Here are the latest developments in global markets:

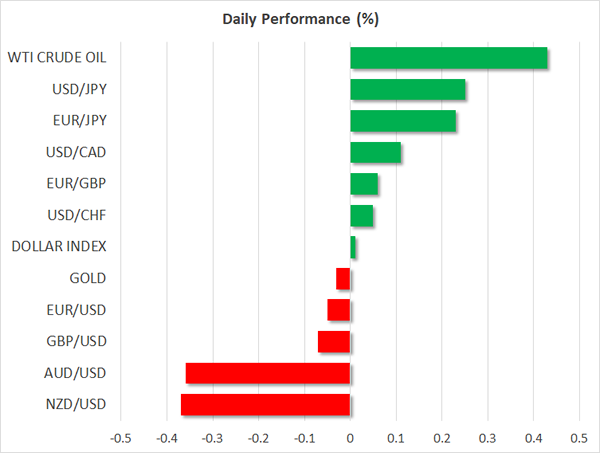

FOREX: The dollar index was practically unchanged on Friday ahead of the US employment data, after it previously posted notable losses on Thursday. The yen tumbled against its major peers, weighed on by the BoJ’s regular bond-buying operations, which pushed Japanese bond yields lower.

STOCKS: Japanese markets retreated despite the overnight tumble in the yen. The Nikkei fell 0.9%, while the Topix pulled back 0.3%. In Hong Kong, the Hang Seng was in the green, though not by much. In Europe, futures tracking the Euro STOXX 50 were in negative territory. Finally, in the US, the major indices were mixed yesterday. The Dow Jones closed marginally higher, though the S&P 500 and the Nasdaq Composite both finished lower. The recent underperformance of US equities is being attributed to the continued surge in US Treasury yields. As yields rise, bonds begin to offer a higher and “safer” return for investors, thereby curbing demand for stocks. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently in negative territory.

COMMODITIES: Oil was one of the biggest movers on Friday, with WTI and Brent crude surging 0.5% and 0.4% respectively. Today, oil traders are likely to focus on the Baker Hughes US oil rig count, in order to gauge whether US producers have continued to increase their output in the face of elevated prices. Meanwhile, gold prices were little changed, with the precious metal last trading near $1348 per ounce.

Major movers: Dollar softens ahead of employment data

The greenback tumbled once more during the European trading session on Thursday, with no clear catalyst behind the move. Interestingly enough, the dollar retreated even despite a spectacular surge in US Treasury yields, something that usually supports the currency. The 10-year yield rose to a fresh high – it’s highest since April 2014 – last trading near 2.79%, while 30-year yields broke above the 3% milestone, last trading around 3.03%. The biggest gainers from the tumble in the US currency were the euro and sterling.

Today, dollar-traders will turn their eyes to the US employment report for January. Since the US economy is already considered to be near full employment conditions, investors are likely to focus more on wage growth as opposed to jobs added, as they try to gauge whether inflationary pressures are beginning to intensify.

Despite the softer tone in the greenback, dollar/yen actually rose 0.2% on Friday, underpinned by the BoJ’s bond-buying operations. The Bank stepped into the market and offered to buy “unlimited” amounts of bonds in order to curb Japanese yields from rising. Such actions are typical under the Bank’s QQE with yield-curve control framework. The BoJ has committed to keeping 10-year yields near 0%, so every time yields approach 0.1%, it steps into the market to push them back down.

Elsewhere, the antipodean currencies retreated, with both aussie/dollar and kiwi/dollar declining nearly 0.4%

Day ahead: US NFP report dominates attention; UK releases construction PMI; eurozone producer prices due

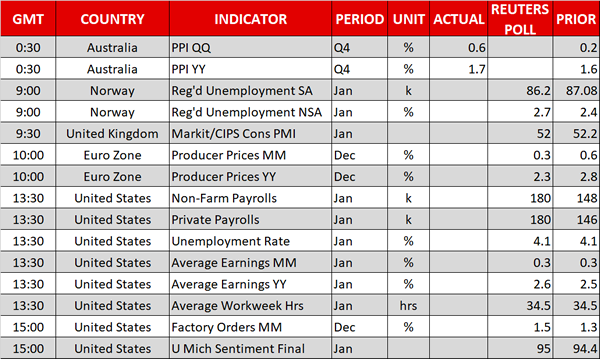

The UK will see the release of the Markit/CIPS construction PMI for the month of January at 0930 GMT. The measure is projected to decline for the second straight month, but at 52.0 – should expectations materialize – it would remain in growth territory (above 50). Yesterday’s manufacturing PMI for the same month surprised to the downside, leading to sterling weakness. The respective PMI figure for the much more important for the UK economy services sector will be released next week (Monday).

Eurozone data on December producer prices will be made public at 1000 GMT. Prices are expected to reflect a slowdown on both a monthly and an annual basis.

Without a doubt the highlight of the day – and the release having the capacity to spur sharp movements in dollar pairs – will be the US nonfarm payrolls report for the month of January due at 1330 GMT. The number of positions added to the economy is anticipated to have bounced up after some weakness in December on the back of poor weather conditions; forecasters project the addition of 180k jobs versus 148k in December. The unemployment rate is expected to remain at the 17-year low of 4.1%, but yet again investors’ focus is likely to turn on wage growth. Average hourly earnings are expected to grow at a monthly rate of 0.3%, the same as in December, while on an annual basis they’re projected to expand by 2.6% – this compares to 2.5% in December. Growth in wages has the potential to alter the outlook for inflation and thus affect the Federal Reserve’s tightening cycle.

Later in the day (at 1500 GMT), the US will see the release of data pertaining to December’s factory orders, as well as the University of Michigan’s final reading on consumer sentiment for the month of January.

In energy markets, the US Baker Hughes oil rig count is due at 1800 GMT.

Policymakers making appearances include ECB executive board member Benoit Coeure who will be speaking at the conference titled “Deepening of EMU” at 1000 GMT, and Fed Bank of Dallas President Robert Kaplan – a non-voting FOMC member in 2018 – who will be participating in a Q&A session before the Teacher Retirement System of Texas Annual Conference at 1830 GMT. Fed Bank of San Francisco President John Williams – a voting FOMC member in 2018 – will be talking about the US economy before the Financial Women of San Francisco at 2030 GMT.

Energy companies Chevron and Exxon Mobil and pharma firm Merck & Co. are among firms releasing quarterly results on Friday. All three will be releasing their reports before the US market open.

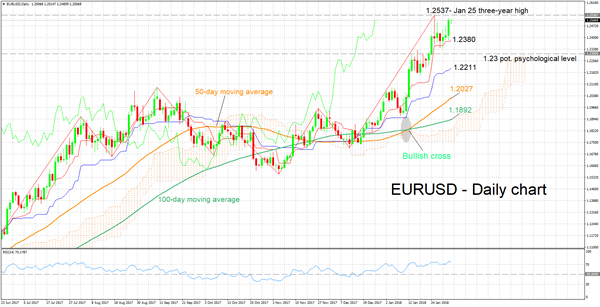

Technical Analysis: EURUSD trades near highest since late 2014; RSI overbought

EURUSD is trading not far below its highest since December 2014 of 1.2537 hit on January 25. Technical indicators are projecting a bullish picture in the short-term: the Tenkan- and Kijun-sen lines are positively aligned and the RSI is well into bullish territory (above 50) and continues rising. The fact that the RSI has crossed above the 70 overbought level though, could be a sign that a short-term pullback in not to be ruled out.

A disappointing US jobs report – especially on the wage growth front – is likely to see the pair rising. In this case, last week’s three-year high of 1.2537 might act as immediate resistance. An upside break, which is not that unlikely in this scenario given that price action is currently taking place close to the aforementioned high, would shift focus to the area around 1.26 as another barrier to the upside; 1.26 being a potential psychological level.

On the downside and in case of a strong NFP report, EURUSD could find support around the current level of the Tenkan-sen at 1.2380. The area around this point also encapsulates 1.24, this being another mark that may be of psychological significance.

{kind=link}