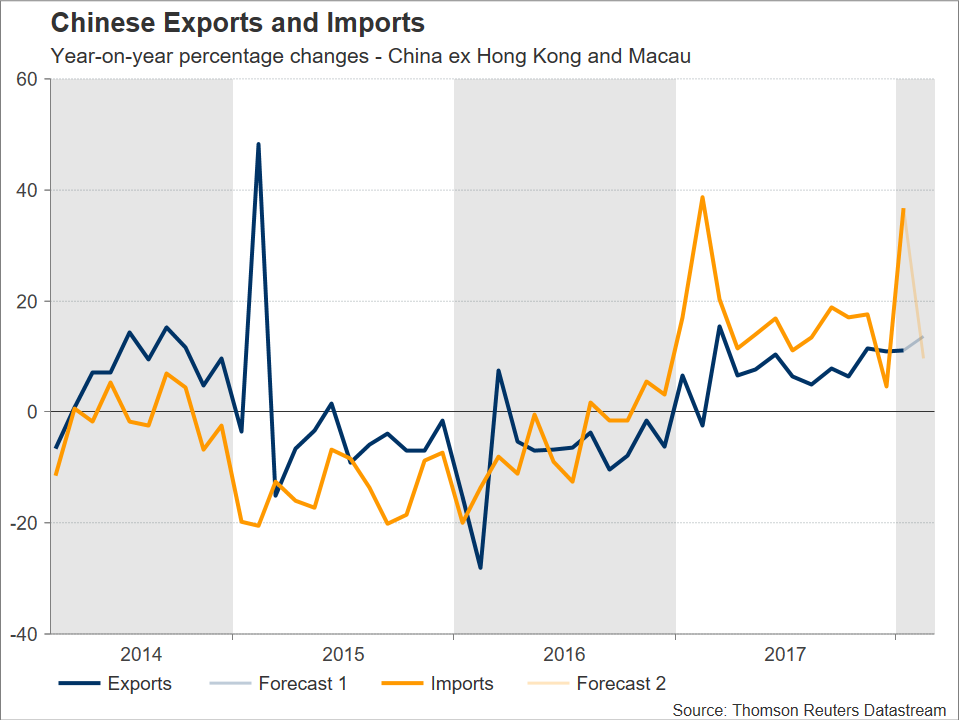

Chinese trade data for the month of February are due on Thursday – the figures lack a fixed time of release – with both exports and imports projected to grow solidly. The readings on producer and consumer prices for the month of February scheduled for release on Friday at 0130 GMT will also be in focus out of the nation. On an annual basis, PPI growth is expected to ease, while CPI expansion is anticipated to accelerate.

Year-on-year, exports and imports are expected to have grown by 13.6% and 9.7% respectively during the second month of the year. These compare to January’s respective increases of 11.1% and 36.9%. Should exports come in line with projections, they would expand at their highest pace since March 2017. February’s trade surplus is anticipated to stand at $0.6 billion from around $20.4bn in January. It deserves mention though, that comparisons are not as useful is this instance as the data were distorted by seasonal factors relating to the timing of Lunar New Year celebrations which took place in mid-February this year. For example, January’s surge in imports was attributed to an inventory buildup ahead of New Year festivities, with higher commodity prices also playing a role. A better approach to gauge the robustness of the figures might be to look at overall first quarter data.

Following Trump’s recent actions, China said it will host US officials for a new round of talks on trade issues. However, reports suggest that the White House is also considering clamping down on Chinese investments in the US and instituting tariffs on a wide range of its imports from the country. Should tensions escalate out of control, with the two countries merely engaging in tit-for-tat retaliatory actions, then the outlook for Chinese exports would look much grimmer than at present.

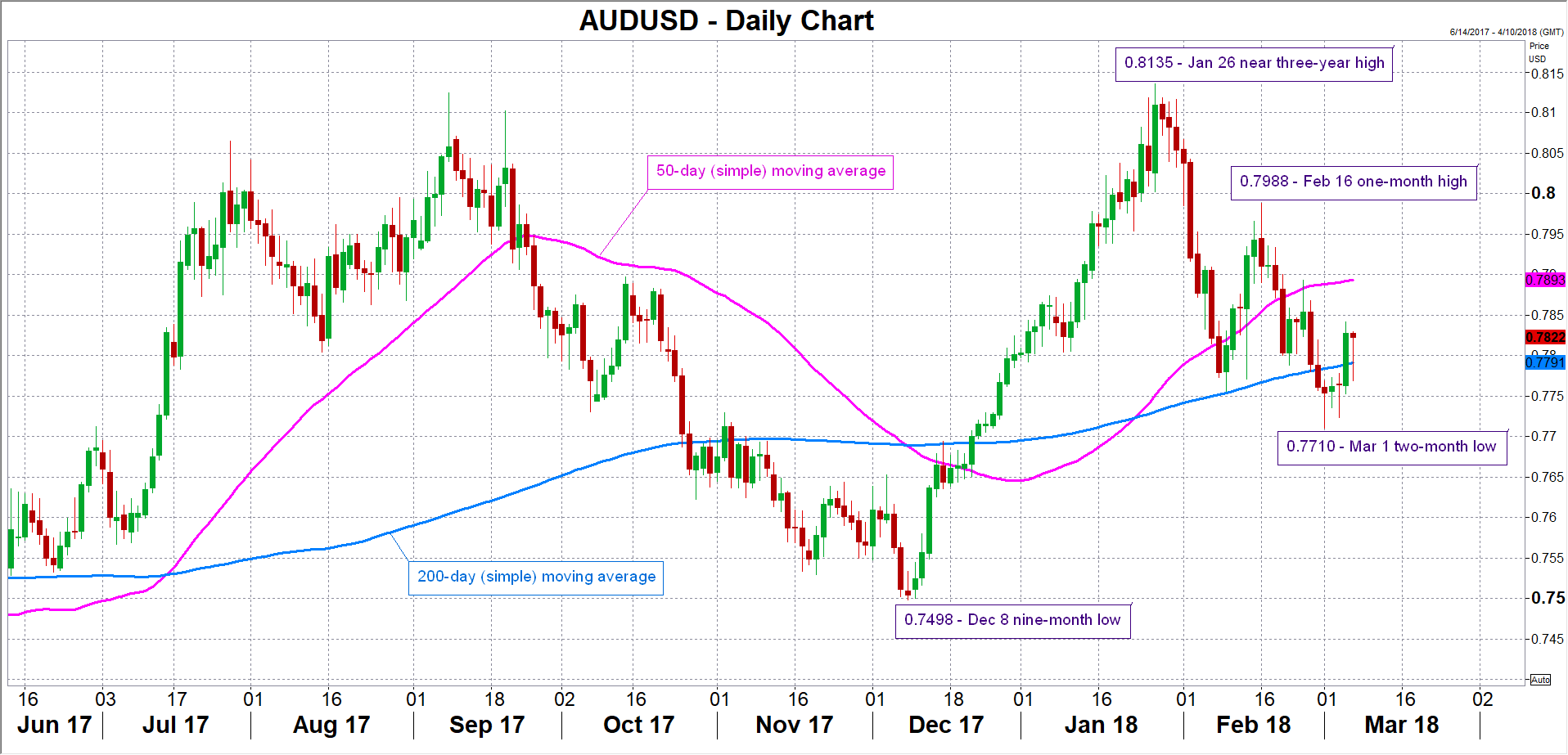

Dollar/yuan is down by around 3% year-to-date, but beyond the Chinese currency, the Australian currency will also be in focus as trade numbers go public. The aussie is viewed as a liquid proxy for China’s economy due to the two nations’ close economic ties, as China is Australia’s largest export and import partner.

Upbeat data could lead to long aussie/dollar positions, with price advances potentially meeting resistance around the current level of the 50-day moving average at 0.7893. The area around this level was subject to congestion in the past and also encapsulates the 0.79 handle that may hold psychological significance. Stronger bullish movement would turn the attention to the one-month high of 0.7988 that was recorded on February 16.

If the figures disappoint though, aussie/dollar might post losses. Should this scenario materialize, support could come around the 200-day MA at 0.7791. Notice that this includes the 0.78 level that could also be of psychological importance. Further below, the two-month low of 0.7710 from March 1 would be eyed next.

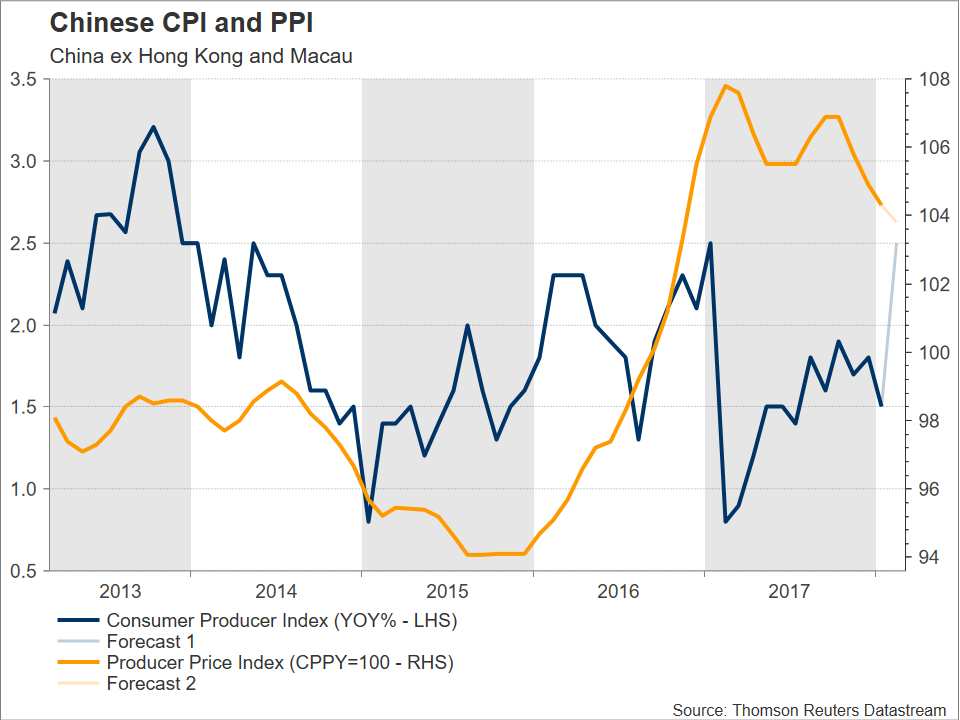

Other important data out of China will pertain to February’s producer and consumer price inflation, both due out on Friday at 1330 GMT. PPI growth is projected to decline to 3.8% y/y (versus 4.3% in January), easing for the fourth straight month. If it comes as expected, its rate of growth would be at its lowest since November 2016, with government efforts to reduce environmental pollution and curb risks in the financial system likely weighing on factory prices. CPI growth, on the other hand, is forecast to increase to 2.5% y/y (versus 1.5% in January), at a pace last seen in January 2017.

{kind=link}