish stance by BoJ; euro at four-week high relative to sterling and at highest since late 2015 versus yen

The dollar index was slightly up after losing ground the three preceding days. The index was at 93.38. This comes after yesterday’s final vote in favor of tax reforms by the House of Representatives. What remains now before it passes into law, is for President Trump to sign the bill.

Dollar/yen was 0.1% up and on its third straight day of advancing. It was last at 113.53, not far below a more than one-week high recorded earlier in the day. The greenback was boosted by rising yields. Indicatively, the 10-year US Treasury yield was last at around its highest since late March at 2.49%. Meanwhile, the BoJ completed its meeting on monetary policy during the Asian session, with policymakers keeping policy unchanged as expected. A press conference by governor Kuroda followed, during which dollar/yen was moving higher as he appeared in no hurry to tighten policy.

Euro/dollar was roughly flat at 1.1868, trading around two-week high levels. Eurozone’s common currency posted hefty gains this week, being boosted by rising German bond yields. Euro/pound was trading at 0.8886, this being around four-week high levels. Euro/yen was 0.1% up at 134.77, just a shade below its highest since late 2015 hit earlier today.

Pound/dollar was 0.15% down at 1.3352 as the EU is being seen as taking a hard stance on Brexit. The antipodeans were also losing ground versus the greenback, with aussie/dollar being down by 0.1% at 0.7660 and kiwi/dollar trading lower by 0.15% and being marginally below the 0.70 handle.

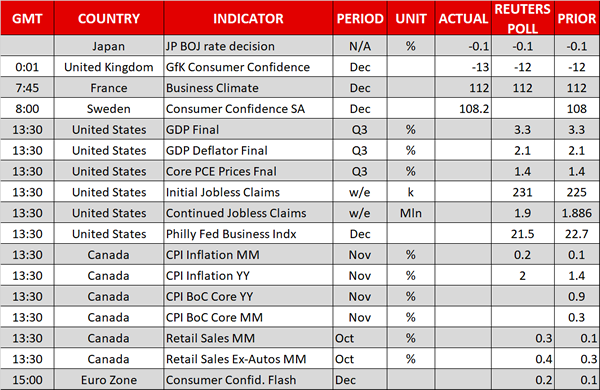

Day ahead: Canadian inflation could reach BoC target

The economic calendar will be pretty busy on Thursday, with the US, Canada and the Eurozone delivering reports ahead of the Christmas holiday.

Out of the US, final Q3 GDP growth figures are due at 1330 GMT, with analysts predicting a growth rate of 3.3% on an annualized basis as was previously reported. This would constitute the highest expansion the economy has experienced in a year.

Meanwhile, final US core PCE prices are expected to stand in line with previous estimates at 1.4% y/y in the third quarter.

US initial jobless claims are anticipated to climb by 6,000 in the week ending December 15, while Philadelphia’s Fed manufacturing index is forecasted to decline by 0.8 points to 21.5 in December.

The main focus, however, would be in Canada where data on inflation and retail sales are scheduled to be published at 1330 GMT, whilst the ADP Canadian employment report will give some evidence on the number of people employed in nonfarm sectors.

According to forecasts, the headline CPI is anticipated to rise by 0.6 percentage points to 2.0% y/y in November, hitting a nine-month high and touching the BoC’s inflation target.

Monthly retail sales are said to expand by 0.3% in October compared to 0.1% seen in September. If true, this would be the highest mark posted since July. The core measure, which excludes volatile items is projected to inch up by 0.1 percentage points to 0.4%.

Elsewhere, flash readings on Eurozone’s consumer confidence will be available at 1500 GMT, with analysts awaiting the measure to edge down to zero in December after reaching positive levels of 0.1 in the previous month for the first time since 2001. Meanwhile, Catalonia will be holding regional elections today. It will be interesting to see whether pro-independence forces come out stronger or weaker.

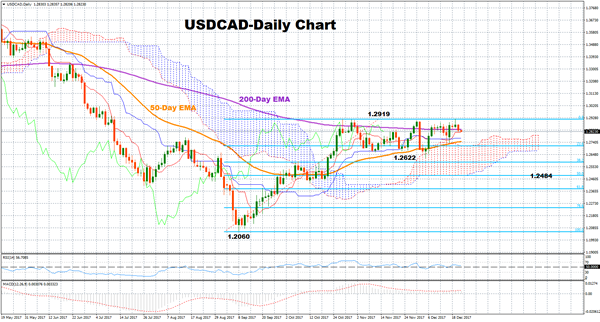

Technical Analysis: USDCAD within a range, looks neutral in short-term

USDCAD has been moving between 1.2622 and 1.2915 since the end of October. The RSI, which has been moving sideways in recent days, is projecting a neutral picture in the short-term.

Better-than-expected data out of Canada later today are expected to push the pair lower. In such a case, support could be met at around the 50-day exponential moving average at 1.2746. The lower bound of the range at 1.2622 could also act as support, while steeper declines could target the 50% Fibonacci at 1.2484 of the upleg from 1.2060 to 1.2919.

If on the other hand Canadian releases disappoint, prices could find room to rise back to the top of the range at 1.2919, with the area around this level potentially acting as a barrier to the upside. Further increases might also shift the focus towards the 1.30-1.31 key area.

{kind=link}