Sunrise Market Commentary

- Rates: Inflation (expectations) on the rise

Market-based inflation expectations resumed their march higher and so did US yields. The curve significantly bear steepened. Today’s eco calendar contains the US labour market report. The bar for average hourly earnings is rather low. Beating it could resume current trends while a disappointment could trigger some short covering ahead of the weekend. - Currencies: Dollar struggles despite sharp rise in US yields

Yesterday, the dollar hardly profited from a new up-leg in US yields. EUR/USD even holds near its multi-year peak. The yen declined slightly this morning as the BOJ stepped up its easing efforts. Later today, focus for USD trading turns to the US payrolls. In the current environment, there is no guarantee that strong payrolls will trigger a sustained USD rebound

The Sunrise Headlines

- US stock markets ended nearly unchanged, outperforming Europe yesterday. The Nasdaq slightly underperformed (-0.35%) ahead of big US tech earnings. Asian risk sentiment is negative overnight with Korea underperforming.

- The BOJ offered to buy an unlimited amount of bonds at a fixed rate for the first time since July, backing up its repeated stance that actions by its peers and global yields wouldn’t dictate its policy.

- Stronger iPhone prices and hints that Apple could return more than half of its $285 bn in cash to shareholders eased concerns among investors, even as the company gave a disappointing revenue outlook for the current quarter.

- Google parent Alphabet confounded WS with news of a big jump in costs in the final quarter of last year, along with fresh evidence of increasing pressure on profit margins as it becomes more dependent on mobile advertising.

- The White House will likely give Congress approval to make public a secret Republican memo alleging FBI bias against President Trump in its Russia probe, an official said, as tensions over the disputed document gripped Washington.

- The EU will hold out the prospect of membership to western Balkan countries (6) by 2025 as it seeks to breathe new life into enlargement, strengthen controls on migration, and counter Russian influence in the volatile region.

- Today’s eco calendar contains US payrolls, the unemployment rate and average hourly earnings. Fed Kaplan, Fed Williams and ECB Coeuré are scheduled to speak.

Currencies: Dollar Struggles Despite Sharp Rise In US Yields

Dollar struggles despite sharp rise in US yields

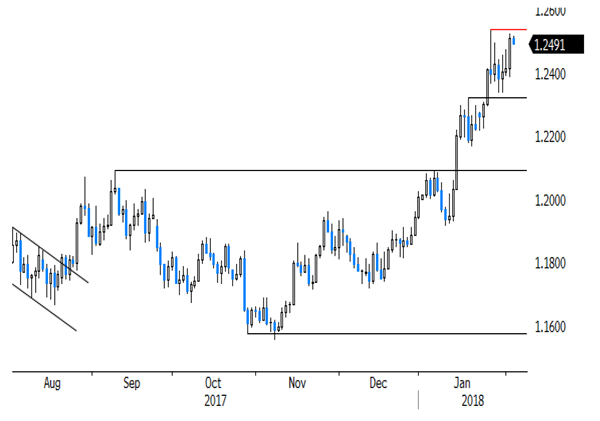

Wednesday’s positive Fed guidance didn’t help the dollar much. EUR/USD returned temporary to ST support below 1.24, but the test was rejected. The US manufacturing ISM was strong. The US bond sell-off resumed after the report, but the dollar hardly profited. USD/JPY held up fairly well despite rising nervousness on the equity markets. The rise in USD yields didn’t stop the EUR/USD rebound. The pair returned north of 1.25, but a break of the EUR/USD 1.2537 top didn’t occur.

Overnight, Asian equities are mostly trading in the red. Mixed results from US tech giants and the bond sell-off are weighing. The BOJ offered to buy an unlimited amount of 10-yr bonds at a fixed rate (0.11%) signaling a disconnect from the trend to global policy/interest rate normalization. The yen declined slightly. USD/JPY trades at 109.75 and EUR/JPY north of 137. The euro is holding strong across the board. EUR/USD hovers near the 1.25 big figure.

Today, the focus is on the US Payrolls. Net job growth is expected at 180.000. The unemployment rate is expected unchanged at 4.1% and AHE at 0.2% M/M and 2.6% Y/Y (from 2.5%). A good report might solidify the recent uptrend in US yields. Of late that didn’t help USD even if it widened interest rate differentials. The disconnect of the dollar from interest rate trends and eco data won’t last forever, but for now the established trends are strong. Short-term, even a strong payrolls report is no guarantee for a USD rebound. We look out whether the rise in yields triggers a rise in volatility of risky assets even if the dollar apparently hasn’t that much of a safe haven role to play. So, we need a technical sign (or new market theme) before concluding that the sharp repositioning ran its course. That sign is currently not available. Technical picture: the dollar decline slowed end of last week, but no meaningful rebound occurred, especially not against the euro. EUR/USD 1.2537/98 is the first topside resistance. A break would signal more trouble for the USD short term. EUR/USD 1.2323/35 is a minor support A break below 1.2165 would call off the ST downside alert (for the dollar).

Yesterday, a dip in EUR/GBP was reversed after a disappointing UK manufacturing ISM. The intraday rebound of EUR/USD also reinforced the intraday rise of EUR/GBP. Today, The UK construction PMI is expected little changed at 52.0. We expect sterling to stay in the 0.8690/0.8833 consolidation pattern.

EUR/USD near multi-year top going into US payrolls report

{kind=link}